Dairy Foods Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Milk, Cheese, Yogurt, Butter & Cream, Milk Powder, Ice Cream & Frozen Desserts, Others), by Category (Conventional, Organic), by Nature (Regular, Lactose-Free, Fortified / Functional), by Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail / E-Commerce, Specialty Stores, Direct Sales / Dairy Cooperatives), by End User (Household / Retail Consumers, Foodservice, Food Processing Industry, Bakery & Confectionery Industry)

| Status : Published | Published On : Mar, 2026 | Report Code : VRFB11041 | Industry : Food & Beverage | Available Format :

|

Page : 195 |

Dairy Foods Market Overview

The dairy foods market which was valued at approximately USD 1,029.2 billion in 2025 and is estimated to reach around USD 1,148.6 billion in 2026, is projected to reach close to USD 2,388.7 billion by 2035, expanding at a CAGR of about 8.5% during the forecast period from 2026 to 2035.

The dairy foods market is primarily driven by rising global demand for high-protein and nutrient-rich diets, as consumers increasingly prioritize health, immunity, and functional nutrition. Growing urbanization and higher disposable incomes, particularly in emerging economies such as India and China, are accelerating consumption of packaged milk, yogurt, cheese, and value-added dairy products. Expanding quick-service restaurant chains and Western dietary influence are further boosting demand for cheese and cream-based products across both developed and developing regions. Technological advancements in cold chain logistics, processing, and packaging have improved product shelf life and distribution reach, supporting market expansion. Government support programs, cooperative dairy models, and rural milk procurement networks are strengthening supply chains in major producing nations. Additionally, innovation in lactose-free, organic, probiotic, and fortified dairy products is attracting health-conscious consumers. The rapid growth of e-commerce and modern retail channels is also enhancing product accessibility, thereby sustaining steady global market growth.

Dairy Foods Market Dynamics

Market Trends

Rising demand for high-protein and functional dairy products is being fueled by growing consumer awareness around health, fitness, and preventive nutrition. Products such as Greek yogurt, protein-enriched milk, whey-based beverages, and probiotic curd are increasingly preferred for their muscle-building, digestive, and immunity-supporting benefits. The Government of India has allocated a total outlay of ₹1,568.28 crore under NPDD to strengthen dairy processing and chilling infrastructure. This large-scale infrastructure enhancement supports production of value-added, fortified, and protein-rich dairy products by improving quality, cold chain efficiency, and organized milk collection systems. Urban consumers, especially millennials and working professionals, are incorporating protein-rich dairy into daily diets as part of weight management and active lifestyle routines. The expansion of gym culture and sports nutrition trends is further strengthening demand for fortified dairy drinks and snacks. Additionally, functional ingredients like probiotics, omega-3, and vitamin D are being added to traditional dairy formats to enhance nutritional value. Parents are also opting for fortified milk products to support children’s growth and development. Continuous product innovation and premium positioning are helping manufacturers capture higher margins while meeting evolving health-focused consumption patterns.

Growth Drivers

Increasing global population and rapid urbanization are major drivers of the dairy foods market, as a larger consumer base directly increases overall food demand. Expanding urban centers are changing dietary patterns, with consumers shifting from loose, unprocessed milk to packaged and branded dairy products due to convenience and safety concerns. Urban households typically have higher purchasing power and greater exposure to diversified food options, which boosts demand for value-added products such as cheese, yogurt, butter, and flavored milk. Busy lifestyles in metropolitan areas also increase preference for ready-to-consume and easy-to-store dairy items. The USDA’s Food Infrastructure Improvement Program has allocated approximately $400 million from the American Rescue Plan (FY 2023–2026) to expand capacity for aggregation, processing, storage, transport, and distribution of dairy and other food products. Moreover, improved cold chain infrastructure and organized retail expansion in cities support wider product availability. Population growth in developing regions is further strengthening daily milk consumption as a staple nutritional source. Together, demographic expansion and urban migration continue to create sustained and scalable demand for dairy foods globally.

Market Restraints / Challenges

Volatility in raw milk prices is a significant challenge for the dairy foods market, as fluctuations directly impact production costs and profit margins. Milk prices are highly sensitive to changes in feed costs, weather conditions, fuel prices, and supply-demand imbalances. For instance, droughts or poor harvests can increase cattle feed expenses, raising overall milk procurement costs for processors. Global trade dynamics and export-import policies also influence domestic milk pricing trends. Sudden price spikes reduce manufacturers’ pricing flexibility, while sharp declines can affect farmers’ income sustainability. Small and medium dairy producers are particularly vulnerable to unpredictable price swings. This instability often leads to inconsistent product pricing for consumers and can disrupt long-term supply chain planning across the dairy industry.

Market Opportunities

Rising demand for premium and organic dairy offerings is creating strong growth opportunities within the dairy foods market, as consumers increasingly prioritize quality, safety, and clean-label ingredients. Health-conscious buyers are willing to pay higher prices for products labeled organic, hormone-free, grass-fed, and non-GMO, reflecting growing concerns about chemical residues and artificial additives. Premium dairy categories such as artisanal cheese, A2 milk, specialty yogurt, and gourmet butter are witnessing rising traction, particularly in urban markets. Increasing disposable incomes and exposure to global food trends are encouraging consumers to shift from basic staples to value-added dairy products. The U.S. federal government supports organic dairy through programs under the United States Department of Agriculture (USDA) such as the Organic Certification Cost Share Program (OCCSP), which reimburses organic dairy producers for up to 75% of certification costs, helping small and medium farms adopt organic practices and expand premium organic milk supply. Retailers are also dedicating more shelf space to certified organic and ethically sourced dairy items. Furthermore, transparent sourcing practices and farm-to-table branding strategies are strengthening consumer trust. This premiumization trend not only enhances revenue margins for producers but also supports long-term brand differentiation in a competitive marketplace.

Global Dairy Foods Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1029.2 Billion |

|

Revenue Forecast in 2035 |

USD 2388.7 Billion |

|

Growth Rate |

8.5% |

|

Segments Covered in the Report |

Product Type, Category, Nature, Distribution Channel, End User, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Nestlé S.A., Danone S.A., Lactalis Group, Fonterra Co-operative Group Limited, Arla Foods amba, Royal FrieslandCampina N.V., Dairy Farmers of America, Inc., Saputo Inc., The Kraft Heinz Company, Gujarat Cooperative Milk Marketing Federation Ltd. |

|

Customization |

Available upon request |

Dairy Foods Market Segmentation

By Product Type

Milk is the largest category with a market share of about 35% in 2025, due to its role as a daily staple across households globally. It serves as the primary source of nutrition and is widely consumed across all age groups. Government nutrition programs, school milk schemes, and strong rural consumption further strengthen its dominance. Packaged and fortified milk variants are expanding rapidly in urban areas. Its affordability, high penetration rate, and extensive distribution network maintain its leading position worldwide.

Cheese is the fastest-growing category with a CAGR of 8.7% during the forecast period, driven by increasing westernization of diets and expansion of quick-service restaurant chains. Rising consumption of pizza, burgers, and ready-to-eat meals significantly boosts cheese demand. Emerging economies are witnessing growing adoption due to urbanization and rising disposable incomes. Product innovation in processed, flavored, and specialty cheese variants further accelerates category growth. Improved cold chain infrastructure also supports wider availability.

By Category

Conventional is the largest category with a market share of about 85% in 2025, as it remains more affordable and widely accessible compared to organic alternatives. Large-scale dairy farming and established procurement networks ensure consistent supply. Price-sensitive consumers in developing markets predominantly rely on conventional dairy products. Supermarket penetration and private-label offerings further reinforce dominance. Despite growing health awareness, conventional dairy continues to account for the majority share globally.

Organic is the fastest-growing category with a CAGR of 8.9% during the forecast period, fueled by increasing preference for hormone-free, non-GMO, and clean-label products. Health-conscious consumers are willing to pay premium prices for certified organic milk, yogurt, and cheese. Environmental sustainability concerns are also influencing purchasing decisions. Growth of specialty retail stores and online grocery platforms improves accessibility. Expanding organic dairy farming initiatives further support long-term expansion.

By Nature

Regular is the largest category with a market share of about 80% in 2025, as it represents the standard dairy consumption pattern across global markets. Most consumers continue to prefer traditional dairy products due to taste familiarity and lower cost. Strong supply chain infrastructure ensures large-scale availability. Regular dairy products are deeply integrated into daily diets across both urban and rural regions. Their widespread affordability keeps this segment dominant.

Lactose-Free is the fastest-growing category during the forecast period, driven by increasing awareness of lactose intolerance and digestive health concerns. A growing portion of the population is actively seeking easier-to-digest dairy alternatives. Product diversification across milk, yogurt, and cheese variants strengthens demand. Premium positioning and targeted marketing are further accelerating adoption. Rising health consciousness in developed markets significantly supports growth.

By Distribution Channel

Supermarkets & Hypermarkets is the largest category with a market share of about 45% in 2025, due to their extensive product variety, competitive pricing, and strong cold storage infrastructure. Consumers prefer organized retail for packaged and branded dairy purchases. Promotional discounts and private-label products enhance sales volumes. Urban expansion and rising retail penetration further strengthen dominance. Large shelf space allocation ensures consistent visibility of dairy products.

Online Retail / E-Commerce is the fastest-growing category with a CAGR of 8.8% during the forecast period, driven by increasing digital adoption and convenience-oriented shopping behavior. Subscription-based milk delivery models and quick-commerce platforms are gaining traction. Urban consumers value doorstep delivery of fresh dairy products. Improved cold chain logistics and last-mile delivery infrastructure support online expansion. Growing smartphone penetration further accelerates digital dairy sales.

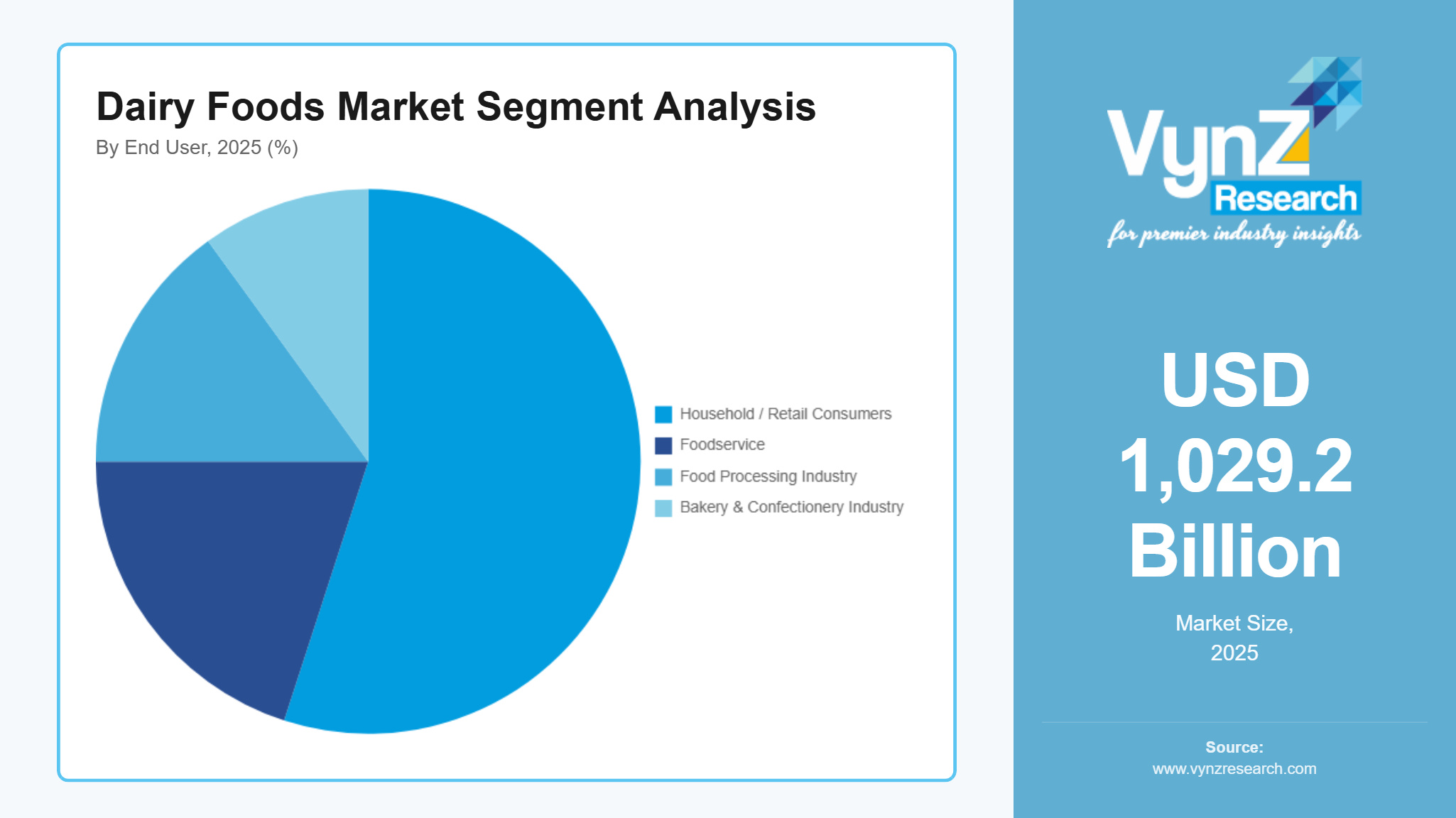

By End User

Household / Retail Consumers is the largest category with a market share of about 55% in 2025, as dairy remains a daily consumption staple in homes worldwide. Regular intake of milk, yogurt, butter, and cheese drives consistent demand. Population growth and urbanization further expand the consumer base. Strong retail distribution networks ensure easy accessibility. Cultural dietary habits also support high household dairy consumption.

Foodservice is the fastest-growing category during the forecast period, supported by rapid expansion of restaurants, cafés, bakeries, and quick-service chains. Rising demand for cheese-based meals, desserts, and dairy beverages fuels growth. Urban lifestyle changes are increasing out-of-home food consumption. Hospitality sector recovery and tourism growth further boost dairy usage. Menu innovation and premium dairy ingredients strengthen long-term expansion.

Regional Insights

North America

North America holds a significant share in the Dairy Foods Market, supported by high per capita dairy consumption and a well-established processing industry. The United States and Canada have advanced cold chain infrastructure and strong retail penetration, ensuring consistent availability of milk, cheese, yogurt, and butter products. Consumer preference for high-protein, organic, and lactose-free dairy options is driving premium segment growth. The Northeast Dairy Business Innovation Center (NE-DBIC), funded through the U.S. Department of Agriculture’s Agricultural Marketing Service, made $1,000,000 available under the Dairy Processor Modernization Grant program to strengthen dairy processing infrastructure. The region also benefits from strong dairy cooperatives and large-scale commercial farms that ensure stability supply. Innovation in functional dairy beverages and probiotic products continues to expand product portfolios. Strict food safety regulations and labeling standards enhance consumer trust. Additionally, growing demand from foodservice chains further supports steady regional expansion.

Asia Pacific

Asia-Pacific is the largest and fastest-growing region in the dairy foods market, driven by high population density and rising disposable incomes in countries such as India, China, and Japan. China’s government has allocated around CNY 500–700 million (approximately USD 70–100 million) through agricultural modernization and food safety programs to establish and upgrade dairy collection centers and milk testing facilities across major dairy-producing provinces. Rapid urbanization is shifting consumption from loose milk to packaged and branded dairy products. Government-backed dairy development programs and cooperative networks strengthen domestic production capacity. Expanding middle-class populations are increasing demand for cheese, yogurt, and flavored dairy products. Western dietary influence and quick-service restaurant expansion are boosting cheese consumption. Improvements in cold chain logistics and modern retail infrastructure enhance market penetration. Strong economic growth and rising nutritional awareness continue to accelerate regional demand.

Europe

Europe represents a mature and well-established dairy market, characterized by strong production capabilities and high export volumes. Countries such as Germany, France, the Netherlands, and Ireland are major dairy producers with advanced processing technologies. The region shows strong demand for specialty cheeses, organic milk, and premium dairy products. France and the Netherlands provide approximately €300–500 million annually in multi-year subsidies to dairy cooperatives for improving milk collection logistics, cold chain networks, and quality testing facilities. In Ireland, the government offers targeted grants of up to €150,000 per farm to help small dairy producers modernize and develop value-added product lines. Sustainability initiatives and animal welfare standards play a significant role in shaping product innovation. European consumers prioritize clean-label and high-quality dairy offerings, supporting premiumization trends. Strict regulatory frameworks ensure high food safety and quality standards. In addition, growing lactose-free and functional dairy segments are contributing to steady market development.

Rest of the World

The Rest of the World, including Latin America, the Middle East, and Africa, is experiencing gradual expansion in dairy consumption. Countries like Brazil and Argentina are strong dairy producers in Latin America, supporting regional supply growth. Brazil supports dairy modernization through low-interest federal agricultural credit programs, with nearly USD 12 billion directed toward farm and processing upgrades. These funds help improve milking systems, cold storage, and processing capacity. Additionally, around R$200 million has been allocated to strengthen domestic dairy competitiveness and production stability. Rising urban populations and improving retail infrastructure are increasing packaged dairy demand. In the Middle East, high reliance on dairy imports is complemented by growing investments in domestic production facilities. African markets are witnessing rising milk consumption supported by population growth and government nutrition initiatives. Although infrastructure gaps remain in some areas, increasing foreign investments and modernization efforts are strengthening supply chains. Expanding foodservice industries and improving cold storage capabilities are expected to support long-term regional growth.

Competitive Landscape / Company Insights

The dairy foods market is moderately fragmented, characterized by the presence of large multinational dairy processors alongside strong regional cooperatives and private-label manufacturers. Global companies such as Nestlé S.A. and Danone S.A. dominate premium and value-added segments including yogurt, infant nutrition, and functional dairy beverages, leveraging extensive distribution networks and strong brand portfolios. Lactalis Group and Fonterra Co-operative Group Limited maintain significant global presence through large-scale milk procurement systems and diversified cheese and milk powder exports, strengthening their international footprint.

Established dairy leaders such as Arla Foods amba and FrieslandCampina N.V. focus on sustainable dairy production, premiumization, and expansion into organic and lactose-free categories. In North America, Dairy Farmers of America, Inc. plays a major role in milk sourcing and private-label production. Meanwhile, regional players and cooperative societies in emerging markets compete through cost efficiency and localized supply chains. Companies are increasingly investing in product innovation, clean-label formulations, and sustainable packaging initiatives to strengthen brand positioning. Despite intense competition, large multinational processors retain advantages in global sourcing capabilities, advanced processing technologies, and long-term retail partnerships.

Mini Profiles

Nestlé S.A. is one of the world’s largest food and beverage companies, with a strong presence in dairy through milk powders, condensed milk, yogurt, and infant nutrition products. The company focuses on value-added and fortified dairy offerings, leveraging advanced R&D capabilities and global distribution networks. Its portfolio emphasizes nutritional enhancement, premiumization, and sustainable sourcing practices across developed and emerging markets.

Danone S.A. is a global leader in fresh dairy products and specialized nutrition, offering yogurt, probiotic drinks, and medical nutrition solutions. The company is recognized for its focus on gut health, immunity-supporting dairy, and plant-based alternatives. Danone integrates sustainability commitments and regenerative agriculture practices into its dairy supply chain strategy.

Lactalis Group is one of the largest dairy product manufacturers globally, specializing in cheese, milk, butter, and cream. The company operates an extensive international production network and exports to numerous countries worldwide. Its diversified brand portfolio and strong milk procurement systems support consistent supply and global expansion.

Fonterra Co-operative Group Limited is a farmer-owned cooperative and a major exporter of dairy ingredients, milk powder, and consumer dairy products. The company plays a significant role in global dairy trade, supplying ingredients to food manufacturers across Asia-Pacific and other regions. Fonterra focuses on sustainability, quality assurance, and large-scale milk processing efficiency.

Arla Foods amba is a leading European dairy cooperative known for its milk, cheese, butter, and organic dairy products. The company emphasizes natural ingredients, clean-label formulations, and carbon reduction initiatives. Its strong farmer ownership structure ensures integrated milk sourcing and long-term supply chain stability across key European markets.

Key Players

- Nestlé S.A.

- Danone S.A.

- Lactalis Group

- Fonterra Co-operative Group Limited

- Arla Foods amba

- Royal FrieslandCampina N.V.

- Dairy Farmers of America, Inc.

- Saputo Inc.

- The Kraft Heinz Company

- Gujarat Cooperative Milk Marketing Federation Ltd.

Recent Developments

January 2026 – Nestlé S.A. announced expansion of its fortified milk and high-protein dairy portfolio in Asia-Pacific, focusing on value-added nutrition products targeting urban consumers and children’s health segments.

December 2025 – Danone S.A. introduced a new range of probiotic-rich yogurt and lactose-free dairy beverages across Europe and North America, strengthening its position in the functional and gut-health dairy segment.

October 2025 – Lactalis Group expanded its cheese production capacity in North America to meet rising foodservice and retail demand, particularly from quick-service restaurant chains.

August 2025 – Fonterra Co-operative Group Limited invested in sustainable dairy processing technologies aimed at reducing carbon emissions and improving energy efficiency across its New Zealand manufacturing facilities.

June 2025 – Arla Foods amba launched a new organic and grass-fed dairy product line in selected European markets, emphasizing clean-label ingredients and sustainable farming practices.

Global Dairy Foods Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Milk

- Cheese

- Yogurt

- Butter & Cream

- Milk Powder

- Ice Cream & Frozen Desserts

- Others

Category Insight and Forecast 2026 - 2035

- Conventional

- Organic

Nature Insight and Forecast 2026 - 2035

- Regular

- Lactose-Free

- Fortified / Functional

Distribution Channel Insight and Forecast 2026 - 2035

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-Commerce

- Specialty Stores

- Direct Sales / Dairy Cooperatives

End User Insight and Forecast 2026 - 2035

- Household / Retail Consumers

- Foodservice

- Food Processing Industry

- Bakery & Confectionery Industry

Global Dairy Foods Market by Region

- North America

- By Product Type

- By Category

- By Nature

- By Distribution Channel

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Category

- By Nature

- By Distribution Channel

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Category

- By Nature

- By Distribution Channel

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Category

- By Nature

- By Distribution Channel

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Dairy Foods Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Category

1.2.3. By

Nature

1.2.4. By

Distribution Channel

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Milk

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Cheese

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Yogurt

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Butter & Cream

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Milk Powder

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Ice Cream & Frozen Desserts

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Others

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.2. By Category

5.2.1. Conventional

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Organic

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Nature

5.3.1. Regular

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Lactose-Free

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Fortified / Functional

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Distribution Channel

5.4.1. Supermarkets & Hypermarkets

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Convenience Stores

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Online Retail / E-Commerce

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Specialty Stores

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Direct Sales / Dairy Cooperatives

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Household / Retail Consumers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Foodservice

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Food Processing Industry

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Bakery & Confectionery Industry

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Category

6.3. By

Nature

6.4. By

Distribution Channel

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Category

7.3. By

Nature

7.4. By

Distribution Channel

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Category

8.3. By

Nature

8.4. By

Distribution Channel

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Category

9.3. By

Nature

9.4. By

Distribution Channel

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Nestlé S.A.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Danone S.A.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Lactalis Group

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Fonterra Co-operative Group Limited

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Arla Foods amba

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Royal FrieslandCampina N.V.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Dairy Farmers of America, Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Saputo Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

The Kraft Heinz Company

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Gujarat Cooperative Milk Marketing Federation Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Dairy Foods Market