TIC Market for Water Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (In-House, Outsourced), by Service Type (Testing, Inspection, Certification), by Industry Vertical (Stadiums, Concert Halls, Theme Parks, Event Planners)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9206 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 180 |

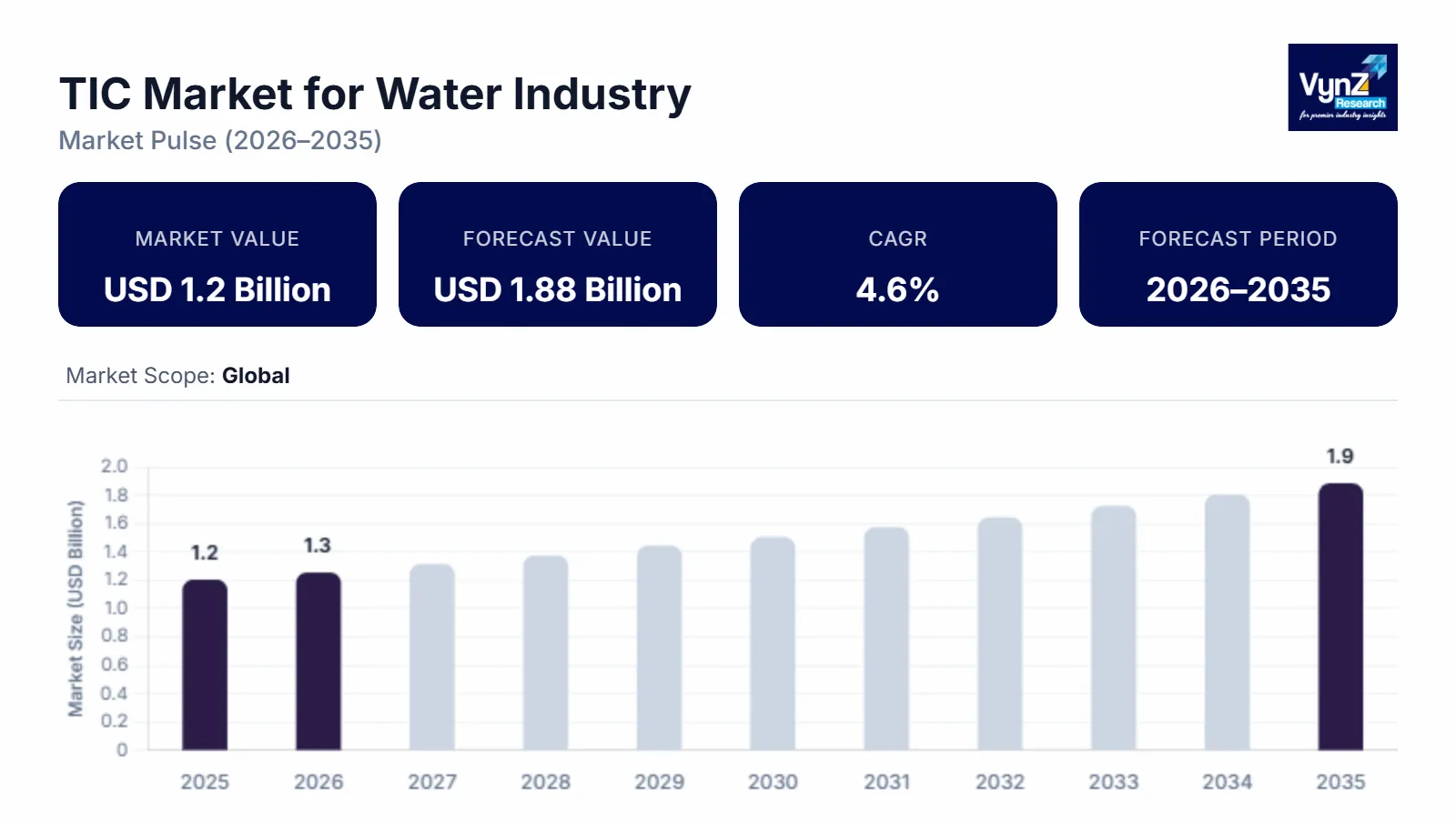

TIC Market for Water Industry Overview

The global TIC Market for Water Industry, which was valued at approximately USD 1.2 billion in 2025 and is estimated to reach around USD 1.25 billion in 2026, is projected to reach approximately USD 1.88 billion by 2035, expanding at a CAGR of about 4.6% during the forecast period from 2026 to 2035.

Development and industrialization are driving up demand for trustworthy water testing and certification services. TIC services are used to monitor drinking water, wastewater, and process water to identify contaminants, verify treatment efficacy, and guarantee adherence to national and international requirements. Improved testing methods are also being used by utilities and industry as a result of increased public health and environmental sustainability awareness. This industry is been driven by inadequate infrastructure and growing concerns about water pollution. The Testing, Inspection, and Certification (TIC) industry is essential for maintaining water quality, safety, and regulatory compliance in municipal, industrial, and environmental applications.

Major participants in the TIC market include specialist labs that concentrate on water analysis as well as global corporations that provide integrated services across industries. The global requirement for safe and sustainable water management, technical improvements, and regulatory enforcement are all projected to support the TIC market's overall steady growth for the water industry. Water quality system certification, treatment facility inspection, and chemical and microbiological testing are crucial services in the TIC sector. Automation, real-time monitoring systems, and digital technologies are often used by businesses to boost accuracy and efficiency.

TIC Market for Water Industry Dynamics

Market Trends

Stricter laws, increased water contamination, and growing demand for safe drinking water are driving the TIC market for the water industry. Testing and inspection procedures are changing as a result of digital technologies like IoT and real-time monitoring. Because of the regular necessity for compliance, testing services are the most popular. Demand for certification is rising due to sustainability trends like zero-liquid discharge and water reuse. Additionally, the demand for TIC services across municipal and industrial water systems is growing due to the quick urbanization and infrastructure development in emerging regions.

Growth Drivers

Tougher rules on clean water push growth in the TIC sector for water systems. Agencies like the EPA, WHO, or local watchdogs require regular checks on drinking and waste flows. Because firms must follow these laws, test numbers jumped about 18% in five years - boosting steady need for audits, analysis, and approval work.

Rising funding for water systems pushes market expansion forward. Worldwide, cash going into pipes and cleanup centers climbs near 6% every year - especially on filters, tubes, plus salt-removal spots. Every fresh setup needs regular checkups, function scans, or approval tags, which lifts steady need for testing checks down the road.

Fears about dirty water and health dangers are pushing the market to grow faster. Because heavy metals, tiny plastics, and factory waste show up more often, lab checks have jumped by over 20% since 2020. That means labs now need better analysis tools, inspections, or outside approvals in the water industry.

Market Restraints / Challenges

High operating expenses and the requirement for sophisticated testing infrastructure are two obstacles facing the water industry's TIC market. Compliance procedures are made more difficult by regional regulations that are fragmented. Service quality and scalability are impacted by a lack of standardization and a paucity of competent workers. Furthermore, small and medium-sized businesses sometimes lack the resources necessary to implement complete TIC services. Efficiency is further hampered by problems with data management and digital tool integration. TIC service providers' profitability is further impacted by pricing pressures and market rivalry.

Market Opportunities

Growing investments in water infrastructure and treatment facilities are driving substantial potential in the TIC market for the water industry. Advanced testing and inspection services are in high demand due to the growing use of digital monitoring systems and smart water technologies. New certification opportunities are created by expanding desalination, water reuse, and environmental initiatives. Emerging markets have significant development potential because of urbanization and industrialization. Furthermore, enterprises and municipalities are being encouraged to depend more on TIC services because to increased public health awareness and increasingly stringent environmental regulations.

Global TIC Market for Water Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.2 Billion |

|

Revenue Forecast in 2035 |

USD 1.88 Billion |

|

Growth Rate |

4.3% |

|

Segments Covered in the Report |

Sourcing Type, Service Type and Industry Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific |

|

Key Companies |

Intertek Group plc, Bureau Veritas, UL LLC, SGS SA, Eurofins USA, TUV Rheinland, Lloyd Register Group Limited, ALS Limited, Applus+, DNV GL |

|

Customization |

Available upon request |

Available upon request

TIC Market for Water Industry Segmentation

By Sourcing Type

Depending on where it comes from, the water industry’s TIC sector splits into internal checks or outside services. Outside options grow fastest - around 7.4% yearly - because they save money, bring skilled know-how, also meet rules better than in-house teams.

Private firms grab most of the market - around 65% of income comes from them - since energy providers and factory managers lean toward third-party checks to satisfy legal plus agreement demands. Using outside help cuts down upfront costs for internal labs or hiring niche inspectors.

In-house TIC services stay consistently popular with big city utilities along with industrial water firms. They build their own testing setups because quicker results matter, also ongoing oversight helps them run smoothly.

Still, tougher rules and more detailed tests are making big companies turn to outside experts who can handle precise water checks. While some manage on their own, many now prefer skilled third-party labs for reliable results.

By Service Type

Depending on what’s offered, the field splits into checking, examining, confirming, reviewing, plus guidance work. Checking leads the pack - growing fastest near 7.9% yearly - as clean water checks happen all the time.

Fifty-fifty almost on tests for chemicals and germs - rules pushing checks for bad bugs, toxic stuff, metal junk, plus new pollutants. Newer lab tricks catching on fast, so this side keeps moving forward.

Inspection work’s picking up, thanks to more checks on pipes, storage units, and processing sites. Old water systems in rich countries mean inspections happen way more often now - boosting the need for these services.

Certification work is growing because companies need to meet ISO rules, eco goals, or green targets. Since more joint ventures pop up, these checks also matter for global water efforts.

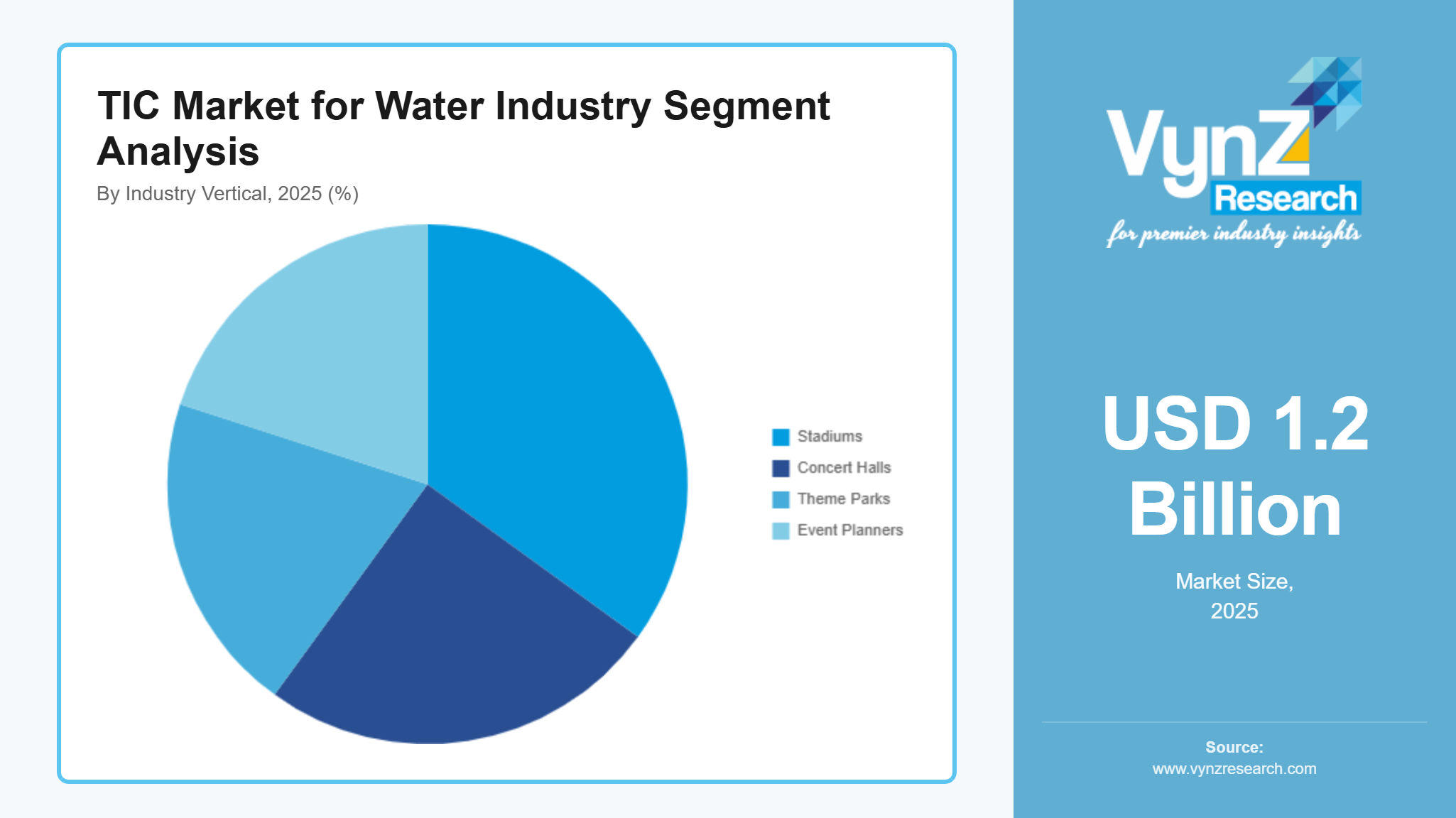

By Industry Vertical

Across different sectors, the water-focused TIC market covers city-run water services, waste processing facilities, factories using water, salt-removal sites, among others. City suppliers lead in need, making up more than two out of every five dollars earned.

Wastewater plants are growing fast because rules on dumping water got tighter, while more places now recycle cleaned water instead. Year after year, demand for checking wastewater quality climbs by about 8%, thanks to tougher standards piling up across regions.

Folks working in factories - like those making energy, chemicals, or food - are big players when it comes to checking process water and meeting waste rules. As environmental oversight grows tighter, more industrial tests on water are happening across the board.

Desalination facilities are growing fast because more dry areas now use them. Since membranes need checking, TIC checks help make sure water is clean while operations run smoothly.

Regional Insights

North America

North America’s rail sector expands by about 6.5% each year, helped along through better train tracks and heavy use of cargo trains. In that region, the U.S. drives most need - thanks to wide shipping routes combined with strict rules set by national rail regulators.

Funding for better train controls boosts checks and approvals. Upgrades in passenger lines also help grow safety reviews through trusted verification.

Public and private teams lean more on outside testers to meet rules, while cutting risks through shared efforts.

Asia Pacific

Asia Pacific’s growing quicker than anywhere else, likely hitting about 8.6% yearly until 2030. Cities expanding fast, along with more people, means higher need for clean drinking water or better waste processing.

China plus India lead regional expansion because of big spending on water systems and efforts to cut pollution. State-supported schemes for checking water quality push up the number of tests done.

More factories popping up plus tighter eco-rules are boosting the TIC market. Depending more on outside labs helps meet standards while also backing smarter water use.

Europe

Europe’s water sector sees steady growth in TIC services, making up about 25% of worldwide demand. Tough EU rules on clean water keep testing needs stable.

Countries like Germany, France, or the UK are ahead because they’ve got solid water systems and tough rules on waste release. Testing tied to meeting regulations still brings in big earnings.

Fresh attention on recycling water, green practices, plus eco-cycles is pushing up need for check-ups, reviews, also validations in Europe’s water industry.

Competitive Landscape / Company Insights

The water industry's TIC market is highly fragmented, yet it is dominated by a combination of specialized regional businesses and worldwide titans. Due to their extensive service portfolios, global reach, and regulatory knowledge, major corporations like SGS, Bureau Veritas, Intertek, Eurofins, ALS, and TÜV Rheinland maintain prominent positions.

Mini Profiles

SGS SA is a global leader in testing, inspection, and certification, SGS offers extensive environmental and water testing services. It focuses on sustainability, ESG validation, and advanced analytical capabilities, supported by a strong global lab network and strategic acquisitions.

Bureau Veritas provides water quality testing, inspection, and certification services across 140+ countries. Known for innovation and digital compliance solutions, it emphasizes AI-driven inspection and strong R&D investments.

Intertek Group plc specializes in quality assurance and environmental testing, including water analysis. It leverages high-throughput labs and digital solutions, with a strong focus on global expansion and advanced testing services.

TUV Rheinland offers testing and certification services across environmental and industrial sectors, including water systems. It is known for safety, compliance, and lifecycle inspection services.

Eurofins Scientific is a major laboratory group specializing in water, food, and environmental testing, with strong expertise in analytical services and regulatory compliance.

Key Players

- Intertek Group plc

- Bureau Veritas

- UL LLC

- SGS SA

- Eurofins USA

- TUV Rheinland

- Lloyd Register Group Limited

- ALS Limited

- Applus+

- DNV GL

Recent Developments

In March 2026, Panasonic has launched a liquid cooling systems business for AI data centers. This business focus on cooling systems for high-performance computing & generative AI servers and development of high-capacity cooling units (1,200 kW+) which aligns with rising demand from data centers and cloud computing.

In March 2026, ABB Robotics Partners with NVIDIA to Deliver Industrial-Grade Physical AI at Scale. The collaboration focuses on combining ABB Robotics’ software programming, design and simulation suite, RobotStudio, with the physically accurate simulation power of NVIDIA Omniverse libraries to close technology's long-standing 'sim-to-real’ gap. Developers can simulate robots in digital twins and generate synthetic data to train their physical AI models, enabling businesses of all types and sizes to deploy AI-driven robotics for various industrial workflows.

In February 2026, Google has awarded Form Energy, Inc. a USD billion contract to provide its cutting-edge iron-air batteries for a Minnesota data center project. One of the biggest and longest-lasting battery installations in the world, this project entails the deployment of a massive energy storage system that can provide electricity constantly for up to 100 hours. Iron-air batteries are less expensive for widespread use since they are made of inexpensive materials like iron.

Global TIC Market for Water Industry Coverage

Sourcing Type Insight and Forecast 2026 - 2035

- In-House

- Outsourced

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Industry Vertical Insight and Forecast 2026 - 2035

- Stadiums

- Concert Halls

- Theme Parks

- Event Planners

Global TIC Market for Water Industry by Region

- North America

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By Country - U.S., Canada, Mexico

- Europe

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for TIC Market for Water Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Sourcing Type

1.2.2. By

Service Type

1.2.3. By

Industry Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Sourcing Type

5.1.1. In-House

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Outsourced

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. Testing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Inspection

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Certification

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. Stadiums

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Concert Halls

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Theme Parks

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Event Planners

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Sourcing Type

6.2. By

Service Type

6.3. By

Industry Vertical

6.3.1.

U.S. Market Estimate and Forecast

6.3.2.

Canada Market Estimate and Forecast

6.3.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Sourcing Type

7.2. By

Service Type

7.3. By

Industry Vertical

7.3.1.

Germany Market Estimate and Forecast

7.3.2.

France Market Estimate and Forecast

7.3.3.

U.K. Market Estimate and Forecast

7.3.4.

Italy Market Estimate and Forecast

7.3.5.

Spain Market Estimate and Forecast

7.3.6.

Russia Market Estimate and Forecast

7.3.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Sourcing Type

8.2. By

Service Type

8.3. By

Industry Vertical

8.3.1.

China Market Estimate and Forecast

8.3.2.

Japan Market Estimate and Forecast

8.3.3.

India Market Estimate and Forecast

8.3.4.

South Korea Market Estimate and Forecast

8.3.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Sourcing Type

9.2. By

Service Type

9.3. By

Industry Vertical

9.3.1.

Brazil Market Estimate and Forecast

9.3.2.

Saudi Arabia Market Estimate and Forecast

9.3.3.

South Africa Market Estimate and Forecast

9.3.4.

U.A.E. Market Estimate and Forecast

9.3.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Intertek Group Plc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bureau Veritas

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

MISTRAS Group

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

SGS SA

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Eurofins Scientific

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

TUV Rheinland

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

TUV SUD

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

DEKRA SE

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Applus+

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

DNV GL

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

TIC Market for Water Industry