Asia Pacific Pet Food Processing Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Equipment Type (Mixing and blending equipment, Extrusion equipment, Drying and cooling equipment, Coating equipment, Others), by Process Type (Dry pet food processing, Wet pet food processing, Semi moist pet food processing), by Application (Dog food, Cat food, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRCG7053 | Industry : Consumer Goods | Available Format :

|

Page : 135 |

Asia Pacific Pet Food Processing Market Overview

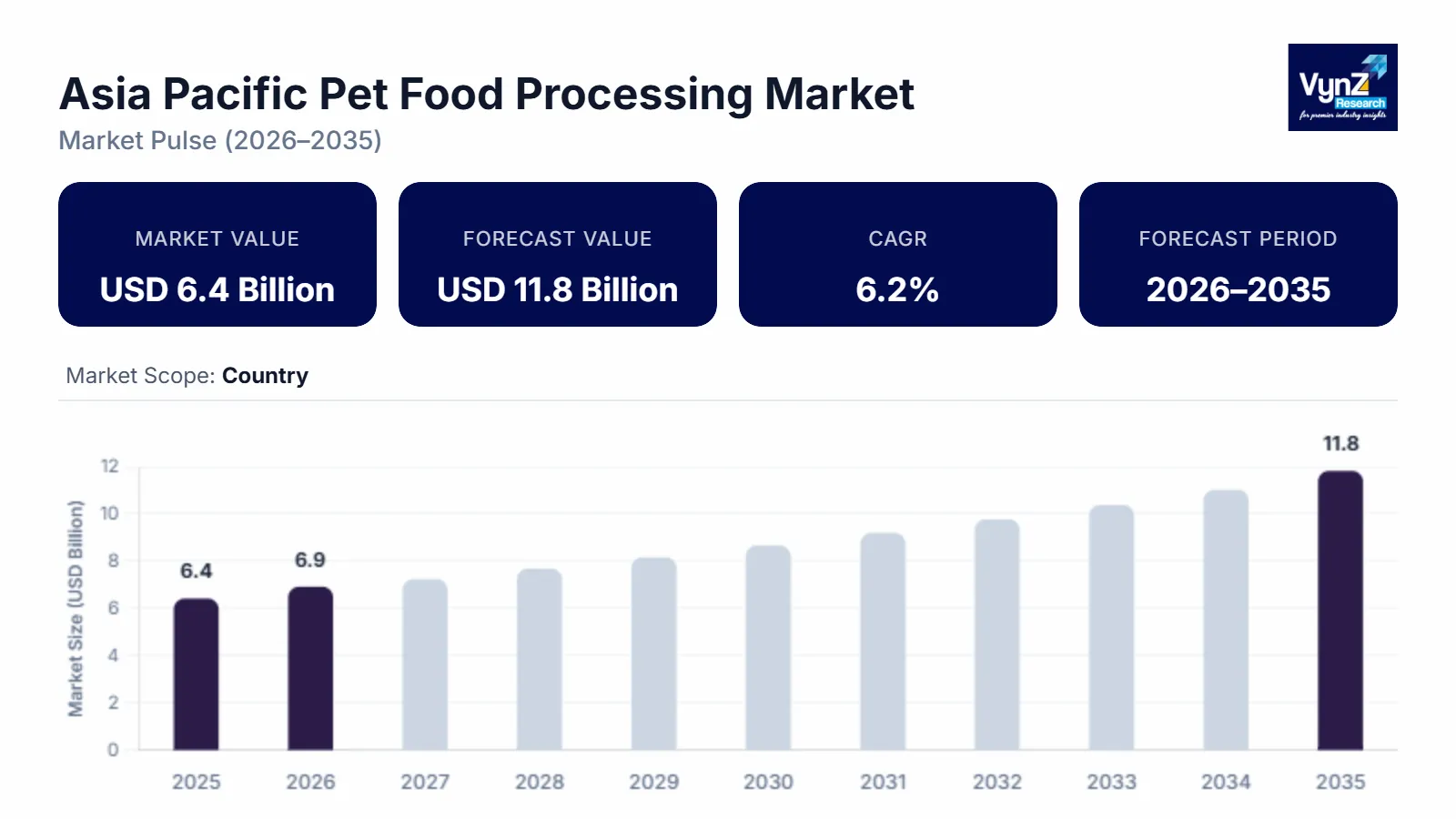

The Asia Pacific pet food processing market which was valued at approximately USD 6.4 billion in 2025 and is estimated to rise further up to almost USD 6.9 billion by 2026, is projected to reach around USD 11.8 billion in 2035, expanding at a CAGR of about 6.2% during the forecast period from 2026 to 2035.

Urban pet ownership growth results in increased market demand for processed pet food products which provide balanced nutrition while manufacturing plants develop automated food processing systems and adopt advanced extrusion and drying technologies. The premium pet nutrition market expands because customers demand functional pet food products while regulatory bodies establish food safety standards which create market growth opportunities in China, India, and Japan.

The market expansion throughout the area receives strong support from government supported programs especially their regulatory frameworks which enable efficient market operation. Asia Pacific food safety authorities and agricultural departments are developing more stringent processing and labeling requirements to guarantee pet food production meets quality standards while traceable origins. The World Health Organization and other global organizations establish food safety standards which protect against diseases that transmit between humans and animals thereby establishing a need for hygienic food processing facilities. The national livestock and veterinary development programs which promote animal health and nutrition awareness lead to increased demand for scientifically processed pet food products, which drives industry growth in the long term.

Asia Pacific Pet Food Processing Market Dynamics

Market Trends

The market experiences significant technological changes while customers increasingly prefer premium health-oriented pet food products. The trend demonstrates that manufacturers are adopting automated hygienic processing systems because customers now prioritize efficient production methods which deliver consistent products and meet food safety standards. The food safety authorities establish regulatory frameworks which World Health Organization guidelines support to promote hygienic processing and contamination control practices while manufacturers need to update their manufacturing processes.

The market now sees rising demand for functional specialized pet food products which result from increasing human-like treatment of pets and better understanding of animal health needs. Asian Pacific governments support veterinary and livestock development programs to show communities that proper nutrition and disease prevention are essential for product development and product development and product development of veterinary medicines. The industry now sees businesses targeting advanced product development which includes value-added formulations and sophisticated processing technologies to create unique products which transform market competition.

Growth Drivers

The market experiences continuous expansion because more people adopt pets and spend more money on pet care which creates permanent demand in urban homes and consumer groups with middle-income levels. The increase in food processing infrastructure investments together with manufacturing capacity development, drives market growth especially in developing markets which see a rise in organized pet food production. The government-sponsored initiatives which support food processing sector expansion together with agro-based manufacturing hubs, lead to better supply chain performance which drives industrial development.

The rising public knowledge about pet nutrition and health benefits is driving more people to adopt pets than before. The demand for processed pet food products which are scientifically developed will stay strong because consumers now choose products based on their quality and safety and nutritional content. The public health systems and veterinary advisory bodies of government agencies, focus on animal health management and disease prevention which creates a need for uniform top-quality pet food processing solutions throughout the region.

Market Restraints / Challenges

The market sees growth potential, but the market faces multiple obstacles which will limit its future expansion. The food safety regulations and advanced processing equipment require high initial investment costs, which affects small and medium manufacturers in price-sensitive markets because they must balance equipment expenses with their need for food safety compliance. The food safety authorities establish regulatory frameworks which require organizations to perform continuous quality monitoring while they must obtain certification and maintain compliance with established quality standards which increases their operational challenges.

The manufacturing companies face operational difficulties because they depend on imported processing equipment and specialized ingredient supplies. The government and trade reports show that businesses which depend on external technology systems and supply networks experience cost increases and delivery delays and face challenges with their business expansion during times of economic instability. The production process will experience lower operational efficiency while the market will suffer due to material supply uncertainty and variable input prices.

Market Opportunities

The market shows considerable growth potential for pet food processing, particularly in premium and functional pet food processing because urban areas expand and pet ownership grows with increasing pet health awareness. The companies which deliver high-performance processing solutions according to customers specifications will draw new customers who desire specialized pet food products with high nutritional value. The government-supported initiatives which promote food processing innovation together with agricultural output value addition create better growth conditions for the industry.

The marketable opportunity for businesses, exists in their implementation of digital processing systems while automation technologies drive higher productivity levels. The market, which already sees increased smart manufacturing system investments, will achieve improvements through better quality monitoring systems that deliver long-term efficiency advantages. The production process will experience lower operational efficiency while the market will suffer due to material supply uncertainty and variable input prices.

Market Opportunities

The market shows considerable growth potential for pet food processing, particularly in premium and functional pet food processing because urban areas expand and pet ownership grows. The companies which deliver high-performance processing solutions according to customers specifications will draw new customers who desire specialized pet food products with high nutritional value. The government-supported initiatives which promote food processing innovation together with agricultural output value addition create better growth conditions for the industry.

The marketable opportunity for businesses, exists in their implementation of digital processing systems while automation technologies drive higher productivity levels. The market, which already sees increased smart manufacturing system investments, will achieve improvements through better quality monitoring systems that deliver long-term efficiency advantages. The production process will experience lower operational efficiency while the market will suffer due to material supply uncertainty and variable input prices.

Asia Pacific Pet Food Processing Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.4 Billion |

|

Revenue Forecast in 2035 |

USD 11.8 Billion |

|

Growth Rate |

6.2% |

|

Segments Covered in the Report |

Equipment Type, Process Type, Application |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Japan, Australia |

|

Key Companies |

ADM, Blue Buffalo Pet Products Inc., Diamond Pet Foods, Farmina Pet Foods, General Mills Inc., Hill's Pet Nutrition Inc., Mars Petcare Ltd, Nestle Purina Petcare, Unicharm Corporation, Wellness Pet Company |

|

Customization |

Available upon request |

Asia Pacific Pet Food Processing Market Segmentation

By Equipment Type

The market encountered its highest revenue with extrusion equipment which generated 34% of total revenue in 2025. The equipment it controls proves to be the leading choice for dry pet food production because it delivers reliable product quality together with effective capacity management for high-volume operations. The growing need for consistent texture and long-lasting shelf life in processed pet food products drives their adoption in major manufacturing plants. The process of implementing advanced extrusion systems becomes necessary in critical markets because regulatory bodies and food safety standards demand their utilization.

The market for drying and cooling equipment will experience the highest growth rate according to the forecasted CAGR of 6.8% between 2026 and 2035. The market demand for moisture management together with better product preservation and food safety standard adherence drives this expansion. The segment development gets bolstered by rising investments toward hygienic processing infrastructure and automation technology. The need to customize products together with new nutritional formulations in pet food manufacturing creates ongoing demand for coating and mixing systems.

By Process Type

Dry pet food processing held the largest market share in 2025, contributing approximately 48% of total segment revenue. The product maintains its market position because people purchase it frequently, it remains fresh for a long time and production costs for mass production stay low. The market for dry processed pet food products continues to grow because more people own pets in cities and they want affordable and convenient feeding options. The manufacturing units will adopt the new systems because regulatory frameworks which focus on safe storage and contamination risk reduction will help them meet industry requirements.

The wet pet food processing market will expand at the highest rate during the upcoming years according to projections which predict a CAGR of 6.9% between 2026 and 2035. The need for high-moisture pet diets with protein content grows among premium pet owners. The rising demand for wet food production capacity increases because pet health knowledge has grown among pet owners together with veterinary health programs and veterinary guidelines. The market for semi-moist processing products continues to expand because of the need for special products and the creative product differentiation strategies that businesses use.

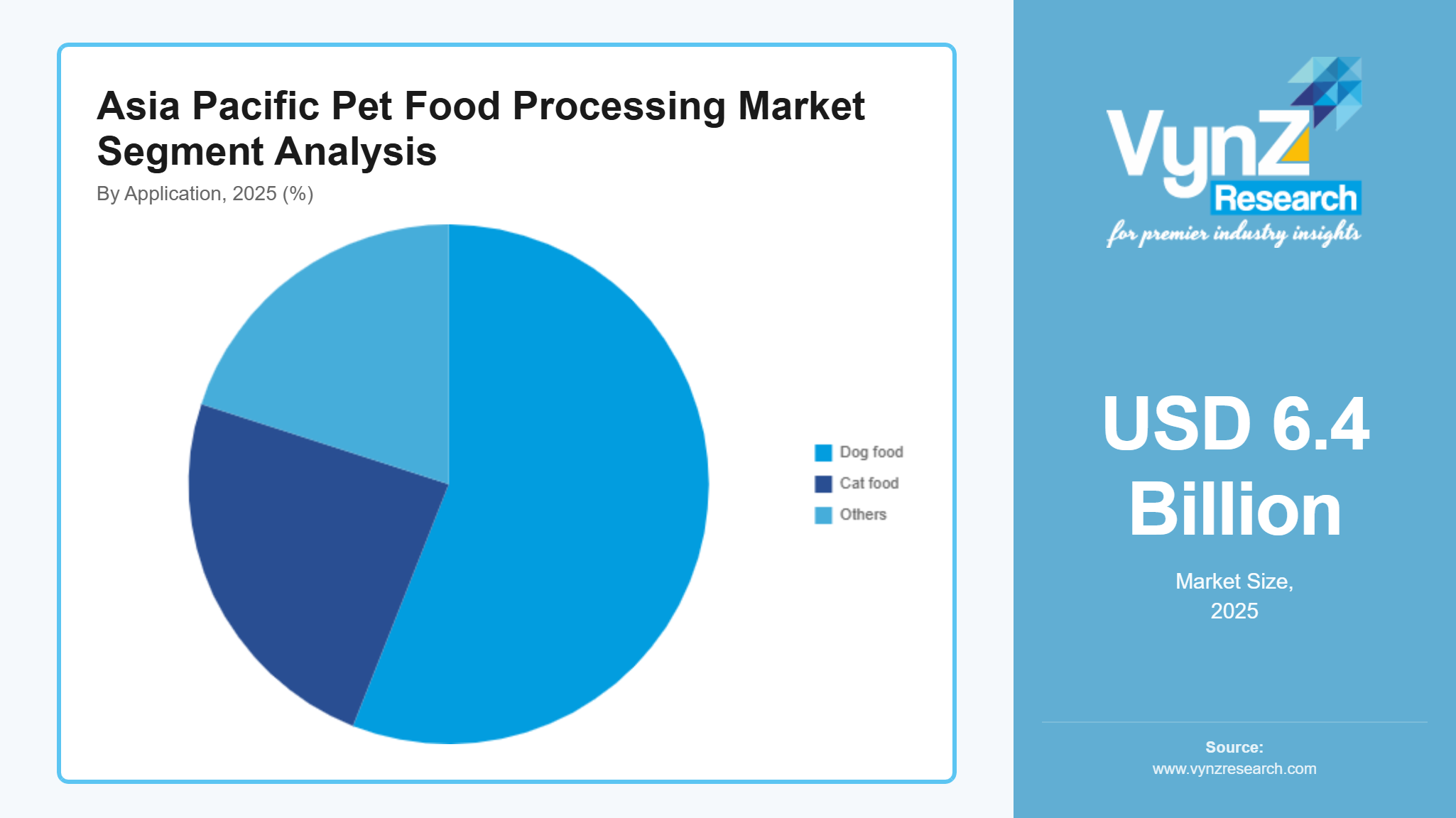

By Application

Dog food processing accounted for the largest share in 2025, representing approximately 56% of total market revenue. The product dominates the market because urban and semi-urban areas have more dog owners who spend more on pet nutrition and care. Veterinary advisory programs and government-funded animal health awareness initiatives keep promoting balanced diets for companion animals which drives demand for processed dog food products. The segment growth in major economies experiences support from expanding retail distribution and premium product offerings.

The market for cat food processing will experience the fastest growth rate according to projections which predict a CAGR of 6.7% during the upcoming period. Urban cat adoption ascends because more people choose to adopt cats as they move to cities while their lifestyle changes lead them to prefer pets that require less maintenance. The segment growth process receives backing from new specialized cat food products which provide both functional and premium options. Companion animal ownership patterns are becoming more diverse while consumer preferences keep changing which leads to ongoing growth in other pet food categories.

Regional Insights

China

The market during 2025 showed China holding 34% of the total market share because people in cities like Beijing, Shanghai and Guangzhou acquired more pets while their urbanization and disposable income increased. The high demand for processed pet food products which contain premium quality ingredients enables manufacturers to build new large-scale production plants while they develop advanced methods of processing. National food authorities through their supported food safety regulations and quality control systems create a framework which requires manufacturers to follow standardized production methods while maintaining traceability and sanitary practices.

Japan

Japan held an estimated share of around 18% in 2025 which resulted from people choosing expensive pet food products that offer both premium quality and nutritional benefits according to pet humanization trends. Pet ownership rates have increased because elderly residents of Tokyo and Osaka who belong to the changing household demographic system now own pets. The country’s stringent food safety and quality standards which comply with government regulations drive manufacturers to use modern hygienic processing methods.

India

In 2025 India held a market share of 14% which resulted from rising pet ownership and an expanding middle-class population who live in urban areas alongside increasing knowledge about pet health and nutrition. The three major cities of Mumbai, Delhi and Bengaluru face growing demand for processed pet food because their residents adopt new consumer habits which allow them to spend more money. Government support for food processing industries together with agro-based manufacturing development programs leads to higher domestic production investments.

Australia

Australia held a market share of 11% in 2025 because many people own pets and the country has developed comprehensive pet care services. Consumers show strong demand for pet food products which have premium quality organic ingredients and balanced nutritional content. The implementation of government food safety regulations and quality standards and labeling standards has led manufacturers to adopt advanced processing technologies while establishing compliance-driven manufacturing systems.

The remaining share of approximately 23% is distributed across other Asia Pacific countries not covered in the above analysis.

Competitive Landscape / Company Insights

The market shows moderate competition because both international and local companies operate in the market and they use technology development, capacity growth and regional distribution methods to compete. Companies are investing in three main areas which include automation systems, advanced processing technologies and quality control systems to enhance their competitive strength in the market. The combination of government-created regulatory frameworks together with food safety standards and international public health guidelines leads organizations to develop compliant innovations which compete with ongoing regional manufacturing and supply chain enhancement investments.

Mini Profiles

ADM focuses on pet nutrition ingredients and feed solutions, supported by global supply chains, sourcing capabilities, and extensive distribution networks ensuring cost efficiency and consistent product availability.

Blue Buffalo Pet Products Inc. operates in premium pet food segments, emphasizing natural ingredients, protein formulations, and brand-driven marketing, appealing to health-conscious consumers seeking quality nutrition and pet care solutions.

Diamond Pet Foods operates in mass pet food segments, emphasizing affordability, production, and retail presence, delivering nutrition products through efficient manufacturing processes and extensive distribution across domestic and international markets.

Farmina Pet Foods leverages research and partnerships with veterinarians to develop premium pet nutrition products, expanding market presence through localized manufacturing, strong brand positioning, and distribution networks across global regions.

General Mills Inc. focuses on branded pet food offerings, supported by brand recognition through Blue Buffalo, retail distribution, and marketing capabilities, strengthening its position in the competitive pet care market.

Key Players

- ADM

- Blue Buffalo Pet Products Inc.

- Diamond Pet Foods

- Farmina Pet Foods

- General Mills Inc.

- Hill's Pet Nutrition Inc.

- Mars Petcare Ltd

- Nestle Purina Petcare

- Unicharm Corporation

- Wellness Pet Company

Recent Developments

In July 2025, Farmina expanded its premium natural diet portfolio with new high-protein and grain-free formulations targeting health-conscious pet owners. In February 2026, the company strengthened its global distribution network to expand presence across Asia and Europe.

In June 2025, General Mills expanded its pet segment through innovation in Blue Buffalo’s fresh and natural pet food offerings. In January 2026, the company increased investments in premium pet nutrition to capitalize on rising demand for high-quality formulations.

In April 2025, Hill’s introduced enhanced veterinary diet formulas focusing on immunity and digestive health. In November 2025, the company expanded science-backed product lines tailored for age-specific and condition-based pet nutrition.

In March 2026, Unicharm established its first pet food manufacturing plant in China to tap rising regional demand. In September 2025, the company expanded its pet care portfolio across Asia with new hygiene and nutrition products.

In August 2025, Wellness Pet Company launched new natural and functional pet food lines focused on holistic nutrition. In January 2026, the company expanded product availability through e-commerce and specialty retail channels to strengthen market reach.

Asia Pacific Pet Food Processing Market Coverage

Equipment Type Insight and Forecast 2026 - 2035

- Mixing and blending equipment

- Extrusion equipment

- Drying and cooling equipment

- Coating equipment

- Others

Process Type Insight and Forecast 2026 - 2035

- Dry pet food processing

- Wet pet food processing

- Semi moist pet food processing

Application Insight and Forecast 2026 - 2035

- Dog food

- Cat food

- Others

Asia Pacific Pet Food Processing Market by Region

- China

- By Equipment Type

- By Process Type

- By Application

- Japan

- By Equipment Type

- By Process Type

- By Application

- India

- By Equipment Type

- By Process Type

- By Application

- South Korea

- By Equipment Type

- By Process Type

- By Application

- Vietnam

- By Equipment Type

- By Process Type

- By Application

- Thailand

- By Equipment Type

- By Process Type

- By Application

- Malaysia

- By Equipment Type

- By Process Type

- By Application

- Rest of Asia-Pacific

- By Equipment Type

- By Process Type

- By Application

Table of Contents for Asia Pacific Pet Food Processing Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Equipment Type

1.2.2. By

Process Type

1.2.3. By

Application

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Asia Market Estimate and Forecast

4.1. Asia Market Overview

4.2. Asia Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Equipment Type

5.1.1. Mixing and blending equipment

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Extrusion equipment

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Drying and cooling equipment

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Coating equipment

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Others

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Process Type

5.2.1. Dry pet food processing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Wet pet food processing

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Semi moist pet food processing

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Dog food

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cat food

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Others

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Equipment Type

6.2. By

Process Type

6.3. By

Application

7. Japan Market Estimate and Forecast

7.1. By

Equipment Type

7.2. By

Process Type

7.3. By

Application

8. India Market Estimate and Forecast

8.1. By

Equipment Type

8.2. By

Process Type

8.3. By

Application

9. South Korea Market Estimate and Forecast

9.1. By

Equipment Type

9.2. By

Process Type

9.3. By

Application

10. Vietnam Market Estimate and Forecast

10.1. By

Equipment Type

10.2. By

Process Type

10.3. By

Application

11. Thailand Market Estimate and Forecast

11.1. By

Equipment Type

11.2. By

Process Type

11.3. By

Application

12. Malaysia Market Estimate and Forecast

12.1. By

Equipment Type

12.2. By

Process Type

12.3. By

Application

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Equipment Type

13.2. By

Process Type

13.3. By

Application

14. Company Profiles

14.1.

ADM

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

Blue Buffalo Pet Products Inc.

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

Diamond Pet Foods

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

Farmina Pet Foods

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

General Mills Inc.

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

Hill's Pet Nutrition Inc.

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Mars Petcare Ltd

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

Nestle Purina Petcare

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

Unicharm Corporation

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

14.10.

Wellness Pet Company

14.10.1.

Snapshot

14.10.2.

Overview

14.10.3.

Offerings

14.10.4.

Financial

Insight

14.10.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Asia Pacific Pet Food Processing Market