Roll-to-Roll Battery Manufacturing Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Battery Type (Lithium-ion batteries, Solid-state batteries, Lithium-sulfur batteries, Others), by Process Type (Electrode coating, Electrode printing, Dry electrode processing, Lamination and assembly), by Application (Electric vehicles, Consumer electronics, Energy storage systems, Industrial applications, Aerospace and defense), by Material Type (Cathode materials, Anode materials, Electrolytes, Separator films), by End User (Automotive manufacturers, Battery manufacturers, Electronics manufacturers, Energy storage system providers, Defense and aerospace organizations)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9206 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 163 |

Roll-to-Roll Battery Manufacturing Market Overview

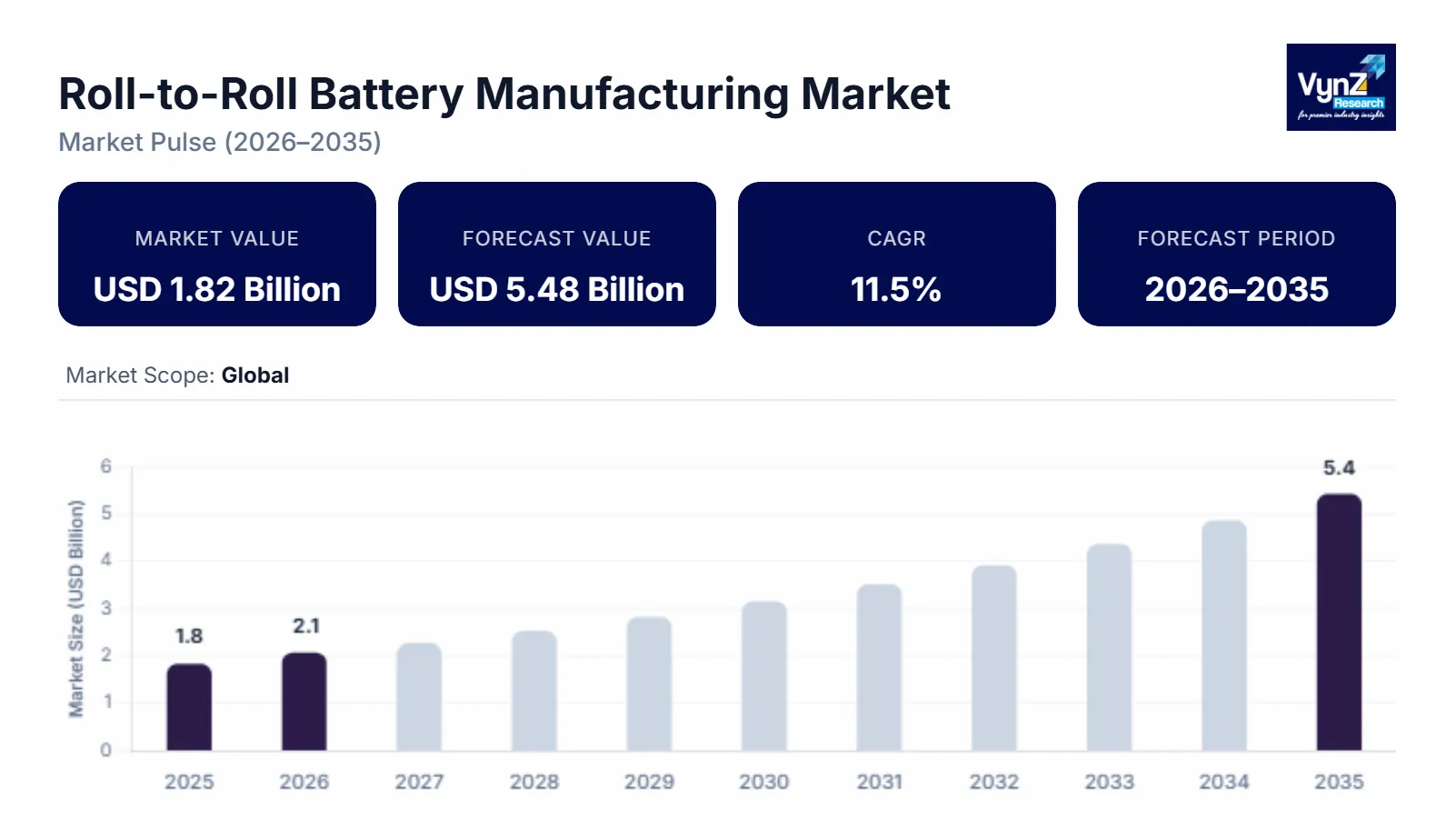

The global roll to roll battery manufacturing market which was valued at approximately USD 1.82 billion in 2025 and is estimated to rise further up to almost USD 2.06 billion by 2026, is projected to reach around USD 5.48 billion by 2035, expanding at a CAGR of about 11.5% during the forecast period from 2026 to 2035.

The market expansion occurs because of three factors which include growing demand for energy storage systems with high efficiency, increasing electric vehicle manufacturing and flexible electronics deployment, and rising use of continuous roll to roll coating and printing technologies. The International Energy Agency reports that worldwide electrification and clean energy storage systems have created permanent market shift which currently drives battery manufacturing technological progress. The market expansion in China, the United States and Germany receive support from two factors which include rising demand for lightweight high-performance batteries in consumer electronics and mobility applications and government investments in advanced battery gigafactories and energy transition programs.

Roll-to-Roll Battery Manufacturing Market Dynamics

Market Trends

The industry shows significant changes which affect both production technology methods and industrial equipment purchasing choices. The market experiences its most important development from manufacturers who now prefer continuous roll to roll electrode coating and printing processes because these techniques deliver better production efficiency, lower material waste and cheaper large scale battery manufacturing costs. The battery value chain now uses advanced automation together with digital manufacturing systems because technological progress and smart factory systems grow rapidly in the market. Manufacturing companies now shift their focus towards integrated production lines and high precision coating systems because these two factors create a new competitive environment in the manufacturing industry.

Growth Drivers

The market expands because electric vehicle demand leads to sustained automotive and energy storage requirements. The market expansion receives additional momentum from rising investments in battery gigafactories and large-scale manufacturing facilities. The consumer electronics market together with renewable energy storage systems experiences rapid growth which drives system adoption. Automotive manufacturers and energy providers together with electronics companies will continue to drive strong demand for advanced battery manufacturing solutions until the end of the forecast period because they focus on developing energy with cost effective and scalable production systems. Government backed clean energy transition initiatives and national electric mobility programs are further strengthening long term market growth.

Market Restraints / Challenges

The market shows positive growth potential yet certain obstacles may hinder its expansion. The high capital investment requirements together with production equipment costs create challenges for all manufacturers but they particularly affect emerging companies and small-scale producers. The operational challenges for manufacturers exist because their supply chains depend on essential raw materials which include lithium, cobalt and nickel. The process of importing materials together with importing specialized manufacturing equipment creates cost variations which lead to delivery delays and limits production capacity. Government energy agencies together with international supply chain assessments identify raw material price fluctuations as a major risk factor which affects battery manufacturing production scheduling and price stability across the entire industry.

Market Opportunities

The market offers attractive growth potential through upcoming solid state and flexible battery production technologies which rely on current energy storage developments and the increasing need for lightweight power solutions. Companies which provide roll to roll manufacturing systems that deliver both high performance and scalable production capabilities will gain market share through sales to electric vehicle manufacturers, consumer electronics producers and renewable energy storage developers. The development of domestic manufacturing ecosystems together with clean energy infrastructure investments creates an opportunity for sustainable growth through the establishment of battery production facilities and the expansion of gigafactories. The market will enhance its production capacity through automation, smart manufacturing systems and digital process optimization which improve yield rates. The government supported electrification programs together with energy storage deployment initiatives drive higher adoption rates in important industrial areas.

Global Roll-to-Roll Battery Manufacturing Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.82 Billion |

|

Revenue Forecast in 2035 |

USD 5.48 Billion |

|

Growth Rate |

11.5% |

|

Segments Covered in the Report |

Battery Type, Process Type, Application, Material Type, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Amprius Technologies, Applied Materials, Blue Solutions, CATL (Contemporary Amperex Technology Co. Limited), Durst Group, LG Energy Solution, Northvolt, Panasonic Energy, Samsung SDI, Tesla |

|

Customization |

Available upon request |

Roll-to-Roll Battery Manufacturing Market Segmentation

By Battery Type

Lithium-ion batteries achieved market dominance in 2025 by generating approximately 63% of total revenue which resulted from their widespread use in electric vehicles and consumer electronics and grid storage systems. The combination of roll-to-roll electrode processing and established manufacturing ecosystems enables companies to maintain their dominant market position. The implementation of government-backed electrification programs which mandate clean energy usage drives industrial markets to implement large-scale electrification projects.

The research projects that solid state batteries will experience the fastest market growth which will reach an estimated CAGR of 12.9% from 2026 until 2035. The growth of the market stems from rising demand for storage systems which provide high energy density along with improved safety performance and advancements in battery chemistry technologies which are being developed for next-generation batteries. The automotive and energy storage sectors experience segment growth from increasing investments which support pilot production line development and national research programs that focus on advanced battery technology.

By Process Type

The revenue of electrode coating reached 48% of total revenue in 2025 because it played a vital role in large-scale battery production and its continuous manufacturing capabilities allowed for broad operational use. The lithium-ion battery production lines sustain its market dominance because industrial users have adopted it as part of their existing operations which connect with all gigafactory production processes. The government-backed manufacturing expansion initiatives and industrial automation programs result in increased adoption of these technologies.

Dry electrode processing will experience the most rapid growth in the upcoming years because it will achieve a CAGR of 13.2% between 2026 and 2035. The market expansion results from increasing demand for battery systems which need both better performance and reduced costs along with the complete removal of solvent-based methods during battery production. The combination of material engineering developments and next-generation production technology investments leads to a rapid adoption of these technologies by major battery producers.

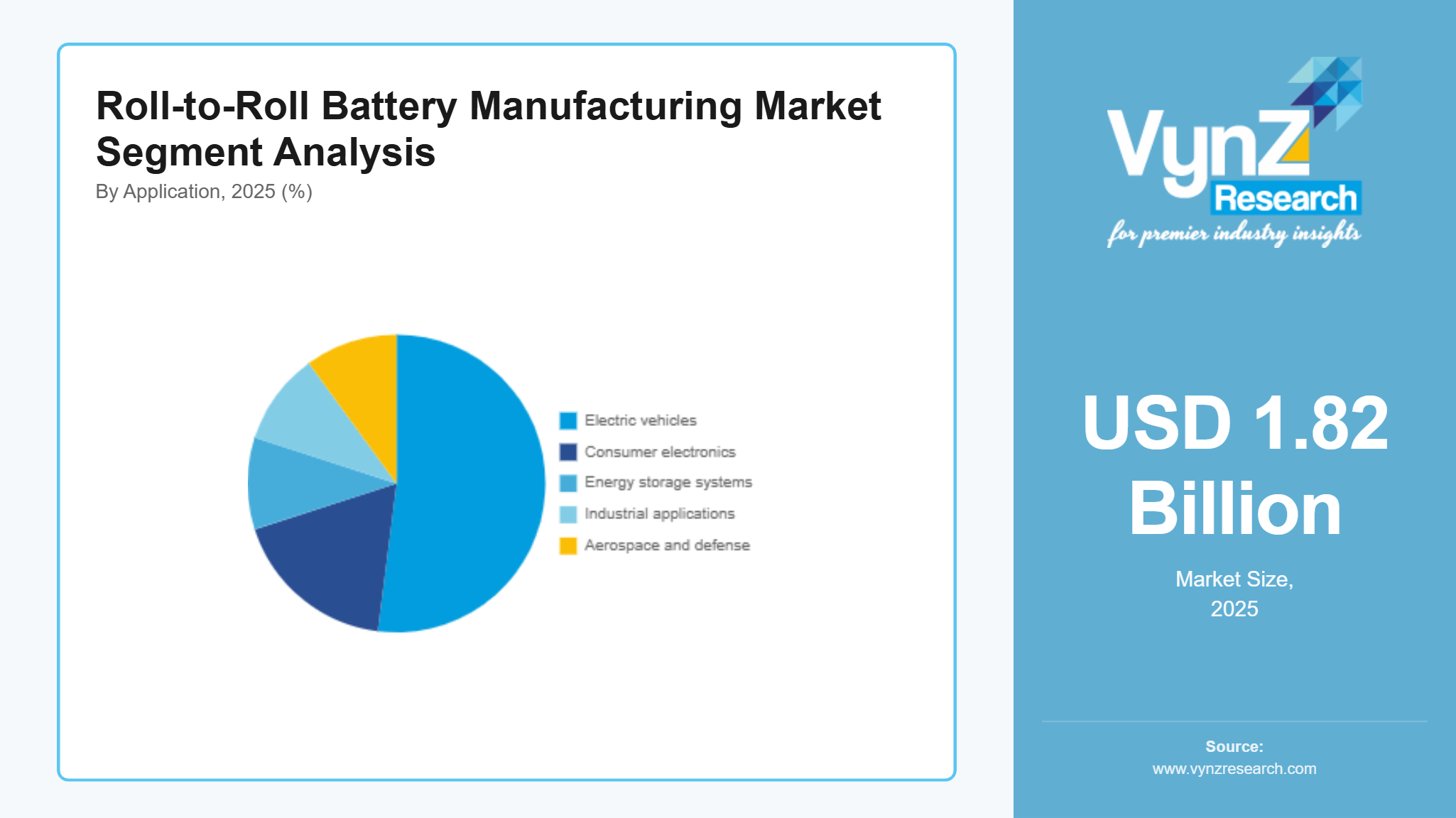

By Application

Electric vehicles accounted for the largest market share in 2025, representing approximately 52% of total revenue, supported by rapid global EV adoption, expansion of charging infrastructure, and increasing government incentives for electric mobility. The combination of large-scale production requirements and the high demand for efficient battery cells enables this segment to maintain its dominance.

Energy storage systems will experience the fastest market growth because they will achieve a CAGR of 13.5% from 2026 until 2035. The market expansion results from renewable energy sources being integrated into existing infrastructure and new grid modernization programs being implemented which create demand for large-scale stationary energy storage systems. The deployment of utility-scale projects across the market receives a push from government-backed clean energy transition initiatives and funding for decentralized energy infrastructure projects.

By Material Type

The revenue share of cathode materials reached 45% in 2025 because these materials establish the costs that determine total battery production expenses while their performance capabilities establish the energy storage potential of batteries. The industry maintains its market dominance because advancing nickel-rich chemistries enable the large-scale production of lithium-based cathodes. The government programs which focus on critical mineral supply chain development together with battery material localization strategies enable this market segment to build greater strength.

Anode materials will experience the most rapid growth because they will achieve a CAGR of 12.7% between 2026 and 2035. The market growth stems from the rising demand of silicon-based anodes and next-generation graphite enhancements which improve both battery capacity and charging efficiency. The advanced material research field is experiencing growth because industries are investing in the development of high-performance anode technologies while companies establish their industrial capacity for these advanced materials.

By End User

The automotive manufacturing sector generated the largest revenue share in 2025 when it captured approximately 49% of total sales because electric vehicle production continued to expand while high-efficiency battery systems experienced increasing demand. The global expansion of EV manufacturing facilities together with government policies which support zero-emission vehicle programs enables this segment to maintain its market leadership position.

The market for energy storage system providers will experience rapid growth because it will achieve a CAGR of 13.8% from 2026 until 2035. The market expansion results from renewable energy production at utility scale which requires grid stability solutions and investment increases for energy storage solutions at stationary positions. The worldwide adoption of renewable energy targets together with energy transition frameworks which receive government support leads to increased market adoption across energy sectors.

Regional Insights

North America

North America contributed about 32% of the market during 2025 because electric vehicle manufacturing, battery research facilities and gigafactory construction projects created strong demand. The United States industrial centers which include California, Texas and Michigan continue to generate high demand for advanced battery manufacturing technologies. The combination of clean energy transition programs, domestic semiconductor and battery supply chain policies which receive support from national energy agencies and federal manufacturing incentives leads to faster technology adoption. The market performance of the region improves because of expanded EV manufacturing capacity combined with increased deployment of renewable energy storage systems.

Europe

Europe offered about 24% of the market during 2025 because its carbon neutrality goals, regulatory framework and electric transportation systems create fast growth. The automotive manufacturing hubs of Germany, France, Sweden and the United Kingdom create ideal conditions for electric vehicle adoption through their existing manufacturing systems and strategic battery gigafactory investments. European Union clean energy policies and battery sustainability regulations which provide regulatory support enable companies to establish advanced roll to roll manufacturing systems at large scale. Government supported industrial decarbonization initiatives and funding programs for next generation battery technologies are further strengthening regional growth across automotive and energy storage sectors.

Asia Pacific

Asia Pacific in 2025 represented 38% of the market through its battery manufacturing facilities and its ability to manage supply chains. The production centers of China, Japan and South Korea contain their major industrial cities which include Shenzhen, Tokyo and Seoul. The strong demand for products continues because electric vehicle manufacturing and consumer electronics production have both expanded at a rapid pace. National battery development programs, clean mobility targets and industrial automation investments supported by government initiatives create conditions for faster growth. Asia Pacific serves as the main worldwide center for lithium-ion battery production and technological advancements according to global energy transition studies.

Rest of the World

The Rest of the World which includes Latin America, the Middle East and Africa controlled approximately 6% of the market during 2025. The regions experience growth because renewable energy investments, electric vehicle adoption, and development in battery manufacturing infrastructure. The countries of Brazil, the United Arab Emirates and South Africa are experiencing newly emerging energy storage demand. The adoption of advanced manufacturing systems receives support from government clean energy programs and international technology transfer partnerships.

Competitive Landscape / Company Insights

The market operates at a moderate to highly competitive level because worldwide equipment producers, battery technology companies and industrial automation firms concentrate their efforts on improving production processes, developing new materials and building industrial facilities with expanded production capabilities. Companies are investing more funds into their research and development programs while they proceed to implement advanced manufacturing automation systems and digital production technologies to enhance their market presence. Government-sponsored clean energy transition projects and national battery manufacturing programs which energy and industrial development agencies back have created a framework that drives technology implementation and facility development. The establishment of strategic partnerships with automotive manufacturers and energy storage producers together with the adoption of high throughput production systems dictate how businesses compete in international markets.

Mini Profiles

Applied Materials focuses on advanced semiconductor and battery manufacturing equipment, supported by strong global distribution networks and deep technological expertise in precision engineering and industrial production systems.

Blue Solutions operates in the premium solid state battery segment, emphasizing high energy density design and advanced lithium metal polymer technology for electric mobility and stationary energy storage applications.

CATL leverages large scale local manufacturing capabilities and strong strategic partnerships with automotive and energy companies to expand its global leadership in lithium-ion battery production markets.

Durst Group focuses on industrial roll to roll printing and coating systems, supported by strong engineering innovation and cost-efficient production technologies for advanced battery electrode manufacturing applications.

LG Energy Solution operates in the premium battery manufacturing segment, emphasizing high performance lithium-ion solutions and global production networks supporting electric vehicles, energy storage systems, and consumer electronics.

Key Players

- Amprius Technologies

- Applied Materials

- Blue Solutions

- CATL (Contemporary Amperex Technology Co. Limited)

- Durst Group

- LG Energy Solution

- Northvolt

- Panasonic Energy

- Samsung SDI

- Tesla

Recent Developments

In January, 2026, CATL announced expansion of its roll-to-roll compatible electrode manufacturing capacity to support next generation high energy density batteries for electric vehicles and grid storage systems. The company is strengthening global supply chain integration through new production facilities in Europe and Asia.

In March, 2025, LG Energy Solution expanded its advanced battery production line focused on high efficiency lithium-ion cells for electric vehicles and energy storage systems. The company also increased investment in automated roll-based electrode processing to improve manufacturing scalability and cost efficiency.

In May, 2025, Panasonic Energy initiated upgrades to its cylindrical battery production facilities to support higher throughput roll to roll electrode processing technologies. The development is aligned with increasing demand from automotive partners for long range electric vehicle battery systems.

In July, 2025, Samsung SDI announced enhancement of its pilot solid state and next generation battery production lines using advanced roll-based manufacturing techniques. The company is focusing on improving energy density and safety performance for electric mobility applications.

In September, 2025, Tesla expanded its battery manufacturing ecosystem through increased integration of roll-to-roll electrode production in its gigafactory operations. The initiative supports higher volume 4680 cell production for electric vehicles and large-scale energy storage deployment.

Global Roll-to-Roll Battery Manufacturing Market Coverage

Battery Type Insight and Forecast 2026 - 2035

- Lithium-ion batteries

- Solid-state batteries

- Lithium-sulfur batteries

- Others

Process Type Insight and Forecast 2026 - 2035

- Electrode coating

- Electrode printing

- Dry electrode processing

- Lamination and assembly

Application Insight and Forecast 2026 - 2035

- Electric vehicles

- Consumer electronics

- Energy storage systems

- Industrial applications

- Aerospace and defense

Material Type Insight and Forecast 2026 - 2035

- Cathode materials

- Anode materials

- Electrolytes

- Separator films

End User Insight and Forecast 2026 - 2035

- Automotive manufacturers

- Battery manufacturers

- Electronics manufacturers

- Energy storage system providers

- Defense and aerospace organizations

Global Roll-to-Roll Battery Manufacturing Market by Region

- North America

- By Battery Type

- By Process Type

- By Application

- By Material Type

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Battery Type

- By Process Type

- By Application

- By Material Type

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Battery Type

- By Process Type

- By Application

- By Material Type

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Battery Type

- By Process Type

- By Application

- By Material Type

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Roll-to-Roll Battery Manufacturing Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Battery Type

1.2.2. By

Process Type

1.2.3. By

Application

1.2.4. By

Material Type

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Battery Type

5.1.1. Lithium-ion batteries

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Solid-state batteries

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Lithium-sulfur batteries

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Others

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Process Type

5.2.1. Electrode coating

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Electrode printing

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Dry electrode processing

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Lamination and assembly

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Electric vehicles

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Consumer electronics

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Energy storage systems

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Industrial applications

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Aerospace and defense

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Material Type

5.4.1. Cathode materials

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Anode materials

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Electrolytes

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Separator films

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Automotive manufacturers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Battery manufacturers

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Electronics manufacturers

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Energy storage system providers

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Defense and aerospace organizations

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Battery Type

6.2. By

Process Type

6.3. By

Application

6.4. By

Material Type

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Battery Type

7.2. By

Process Type

7.3. By

Application

7.4. By

Material Type

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Battery Type

8.2. By

Process Type

8.3. By

Application

8.4. By

Material Type

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Battery Type

9.2. By

Process Type

9.3. By

Application

9.4. By

Material Type

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Benchmark Electronics, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Celestica Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Flex Ltd.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Jabil Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Kimball Electronics, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Plexus Corp.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Sanmina Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

SIIX Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

TE Connectivity Ltd.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Zollner Elektronik AG

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Roll-to-Roll Battery Manufacturing Market