Asia-Pacific Cleanroom Doors Market Overview

The Asia-Pacific cleanroom doors market which was valued at approximately USD 1.12 billion in 2025 and is estimated to rise further up to almost USD 1.22 billion by 2026, is projected to reach around USD 2.83 billion by 2035, expanding at a CAGR of about 9.1% during the forecast period from 2026 to 2035.

Market growth is driven by rising pharmaceutical manufacturing capacity, expanding semiconductor fabrication activity, and increasing compliance requirements for controlled environments. The growing adoption of modular and airtight door systems supports demand across healthcare, life sciences, and electronics manufacturing facilities, as emphasized in infection prevention and manufacturing quality guidance published by the World Health Organization.

Government-backed initiatives aimed at strengthening healthcare infrastructure, pharmaceutical self-sufficiency, and advanced manufacturing are further supporting market expansion across the Asia-Pacific region. Policy frameworks and industrial roadmaps issued by authorities such as the World Health Organization, national ministries of health, and ministries of industry emphasize contamination control, infection prevention, and compliance with cleanroom standards, reinforcing adoption of high-performance door solutions. Public investment programs promoted by government agencies in China, India, Japan, and South Korea, focused on biotechnology parks, medical device manufacturing, and semiconductor cluster development, are accelerating installations, while other regional markets continue to contribute to sustained industry expansion.

Asia-Pacific Cleanroom Doors Market Dynamics

Market Trends

The industry is witnessing notable shifts toward advanced contamination-control designs, driven by stricter regulatory compliance and increased focus on infection prevention across critical environments. One of the key trends shaping the landscape is the growing preference for modular, airtight, and automation-compatible door systems, reflecting demand for enhanced efficiency, durability, and regulatory alignment. Guidance and technical frameworks issued by government-backed bodies such as the World Health Organization (WHO) and national health ministries emphasize contamination mitigation, airflow control, and cleanroom integrity within healthcare and pharmaceutical facilities, accelerating adoption of high-performance door technologies.

Another emerging trend is the integration of smart access control and sensor-enabled door solutions, driven by digitalization initiatives and manufacturing quality mandates promoted by public authorities. Industrial modernization programs and clean manufacturing policies released by government agencies, including ministries of industry and science across Asia-Pacific economies, support the use of digitally monitored infrastructure to improve compliance and operational transparency. These developments are influencing product innovation and encouraging manufacturers to focus on integrated, value-added solutions, thereby reshaping competitive dynamics within the regional market landscape.

Growth Drivers

Growth across the sector is largely supported by expanding pharmaceutical production capacity and biologics manufacturing, which continues to generate consistent demand across regulated healthcare and life sciences facilities. Increasing public and private investments in hospital infrastructure, vaccine manufacturing plants, and medical device production units are accelerating market expansion. Government-backed initiatives issued by authorities such as the World Health Organization and national drug regulatory agencies emphasize Good Manufacturing Practices (GMP) and controlled environment standards, reinforcing demand for compliant cleanroom infrastructure components.

Additionally, the rapid expansion of semiconductor fabrication and electronics manufacturing is playing a crucial role in boosting adoption. As manufacturers prioritize yield optimization, contamination prevention, and regulatory compliance, demand for specialized cleanroom access systems is expected to remain strong throughout the forecast period. Public investment programs supporting advanced manufacturing, promoted by government agencies in countries such as China, Japan, South Korea, and India, further strengthen the growth outlook by encouraging localized production and technology self-sufficiency.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces certain challenges that may limit expansion. High initial installation costs and regulatory complexity continue to affect adoption, particularly among small-scale manufacturers and facilities operating under constrained capital budgets. Government assessments published by public health authorities and industrial safety regulators indicate that compliance with evolving cleanroom standards requires ongoing investment in certified materials, testing, and validation processes, which can impact profitability and market penetration.

Furthermore, dependence on imported raw materials, specialized hardware components, and skilled technical labor poses operational challenges for suppliers. Government trade and manufacturing reports highlight that supply chain disruptions and cross-border procurement dependencies can lead to cost pressures and extended project timelines. These factors may impact scalability and performance during periods of economic volatility or policy uncertainty, especially in emerging regional markets.

Market Opportunities

The landscape presents significant opportunities in the expansion of healthcare infrastructure and localized pharmaceutical manufacturing, particularly driven by public health investment programs and industrial development policies. Companies offering modular, cost-efficient, and regulatory-compliant door systems are well-positioned to capture incremental demand from new hospitals, diagnostic centers, and biotech facilities supported by government-funded healthcare expansion initiatives.

Another key opportunity lies in advanced manufacturing and semiconductor ecosystem development, where rising public investments in high-specification facilities are creating demand for premium and specialized cleanroom solutions. Government-backed digital manufacturing and Industry 4.0 initiatives encourage adoption of smart infrastructure components, including automated and sensor-enabled access systems. Advancements in monitoring technologies and integrated building management systems are expected to enhance compliance tracking and operational efficiency, enabling suppliers to build long-term partnerships and sustain competitive advantage.

Asia-Pacific Cleanroom Doors Market Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 1.12 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 2.83 Billion

|

|

Growth Rate

|

9.1%

|

|

Segments Covered in the Report

|

By Product, By Mode of Application, By End User

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

China, India, Japan, Australia, South Korea, Singapore, Other Regions

|

Asia-Pacific Cleanroom Doors Market Segmentation

By Product

Swinging doors accounted for the largest share of the market in 2025, representing approximately 44% of total revenue. Their dominance is supported by widespread deployment across pharmaceutical manufacturing plants, biotechnology facilities, and medical device production units, where durability, airtight sealing, and regulatory compliance remain critical. Standards and contamination control guidance issued by public health authorities such as the World Health Organization and national drug regulatory bodies reinforce the use of certified hinged door systems in controlled environments. Continuous public investment in pharmaceutical capacity expansion and hospital infrastructure modernization across Asia-Pacific further sustains demand for this product category.

Roll-up doors are expected to register the fastest growth during the forecast period from 2026 to 2035, with an estimated CAGR of 9.6%, driven by increasing adoption in semiconductor fabrication plants and electronics manufacturing cleanrooms requiring high-speed access and space optimization.

Sliding doors and other specialized configurations are projected to grow at a CAGR of approximately 8.4%, supported by modular cleanroom installations in research laboratories and healthcare facilities.

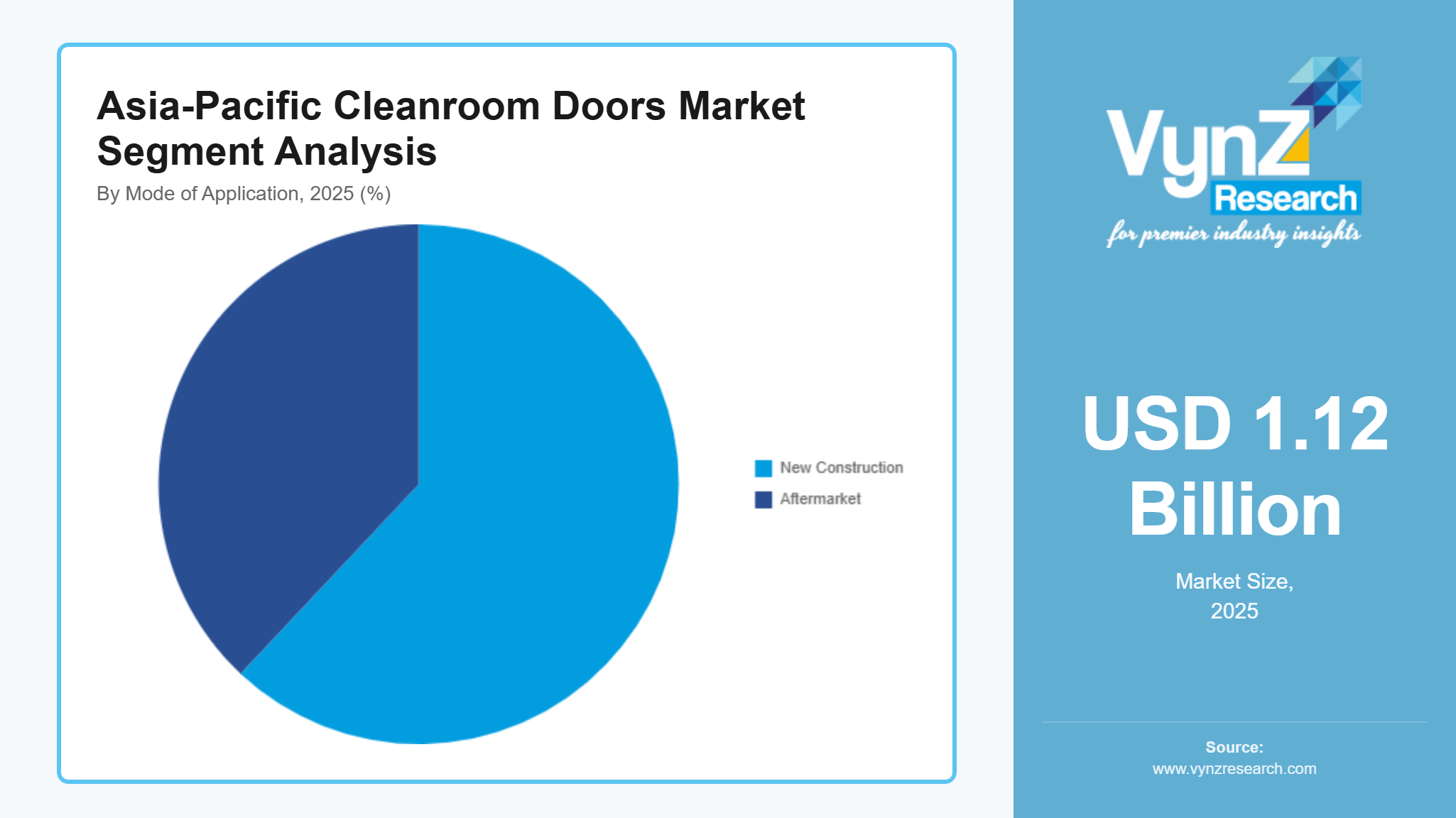

By Mode of Application

New construction accounted for the largest share of the market in 2025, contributing approximately 62% of total segment revenue, driven by large-scale investments in greenfield pharmaceutical facilities, biotechnology parks, and advanced manufacturing clusters across Asia-Pacific. Government-backed industrial development programs and healthcare infrastructure expansion policies emphasize contamination-controlled environments, reinforcing procurement of cleanroom door systems during initial construction phases. Regulatory frameworks issued by health and industrial safety authorities further support adoption in newly commissioned facilities.

Aftermarket applications are projected to grow at the fastest pace, registering an estimated CAGR of 9.1% from 2026 to 2035, as existing facilities increasingly undertake retrofit upgrades, compliance audits, and validation cycles. Periodic enforcement of cleanroom standards and infection prevention guidelines by public health agencies continues to drive replacement demand, while operational efficiency requirements encourage upgrades to advanced airtight and automated door systems.

By End User

The biotechnology, pharmaceutical, and medical device industry accounted for the largest share of the market in 2025, representing approximately 48% of total revenue, supported by stringent contamination control requirements for sterile manufacturing and quality assurance. Government initiatives promoting pharmaceutical self-sufficiency, drug safety, and localized manufacturing capacity across countries such as China, India, and Japan reinforce sustained investment in certified cleanroom infrastructure.

Hospitals and diagnostic laboratories are expected to witness the fastest growth, with an estimated CAGR of 8.9% during 2026 to 2035, driven by rising healthcare expenditure, infection prevention mandates, and expansion of sterile processing and diagnostic facilities.

Academic research institutes and other end users are projected to grow steadily at a CAGR of around 7.8%, reflecting increasing research activity, laboratory expansion, and compliance with publicly issued biosafety and cleanroom standards.

Regional Insights

China

China is estimated to account for approximately 34% of the market in 2025. Growth in the country is driven by large-scale pharmaceutical manufacturing expansion, rapid growth in semiconductor fabrication capacity, and strict regulatory oversight enforced by the National Medical Products Administration and the National Health Commission. Major industrial and healthcare hubs including Shanghai, Shenzhen, Suzhou, and Beijing continue to record strong demand for controlled environment infrastructure across life sciences, medical device production, and electronics manufacturing.

Government-backed initiatives supporting pharmaceutical self-reliance, biosafety compliance, and advanced manufacturing development are encouraging sustained investments in certified cleanroom door systems. National cleanroom and contamination control standards issued by regulatory authorities continue to reinforce adoption across regulated production facilities.

India

India represents approximately 24% of the regional market in 2025, supported by expanding pharmaceutical exports, increasing vaccine manufacturing capacity, and steady growth in biotechnology research infrastructure. Rising adoption across formulation plants, contract manufacturing organizations, and hospital cleanroom facilities is driving consistent demand. Regulatory guidance issued by the Central Drugs Standard Control Organization and policy frameworks from the Ministry of Health and Family Welfare emphasize contamination control and clean manufacturing compliance.

Government programs promoting domestic pharmaceutical manufacturing, healthcare infrastructure modernization, and biotechnology park development are accelerating cleanroom investments across major industrial corridors and emerging life sciences clusters.

Japan

Japan accounts for an estimated 14% of the market in 2025. Growth is supported by advanced semiconductor manufacturing, precision electronics production, and high-value pharmaceutical research concentrated in regions such as Tokyo, Osaka, and Yokohama. Regulatory oversight by the Ministry of Health, Labor and Welfare enforces strict cleanroom standards related to infection control, product quality, and environmental safety.

Public investment in advanced manufacturing technologies, industrial automation, and healthcare system resilience continues to sustain demand for high-performance cleanroom door solutions across regulated industries.

Other Regions

Other Asia-Pacific regions, including South Korea, Southeast Asia, and Oceania, collectively account for approximately 18% of the market in 2025. Growth across these markets is supported by expanding electronics manufacturing, increasing pharmaceutical outsourcing activity, and rising healthcare infrastructure investments. Regulatory bodies such as the Ministry of Food and Drug Safety in South Korea and national health authorities across Southeast Asia promote compliance with cleanroom and biosafety standards.

Government-backed industrial development programs, medical manufacturing incentives, and healthcare modernization initiatives are supporting gradual adoption. The remaining regional demand is distributed across smaller and emerging Asia-Pacific economies, contributing to long-term market expansion beyond the primary markets covered above.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional players focusing on product innovation, pricing optimization, and geographic expansion to strengthen market positioning. Companies are increasingly investing in R&D, airtight and modular door technologies, and compliance-focused designs to meet evolving cleanroom standards. Adoption is supported by regulatory guidance and infrastructure initiatives issued by government-backed authorities such as the World Health Organization, national health ministries, and industrial safety regulators across Asia Pacific, which promote contamination control, pharmaceutical quality assurance, and advanced manufacturing compliance, reinforcing sustained competitive activity across the landscape.

Mini Profiles

Assa Abloy focuses on secure and hygienic door solutions for controlled environments, supported by strong brand recognition, global distribution networks, and engineering expertise in access and sealing technologies.

Chase Industries, Inc. operates in industrial and institutional segments, emphasizing durable door protection systems, performance reliability, and customized solutions tailored to high-traffic cleanroom and healthcare facilities.

Dortek specializes in composite cleanroom door systems, supported by regulatory compliance expertise, precision manufacturing, and strong penetration across pharmaceutical, healthcare, and laboratory infrastructure projects.

Gandhi Automations Pvt Ltd. leverages local manufacturing and automation expertise to expand market presence, offering cost-efficient cleanroom and industrial door solutions across pharmaceutical and advanced manufacturing sectors.

Nicomac Srl operates in premium cleanroom infrastructure solutions, emphasizing modular design, customization capabilities, and integrated cleanroom systems that support high-spec pharmaceutical and life-science environments.

Key Players

- Assa Abloy

- Avians

- Chase Industries, Inc.

- Dortek

- EFAFLEX

- Gandhi Automations Pvt Ltd.

- Nicomac Srl

- Rite-Hite

- Terra Universal, Inc.

Recent Developments

In February 2026, ASSA ABLOY has acquired NSP Security (“NSP”) in the UK, a company providing design, manufacturing and installation of access control solutions primarily within the student accommodation segment.

In November 2025, A new platform that aims to create a "national network of legacy factory automation businesses" has the support of the family that owns Rite-Hite, a manufacturer of industrial equipment. In order to "acquire, build, and integrate automation-focused distribution, assembly, and engineering service companies across the United States," Heritage Automation Partners was formed in collaboration with SixSibs Capital, which officials referred to as "the family investment office" of the White family.