Electric Insulator Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Dielectric Material (Ceramic / Porcelain, Glass, Composite / Polymer), by Voltage Rating (Low Voltage, Medium Voltage, High Voltage, Extra-High Voltage), by Installation Environment (Indoor, Outdoor), by Application (Transmission Lines and Cables, Substations and Switchgear, Transformers and Bushings, Surge and Lightning Protection), by Product Type (Pin and Shackle Insulators, Suspension Insulators, Specialized Insulators), by End User (Utilities, Industrial / Commercial, Residential)

| Status : Published | Published On : Feb, 2026 | Report Code : VREP3052 | Industry : Energy & Power | Available Format :

|

Page : 185 |

Electric Insulator Market Overview

The electric insulator market which was valued at approximately USD 20.76 billion in 2025 and is estimated to rise further up to almost USD 22.03 billion by 2026, is projected to reach around USD 37.53 billion by 2035, expanding at a CAGR of about 6.1% during the forecast period from 2026 to 2035.

Market expansion is driven by sustained transmission and distribution infrastructure upgrades increasing grid reliability requirements and accelerating renewable energy integration across utility networks. Government led power sector modernization initiatives supported by the U.S. Department of Energy, the European Commission Energy Directorates, and national electricity authorities across Asia Pacific are reinforcing long term demand across the global power infrastructure landscape.

Adoption is further supported by regulatory and safety frameworks promoted by public institutions such as the International Electrotechnical Commission and occupational safety guidelines aligned with recommendations from the World Health Organization related to electrical safety and risk mitigation. National rural electrification programs smart grid development plans and renewable energy evacuation policies backed by public funding authorities are emphasizing durable and high-performance insulation systems to reduce transmission losses and operational hazards. Continued public investment across North America, Europe and Asia Pacific in grid expansion energy efficiency and system resilience remains a key contributor to sustained demand from utilities and large-scale industrial users.

Electric Insulator Market Dynamics

Market Trends

The electric insulator industry is experiencing a gradual shift toward advanced materials and higher performance insulation solutions aligned with evolving grid reliability and safety requirements defined by public energy authorities. Utilities are increasingly adopting composite and polymer-based insulators to improve contamination resistance, reduce maintenance frequency and enhance lifecycle performance across transmission and distribution networks. Government backed grid modernization programs promoted by institutions such as the U.S. Department of Energy and the European Commission emphasize improved asset durability and reduced outage risks, encouraging replacement of aging porcelain installations across high voltage corridors.

Another notable trend is the rising specification of insulators designed for renewable energy evacuation and climate resilient infrastructure. Regulatory frameworks issued by bodies such as the Central Electricity Authority in India and transmission system operators across Europe increasingly account for extreme weather exposure, pollution levels and load variability. This has driven demand for insulators capable of operating under higher mechanical stress and environmental contamination while maintaining electrical performance. These developments are reshaping procurement standards and influencing manufacturers to prioritize material innovation, testing compliance and long-term reliability.

Growth Drivers

Expansion of transmission and distribution infrastructure remains a primary driver for the market as governments prioritize grid reinforcement to meet rising electricity demand. Public investment programs targeting network expansion, loss reduction and rural electrification supported by national energy ministries and power authorities are generating sustained demand for line and substation insulation components. Large scale transmission projects supported by multilateral development banks and public funding mechanisms further reinforce consistent procurement across developing and emerging economies.

The accelerated integration of renewable energy is another major growth driver influencing insulation demand. Wind, solar and hybrid power projects require extensive high voltage transmission infrastructure to evacuate power from remote generation sites to consumption centers. Government renewable energy targets and grid codes issued by authorities such as the International Energy Agency and national electricity regulators mandate robust insulation systems to manage voltage fluctuations and variable load conditions, supporting steady adoption across utility scale projects.

In addition, regulatory emphasis on electrical safety and system reliability continues to strengthen market fundamentals. Guidelines aligned with recommendations from organizations such as the World Health Organization and national occupational safety agencies highlight the importance of minimizing electrical hazards and preventing infrastructure failures. Compliance driven upgrades of aging grid assets are therefore contributing to replacement demand across mature power systems.

Market Restraints / Challenges

Despite favorable long-term outlooks, the market faces challenges related to raw material cost volatility and supply chain dependency. Government trade and industrial policy reports highlight periodic fluctuations in ceramic minerals, fiberglass and polymer feedstocks which can affect manufacturing costs and pricing stability. These pressures are particularly significant for price sensitive utilities in emerging markets where procurement decisions are closely linked to public budget allocations and regulated tariff structures.

Another constraint involves compliance complexity associated with evolving technical and environmental standards. National grid authorities and international standardization bodies continue to update performance and testing requirements for high voltage insulation systems. Manufacturers must invest continuously in certification testing and product adaptation to meet region specific regulations. This increases operational costs and can slow product commercialization, particularly for smaller suppliers with limited access to capital and testing infrastructure.

Market Opportunities

Significant opportunities are emerging from large scale grid refurbishment and asset replacement programs across aging power networks. Government backed infrastructure assessments conducted by authorities such as the U.S. Department of Energy and European transmission regulators highlight the need to replace legacy insulation assets that have exceeded their operational life. Suppliers offering high durability, low maintenance solutions are well positioned to capture incremental demand arising from refurbishment focused capital expenditure programs.

Another major opportunity lies in the expansion of power infrastructure across developing economies supported by public electrification and industrialization initiatives. National development plans issued by energy ministries in Asia Pacific, the Middle East and Africa emphasize new transmission corridors, industrial parks and renewable integration zones. Advancements in material engineering and smart monitoring compatible insulation systems are expected to further enhance adoption by improving reliability, reducing outage risks and supporting long term grid resilience.

Global Electric Insulator Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 20.76 Billion |

|

Revenue Forecast in 2035 |

USD 37.53 Billion |

|

Growth Rate |

6.1% |

|

Segments Covered in the Report |

By Dielectric Material, By Voltage Rating, By Installation Environment, By Application, By Product Type, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Asia Pacific, Europe, GCC and Middle East, Other Regions |

|

Key Companies |

Aditya Birla Insulators, Bharat Heavy Electricals Ltd (BHEL), Dalian Insulator Group, GE Grid Solutions / General Electric Company, Hitachi Energy Ltd, Hubbell Inc / Hubbell Power Systems, Lapp Insulators GmbH, MacLean Power Systems / MacLean-Fogg Company, NGK Insulators Ltd, Olectra Greentech, PPC Insulators, Preformed Line Products (PLP), Seves Group, Siemens AG / Siemens Energy, TE Connectivity Ltd, Toshiba Corporation, Zhejiang Tailun Insulator / Zhejiang TCI Composite Insulators |

|

Customization |

Available upon request |

Electric Insulator Market Segmentation

By Dielectric Material

Ceramic and porcelain insulators are projected to account for approximately 48% of total market revenue in 2025. Their dominance reflects extensive adoption in high voltage transmission lines and substations, driven by reliability, long replacement cycles, and compliance with safety and performance standards established by authorities such as the U.S. Department of Energy and India’s Central Electricity Authority. Government-backed grid modernization programs reinforce their continued deployment across mature and emerging networks.

Glass insulators are witnessing steady growth with a CAGR of approximately 5.8% during 2026 to 2035, supported by increasing demand for corrosion-resistant, long-life solutions in outdoor installations.

Composite and polymer insulators are expected to register the fastest growth, at an estimated CAGR of 7.3%, driven by innovation in lightweight materials, climate-resilient infrastructure, and regulatory focus on sustainable and low-maintenance insulation solutions.

By Voltage Rating

Medium voltage insulators hold the largest market share, accounting for roughly 42% of revenue in 2025. Their prominence stems from deployment in regional distribution networks, industrial microgrids, and urban electrification programs backed by national energy authorities and public infrastructure initiatives.

High voltage insulators are estimated to grow at a CAGR of 6.9%, driven by expansion of long-distance transmission lines, renewable energy evacuation projects, and government mandates for grid reliability.

Low voltage insulators are expected to record a CAGR of around 5.2%, benefiting from residential, commercial, and small industrial adoption where safety, efficiency, and regulatory compliance remain critical.

Extra-high voltage applications are also emerging, projected to grow at a CAGR of 7.1% due to cross-border and high-capacity transmission projects.

By Installation Environment

Outdoor insulators are projected to dominate the market in 2025, accounting for approximately 63% of total revenue. Their largest share is attributed to extensive use in transmission lines, substations, and renewable energy corridors, where exposure to extreme weather and environmental stress necessitates durable and low-maintenance insulation. Government safety regulations and grid codes support this deployment.

Indoor insulators are expected to grow at a CAGR of 6.2%, driven by rising industrial automation, compact distribution networks, and compliance with occupational safety and electrical hazard mitigation guidelines. Demand for indoor applications is also being reinforced by modernization of transformer rooms, switchgear installations, and industrial facilities in emerging economies.

By Application

Transmission lines and cables account for the largest share, approximately 45% of market revenue in 2025. Their prominence is supported by public electrification programs, rural transmission upgrades, and renewable power evacuation infrastructure guided by national energy authorities and international safety standards.

Substations and switchgear applications are expected to grow at a CAGR of 6.8%, driven by grid modernization programs and regulatory mandates to enhance operational reliability.

Transformers and bushings are estimated to record a CAGR of 5.9%, supported by infrastructure upgrades and energy efficiency initiatives.

Surge and lightning protection applications, while smaller in base revenue, are projected to grow fastest at around 7.2% CAGR due to increasing awareness of environmental hazards and government-backed protective measures.

By Product Type

Pin and shackle insulators hold the largest share, approximately 54% of total market revenue in 2025, reflecting their wide applicability in conventional distribution and utility networks and adherence to long-established performance standards.

Suspension and specialized insulator designs are projected to register a CAGR of 7.1%, driven by adoption in high voltage transmission lines, renewable integration projects, and climate-resilient infrastructure. Innovation in material composition, lightweight structures, and modular installation techniques further accelerates their adoption across developed and emerging markets.

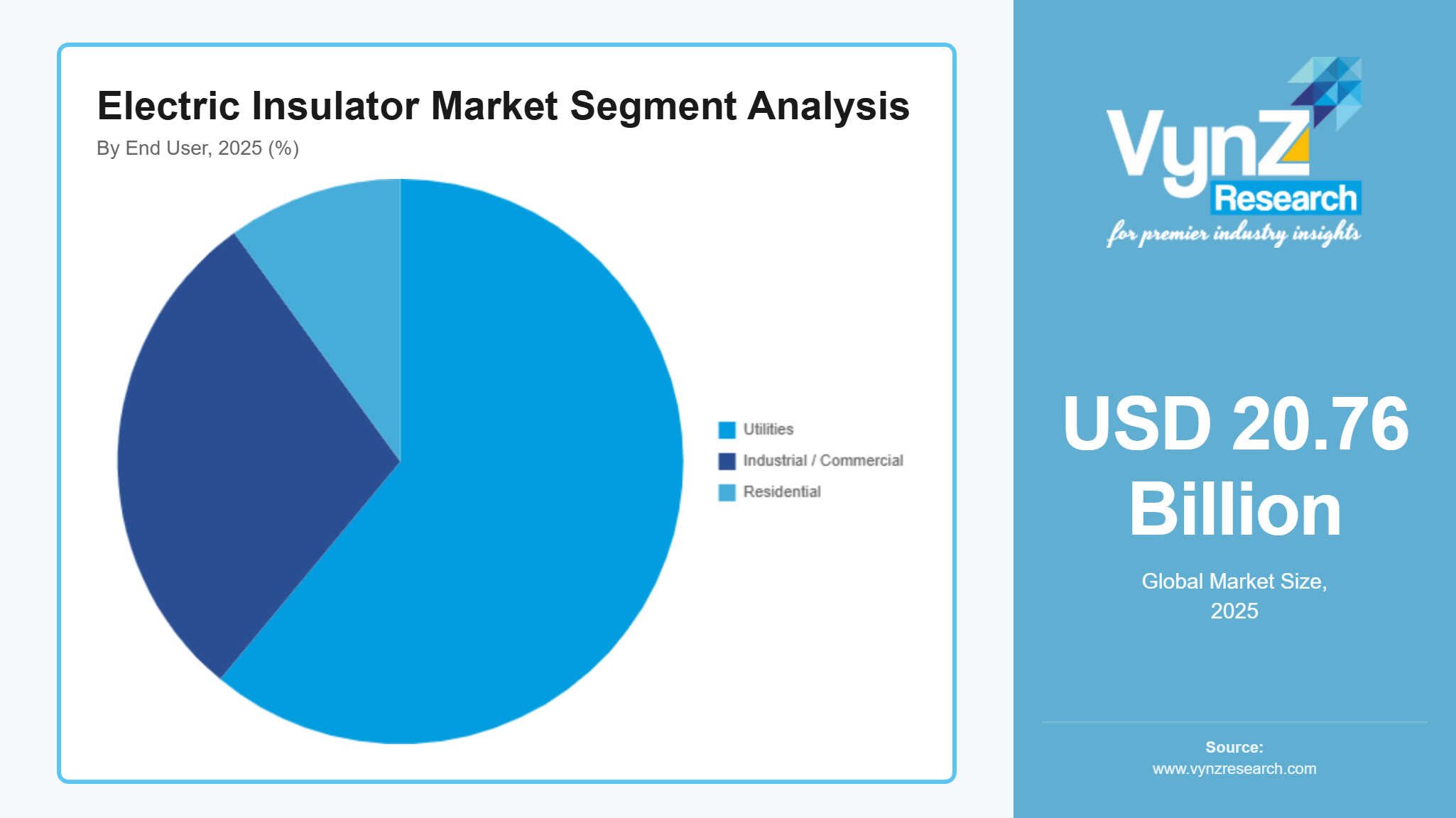

By End User

Utilities account for the largest segment, contributing roughly 61% of total market revenue in 2025. Their share is reinforced by government-backed investments in grid expansion, renewable integration, network modernization programs, and adherence to safety and operational standards across North America, Europe, and Asia Pacific.

Industrial and commercial end users, including manufacturing facilities, airports, railways, and critical infrastructure, are projected to grow at a CAGR of 6.7%, supported by operational reliability requirements, regulatory compliance, and integration with energy management systems.

Residential adoption is expected to record a CAGR of 5.5%, driven by urban electrification initiatives, energy-efficient distribution networks, and rising household electrification rates in developing regions.

Regional Insights

North America

North America is estimated to hold approximately 30% of the market in 2025. The region’s growth is driven by modernization of aging transmission and distribution networks, integration of renewable energy, and enhanced operational safety standards enforced by the U.S. Department of Energy (DOE) and Federal Energy Regulatory Commission (FERC). Utilities in states such as Texas, California, and New York are deploying high-voltage insulators, composite designs, and upgraded substations to improve grid resilience. Government incentives, combined with industrial and urban electrification initiatives, encourage investment in durable insulation solutions, while adoption of smart grids and IEC-compliant infrastructure continues to strengthen market performance.

Asia Pacific

Asia Pacific is projected to account for roughly 34% of the market in 2025. Rapid urbanization, surging electricity demand, and large-scale renewable energy projects are driving adoption of electric insulators. China leads with ultra-high-voltage (UHV) transmission lines, renewable energy evacuation infrastructure, and deployment of porcelain and composite insulators across utilities such as SGCC. In India, programs such as the Resilient and Digital Substation Scheme (RDSS) and national smart grid initiatives accelerate adoption of polymer and ceramic insulators for substations and distribution lines. Growth is supported by high-volume infrastructure development, government-led safety standards, and increased industrial electrification.

Europe

Europe represents approximately 17% of the market in 2025. Growth is supported by decarbonization policies, grid modernization programs, and regulatory compliance for network safety. Germany, the UK, France, and Spain are investing in high-voltage transmission lines, polymer and porcelain insulators, and upgraded substations to maintain reliability and integrate renewable energy. National grid codes and EU directives on electrical safety and environmental protection reinforce adoption, while offshore wind farms and cross-border interconnections drive demand for durable, high-performance insulation products.

GCC and Middle East

The GCC and Middle East are projected to contribute around 9% of total market revenue in 2025. Expansion is supported by large-scale industrial projects, desert-resilient infrastructure, and government initiatives for smart grids and renewable integration. Countries such as Saudi Arabia, UAE, and Qatar are deploying advanced high-voltage and composite insulators for transmission lines and substations to improve system reliability. Strategic investments in power networks and regulatory incentives for modernization are encouraging utilities to adopt lightweight, high-durability solutions suitable for harsh climatic conditions.

Other Regions

The remaining regions, including Latin America and Africa, collectively account for approximately 10% of the global market. Growth is supported by infrastructure development, rural electrification projects, and renewable energy integration. Although adoption is slower compared with North America, Asia Pacific, Europe, and GCC, these regions present long-term opportunities for market expansion and deployment of durable, climate-resilient electric insulators. Government-led modernization programs and regional grid reliability initiatives continue to encourage investment in both urban and semi-urban areas.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional players focusing on product innovation, cost optimization, and geographic expansion. Key vendors are investing in advanced materials, lightweight designs, and climate-resilient insulators to enhance performance. Adoption is supported by government initiatives such as the U.S. DOE Grid Modernization Program, India’s Resilient and Digital Substation Scheme (RDSS), and national electrification and safety standards across Europe and Asia Pacific. These regulatory frameworks encourage companies to strengthen market position and secure long-term utility, industrial, and infrastructure contracts.

Mini Profiles

Aditya Birla Insulators focuses on high-performance ceramic and polymer insulators, supported by strong manufacturing capabilities, cost-efficient production, and extensive distribution, serving utilities and industrial customers across domestic and international markets

Bharat Heavy Electricals Ltd (BHEL) operates in mass-market transmission and distribution solutions, emphasizing reliability, local manufacturing, and standardized quality, supporting renewable integration and modernization projects in India’s power sector.

Dalian Insulator Group leverages strategic partnerships and advanced manufacturing technologies to expand global reach, providing composite and porcelain insulators for high-voltage transmission and distribution applications with consistent performance.

Hitachi Energy Ltd delivers IEC 61850-compliant substations, advanced protection relays, and HV insulator solutions, supported by global engineering expertise, predictive maintenance, and renewable integration capabilities for utility modernization worldwide.

NGK Insulators Ltd specializes in ceramic and glass insulators for high-voltage networks, emphasizing product innovation, energy efficiency, and quality control, backed by global distribution and localized service support for utilities and infrastructure projects.

Key Players

- Aditya Birla Insulators

- Bharat Heavy Electricals Ltd (BHEL)

- Dalian Insulator Group

- GE Grid Solutions / General Electric Company

- Hitachi Energy Ltd

- Hubbell Inc / Hubbell Power Systems

- Lapp Insulators GmbH

- MacLean Power Systems / MacLean-Fogg Company

- NGK Insulators Ltd

- Olectra

- Greentech

- PPC Insulators

- Preformed Line Products (PLP)

- Seves-Group

- Siemens AG / Siemens Energy

- TE Connectivity Ltd

- Toshiba Corporation

- Zhejiang -Tailun-Insulator / Zhejiang TCI Composite Insulators

Recent Developments

In August 2025, Hubbell, a US utility and electrical solutions supplier, has finalized a deal to pay $825 million in cash to Golden Gate Capital's portfolio firm, DMC Power. DMC Power supplies tools and connections to the transmission and utility substation markets. It creates and produces connector technology solutions that are necessary for infrastructure that uses high voltage electricity. With two manufacturing sites in Carson, California, and Olive Branch, Mississippi, as well as numerous distribution centers around North America, the company employs over 350 people.

In August 2025, By enlarging its production facilities in Mysuru, Karnataka, Hitachi Energy India Ltd. has announced an investment of INR 300 crores in its insulation and components business in India. A crucial insulating material used in power and distribution transformers, EHV class high-quality pressboard and laminated board will be produced at a factor of two thanks to the expansion. Hitachi Energy India will upgrade its Mysuru location to an ultra-low carbon pressboard factory by replacing the fossil fuel boiler as part of the development.

In May 2025, The establishment of a new joint venture to localize the production of high-voltage porcelain insulators, a crucial part of the Kingdom's efforts to enhance domestic manufacturing and lessen dependency on imports, is expected to significantly boost Saudi Arabia's power sector. Signed under the Ministry of Energy's auspices, the deal unites Saudi company Greengrid, Al-Ojaimi Industrial Group subsidiary Power Union Co., and China's Dalian Insulators Group. To manufacture high-voltage and extra-high-voltage suspension porcelain insulators for use in electrical transmission and distribution networks, the partnership plans to build a new factory in the Kingdom.

Global Electric Insulator Market Coverage

Dielectric Material Insight and Forecast 2026 - 2035

- Ceramic / Porcelain

- Glass

- Composite / Polymer

Voltage Rating Insight and Forecast 2026 - 2035

- Low Voltage

- Medium Voltage

- High Voltage

- Extra-High Voltage

Installation Environment Insight and Forecast 2026 - 2035

- Indoor

- Outdoor

Application Insight and Forecast 2026 - 2035

- Transmission Lines and Cables

- Substations and Switchgear

- Transformers and Bushings

- Surge and Lightning Protection

Product Type Insight and Forecast 2026 - 2035

- Pin and Shackle Insulators

- Suspension Insulators

- Specialized Insulators

End User Insight and Forecast 2026 - 2035

- Utilities

- Industrial / Commercial

- Residential

Global Electric Insulator Market by Region

- North America

- By Dielectric Material

- By Voltage Rating

- By Installation Environment

- By Application

- By Product Type

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Dielectric Material

- By Voltage Rating

- By Installation Environment

- By Application

- By Product Type

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Dielectric Material

- By Voltage Rating

- By Installation Environment

- By Application

- By Product Type

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Dielectric Material

- By Voltage Rating

- By Installation Environment

- By Application

- By Product Type

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Electric Insulator Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Dielectric Material

1.2.2. By

Voltage Rating

1.2.3. By

Installation Environment

1.2.4. By

Application

1.2.5. By

Product Type

1.2.6. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Dielectric Material

5.1.1. Ceramic / Porcelain

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Glass

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Composite / Polymer

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Voltage Rating

5.2.1. Low Voltage

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Medium Voltage

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. High Voltage

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Extra-High Voltage

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Installation Environment

5.3.1. Indoor

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Outdoor

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Transmission Lines and Cables

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Substations and Switchgear

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Transformers and Bushings

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Surge and Lightning Protection

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Product Type

5.5.1. Pin and Shackle Insulators

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Suspension Insulators

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Specialized Insulators

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.6. By End User

5.6.1. Utilities

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Industrial / Commercial

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Residential

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Dielectric Material

6.2. By

Voltage Rating

6.3. By

Installation Environment

6.4. By

Application

6.5. By

Product Type

6.6. By

End User

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Dielectric Material

7.2. By

Voltage Rating

7.3. By

Installation Environment

7.4. By

Application

7.5. By

Product Type

7.6. By

End User

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Dielectric Material

8.2. By

Voltage Rating

8.3. By

Installation Environment

8.4. By

Application

8.5. By

Product Type

8.6. By

End User

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Dielectric Material

9.2. By

Voltage Rating

9.3. By

Installation Environment

9.4. By

Application

9.5. By

Product Type

9.6. By

End User

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Aditya Birla Insulators

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bharat Heavy Electricals Ltd (BHEL)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Dalian Insulator Group

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

GE Grid Solutions / General Electric Company

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Hitachi Energy Ltd

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Hubbell Inc / Hubbell Power Systems

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Lapp Insulators GmbH

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

MacLean Power Systems / MacLean-Fogg Company

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

NGK Insulators Ltd

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Olectra Greentech

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

PPC Insulators

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Preformed Line Products (PLP)

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

10.13.

Seves Group

10.13.1.

Snapshot

10.13.2.

Overview

10.13.3.

Offerings

10.13.4.

Financial

Insight

10.13.5.

Recent

Developments

10.14.

Siemens AG / Siemens Energy

10.14.1.

Snapshot

10.14.2.

Overview

10.14.3.

Offerings

10.14.4.

Financial

Insight

10.14.5.

Recent

Developments

10.15.

TE Connectivity Ltd

10.15.1.

Snapshot

10.15.2.

Overview

10.15.3.

Offerings

10.15.4.

Financial

Insight

10.15.5.

Recent

Developments

10.16.

Toshiba Corporation

10.16.1.

Snapshot

10.16.2.

Overview

10.16.3.

Offerings

10.16.4.

Financial

Insight

10.16.5.

Recent

Developments

10.17.

Zhejiang Tailun Insulator / Zhejiang TCI Composite Insulators

10.17.1.

Snapshot

10.17.2.

Overview

10.17.3.

Offerings

10.17.4.

Financial

Insight

10.17.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Electric Insulator Market