Europe TIC Market for Food and Beverage Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (in-house, outsourced), by Service Type (testing, inspection, certification), by Industry Vertical (convenience food solutions, dairy solutions, animal feed & pet food solutions, honey solutions, fruits and vegetable solutions, meat & seafood solutions, others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9205 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 144 |

Europe TIC Market for Food and Beverage Industry Overview

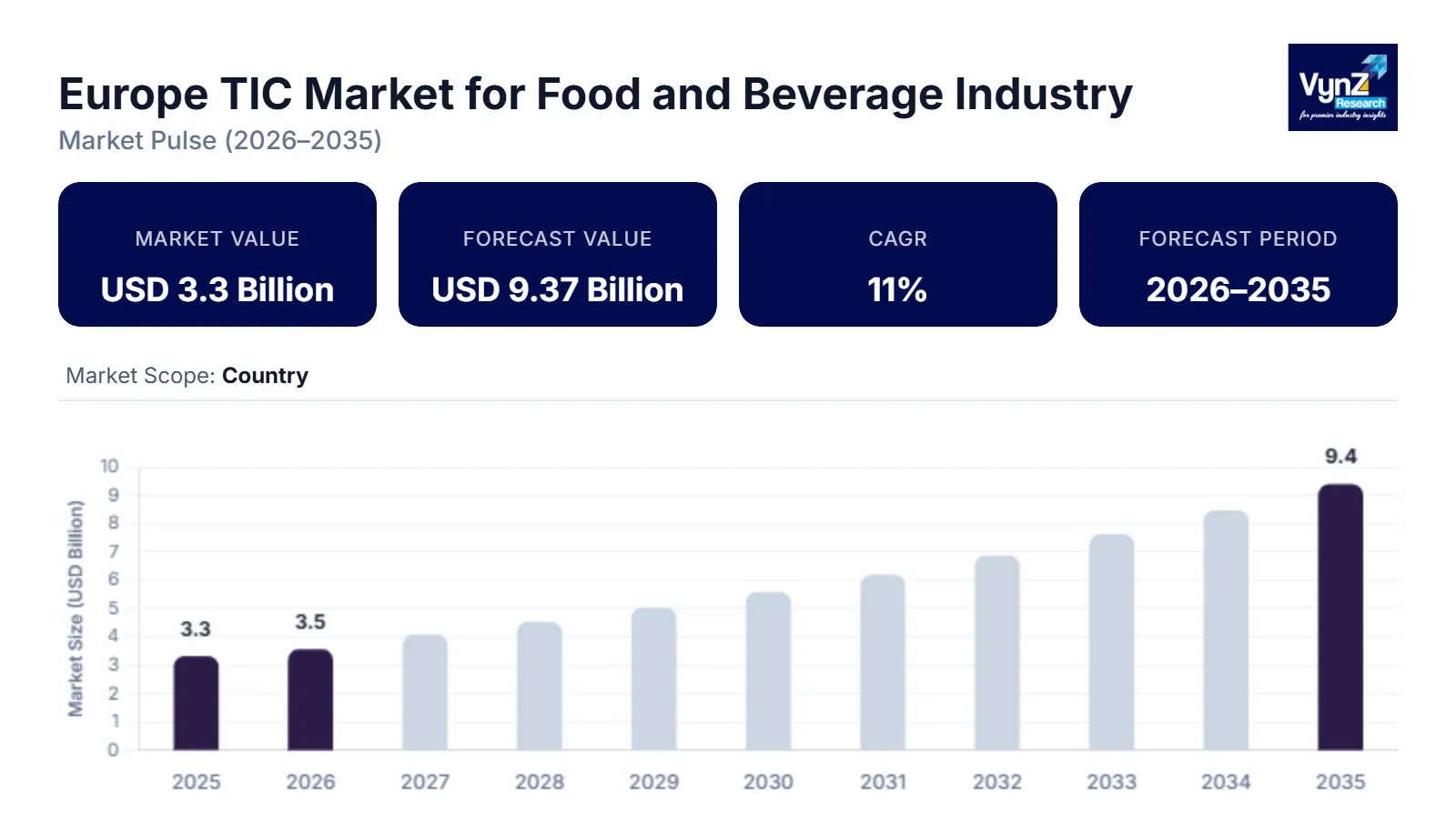

The Europe testing, inspection, and certification market for the food and beverage industry, which was valued at approximately USD 3.3 billion in 2025 and is estimated to reach around USD 3.55 billion in 2026, is projected to reach approximately USD 9.37 billion by 2035, expanding at a CAGR of about 11% during the forecast period from 2026 to 2035.

The market growth results from two main factors, which include food production and processing operations that must meet increasing regulatory compliance needs and consumers who want safe and high-quality food products along with technological improvements in testing and certification systems. The European Food Safety Authority (EFSA) reports that member states must implement strict safety and quality standards, which increases their need for dependable testing and inspection services.

The market expansion receives support from government activities that promote food safety and hygiene through their implementation of EU-wide food control programs and national standards enforcement frameworks. Digital traceability, laboratory automation and quality assurance process investments help industry players achieve better operational efficiency. The major markets that include Germany, France and Italy experience increased demand through supportive measures and foodborne disease prevention awareness while the rest of the demand comes from unspecified regions.

Europe TIC Market for Food and Beverage Industry Dynamics

Market Trends

The industry in Europe undergoes fundamental changes which result from two main factors, namely, unified regulations and increased public understanding of food safety standards. The European Union established a comprehensive food safety system which requires complete tracking of food products from their initial production stage until they reach the retail market and determines which situations require immediate public health warnings. According to sources from the European Commission and the European Food Safety Authority, EU citizens have become more involved in matters related to food safety, which increased their demand for viewing test results and inspection records and certification documents, as they became more aware of contaminants and pesticide residues and microbiological hazards. The industry now requires enterprises to use automated analytics and digital traceability platforms and improved quality control systems, which will transform market competition through these new technologies.

Growth Drivers

The market grows primarily because regulatory agencies demand full compliance with safety and hygiene and quality standards which EU institutions enforce through their safety rules. The European Union established General Food Law and its corresponding regulations to create the legal framework which enables systematic testing and certification processes to operate throughout the member states. Public investment in food safety infrastructure and expanded laboratory capacity further accelerates market expansion by enabling operators to meet complex compliance requirements and international export standards. Consumers today expect to receive safe and high-quality food products, which requires inspection and certification services to become industry-standard for all vital product categories.

Market Restraints / Challenges

The market shows excellent potential for growth; however, the industry faces major obstacles which will limit its capacity to expand. The high operational costs of advanced analytical technologies and specialized equipment create entry barriers for smaller independent laboratories, which particularly affects less developed regions because their operational budgets do not allow for such expenses. Multinational service providers need to obtain multiple accreditations and develop localized expertise to handle the distinct sampling protocols and analytical standards of each EU member state because the regulatory framework requires them to follow different jurisdictional rules. Economic volatility causes these elements to impact market penetration rates and profitability levels during times of financial instability.

Market Opportunities

The market generates strong growth opportunities through digital transformation and innovation, which companies gain by implementing rapid testing technologies and automated laboratory systems that boost productivity while shortening the time needed for results. Integrated digital solution companies which provide traceability and risk assessment and predictive analytics solutions will secure additional business from major food manufacturers and export-driven companies. Food safety policy objectives established by the EU drive growing investments in sustainability and quality assurance methods, which enable TIC service providers to broaden their service offerings while forming enduring partnerships with regulatory bodies and industry partners to sustain market demands throughout the entire forecast period.

Europe TIC Market for Food and Beverage Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.3 Billion |

|

Revenue Forecast in 2035 |

USD 9.37 Billion |

|

Growth Rate |

11% |

|

Segments Covered in the Report |

By Sourcing Type, By Service Type, By Industry Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, France, Italy, Spain, United-Kingdom and Rest of Europe |

|

Key Companies |

ALS Limited, Bureau Veritas, DEKRA SE, DNV Group, Eurofins Scientific, Intertek Group plc, Mérieux NutriSciences, SGS SA, TÜV Rheinland, TÜV SÜD |

|

Customization |

Available upon request |

Europe TIC Market for Food and Beverage Industry Segmentation

By Sourcing Type

The market reached its peak in 2025 through in-house sourcing which generated about 58% of total market revenue. The market maintains its leading position because large food manufacturers operate their own laboratories which enable them to conduct continuous quality checks while satisfying EU food safety standards through their quick testing process. The European Commission regulatory frameworks together with European Food Safety Authority guidance create the conditions which require real-time compliance. The systems enable organizations in high-volume production areas to build their internal capabilities.

The period from 2026 to 2035 will see outsourced sourcing experience its highest expansion with a projected CAGR of 11.5%. The demand for third-party laboratory testing services has increased among small and medium enterprises which need specialized testing solutions that help them save costs. The adoption of accredited external service providers results from the growing complexities in food safety standards and the requirements for cross-border trade thus enabling businesses to maintain their ongoing segment development.

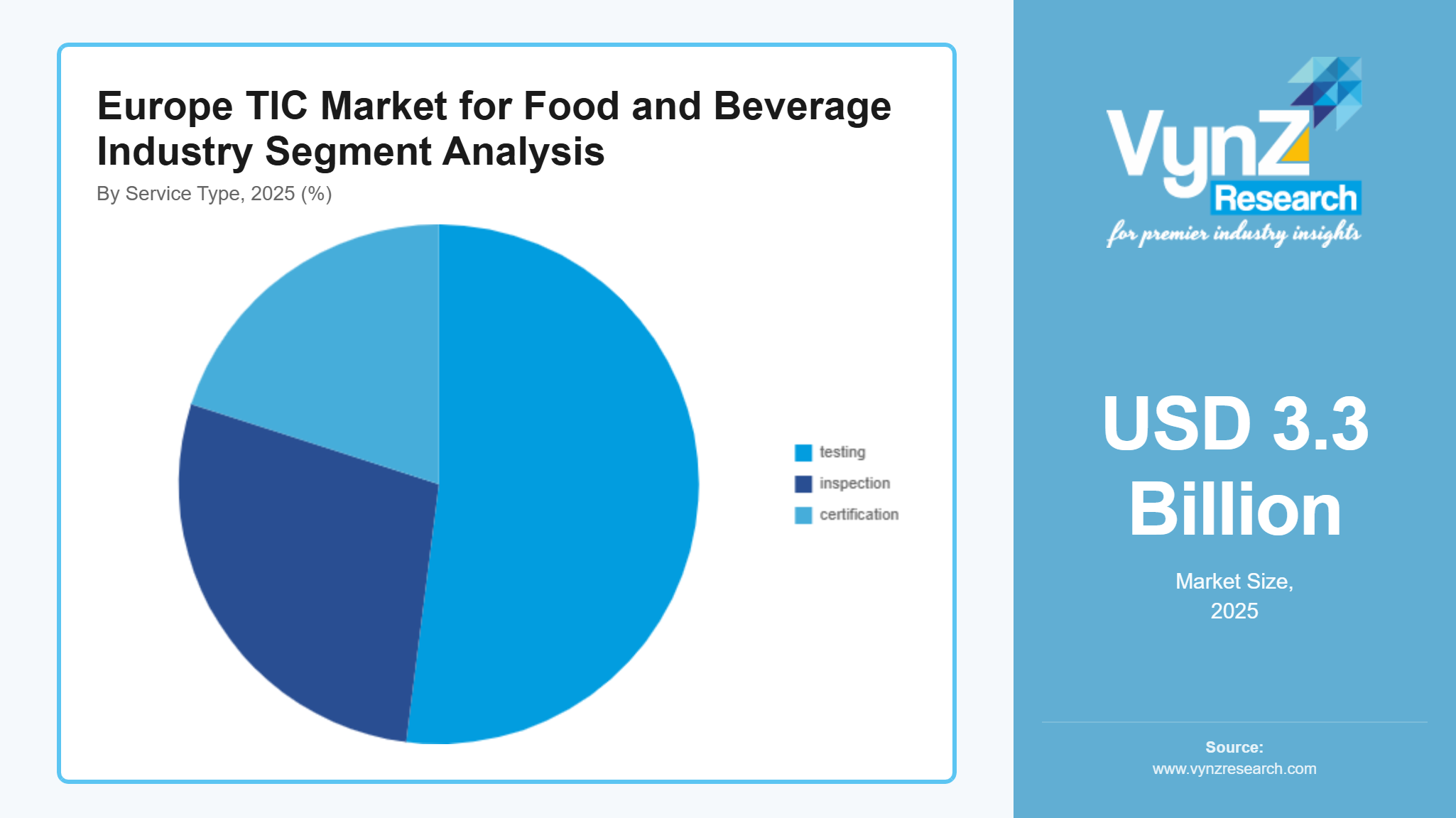

By Service Type

The testing services segment dominated the market in 2025 by providing about 52% of total market revenue. The market maintains its leading position because analytical testing enables contamination detection and product quality assessment while fulfilling EU compliance requirements. The European Commission food safety regulations together with EFSA risk assessment guidelines drive the ongoing demand for laboratory testing services which are needed in dairy products, meat products, and processed food items.

The inspection services market will achieve the highest growth rate during 2026 to 2035 with a projected CAGR of 11.3%. The supply chains experience expansion because organizations are starting to use automated inspection systems and digital monitoring solutions and tools for real-time quality assessment. The certification services market is experiencing continuous growth because international trade and premium food sectors require standardized labeling and export compliance and consumer trust.

By Industry Vertical

The dairy solutions market achieved its highest value in 2025 through its 27% contribution to overall revenue. The EU food safety authorities require strict microbiological testing and regular quality audits which result in high consumption levels that maintain the dominant position of this sector. The need for TIC services in this segment gets reinforced by government-supported monitoring programs which create hygiene regulations that control dairy processing facilities.

The meat and seafood solutions market will experience the fastest growth with a projected CAGR of 11.6% during the period from 2026 to 2035. The demand for advanced testing technologies which can detect pathogens has risen because of stringent traceability requirements and growing contamination concerns and increasing adoption of these technologies. The ongoing growth in processed food demand along with regulatory compliance requirements across various product categories is driving the development of convenience food products and fruits and vegetables and animal feed.

Regional Insights

Germany

Germany resulted in 24% of this sector in 2025. Berlin, Hamburg, and Munich serve as key industrial centers that create strong demand for testing, inspection, and certification services which apply to dairy, meat, and processed food products. The European Commission works with the European Food Safety Authority to establish regulatory enforcement which results in organizations adopting TIC services.

Food safety programs that receive government funding together with rising consumer demand for product traceability and quality control are driving investments into modern laboratory setups and digital testing equipment. The market achieves better performance results because of the implementation of automated inspection systems and certified platforms which operate throughout the nation.

France

France held an 18% market share in 2025 because of its robust agricultural production together with its established food manufacturing facilities and its increasing commitment to product safety and quality assurance. The TIC service market is expanding because cities like Paris, Lyon, and Marseille adopt these services for their dairy and bakery operations and processed food production. Businesses continue to require inspection and certification services because they must follow both EU food safety regulations and national monitoring programs.

Government initiatives that promote food quality standards together with consumer preference for certified and safe food products create conditions that enable investment in testing infrastructure. Regional market growth is experiencing an upward trend because businesses are starting to use digital traceability systems and quality monitoring tools.

Italy

Italy represented 16% market share in 2025 because of its strong export business in packaged food and dairy products and specialty food items. The cities of Milan, Rome and Bologna serve as important centers which handle food production and certification of food quality. European Commission and EFSA guidelines about food safety and contamination risks have created two drives for growth, which include rising regulatory oversight and increase food safety awareness.

Food industry organizations need to implement TIC services because government quality assurance programs and export compliance standards require them to do so. The country experiences market growth because businesses invest in lab upgrades and automated testing systems and certification operations.

Rest of Europe

The rest of Europe including Spain and the United Kingdom captured 20% of the market in 2025. The meat and seafood and convenience food markets in these countries are growing because Madrid, Barcelona, London and Manchester begin using TIC services.

Government-supported food safety initiatives, combined with increasing consumer awareness and demand for certified products, are fostering investments in inspection and testing services. The market gains operational efficiency together with market growth because businesses implement digital compliance systems and automated quality monitoring and traceability platforms. Other European countries not mentioned above control the remaining market share, which supports the overall development of the regional market.

Competitive Landscape / Company Insights

The industry is moderately competitive, with the presence of established global and regional players focusing on service innovation, accreditation expansion, and geographic reach. Companies are increasingly investing in advanced laboratory technologies and digital traceability solutions and automation systems to strengthen their market position. The testing and certification capabilities of organizations in the market must be improved because the European Commission and European Food Safety Authority have established regulatory frameworks and compliance standards which drive organizations to achieve competitive advantages.

Mini Profiles

ALS Limited focuses on laboratory testing, inspection, and certification services, supported by strong global laboratory networks, technical expertise, and consistent service quality across food safety and environmental testing applications.

Bureau Veritas operates in premium and compliance-driven segments, emphasizing quality assurance, regulatory certification, and risk management solutions tailored to food and beverage safety and international trade requirements.

DEKRA SE leverages extensive certification expertise and digital inspection capabilities to expand market presence, supported by strong European regulatory alignment and advanced testing infrastructure across industrial and food safety applications.

DNV Group focuses on assurance, risk management, and certification services, supported by strong technical expertise, global presence, and growing adoption of digital assurance solutions across food supply chains.

Eurofins Scientific operates in specialized and high-precision testing segments, emphasizing advanced laboratory capabilities, scientific innovation, and comprehensive analytical services to ensure food safety, quality compliance, and traceability.

Key Players

- ALS Limited

- Bureau Veritas

- DEKRA SE

- DNV Group

- Eurofins Scientific

- Intertek Group plc

- Mérieux NutriSciences

- SGS SA

- TÜV Rheinland

- TÜV SÜD

Recent Developments

In March 2026, Intertek expanded its sustainability services by certifying hotels under GSTC standards. The company also enhanced its real-time inspection and low-methane emissions testing capabilities.

In January 2026, SGS inaugurated its new global headquarters in Baar, Switzerland, boosting collaboration and innovation. In March 2026, it partnered with Exterra Technologies to integrate modular analytical systems into laboratories.

Throughout 2025–2026, Eurofins developed food safety training programs on microbiology, allergens, and HACCP compliance. These initiatives strengthened its analytical services and regulatory support in Europe.

In May 2026, Mérieux NutriSciences showcased advanced testing solutions at Vitafoods Europe 2026. Earlier in February, it highlighted food and fresh produce quality and compliance at Fruit Logistica 2026.

In 2025, Bureau Veritas transferred parts of its food testing business to Mérieux NutriSciences, expanding lab network reach. The company also strengthened regulatory compliance services through its strategic LEAP portfolio realignment.

Europe TIC Market for Food and Beverage Industry Coverage

Sourcing Type Insight and Forecast 2026 - 2035

- in-house

- outsourced

Service Type Insight and Forecast 2026 - 2035

- testing

- inspection

- certification

Industry Vertical Insight and Forecast 2026 - 2035

- convenience food solutions

- dairy solutions

- animal feed & pet food solutions

- honey solutions

- fruits and vegetable solutions

- meat & seafood solutions

- others

Europe TIC Market for Food and Beverage Industry by Region

- Germany

- By Sourcing Type

- By Service Type

- By Industry Vertical

- U.K.

- By Sourcing Type

- By Service Type

- By Industry Vertical

- France

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Italy

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Spain

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Russia

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Rest of Europe

- By Sourcing Type

- By Service Type

- By Industry Vertical

Table of Contents for Europe TIC Market for Food and Beverage Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Sourcing Type

1.2.2. By

Service Type

1.2.3. By

Industry Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Sourcing Type

5.1.1. in-house

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. outsourced

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. testing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. inspection

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. certification

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. convenience food solutions

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. dairy solutions

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. animal feed & pet food solutions

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. honey solutions

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. fruits and vegetable solutions

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. meat & seafood solutions

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. others

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Sourcing Type

6.2. By

Service Type

6.3. By

Industry Vertical

7. U.K. Market Estimate and Forecast

7.1. By

Sourcing Type

7.2. By

Service Type

7.3. By

Industry Vertical

8. France Market Estimate and Forecast

8.1. By

Sourcing Type

8.2. By

Service Type

8.3. By

Industry Vertical

9. Italy Market Estimate and Forecast

9.1. By

Sourcing Type

9.2. By

Service Type

9.3. By

Industry Vertical

10. Spain Market Estimate and Forecast

10.1. By

Sourcing Type

10.2. By

Service Type

10.3. By

Industry Vertical

11. Russia Market Estimate and Forecast

11.1. By

Sourcing Type

11.2. By

Service Type

11.3. By

Industry Vertical

12. Rest of Europe Market Estimate and Forecast

12.1. By

Sourcing Type

12.2. By

Service Type

12.3. By

Industry Vertical

13. Company Profiles

13.1.

ALS Limited

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Bureau Veritas

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

DEKRA SE

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

DNV Group

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Eurofins Scientific

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Intertek Group plc

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Mérieux NutriSciences

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

SGS SA

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

TÜV Rheinland

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

TÜV SÜD

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe TIC Market for Food and Beverage Industry