Asia Pacific Light Electric Charging Station Market Overview

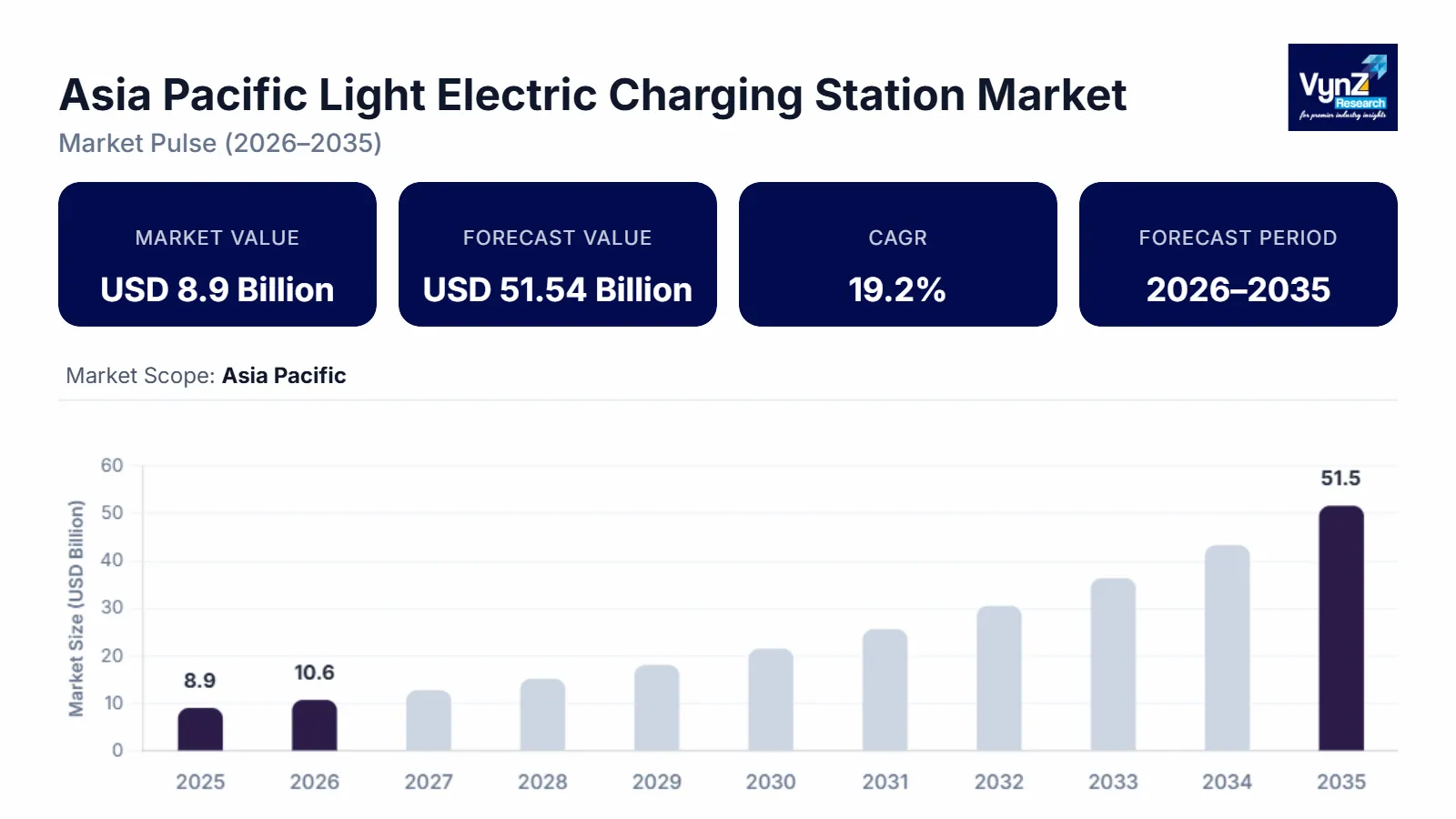

The Asia Pacific light electric charging station market which was valued at approximately USD 8.9 billion in 2025 and is estimated to rise further up to almost USD 10.6 billion by 2026, is projected to reach around USD 51.5 billion in 2035, expanding at a CAGR of about 19.2% during the forecast period from 2026 to 2035.

Market growth which depends on three main factors, progresses through the rapid electrification of transport systems, the development of urban mobility infrastructure and the implementation of regulations that encourage low emission vehicle usage together with smart charging technology implementation. Two factors drive market growth in China, Japan and India for charging network solutions which urban consumers and fleet operators need, while national energy and transport policies fund public charging infrastructure development.

Regional deployment receives stronger support through governmental backing from institutional entities and international organizations. The International Energy Agency reports that electric vehicle adoption continues to increase throughout Asia Pacific which creates a need for extensive charging infrastructure across the region. The combination of national programs that support clean mobility, renewable energy integration and grid modernization projects enables faster charging station installation. Public sector investments in urban transport electrification and incentives for private sector participation create more infrastructure density, while regulatory climate goal alignment supports long-term market growth in important economies.

Asia Pacific Light Electric Charging Station Market Dynamics

Market Trends

The market is experiencing significant changes because of new technology implementation and different infrastructure installation methods that now concentrate on intelligent and networked charging systems. The market currently undergoes transformation because smart charging system integration demonstrates new market requirements which combine energy efficiency with real time system monitoring and grid control. Digital energy management together with interoperability standards receives backing from policy frameworks that international organizations like the International Energy Agency and national energy ministries established, which enables the creation of connected charging networks to support renewable energy integration in major economies.

Growth Drivers

The market expands because of electric vehicle adoption, which creates steady demand for urban mobility and commercial fleets and public transport systems. Market expansion receives additional support from increased capital investments in both transport infrastructure systems and energy distribution network systems. The International Energy Agency reports that electric mobility in the Asia Pacific region continues to experience ongoing growth, which various national emission reduction targets and clean energy transportation systems are supporting. Government policies and electrification programs with financial incentives function as key factors, which drive user adoption of electric vehicles. The demand for charging stations that deliver high performance standards will continue to grow, because organizations and consumers need to meet three priorities, which include budget efficiency and environmental standards and operational effectiveness.

Market Restraints / Challenges

The market shows strong expansion potential, but the market faces specific obstacles, which will restrict its growth potential. The market penetration problem for price-sensitive groups in urban and semi-urban areas suffers from high operational costs and uneven distribution of infrastructure resources. The government energy reports state that developing economies face major obstacles to installation, land acquisition and grid connectivity because of their high capital costs, which remain as the primary barrier to progress. The reliance on advanced components and external technologies increases operational challenges that manufacturers and infrastructure providers must handle. The need for imported equipment together with specialized technical knowledge creates problems, which result in higher costs and disruptions in the supply chain and delays in large-scale implementation.

Market Opportunities

The market demonstrates multiple expansion possibilities through increasing public and semi-public charging station networks, which develop because of urban growth and rising needs for eco-friendly transportation options. Companies that deliver modular and scalable charging solutions will gain market advantage from their ability to meet rising demand from fleet operators and residential areas and commercial properties. The governments of Asia Pacific countries support both urban mobility missions and clean energy transition programs, which result in infrastructure development that creates beneficial conditions for future market growth.

Asia Pacific Light Electric Charging Station Market Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 8.9 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 51.5 Billion

|

|

Growth Rate

|

19.2%

|

|

Segments Covered in the Report

|

Charging Station Type, Charging Technology, Application, End Users

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

China, India, Japan, South Korea, Rest of Asia Pacific

|

Asia Pacific Light Electric Charging Station Market Segmentation

By Charging Station Type

Public charging stations accounted for the largest share in 2025, contributing approximately 58% of total revenue, supported by expanding urban infrastructure and government backed deployment programs aimed at improving accessibility. The shared charging networks which major economies build through their transport electrification strategies and public investment programs, enable constant utilization, revenue production, and installation of charging networks across busy urban areas.

The forecast period of 2026 to 2035 will see private charging stations achieve their most rapid market expansion, which will happen at a compound annual growth rate of 20.1%. The market expansion emerges from people increasingly using home charging solutions and workplace charging facilities, which receive backing from home charging equipment subsidies and energy distribution system support. People prefer using decentralized charging stations which operate in residential and semi-urban areas, because they want to charge their electric two-wheelers and passenger vehicles in more accessible locations.

By Charging Technology

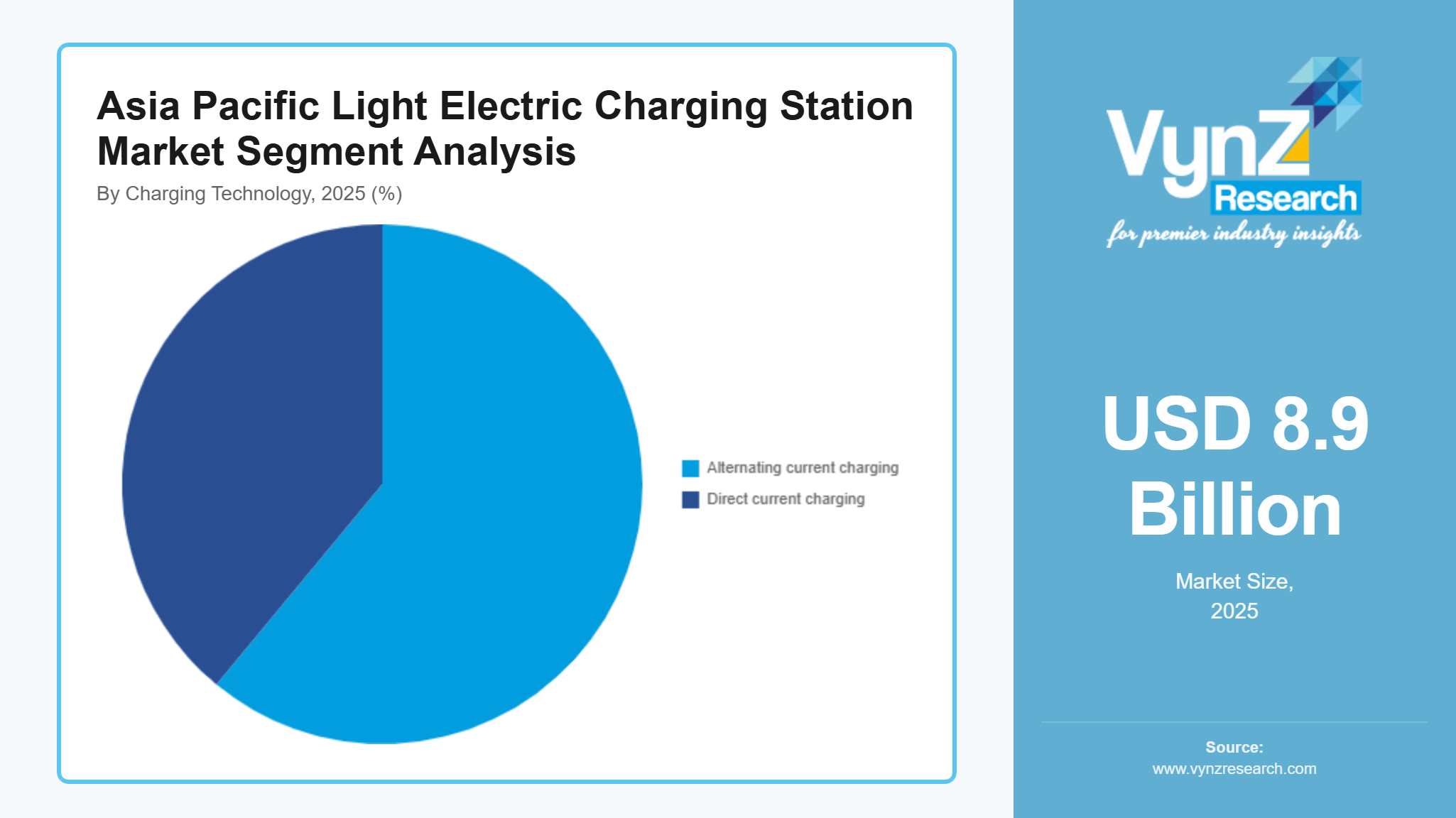

The residential and low-cost installations of the market showed their most basic system in 2025, which reached 61% of the entire segment revenue through its sales. The system maintains its dominant market position because it provides lower installation costs and uses existing grid systems, while developing countries show fast adoption of the system because they need to reduce operating costs. The ongoing technology implementation at distribution centers receives support from both government energy efficiency initiatives and distribution level infrastructure improvements.

Direct current charging will achieve the most rapid market expansion during the period from 2026 to 2035, when the market will show a compound annual growth rate of 21.3%. The market expansion occurs because people want faster charging options at urban transportation facilities and commercial businesses. The segment has achieved growth in high population urban zones because of two main factors, which include charging infrastructure policies that support fast charging stations at highways and urban bus stations, and technological developments that boost charging speed and operational performance.

By Application

The public infrastructure applications represented the biggest market portion in 2025, which reached 47% of total demand because of government projects and urban mobility initiatives. The public charging networks should be expanded according to national clean energy and transportation regulations, so that electric vehicles can achieve mass adoption in urban areas.

The retail complex and office space and fleet management facility market expansion will enable commercial applications to grow at a compound annual growth rate of 19.6% throughout the forecast period. The logistics and ride-sharing sectors need more electrified fleets and better operational efficiency, which enables the segment to grow. The residential applications market maintains its steady growth rate, which originates from both consumer product knowledge and home charging solution tax benefits that create market balance across different product applications.

By End Users

Public authorities controlled the market share in 2025 by generating 52% of total revenue through their national power distribution projects and infrastructure development initiatives. Government initiatives that target emission reduction and enhanced urban mobility drive the establishment of public transport systems and municipal infrastructure projects.

The commercial sector will experience its highest market growth, which will occur at a compound annual growth rate of 20.4%, between 2026 and 2035. Private companies establish more charging networks, which operate better because customers can use digital payment systems for charging management. Individual consumers create ongoing demand for electric vehicles, because they now have access to more residential charging options that let them charge electric vehicles in urban and semi-urban areas.

Regional Insights

China

China achieved market share of 34% in during 2025 because its transport system electrification and manufacturing power. The cities of Beijing, Shanghai and Shenzhen continue to establish charging stations because their electric vehicle usage remains high. The national clean energy targets and emissions reduction plans of the government drive infrastructure development. China leads global electric vehicle adoption according to International Energy Agency reports which creates a need for charging stations that offer dense and accessible coverage in urban areas and between cities.

India

India held 18% of the 2025 market share due to its increasing urban population and rising demand for environmentally friendly transportation options. Delhi, Mumbai and Bengaluru have become important centers for electric vehicle adoption and the establishment of charging stations. Government programs which include national electric mobility initiatives and clean transportation policies create permanent funding for charging station development.

Japan

Japan held 14% of the 2025 market share because it has developed advanced technological systems and created policies to support clean energy usage. The cities of Tokyo, Osaka and Yokohama have active high efficiency charging system installations which originate from their established automotive and electronics industries. Government energy transition programs require reductions in carbon emissions while promoting electric vehicle usage, which supports steady market expansion.

South Korea

South Korea held 12% of the market in 2025 due to its advanced digital infrastructure and market demand for modern mobility solutions. Seoul and Busan lead the establishment of intelligent charging systems, which function through their integration with smart city projects. The government supports green transportation and energy-efficient practices, which results in more funds for public and private charging station construction.

Competitive Landscape / Company Insights

The market witnesses competition between international companies and local businesses who both work on creating new products and establishing new operational areas while they use their pricing methods to control market competition. Companies are investing more resources into research and development activities and digital energy management system development to create stronger market power. Private sector investment receives support from International Energy Agency and national energy authorities through their established policy frameworks and deployment targets while public infrastructure projects and standardization efforts drive competition throughout the region.

Mini Profiles

ABB focuses on electric vehicle charging infrastructure and power distribution systems, supported by strong global engineering capabilities and advanced grid integration solutions across commercial and public charging networks.

Blink Charging Co. operates in the electric mobility charging segment, emphasizing scalable charging network deployment and digital platform integration, enabling efficient access, monitoring, and payment solutions across urban infrastructure.

ChargePoint leverages cloud based charging management systems and strategic partnerships with fleet operators and businesses to expand its presence across residential, commercial, and public charging ecosystems globally.

Delta Electronics focuses on power electronics and charging solutions, supported by strong manufacturing capabilities and energy efficient product design, enabling reliable fast charging infrastructure deployment across industrial and transport applications.

Shell operates in the energy transition and mobility services segment, emphasizing integrated energy solutions and expanding electric vehicle charging networks through its global fuel retail infrastructure and strategic sustainability initiatives.

Key Players

- ABB

- Blink Charging Co.

- BP

- Pulse

- ChargePoint

- Delta Electronics

- Hangzhou

- AoNeng

- Power Supply Equipment Co. Ltd

- Schneider Electric

- Shell

- Tesla

- Webasto Group

Recent Developments

In June 2025, Tesla expanded its Supercharger network in Asia Pacific, focusing on high-capacity V4 stations to support growing electric vehicle adoption. In March 2026, the company enhanced interoperability by opening select charging stations to non-Tesla EVs across multiple regional markets.

In September 2025, BP Pulse accelerated deployment of ultra-fast charging hubs across urban and highway corridors in Asia and Europe. In January 2026, the company strengthened its fleet charging partnerships with logistics operators to support large-scale electrification initiatives.

In April 2025, Schneider Electric introduced upgraded EV charging infrastructure solutions integrated with advanced energy management systems. In February 2026, the company expanded its smart grid-enabled charging ecosystem, improving load optimization and renewable energy integration.

In August 2025, EVBox expanded its fast-charging product line to support commercial fleet electrification across Europe and Asia Pacific. In May 2026, the company focused on software-driven charging station management tools to enhance operational efficiency and uptime performance.

In July 2025, Webasto Group increased production capacity for compact EV charging solutions targeting residential and workplace applications. In March 2026, the company advanced its modular charging systems portfolio to improve installation flexibility and reduce infrastructure costs.