Air Taxi Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Range (Intercity (20-100 km), Intracity (100-400 km)), by Propulsion Type (Parallel Hybrid, Electric, Turboshaft, Turboelectric, Others), by Aircraft Type (Multicopter, Side-By-Side Aircraft, Tiltwing Aircraft, Tiltrotor Aircraft, Other), by End-Use (Airport Shuttle, On-Demand Air Taxi, Corporate Shuttle, Emergency Medical Services (EMS), Tourism/Sightseeing, Military/Defense)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9667 | Industry : Automotive & Transportation | Available Format :

|

Page : 178 |

Air Taxi Market Overview

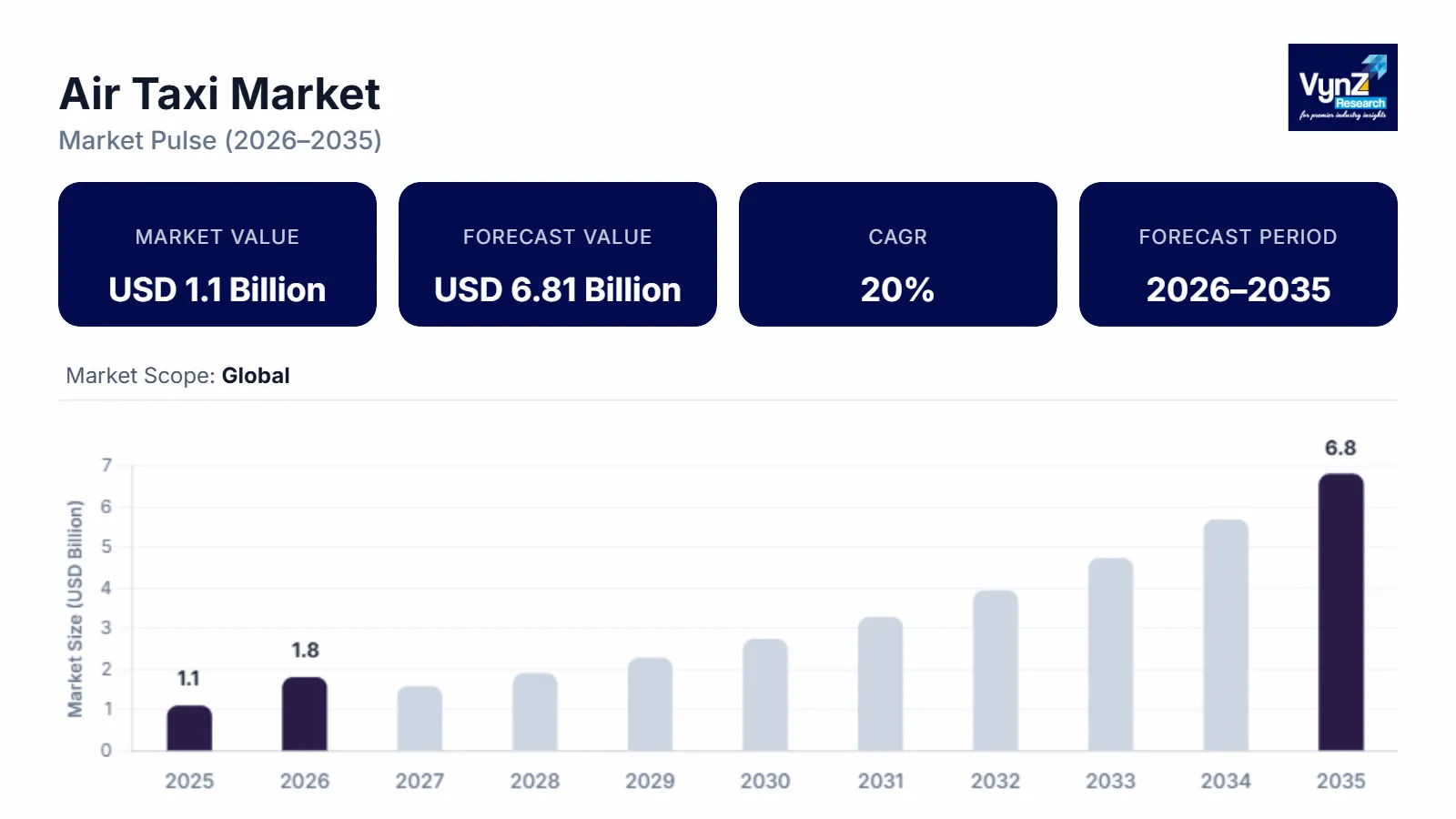

The air taxi market, which was valued at approximately USD 1.1 billion in 2025 and is estimated to rise further up to almost USD 1.8 billion in 2026, is projected to reach around USD 6.81 billion by 2035, expanding at a CAGR of about 20% during the forecast period from 2026 to 2035.

The market experiences expansion through three main factors which include fast electric vertical takeoff and landing aircraft development, increased funding for advanced air mobility infrastructure, and rising need for efficient urban transportation solutions. The need for time efficient point to point mobility solutions together with increasing traffic problems in major urban centers has driven both commercial and premium passenger markets to implement air mobility systems.

The sector development receives additional support from government funding of aviation modernization programs and their associated regulatory frameworks. Aviation authorities and global institutions such as the International Civil Aviation Organization and the Federal Aviation Administration have issued frameworks that establish guidelines for advanced air mobility platform integration into current airspace management systems. Public investment into smart mobility infrastructure together with research programs for electric aviation technology enables aerospace manufacturers and mobility service providers to accelerate their innovation efforts which results in expanded commercial deployment throughout major urban centers that include Los Angeles, Dubai, and Singapore, where advanced air mobility trials and regulatory readiness programs are currently being developed.

Air Taxi Market Dynamics

Market Trends

The industry is experiencing a fundamental transformation which leads to the development of modern urban air mobility systems through the application of electric vertical takeoff and landing aircraft technology together with autonomous flight systems. The industry major trend is shifting toward electric propulsion systems which sustainable aviation practices and decreased carbon footprint through reduced emissions. The International Civil Aviation Organization and aviation authorities together with international regulatory bodies have developed strategic frameworks which promote the creation of low emission aircraft systems and urban air mobility system connectivity.

The development of digital air traffic management systems together with autonomous navigation systems has become a new trend which uses artificial intelligence advances and aviation communication system improvements. The Federal Aviation Administration and the European Union Aviation Safety Agency are creating certification standards together with operational safety protocols which will allow advanced air mobility systems to safely operate in urban areas.

Growth Drivers

The market shows strong growth because cities need fast urban transportation systems to handle their increasing traffic and insufficient ground transportation options. Government supported smart mobility initiatives and aviation innovation programs are encouraging investment in advanced air mobility technologies which will shorten travel time through densely populated urban areas. The National Aeronautics and Space Administration published reports which demonstrate how electric vertical takeoff aircraft will function in urban transportation networks because they provide efficient short distance travel services which connect with smart city mobility systems.

Increasing investment in aviation innovation together with aviation infrastructure development drives faster deployment of advanced air mobility services. Major economies support pilot programs and test corridors to assess new aviation technologies for their operational performance. The U.S. Department of Transportation leads regulatory roadmaps and mobility innovation programs which enable aerospace manufacturers and mobility operators and technology developers to work together.

Market Restraints / Challenges

The market experiences multiple growth limitations which stem from its current technological limitations during its initial phase of market introduction. The primary growth limitation stems from the complex regulations which govern aircraft certification, airspace integration and passenger safety regulations. Aviation safety authorities including the Federal Aviation Administration and the European Union Aviation Safety Agency require extensive testing, certification procedures, and operational approvals for electric vertical takeoff aircraft before commercial deployment. The regulatory requirements of aircraft manufacturers together with mobility service providers lead to extended development periods and higher operational expenses.

The development of urban air mobility systems needs various components which include vertiports and advanced air traffic management systems and charging infrastructure and specialized maintenance facilities. The International Civil Aviation Organization reports that new mobility systems require coordinated infrastructure upgrades and standardized operational frameworks to integrate into existing aviation networks. The need for advanced battery technologies together with specialized aerospace components results in supply chain difficulties and increased costs especially during the initial stages of market growth.

Market Opportunities

The market presents significant opportunities in urban mobility transformation programs, particularly as governments and transportation planners explore alternatives to traditional ground transportation systems. Public funding for smart city infrastructure development together with next generation aviation technologies creates an environment which enables advanced air mobility services to achieve commercial success. Aviation research initiatives supported by the National Aeronautics and Space Administration highlight the potential of electric air mobility platforms to support urban transport networks through rapid point to point travel, improved regional connectivity, and reduced congestion in major metropolitan areas.

The development of integrated mobility ecosystems which connect digital booking platforms with autonomous aircraft operations and sustainable aviation technologies represents another crucial business opportunity. The U.S. Department of Transportation establishes regulatory frameworks and urban mobility programs which promote aerospace manufacturers and mobility service providers and technology companies to collaborate on commercial air taxi service development.

Global Air Taxi Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.1 Billion |

|

Revenue Forecast in 2035 |

USD 6.81 Billion |

|

Growth Rate |

20% |

|

Segments Covered in the Report |

By Range, By Propulsion Type, By Aircraft Type, By End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Airbus, Archer Aviation, AutoFlight, Beta Technologies, EHang, Eve Air Mobility, Joby Aviation, Lilium, Vertical Aerospace, Volocopter, Wisk Aero (Boeing) |

|

Customization |

Available upon request |

Air Taxi Market Segmentation

By Range

The market saw its highest intercity range aircraft share in 2025 through approximately 58% revenue distribution throughout the entire market segment. The current trend shows rising demand for fast transportation solutions between urban areas and adjacent cities, which face obstacles from heavy traffic and long travel distances. The International Civil Aviation Organization and other regulatory bodies promote advanced air mobility solutions through their regulatory programs, which support operations of short regional travel aircraft systems throughout urban metropolitan areas.

The intracity range aircraft market will experience the highest growth rate, estimating a 21% CAGR through the years 2026 to 2035. The need for quick transportation methods in urban centers combined with increasing city populations drives market expansion. The National Aeronautics and Space Administration conducted aviation research programs and urban mobility projects funding their research into short distance aerial mobility systems, which help to decrease urban congestion while improving travel efficiency. Compact electric vertical takeoff aircraft systems are presently being deployed to speed up market development for urban transportation solutions.

By Propulsion Type

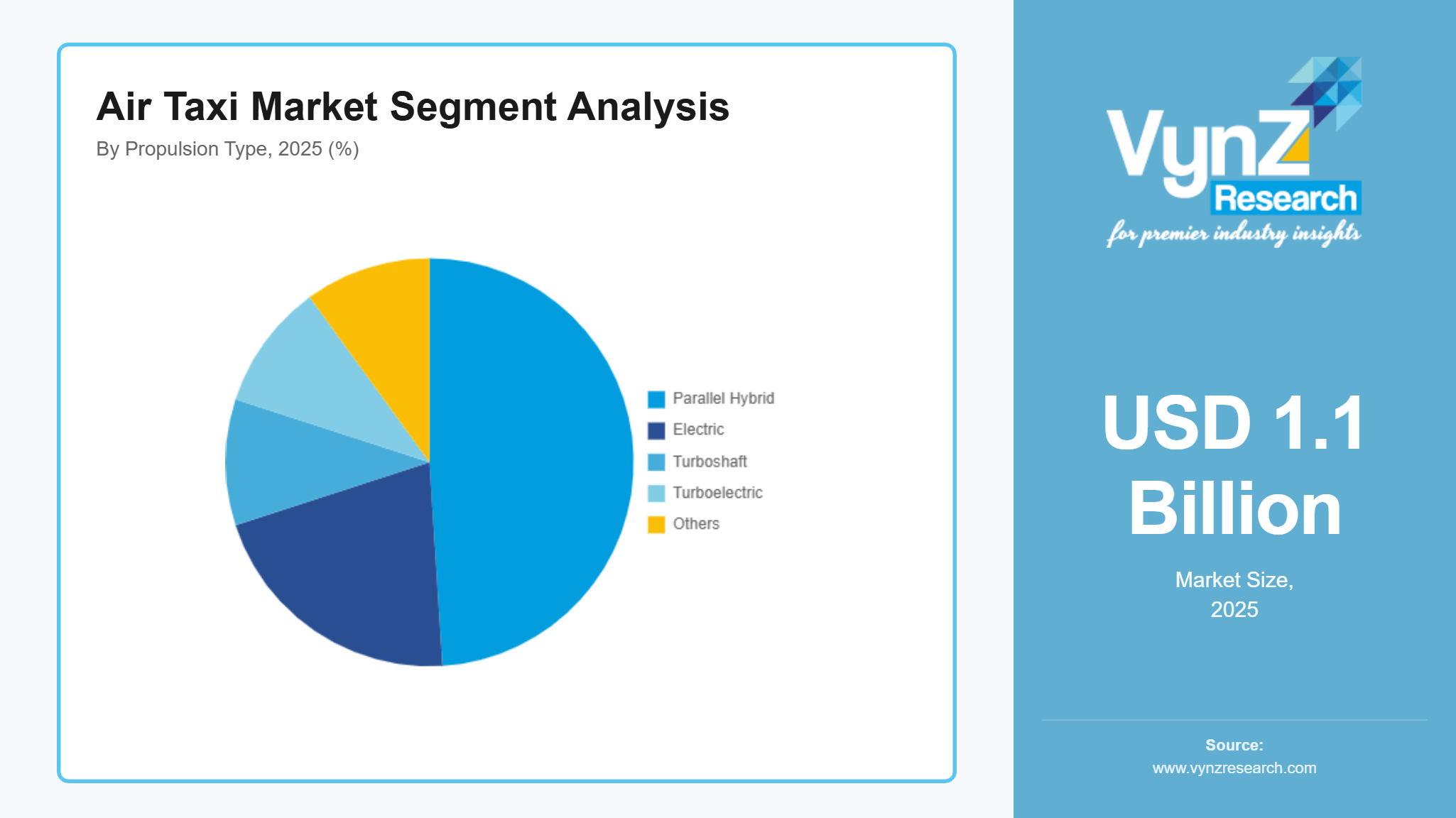

Electric propulsion systems achieved their greatest market share in the market by delivering 49% of total segment revenue during 2025. The sector currently operates under its leading position because battery technology advances request lower emissions together with additional support from aviation regulatory bodies towards sustainable aviation practices. The International Civil Aviation Organization and other organizations drive electric aviation development through their decarbonization programs, which require organizations to develop short distance urban mobility electric aviation platforms.

The hybrid propulsion market will experience the fastest growth rate, projecting a 20.8% compound annual growth rate during the entire forecasting period. Parallel hybrid and turboelectric propulsion systems are gaining attention as they provide improved operational range and energy efficiency compared with purely electric platforms. The Federal Aviation Administration and other aviation technology research agencies control research programs, which demonstrate how hybrid propulsion systems deliver better aircraft performance through their reduced emissions output.

By Aircraft Type

Multi-copter aircraft represented the largest segment in 2025, contributing roughly 46% of total market revenue. The current market leader position of the company exists because its product has both straightforward mechanical design and better vertical takeoff performance together with urban environment operation flexibility. Multi-copter platforms are widely used in early commercial prototypes and pilot programs due to their relatively straightforward engineering architecture and lower development complexity. The Federal Aviation Administration controls mobility trials together with regulatory testing programs, which use multi-copter platforms to assess operational safety and performance inside urban airspace, showing their early-stage market adoption.

The market for tiltrotor and tiltwing aircraft will expand at the highest rate between 2026 and 2035, which predicts a 21.4% compound annual growth rate. The aircraft designs allow for faster speeds and longer operational range than multi-copter platforms, which makes them ideal for regional transport routes. The National Aeronautics and Space Administration supports aviation innovation programs and advanced mobility research initiatives, which demonstrate how hybrid lift and cruise aircraft designs help create both urban and regional mobility systems.

By End Use

The market in 2025 obtained its largest revenue share through on demand air taxi services, which generated 41% of total market income. The current transportation market leads through its ability to provide flexible point-to-point travel options that appeal to both city commuters and business travelers who need premium transport services. The U.S. Department of Transportation and other governmental bodies back urban mobility plans together with aviation infrastructure projects because they recognize how on-demand aerial mobility services help users reach destinations faster while connecting cities to their primary airports.

Airport shuttle services and emergency medical services will experience the highest market growth rate, which estimates a 21% compound annual growth rate from 2026 to 2035. Major market growth occurs because rapid medical transportation services and disaster response operations and first responder teams all need fast medical transportation solutions. Public safety programs and emergency response systems rely on international aviation organizations like the International Civil Aviation Organization, which demonstrate how advanced air mobility systems will support critical healthcare transport and emergency response operations through their system applications across public service networks.

Regional Insights

North America

The market in North America reached a share of 32% during 2025 because the region developed advanced aerospace manufacturing capabilities and urban air mobility programs received major financial support and strong technological progress. Major metropolitan hubs including Los Angeles, New York City, and Dallas are conducting active testing programs which include electric vertical takeoff aircraft pilot deployments. The Federal Aviation Administration and other aviation authorities are creating certification pathways together with operational frameworks to enable safe advanced air mobility system operation inside current airspace systems.

Government programs that back next generation aviation technology development and smart transportation networks create additional support for regional growth. The National Aeronautics and Space Administration coordinates research programs that show electric aircraft play a vital role in developing efficient urban transportation systems. Public entities fund vertiport infrastructure and digital air traffic management systems and sustainable aviation research to create an environment where aerospace manufacturers and mobility service providers can work together to boost regional market growth.

Europe

Sustainable aviation technologies in 2025 enable Europe to reach a market share of 25% through its strong regulatory frameworks and increased investment in these technologies. Japan and India together with China have started more intense partnerships between their aerospace manufacturers and technology developers which will help them build urban air mobility platforms. The European Union Aviation Safety Agency together with other regulatory bodies has created certification standards and safety protocols which will permit electric vertical takeoff aircraft to begin their commercial operations throughout European airspace.

The region experiences growth because its sustainability policies promote both decreased aviation emissions and electric propulsion system implementation. International Civil Aviation Organization environmental targets promote aviation decarbonization strategies that lead aircraft manufacturers to develop electric and hybrid propulsion systems. Major European cities implement smart transportation infrastructure projects together with their urban mobility initiatives which help them bring advanced air mobility services into commercial operation.

Asia Pacific

The market share of Asia Pacific stands at 22% during the year 2025. The region has experienced growth because its urban areas expand while more people seek air travel and investments increase in advanced aviation infrastructure development. China and Japan and India have established more intense partnerships between their aerospace manufacturers and technology developers to speed up the creation of urban air mobility platforms. The major cities of Shanghai and Tokyo function as essential sites for testing advanced mobility technologies through their pilot projects and demonstration flights.

Regional growth receives support from government programs that modernize aviation systems and develop smart city technologies. The Civil Aviation Administration of China has developed aviation development strategies which prioritize both technological innovation and the development of next generation urban mobility systems. The regional aviation mobility landscape will experience long-term growth because infrastructure investments will increase and demand for fast urban transportation solutions will rise.

Rest of the World

The market in 2025 is divided between Rest of the World which includes Middle East regions and Latin America and parts of Africa and its local areas which contribute 21% to market growth. Increasing smart city infrastructure investments together with advanced transportation technology investments create growth opportunities for these regions. Cities such as Dubai are actively exploring commercial deployment of advanced air mobility services through pilot projects and regulatory collaborations. The International Civil Aviation Organization along with other aviation authorities supports international efforts which maintain safe aerial mobility platform operations between various global aviation systems.

Government-supported mobility innovation programs together with infrastructure funding led to the implementation of advanced aviation technologies across emerging markets. Urban expansion and tourism growth and dedicated aviation development plans create perfect conditions which allow advanced mobility services to operate throughout developing regions.

Competitive Landscape / Company Insights

The aerospace industry market operates between two competitive levels which begin at moderate competition and reach a state of high competitiveness. Global aerospace manufacturers and mobility technology companies allocate their resources toward developing aircraft technology and achieving higher propulsion efficiency and establishing partnerships to enhance their market standing. Companies are spending more money on research for electric aviation and autonomous flight systems and digital fleet management platforms. The Federal Aviation Administration and International Civil Aviation Organization handle authorities who establish regulatory frameworks and safety guidelines which enable structured commercialization processes while companies conduct advanced air mobility testing programs and deployment activities.

Mini Profiles

Airbus focuses on advanced electric vertical takeoff aircraft and urban air mobility platforms, supported by global aerospace expertise, strong research capabilities, and strategic partnerships that strengthen development of next generation aviation technologies.

Beta Technologies operates in specialized electric aviation segments, emphasizing performance efficiency, sustainable propulsion technologies, and integrated charging infrastructure that support emerging advanced air mobility networks and commercial electric aircraft deployment.

EHang leverages autonomous flight technologies and digital control systems to expand market presence, offering unmanned aerial mobility solutions supported by urban mobility trials, regulatory collaborations, and expanding demonstration programs.

Joby Aviation focuses on electric vertical takeoff aircraft development and commercial air mobility services, supported by strong engineering capabilities, strategic investments, and pilot programs designed to accelerate urban air transportation deployment.

Vertical Aerospace operates in advanced electric aircraft development, emphasizing sustainable aviation design and scalable production strategies supported by strategic partnerships with aerospace suppliers and mobility service providers.

Key Players

- Airbus

- Archer Aviation

- AutoFlight

- Beta Technologies

- EHang

- Eve Air Mobility

- Joby Aviation

- Lilium

- Vertical Aerospace

- Volocopter

- Wisk Aero (Boeing)

Recent Developments

In March 2026, Joby Aviation began FAA-conforming flight testing of its S4 aircraft, marking a critical milestone toward type certification. This phase ensures the aircraft meets strict regulatory standards and brings the company closer to launching commercial air taxi services.

In October 2025, Archer Aviation signed an agreement with Korean Air for up to 100 eVTOL aircraft, significantly expanding its presence in the Asian market. The deal highlights growing airline confidence in urban air mobility and strengthens Archer’s commercialization roadmap.

In March 2025, EHang secured Air Operator Certificates (AOC) in China for its EH216-S aircraft, allowing commercial passenger operations. This makes EHang one of the first companies globally to move from testing to revenue-generating autonomous air taxi services.

In December 2025, Vertical Aerospace initiated advanced flight testing, including successful transitions between vertical lift and forward flight. These tests are essential to validate real-world performance and move closer to certification and large-scale deployment.

In January 2025, Airbus decided to pause development of its CityAirbus eVTOL program as part of a broader strategic review. The move reflects the industry’s challenges around certification timelines, cost pressures, and the path to profitability in the air taxi market.

Global Air Taxi Market Coverage

Range Insight and Forecast 2026 - 2035

- Intercity (20-100 km)

- Intracity (100-400 km)

Propulsion Type Insight and Forecast 2026 - 2035

- Parallel Hybrid

- Electric

- Turboshaft

- Turboelectric

- Others

Aircraft Type Insight and Forecast 2026 - 2035

- Multicopter

- Side-By-Side Aircraft

- Tiltwing Aircraft

- Tiltrotor Aircraft

- Other

End-Use Insight and Forecast 2026 - 2035

- Airport Shuttle

- On-Demand Air Taxi

- Corporate Shuttle

- Emergency Medical Services (EMS)

- Tourism/Sightseeing

- Military/Defense

Global Air Taxi Market by Region

- North America

- By Range

- By Propulsion Type

- By Aircraft Type

- By End-Use

- By Country - U.S., Canada, Mexico

- Europe

- By Range

- By Propulsion Type

- By Aircraft Type

- By End-Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Range

- By Propulsion Type

- By Aircraft Type

- By End-Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Range

- By Propulsion Type

- By Aircraft Type

- By End-Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Air Taxi Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Range

1.2.2. By

Propulsion Type

1.2.3. By

Aircraft Type

1.2.4. By

End-Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Range

5.1.1. Intercity (20-100 km)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Intracity (100-400 km)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Propulsion Type

5.2.1. Parallel Hybrid

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Electric

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Turboshaft

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Turboelectric

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Others

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Aircraft Type

5.3.1. Multicopter

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Side-By-Side Aircraft

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Tiltwing Aircraft

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Tiltrotor Aircraft

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Other

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End-Use

5.4.1. Airport Shuttle

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. On-Demand Air Taxi

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Corporate Shuttle

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Emergency Medical Services (EMS)

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Tourism/Sightseeing

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Military/Defense

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Range

6.2. By

Propulsion Type

6.3. By

Aircraft Type

6.4. By

End-Use

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Range

7.2. By

Propulsion Type

7.3. By

Aircraft Type

7.4. By

End-Use

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Range

8.2. By

Propulsion Type

8.3. By

Aircraft Type

8.4. By

End-Use

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Range

9.2. By

Propulsion Type

9.3. By

Aircraft Type

9.4. By

End-Use

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Bobrick Washroom Equipment

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bradley Corporation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Delta Faucet Company

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Geberit AG

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Kimberly-Clark Worldwide, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Kohler Co.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

LIXIL Group Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Sloan Valve Company

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

TOTO Ltd.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Zurn Industries, LLC

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Air Taxi Market