China Electric Three-wheeler Market Overview

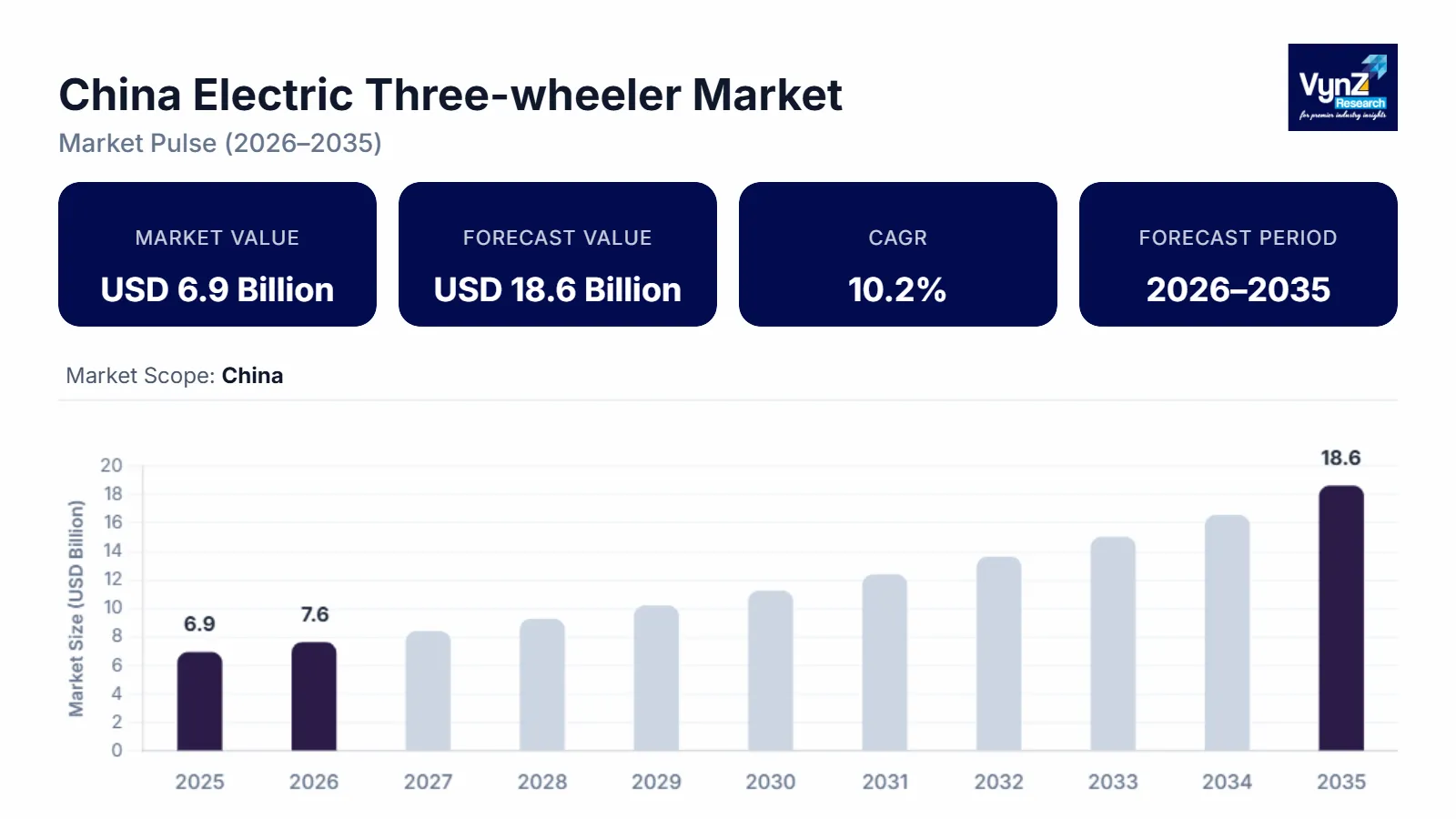

The China electric three-wheeler market which was valued at approximately USD 6.9 billion in 2025 and is estimated to rise further up to almost USD 7.6 billion by 2026, is projected to reach around USD 18.6 billion by 2035, expanding at a CAGR of about 10.2% during the forecast period from 2026 to 2035.

Market growth is basically carried by the fact that both urban and rural people are asking for affordable electric mobility options, plus there’s a bigger push in last mile logistics operations. Also, steady government support so new energy vehicles can be adopted quicker. More and more electric cargo three wheelers are being used for ecommerce drops and quick distance business transport, which is making the whole industry expand faster across many key provinces like Guangdong, Jiangsu, and Shandong.

At the same time, government backed electrification measures, and transportation modernization efforts, keep tightening market reach nationwide. Regulatory moves from the Ministry of Industry and Information Technology along with policy structures for new energy vehicle manufacturing are helping firms scale output and improve battery technology. Also, spending on charging networks and electrifying rural mobility is widening acceptance. As noted in publications from the International Energy Agency and other public organizations, China still shows strong leadership in electric mobility deployment, driven by rising clean transportation goals and emission reduction targets, which in turn keep building long term demand for electric three-wheeler solutions not only for passenger use but also for cargo and commercial transportation needs.

China Electric Three-wheeler Market Dynamics

Market Trends

The industry is seeing a lot of changes, especially around battery technology uptake, smart fleet merging, and cargo centered mobility solutions. A big shift is the move toward lithium-ion battery powered models, mostly because buyers want more mileage, less upkeep, and better energy efficiency. Also, lightweight vehicle platforms, plus connected telematics setups, are helping commercial fleet operators run things more smoothly.

Another trend is the integration of digital fleet management and smart mobility monitoring solutions, pushed by the fast expansion of ecommerce logistics, and urban delivery services. Because of this, manufacturers are paying closer attention to battery swapping compatibility, bigger payload capacity, and more durable vehicle architecture, so they can stand out from competitors. Reports by the International Energy Agency and transport electrification updates coming from the Ministry of Industry and Information Technology keep pointing to faster electric mobility adoption and wider tech modernization inside China’s low speed electric vehicle world.

Growth Drivers

The market growth is mostly supported by demand for low cost urban and rural transportation options, which stays steady across both passenger mobility and cargo logistics uses. More investments are flowing into logistics infrastructure, warehouse distribution networks, and last mile delivery operations, and that’s pushing the market forward. Plus, online retail platforms and food delivery services keep expanding, which means more electric cargo three wheelers get deployed in crowded city areas.

Government electrification initiatives push commercial operators and small enterprises to focus on fuel cost cuts and operational efficiency. So, demand for electric mobility solutions is expected to stay solid through the forecast period. Policy actions that back new energy vehicle development, led by the National Development and Reform Commission and the Ministry of Ecology and Environment are also encouraging cleaner transport adoption and more sustainable mobility infrastructure growth.

Market Restraints / Challenges

Even with all the positive momentum, the market still has problems that could slow things down. Battery raw material price swings, plus supply chain dependency, keep hitting manufacturing costs and profit margins, especially for smaller producers in price sensitive regional areas. Lithium and rare earth material pricing changes have added extra production uncertainty, across battery procurement routes too, somehow.

Also, regulatory standardization is not simple and charging infrastructure is still inaccessible in several areas. Manufacturers and fleet operators can struggle with uneven rural charging access and they may depend on outside battery component supply, which can cause delivery delays and adoption friction in less developed provinces. International Energy Agency releases and transport policy assessments from the Ministry of Transport suggest infrastructure gaps and changing safety compliance expectations are still major factors for long term scaling.

Market Opportunities

There are real opportunities, especially in electric cargo transport and smart city logistics, driven by more ecommerce activity and more pressure for fast last mile delivery. Firms that can offer durable, reasonably priced, higher payload electric three-wheeler models are positioned to win extra demand from logistics operators, retail distribution channels and rural commercial users. The ongoing substitution of fuel based three wheelers with battery operated alternatives is also helping the market outlook in the longer run.

Another opportunity is battery swapping and intelligent fleet connectivity solutions. With rising investments in digital mobility infrastructure, there’s more space for operational efficiency gains, and better customer retention. Improvements in telematics integration, vehicle tracking systems and fast charging technologies should raise fleet productivity and reduce time when vehicles are sitting idle. Government supported clean mobility directions from the Ministry of Industry and Information Technology plus sustainable transport initiatives mentioned by the International Energy Agency are expected to further reinforce investment chances.

China Electric Three-wheeler Market Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 6.9 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 18.6 Billion

|

|

Growth Rate

|

10.2%

|

|

Segments Covered in the Report

|

By Product, By Type, By Motor Power and By Driving Range

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

Guangdong, Jiangsu, Shandong, Rest of China

|

China Electric Three-wheeler Market Segmentation

By Product

Passenger electric three wheelers accounted for the largest share of the market in 2025, around 58% of total revenue. It is backed by strong utilization across urban and semi urban transport routes, plus rising demand for more affordable short distance travel and also the steady replacement of fuel powered vehicles. When public transportation connectivity in lower tier cities keeps expanding and the Ministry of Transport keeps pushing electrification policies, adoption keeps getting a lift.

Cargo electric three wheelers are likely to grow the fastest, with an estimated CAGR of 11.4% across 2026 to 2035. This growth is mainly tied to the rapid spread of ecommerce logistics, food delivery operations, and warehouse distribution activity. More funding going into smart logistics infrastructure as well as clean transportation programs is pushing fleet operators toward electric cargo mobility solutions. Even the International Energy Agency reports have continued to point out the increasing role of electric commercial mobility especially for lowering urban transport emissions and helping logistics modernization move in a more sustainable direction.

By Type

Open body electric three wheelers held the biggest market share in 2025, contributing about 54% of total segment revenue. Their position stays strong due to lower acquisition costs, operational flexibility, and wide use in rural transport as well as commercial goods movement. Demand stays particularly high among small businesses and independent transport operators, mainly because they want cheaper electric mobility options. Government supported rural electrification and low emission transport initiatives by the National Development and Reform Commission are also supporting expansion at the segment level across regional transportation networks.

Closed body electric three wheelers are projected to see the fastest growth from 2026 to 2035, with an estimated CAGR of 10.8%. This is supported by a growing preference for better passenger comfort, weather protection and safety features in urban passenger services. Ride sharing use is rising too, along with commercial passenger mobility applications, and that adds momentum to demand. Also, improvements in vehicle design efficiency plus lightweight body materials and battery integration technologies keep strengthening the competitive edge of closed cabin electric three-wheeler models across metropolitan regions.

By Motor

Power electric three wheelers under 1000W motor power accounted for the largest share in 2025, at nearly 49% of segment revenue. They dominate mostly because they are widely affordable, consume less energy, and have strong penetration in short distance passenger transport scenarios. These vehicles remain especially popular in smaller cities and rural markets, where low operating costs and simplified charging requirements matter a lot when buyers decide. Supportive policies promoting energy efficient transportation systems and low speed electric vehicle adoption keep reinforcing demand across mass market mobility applications.

Models in the 1000W to 1500W bracket are expected to grow the fastest, with an estimated CAGR of 11.1% over the forecast period. Increasing preference for higher payload capacity, stronger acceleration performance, and improved operational durability is driving adoption across cargo transportation and logistics services. More deployment of electric delivery fleets and commercial transport modernization initiatives, supported by the Ministry of Industry and Information Technology, is also encouraging manufacturers to bring in more efficient medium power vehicle platforms, with enhanced battery compatibility and extended service life.

By Driving Range

Electric three wheelers with a driving range below 100 kilometers held the largest market share in 2025, contributing around 57% of total revenue. Their prominence is supported by heavy use in local transportation, urban passenger commuting, and short distance cargo movement. Lower battery costs and simpler charging infrastructure needs keep adoption going among cost sensitive consumers and smaller scale commercial operators. Rising urbanization plus broader deployment of low-speed electric vehicles across local transport corridors continues to sustain penetration throughout major provinces.

Vehicles offering a driving range above 100 kilometers are anticipated to register the fastest growth during 2026 to 2035, with an estimated CAGR of 10.9%. Growth is driven by expanding logistics operations, rising demand for uninterrupted delivery services, and technological improvements in lithium-ion battery efficiency. Upgrades in fast charging infrastructure and higher battery energy density are giving commercial fleet operators more operational flexibility. Clean transportation programs backed by the Ministry of Ecology and Environment together with sustainable mobility recommendations from the International Energy Agency are further supporting adoption of extended range electric mobility solutions across commercial transportation networks.

Regional Insights

Guangdong

Guangdong held roughly 31% of the market in 2025 because of strong manufacturing going on plus quick city logistics expansion and also the heavy uptake of ecommerce delivery services. Steady push coming from the industrial and business clusters like Guangzhou, Shenzhen and Foshan keeps market momentum moving. The province also has solid electric vehicle supply chain advantages, especially battery production knowhow and it manages to blend clean transportation tech across commercial mobility uses.

Jiangsu

Jiangsu made up about 24% of the market in 2025, driven by rising industrial activity, growing urban transportation needs, and regional electrification rules that actually support adoption. Adoption keeps climbing for cargo transport, warehouse distribution, and small-scale logistics operations, which keeps demand steady in places like Nanjing, Suzhou, and Wuxi.

Shandong

Shandong held nearly 21% of the market in 2025 mainly backed by a bigger rural mobility electrification push, modernization of commercial transport, and local manufacturing expansion. Growth across cities like Qingdao, Jinan, and Yantai is tied to more frequent use of electric cargo three wheelers, especially for agricultural logistics, moving local goods, and handling urban delivery. At the same time, people are paying more attention to fuel cost savings and low maintenance transportation options, so penetration keeps gaining ground.

Rest of China

The rest of China collectively accounted for around 24% of the market in 2025. This is supported by gradual electrification of transportation systems and broader adoption of low-cost mobility solutions across provinces such as Zhejiang, Henan, Sichuan, Hubei, and Anhui. In particular, electric delivery vehicle penetration is increasing in tier two and tier three cities, and that is contributing to continued market expansion across these regional areas.

Competitive Landscape / Company Insights

The market is moderately competitive with local manufacturers and regional mobility players leaning on battery improvement vehicle durability and even distribution network expansion, to keep their position strong. In recent times companies are putting more money into intelligent mobility tools, lighter vehicle platforms, and lithium-ion battery integration, to push operational efficiency and make their products feel more distinct. Also, government backed new energy vehicle programs from the Ministry of Industry and Information Technology plus sustainable transport initiatives of the International Energy Agency keep nudging technological progress and broader competitive growth across the whole industry.

Mini Profiles

Baishili focuses on affordable electric three-wheeler solutions, supported by extensive regional distribution capabilities and increasing demand across passenger mobility and light cargo transportation applications.

Bidwin operates in cost competitive electric mobility segments, emphasizing durable vehicle performance, battery efficiency, and expanding dealer presence across regional transportation markets.

Changzhou Yufeng Vehicle Co. Ltd. focuses on commercial electric three-wheeler manufacturing, supported by efficient production capabilities and growing adoption in logistics and delivery applications.

Huaihai leverages strong manufacturing infrastructure and diversified electric mobility offerings to strengthen market presence across urban, rural, and commercial transportation sectors.

Jiangsu East Yonsland Vehicle Manufacturing Co. emphasizes lightweight vehicle engineering and operational reliability, supported by expanding regional distribution networks and rising commercial mobility demand.

Key Players

- Baishili

- Bidwin

- Changzhou Yufeng Vehicle Co. Ltd.

- Huaihai

- Jiangsu East

- Yonsland

- Vehicle Manufacturing Co.

- Jiangsu

- Kingbon

- Vehicle Co. Ltd.

- Jinpeng Group

- Wanhu

- Xianghe

- Qiangsheng

- Electric Tricycle Factory

- Xinge

Recent Developments

In February, 2025, Jiangsu Kingbon Vehicle Co. Ltd. expanded its electric cargo three wheeler production capabilities to support rising commercial mobility demand across regional export markets. The company also increased focus on battery efficient passenger and logistics oriented electric tricycle platforms.

In January, 2026, Jinpeng Group received industry recognition during the China Short Distance Mobility Industry Development Forum for its electric mobility product portfolio. The company also strengthened investments in intelligent manufacturing and commercial electric vehicle expansion initiatives.

In August, 2025, Wanhu expanded its electric three-wheeler lineup targeting urban logistics and commercial cargo transportation applications. The company emphasized operational efficiency improvements and extended battery compatibility for regional fleet operators.

In May, 2025, Xianghe Qiangsheng Electric Tricycle Factory increased production activities for low-speed electric cargo vehicles to address growing rural transportation demand. The company also focused on strengthening regional dealership partnerships and affordable electric mobility distribution capabilities.

In September, 2025, Xinge introduced upgraded electric three-wheeler models featuring improved driving range and lightweight vehicle design for commercial transportation applications. The company also expanded distribution activities across semi urban logistics and passenger mobility markets.