Europe Pet Food Processing Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Equipment Type (Forming Equipment, Extrusion Equipment, Drying Equipment, Coating Equipment, Mixing & Blending Equipment), by Animal Type (Dog, Cat, Others), by Pet Food Type (Dry Pet Food, Wet Pet Food, Semi-Moist Pet Food)

| Status : Published | Published On : Apr, 2026 | Report Code : VRCG7053 | Industry : Consumer Goods | Available Format :

|

Page : 135 |

Europe Pet Food Processing Market Overview

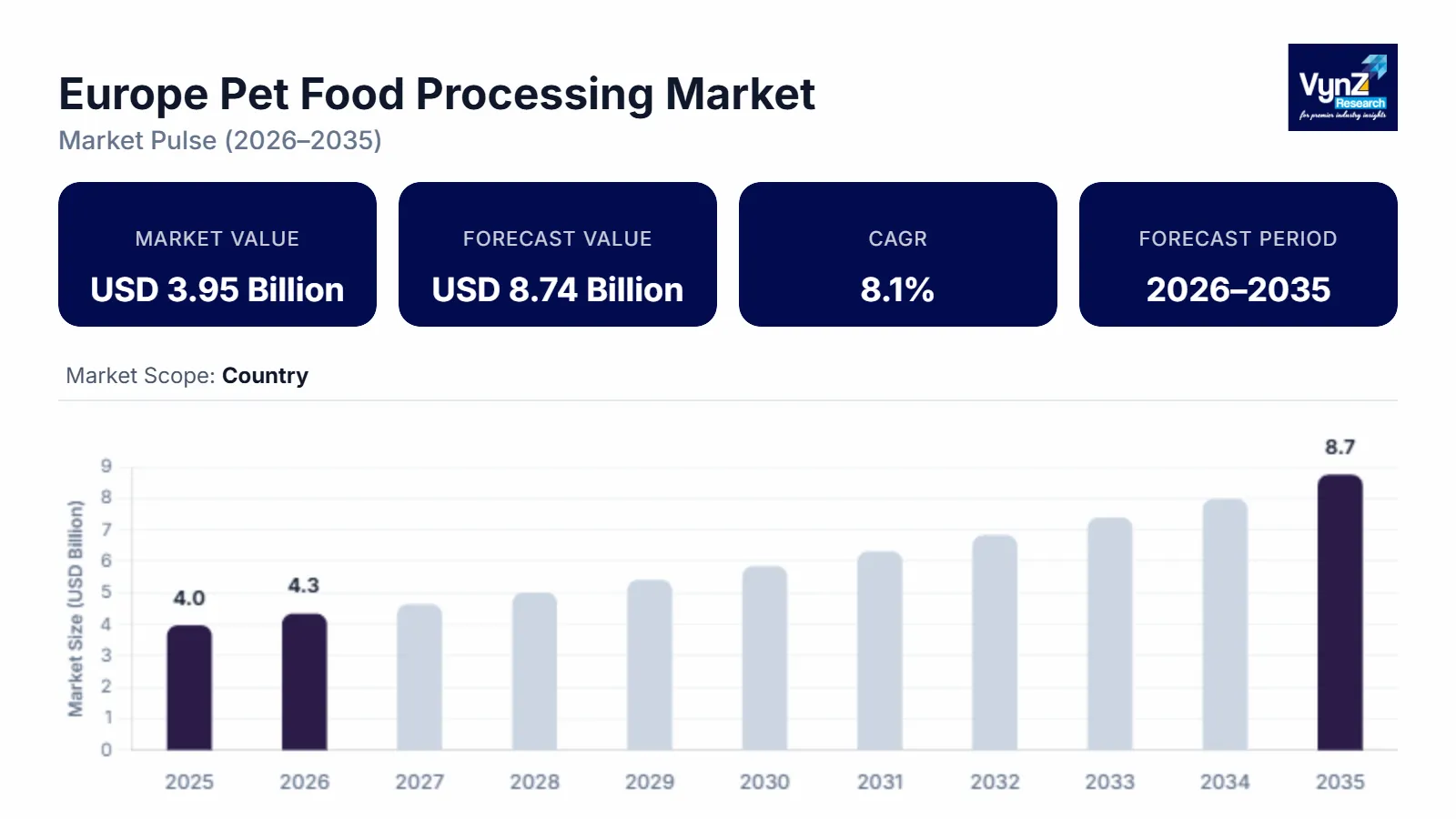

The Europe pet food processing market which was valued at approximately USD 3.95 billion in 2025 and is estimated to rise further up to almost USD 4.32 billion by 2026, is projected to reach around USD 8.74 billion by 2035 while growing at a compound annual growth rate of 8.1% between 2026 and 2035.

The market shows constant growth because more people own pets and they spend more money on high-quality pet food. European Commission and national animal welfare authority reports indicate that companion animal populations have steadily increased which leads to increased production of balanced pet food products. The market receives backing from the rising need for specialized pet diets and functional nutrition products which leads manufacturers to modernize their processing systems and production plants throughout various European nations.

Market expansion is fueled by two major trends which include increasing pet humanization and rising demand for premium and natural pet food products as well as the introduction of better food processing technologies which include extrusion, drying, coating systems and automated processing solutions. The market growth in Germany, France, and the United Kingdom gets support from two factors which include the rising demand for premium pet nutrition products and the ongoing investment in food safety compliance and processing infrastructure development. The European Food Safety Authority and public veterinary health authorities provide ongoing regulatory guidance which establishes better pet food manufacturing standards and drives pet food manufacturers to adopt improved processing technologies while supporting the growth of the European pet nutrition industry.

Europe Pet Food Processing Market Dynamics

Market Trends

The market experiences fundamental shifts through advancements in production technologies and changes in consumer buying behavior. The sector experiences its main development through the increasing demand for premium pet food products which contain high quality components and scientifically designed diets for companion animals. European households are experiencing more pet humanization which leads to rising pet ownership. According to European Commission and veterinary health authorities report, producers are moving towards better extrusion, coating and drying technologies which preserve ingredient quality and nutritional content of their products.

Manufacturing facilities now implement automated food processing equipment with digital control systems as an upcoming trend in their operations. European Food Safety Authority supports regulatory frameworks require pet food producers to follow mandatory food safety standards and maintain traceability of their products while using hygienic processing techniques during production. European food manufacturing sector requires companies to implement integrated energy-efficient processing systems because this approach improves productivity while enhancing quality control and enabling compliance with developing regulatory requirements.

Growth Drivers

European countries show increasing companion animal ownership which drives the market growth because this trend creates ongoing demand for nutritionally balanced pet food products. European Commission reports reveal that pet population growth and increased household spending on pet food have resulted in higher production levels within the pet food manufacturing sector.

Consumers become more aware about pet health and dietary needs which drives them to buy specialized pet food products made with advanced processing equipment. The food safety programs supported by governments and veterinary health monitoring services create a demand for manufacturers to enhance their processing operations which helps them achieve better production results in the long run.

Market Restraints / Challenges

The market displays positive growth potential but it struggles with various operational obstacles. The production process encounters its main limitation because pet food producers must manage volatile raw material prices for meat derivatives and cereals and nutritional additives. International food authorities report that agricultural monitoring shows variations in livestock production and feed ingredient supply which affect both manufacturing costs and profitability.

Manufacturers face additional challenges because they must comply with strict regulatory requirements which control European food production processes. The European Food Safety Authority establishes standards which demand organizations to implement quality control and traceability and labeling requirements that increase their operational expenses and require them to continuously invest in both advanced processing systems and technically trained staff.

Market Opportunities

The market creates business prospects through its need for developing premium pet food products which have special functional benefits because consumers learn more about animal health and nutrition. The European veterinary nutrition programs together with animal welfare initiatives lead to higher demand for advanced processing technologies which help businesses create scientifically balanced diets.

Sustainable manufacturing practices together with energy efficient manufacturing methods present the next business opportunity for companies. European policy initiatives which promote sustainable food systems drive manufacturers to implement automated processing systems and energy-efficient equipment, which help them achieve better production output, while decreasing their environmental footprint. This development opens new business opportunities for the regional pet food processing industry.

Europe Pet Food Processing Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.95 Billion |

|

Revenue Forecast in 2035 |

USD 8.74 Billion |

|

Growth Rate |

8.1% |

|

Segments Covered in the Report |

Equipment Type, Animal Type, Pet Food Type |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Western Europe, Eastern Europe, Rest of Europe |

|

Key Companies |

ADM, Affinity Petcare SA, Andritz AG, Colgate-Palmolive Company, GEA Group AG, Heristo AG, Hillenbrand Inc, Mars Incorporated, Nestle, The Middleby Corp |

|

Customization |

Available upon request |

Europe Pet Food Processing Market Segmentation

By Equipment Type

The market of 2025 saw its highest share from forming equipment which generated approximately 29% of total revenue for that segment. The segment achieves its dominant position because it functions as the primary manufacturing method which creates dry kibble and structured pet food products through large scale production processes. European pet food manufacturers utilize forming systems to achieve consistent product dimensions and uniform texture throughout their production process. Advanced forming technology demand in Germany, France and the United Kingdom will continue to grow because of ongoing production capacity expansion projects across these nations. The segment will experience a growth rate of almost 7.9% during the forecast period as manufacturers implement automated forming equipment to boost their operational productivity.

Coating equipment will achieve the highest growth rate during the period from 2026 to 2035 which will show a projected CAGR of 8.6%. The market expansion occurs because customers demand pet food products which have enhanced flavors and additional nutrients whereas coating technologies enable food manufacturers to distribute fats oils vitamins and palatability enhancers across their products. Premium pet food manufacturers in Europe are turning to advanced coating systems which create better taste and higher nutritional value and unique product differences.

By Animal Type

Dog food processing accounted for the largest share of the market in 2025, representing approximately 46% of segment revenue. The large dog population in European homes establishes this segment as the dominant market force because people want their dogs to have balanced nutritional diets. Dog owners now spend more money on high quality specialized diets which leads manufacturers to produce different types of dry and wet dog food. The segment will experience a growth rate of 8.1% during the forecast period because premium and functional pet nutrition products continue to rise in demand throughout the region.

Cat food processing will experience faster market expansion than other segments because its estimated CAGR will reach 8.5% until 2035. The rising adoption of cats as companion animals across urban European households is driving higher demand for specialized cat food formulations. The growing public understanding of feline diet needs and the increased availability of premium wet food and nutrient enriched products push manufacturers to enhance their production capabilities for cat diets throughout the regional pet food processing industry.

By Pet Food Type

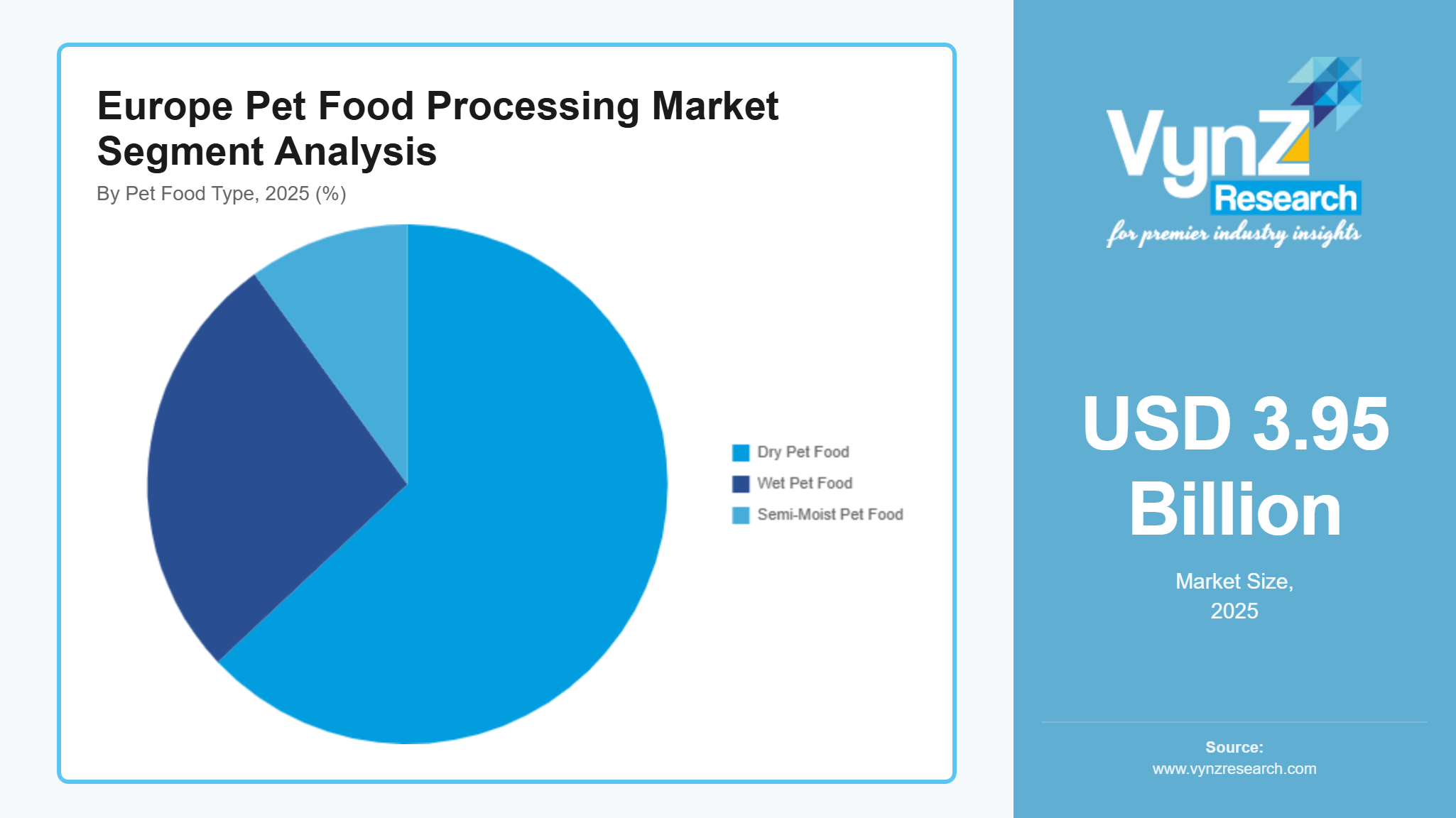

The market of 2025 reached its highest share from dry pet food processing which generated almost 63% of total revenue for that segment. The segment achieves success because customers widely choose its products which offer an extended shelf life and economical pricing and easy storage options. Advanced extrusion, forming and drying technologies are needed for large scale dry kibble production which creates a need for processing equipment in European manufacturing plants. The segment will expand at a CAGR of 7.8% during the forecast period because pet owners prefer to use feeding solutions that require minimal effort.

Wet pet food processing will expand at a quicker rate because its market will grow at an estimated CAGR of 8.4% from 2026 until 2035. The market growth supports itself through rising consumer demand for pet diets which provide high protein content and natural animal food similarities. The trend of premiumization in European pet nutrition markets drives companies to enhance their wet pet food production capabilities through advanced mixing, sterilization and packaging technologies.

Regional Insights

Western Europe

Western Europe held 41% of the market in 2025 because its pet food manufacturing system and consumer demand for premium pet nutrition products. Germany, France, the United Kingdom, and the Netherlands serve as primary production and consumption centers because they have advanced food processing facilities and efficient retail distribution systems. The European Commission and regional veterinary health authorities report that Western Europe has one of the highest rates of companion animal ownership which creates ongoing demand for processed pet food. The European Food Safety Authority requires food safety regulations which receive government support to drive manufacturers toward using better processing technology and automated manufacturing equipment that enhances their production efficiency and product quality in all areas.

Eastern Europe

Eastern Europe holds 21% of the regional market which experiences steady growth because more people own pets and food manufacturing facilities receive more investment. Poland, the Czech Republic and Hungary have become key production and distribution centers for pet nutrition products which they supply to the entire region. European Union funding supports government programs for agricultural development and manufacturing modernization to help companies replace outdated food processing equipment with better technology and increase their local production capacity. People with higher disposable income and better knowledge about companion animal health are driving more packaged pet food consumption which creates steady growth for the regional processing sector.

Rest of Europe

The Rest of Europe holds 15% of the market which sees growth from urban areas and pet food stores that enter smaller markets in multiple countries. Spain, Italy and the Nordic nations have rising demand for premium pet nutrition products because consumers now understand how animal health depends on dietary quality. European regulatory frameworks establish government-supported animal welfare programs and food safety regulations which create incentives for manufacturers to produce high-quality pet food. The market distribution shows 23% across emerging European economies which extend beyond the regional classifications while the European pet food processing sector experiences growth through manufacturing expansion and long-term industry evolution.

Competitive Landscape / Company Insights

The market has a moderate level of competition because both international and local businesses compete through their technological advancements and equipment performance and their efforts to enter new markets. Manufacturers are investing in advanced extrusion systems, automated coating technologies and energy efficient processing equipment to enhance their production capabilities. The European Food Safety Authority and other organizations create regulatory frameworks and food safety guidelines that enable businesses to achieve exceptional manufacturing quality standards. The European pet food manufacturing sector benefits from these policy environments because they promote ongoing investments in processing technologies and enhance competitive advantages for companies within the industry.

Mini Profiles

ADM focuses on large scale ingredient processing and animal nutrition solutions, supported by extensive global supply chains, strong commodity sourcing capabilities, and efficient manufacturing systems that reinforce presence in industrial pet food production.

Buhler Industries Inc operates in specialized processing equipment segments, emphasizing precision engineering and high-performance manufacturing systems that support efficient pet food production, backed by strong industrial design expertise and equipment reliability.

Colgate-Palmolive Company leverages strong brand recognition and established distribution networks to expand presence in pet nutrition markets, offering scientifically formulated pet food products supported by extensive consumer trust and veterinary backed product development.

GEA Group AG focuses on advanced food processing technologies, supported by global engineering expertise, strong industrial automation capabilities, and energy efficient equipment solutions that strengthen production efficiency in pet food manufacturing facilities.

Hillenbrand Inc operates in industrial processing and equipment solutions, emphasizing engineering innovation and customized manufacturing systems that enhance production scalability, supported by diversified industrial technologies and global service networks.

Key Players

- ADM

- Affinity Petcare SA

- Andritz AG

- Colgate-Palmolive Company

- GEA Group AG

- Heristo AG

- Hillenbrand Inc

- Mars Incorporated

- Nestle

- The Middleby Corp

Recent Developments

Affinity Petcare SA expanded its premium pet nutrition portfolio across European markets in March 2026, focusing on science-based formulations and strengthening regional distribution networks to meet rising demand for specialized pet diets.

Mars Incorporated partnered with Big Idea Ventures in October 2025 to launch the Next Generation Pet Food Program, supporting startups developing biotech ingredients, sustainable nutrients, and circular feed innovations for future pet nutrition solutions.

Nestle opened a new wet pet food manufacturing facility in Brazil in March 2026 with an investment of about 370 million, significantly increasing production capacity and supporting export demand in global pet nutrition markets.

ADM announced a strategic animal feed joint venture with Alltech in September 2025, combining feed mill assets and technical expertise to strengthen animal nutrition solutions and improve operational efficiency in feed and pet nutrition sectors.

GEA Group AG supported the global Next Generation Pet Food innovation program with partners including Mars and Bühler in June 2025, helping accelerate development of sustainable ingredients and advanced pet food processing technologies.

Europe Pet Food Processing Market Coverage

Equipment Type Insight and Forecast 2026 - 2035

- Forming Equipment

- Extrusion Equipment

- Drying Equipment

- Coating Equipment

- Mixing & Blending Equipment

Animal Type Insight and Forecast 2026 - 2035

- Dog

- Cat

- Others

Pet Food Type Insight and Forecast 2026 - 2035

- Dry Pet Food

- Wet Pet Food

- Semi-Moist Pet Food

Europe Pet Food Processing Market by Region

- Germany

- By Equipment Type

- By Animal Type

- By Pet Food Type

- U.K.

- By Equipment Type

- By Animal Type

- By Pet Food Type

- France

- By Equipment Type

- By Animal Type

- By Pet Food Type

- Italy

- By Equipment Type

- By Animal Type

- By Pet Food Type

- Spain

- By Equipment Type

- By Animal Type

- By Pet Food Type

- Russia

- By Equipment Type

- By Animal Type

- By Pet Food Type

- Rest of Europe

- By Equipment Type

- By Animal Type

- By Pet Food Type

Table of Contents for Europe Pet Food Processing Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Equipment Type

1.2.2. By

Animal Type

1.2.3. By

Pet Food Type

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Equipment Type

5.1.1. Forming Equipment

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Extrusion Equipment

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Drying Equipment

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Coating Equipment

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Mixing & Blending Equipment

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Animal Type

5.2.1. Dog

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Cat

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Others

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Pet Food Type

5.3.1. Dry Pet Food

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Wet Pet Food

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Semi-Moist Pet Food

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Equipment Type

6.2. By

Animal Type

6.3. By

Pet Food Type

7. U.K. Market Estimate and Forecast

7.1. By

Equipment Type

7.2. By

Animal Type

7.3. By

Pet Food Type

8. France Market Estimate and Forecast

8.1. By

Equipment Type

8.2. By

Animal Type

8.3. By

Pet Food Type

9. Italy Market Estimate and Forecast

9.1. By

Equipment Type

9.2. By

Animal Type

9.3. By

Pet Food Type

10. Spain Market Estimate and Forecast

10.1. By

Equipment Type

10.2. By

Animal Type

10.3. By

Pet Food Type

11. Russia Market Estimate and Forecast

11.1. By

Equipment Type

11.2. By

Animal Type

11.3. By

Pet Food Type

12. Rest of Europe Market Estimate and Forecast

12.1. By

Equipment Type

12.2. By

Animal Type

12.3. By

Pet Food Type

13. Company Profiles

13.1.

ADM

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Affinity Petcare SA

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Andritz AG

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Colgate-Palmolive Company

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

GEA Group AG

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Heristo AG

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Hillenbrand Inc

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Mars Incorporated

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Nestle

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

The Middleby Corp

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Pet Food Processing Market