- 1-888-253-3960

- enquiry@vynzresearch.com

-

This is lorem ipsum doller

- Home /

- Healthcare /

- Europe Isolation Beds Market

- Home >

- Healthcare >

- Europe Isolation Beds Market

Europe Isolation Beds Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Manual, Electric, Hydraulic, Pneumatic), by Usage (Critical, Bariatric, Medical Surgery, Pediatric, Maternal), by End Use (General & Acute Care Hospitals, Multi-Specialty Hospitals, Specialized Hospitals, Ambulatory Surgical Centers, Others)

| Status : Published | Published On : Mar, 2026 | Report Code : VRHC1332 | Industry : Healthcare | Available Format :

|

Page : 145 |

Europe Isolation Beds Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Manual, Electric, Hydraulic, Pneumatic), by Usage (Critical, Bariatric, Medical Surgery, Pediatric, Maternal), by End Use (General & Acute Care Hospitals, Multi-Specialty Hospitals, Specialized Hospitals, Ambulatory Surgical Centers, Others)

Europe Isolation Beds Market Overview

The Europe isolation beds market which was valued at approximately USD 0.452 million in 2025 and is estimated to rise further up to almost USD 0.482 million by 2026, is projected to reach around USD 0.856 million in 2035, expanding at a CAGR of about 6.6% during the forecast period 2026 to 2035.

The growing need for controlled hospital environments to treat infectious diseases together with the increasing requirement for dedicated patient isolation spaces creates a favorable condition for market growth. The World Health Organization and European Centre for Disease Prevention and Control have published reports showing that European healthcare systems still monitor airborne and contact transmitted infections which causes hospitals to improve their infection control systems. Medical facilities now implement advanced hospital furniture which enables safe patient isolation as healthcare providers use these products in various clinical settings throughout their facilities.

The market will continue to expand because of ongoing healthcare infrastructure upgrades and the implementation of infection control measures throughout the European region. The hospital expansion of isolation wards and critical care facilities received funding from government-supported hospital renovation projects and emergency preparedness programming. Public health agencies across countries such as Germany, France, and Italy have emphasized hospital preparedness programs aimed at strengthening infection control management and protecting healthcare personnel. The increased respiratory infection hospital admissions together with the rise in hospital-acquired infections has created a higher need for dedicated isolation spaces. The market for healthcare systems in Western and Central Europe grows stronger through the adoption of advanced hospital equipment together with better infection control methods.

Europe Isolation Beds Market Dynamics

Market Trends

Healthcare facilities are currently moving towards advanced hospital isolation systems which have been specially designed to enhance infection control measures and patient safety in all healthcare settings. The healthcare authorities in Europe have raised their focus on isolation capacity because of increased infectious disease transmission and the rise of hospital-acquired infections. The World Health Organization together with the European Centre for Disease Prevention and Control provides public health recommendations which demonstrate that hospitals must create isolation facilities to stop pathogen spread. Hospitals have started to use specialized furniture which includes isolation beds that enable hospitals to follow infection control procedures and maintain pressure-controlled environments while improving patient monitoring. Hospitals are progressively adopting modular intensive care infrastructure and technologically enhanced beds which have been designed to create safe treatment spaces while supporting clinical operations in infectious disease treatment areas.

The latest trend shows that hospitals now use bed systems which combine ergonomic design with technological features in their isolation ward operations. Hospitals are increasingly investing in electrically adjustable beds, which come with integrated monitoring features and antimicrobial surface materials that help decrease the chances of cross contamination between patients and staff. The healthcare infrastructure development projects currently underway in Germany, France, and Italy, along with other European nations, are driving hospitals to expand their capacity through modernization initiatives because they need to acquire advanced isolation care equipment for infectious disease management.

Growth Drivers

The market growth shows strong support from rising infectious disease cases which create a need for dedicated patient management systems to treat hospital-acquired infections. The World Health Organization and European Centre for Disease Prevention and Control report that approximately 1 million patients experience healthcare-associated infections annually throughout the region, which leads to a persistent requirement for isolation facilities and medical equipment. Hospitals are expanding their isolation wards along with their infection control systems in order to meet the new clinical guidelines and preparedness requirements which have been introduced. The current market situation has prompted healthcare providers to start using specialized beds which are made for controlled patient environments, resulting in continuous demand from hospitals and infectious disease treatment facilities.

The European healthcare infrastructure modernization projects are driving up demand for improved system adoption because they directly increase funding to enhance healthcare systems. Public health authorities and national healthcare systems are launching permanent hospital renovation programs which include capacity expansion activities to build better infectious disease outbreak response systems. Government healthcare investment programs in Germany, France, and the United Kingdom help to expand critical care services through their support of intensive care unit and specialized isolation ward development.

Market Restraints / Challenges

The healthcare sector needs to overcome operational and financial constraints which will slow down technology adoption across different healthcare facilities despite its strong growth potential. The costs which hospitals incur to buy and maintain their advanced isolation beds result in financial difficulties for smaller healthcare systems and public hospitals that operate with restricted funding resources. European public health authorities have published reports which show that hospitals need to spend money on medical equipment and facility redesign and infection control technologies to achieve modern hospital infrastructure standards. The financial restrictions force hospitals to postpone bed replacement schedules while they cannot acquire specialized isolation equipment which costs too much for their budget needs.

Healthcare facilities face obstacles because they must navigate both the regulatory requirements and operational procedures that govern medical equipment purchasing and hospital infrastructure development. European regulatory authorities established stringent safety and medical device standards which healthcare facilities must follow to protect patient safety and guarantee product reliability. The product approval process for manufacturers becomes more time-consuming and expensive because their products require quality certification and infection control standard and clinical safety testing compliance. The manufacturers face operational risks because their businesses contain specialized components and advanced manufacturing technologies which supply chain interruptions can disrupt and create economic burdens that affect their entire operational sector.

Market Opportunities

The sector offers major business growth potential because European healthcare systems will build more hospital facilities and develop better infectious disease response strategies. The World Health Organization and the European Commission developed public health policy frameworks which the World Health Organization and the European Commission developed to help organizations build hospitals with greater resilience and better infection control systems. The healthcare authorities have decided to increase their financial support for isolation wards and emergency preparedness units and critical care infrastructure development. Hospitals that need advanced hospital beds built for controlled infection spaces will begin new procurement activities which these projects will create. The healthcare market for providers who create beds with long-lasting materials and ergonomic designs and technological systems will expand because hospitals will build more new facilities.

Healthcare providers need to establish new hospital furniture designs which combine advanced technology with patient-centered design to promote efficient infection control procedures. Healthcare facilities use smart monitoring systems and automated bed adjustment systems and antimicrobial materials to create advanced hospital beds which help them achieve better patient results and higher staff productivity. European hospitals proceed with digital transformation through their public healthcare modernization plans, which create demand for connected medical equipment that supports real-time patient monitoring and clinical workflow optimization. The healthcare industry will see growing demand for modular and technology-enabled and customizable isolation bed systems which manufacturers will introduce.

Europe Isolation Beds Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

U.S.D. 0.452 Million |

|

Revenue Forecast in 2035 |

U.S.D. 0.856 Million |

|

Growth Rate |

6.6% |

|

Segments Covered in the Report |

By Type, By Usage, By End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, U.K., France, Italy, Spain, Russia, Rest of Europe |

Europe Isolation Beds Market Segmentation

By Type

The market reached its highest revenue point in 2025 through manual isolation beds which generated approximately 36% of total segment revenue. The solution became the most used option, because it provided hospitals with budget-friendly systems, dependable mechanical systems, and shared accessibility across their medical facilities. Central and Eastern European healthcare systems still favor manual hospital beds, because they offer lower initial expenses, which makes them easier to keep operational. The European health authorities report that hospitals with budget limitations choose manual systems, which provide essential patient positioning functions at a cost-effective solution, for their general isolation wards. Public healthcare institutions and mid-scale hospitals maintain constant demand, because these factors create ongoing need for manual isolation beds.

Electric isolation beds will develop most rapidly during the forecast period, with their market expected to grow at a compound annual growth rate of 7.1%. The demand for high-tech hospital infrastructure development together with better patient care methods drives the growth of the market. Hospitals throughout Western Europe increasingly adopt electric beds, which come with automated positioning systems, patient monitoring capabilities, and caregiver-friendly design features. Hospital modernization efforts in Germany, France, and the United Kingdom receive government support, which leads hospitals to replace traditional beds with advanced medical furniture that meets the needs of critical care isolation units. The recent developments in the market drive hospitals to demand electric systems for their new construction and renovation projects.

By Usage

The market generated its highest revenue through critical care applications in 2025, which accounted for 33% of total segment revenue. European hospitals have expanded critical care units to treat patients who need intensive monitoring and infection control, especially during respiratory and infectious disease outbreaks. The World Health Organization and European Centre for Disease Prevention and Control reports show that intensive care units require dedicated isolation facilities to lower hospital-acquired infections while enhancing patient safety. Hospitals adopted specialized isolation beds, which support ventilator connectivity and patient monitoring systems and their capacity for precise patient position adjustments needed during complex medical procedures.

Bariatric applications will experience the highest growth in the upcoming years, with their market expected to increase at a compound annual growth rate of 7.2%. The increasing obesity rates in several European nations create a demand for hospital beds that can handle higher patient weights while providing better comfort during medical treatment. European health agencies report that obesity rates keep rising, which leads to more hospital admissions that require bariatric care facilities. Hospitals need to invest in heavy-duty isolation beds which can withstand higher weight capacities while still meeting infection control requirements to support this market segment.

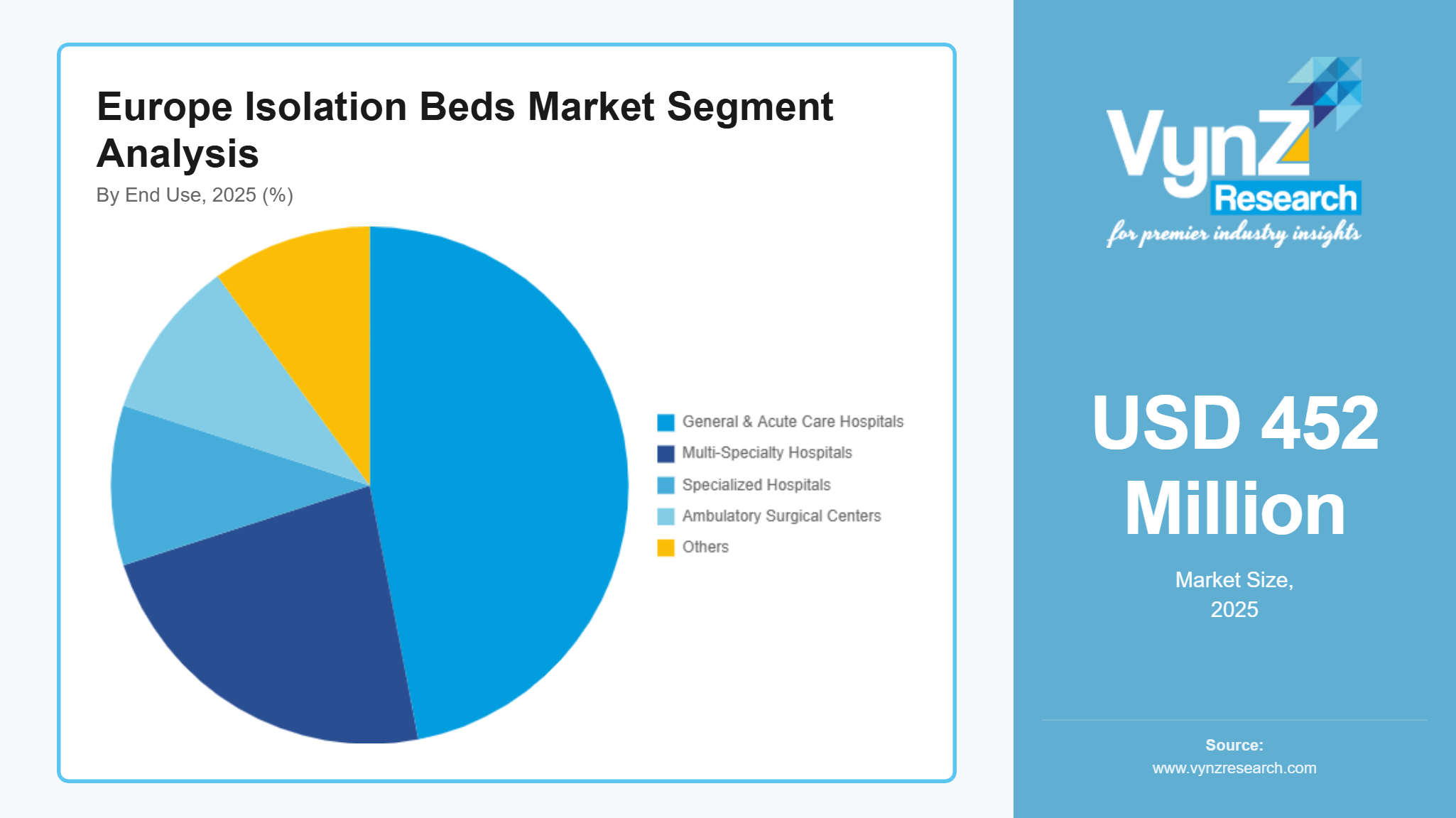

By End Use

The market in 2025 showed its highest percentage from general and acute care hospitals which generated about 47% of total revenue for this market segment. Patient isolation infrastructure at these healthcare institutions supports their treatment of infectious diseases followed by emergency admissions and critical care operations. The European healthcare system preparedness programs require large hospitals to create more infection control wards as a measure to enhance their disease containment abilities while protecting patient safety. Public funding for hospital modernization projects in Germany, France, and Italy has resulted in hospitals acquiring specialized beds that are intended for use in isolation units and infectious disease departments.

The specialized hospitals sector will experience rapid expansion with a projected compound annual growth rate of 7.3% throughout the upcoming period. Facilities that treat infectious diseases and respiratory disorders and critical care patients now need advanced hospital equipment for effective patient treatment. European public health authorities create healthcare policy frameworks that aim to enhance specialized treatment facilities which can manage patients with high-risk infectious diseases. Technological advancements have driven hospitals to acquire isolation beds which come with integrated patient support systems and better infection control systems.

Regional Insights

Germany

The market in 2025 had Germany holding 18% market share because its healthcare system had advanced medical facilities and high hospital bed capacity across its major cities which included Berlin, Munich and Hamburg. The country operates the second largest hospital system in Europe while it continually invests in both infection control systems and intensive care unit development. The Robert Koch Institute and public health system reports which follow World Health Organization guidelines demonstrate that hospitals must prepare to handle infectious diseases effectively. Hospitals which receive government funding for their modernization projects will acquire advanced isolation beds that enable doctors to track patient vital signs while preventing infection spread which will help the hospital system grow at public and university medical facilities.

The United Kingdom

The United Kingdom represents approximately 15% of the sector in 2025, driven by ongoing healthcare infrastructure investments and the expansion of infection control capacity across hospitals. The National Health Service has implemented several hospital improvement programs focusing on patient safety and infectious disease preparedness. The cities of London, Manchester and Birmingham maintain extensive hospital systems which continually refresh their medical instruments to match national healthcare safety protocols. The UK Health Security Agency has issued public health documentation which demonstrates that dedicated isolation facilities are essential for controlling infectious disease outbreak situations. The government policies are prompting hospitals to buy specialized isolation beds which help hospitals control infections while providing better patient care.

France

France contributes approximately 13% of the regional market in 2025, because its public healthcare system develops through new investments which support hospital modernization projects. Major healthcare facilities located in cities such as Paris, Lyon, and Marseille are actively expanding critical care and isolation wards to strengthen infection management capacity. Government health agencies and national hospital infrastructure plans emphasize modernization of medical equipment and improvement of hospital safety standards. The European infection prevention guidelines for public health policies drive hospitals to create advanced patient care systems which need specialized hospital beds that support isolation treatment spaces thus leading to sustained development in the country.

Italy

Italy accounts for approximately 11% of the sector in 2025, because its hospitals undergo ongoing facility improvements while the country develops better infectious disease response capabilities after recent healthcare system changes. Major healthcare centers in Rome, Milan, and Naples are investing in critical care infrastructure and infection prevention equipment to strengthen patient management capabilities. Public health agencies in Italy have introduced national strategies aimed at improving hospital resilience and infection control capacity. Hospitals should adopt protective medical technology which includes isolation beds to maintain patient safety in all public hospitals and healthcare facilities during their operations.

Spain

Spain shows a market share of 9% in 2025 because its healthcare system develops through ongoing infrastructure projects and hospital infection control program expansion efforts. Healthcare facilities across cities such as Madrid, Barcelona, and Valencia are implementing modernization strategies to improve patient care standards and hospital preparedness. National health authorities emphasize strengthening infection prevention infrastructure across hospitals and specialized treatment centers. The country experiences stable demand for isolation beds because hospitals increasingly use modern hospital furniture which is made for both isolation wards and intensive care units.

Russia

Russia contributes approximately 8% of the regional sector in 2025, because the country has extensive hospital networks that the government develops to boost infectious disease treatment abilities. Major healthcare centers in Moscow, Saint Petersburg, and other metropolitan areas continue to expand hospital infrastructure and upgrade medical equipment. The healthcare system development of public health institutions requires them to invest in specialized patient care equipment and isolation beds which treat infectious disease patients. The sector will grow at both public hospitals and specialized hospitals through these technological advancements.

Rest of Europe

The rest of Europe collectively accounts for approximately 6% of the sector in 2025, including healthcare markets across countries in Central and Eastern Europe as well as smaller Western European economies. Hospital infection control systems and patient care equipment need upgrading because European public health frameworks support modern healthcare systems. Hospitals which renovate their facilities and expand their capacity will create more demand for isolation beds as the region develops its healthcare systems. The countries in this analysis account for 80% of the regional healthcare system while remaining demand becomes distributed among other European healthcare markets which this analysis does not specifically address.

Competitive Landscape / Company Insights

The market competition exists at a medium level because multiple international and local manufacturers work to establish their market presence through product development and advanced hospital bed technology and regional market expansion. Hospital bed manufacturers are expanding their research and development activities to create beds that use ergonomic design and automated adjustment system and infection resistant material. Healthcare modernization programs together with World Health Organization and European public health authorities’ infection prevention frameworks support adoption of new technologies which help hospitals modernize their critical care and isolation facilities throughout the region.

Mini Profiles

Arjo Huntleigh (Division of Getinge AB) focuses on advanced hospital bed and patient handling solutions, supported by strong European distribution networks, recognized healthcare brands, and continuous product innovation that strengthens presence in critical care environments.

Gendron Inc. operates in specialized and bariatric healthcare equipment segments, emphasizing durability, patient safety, and high load-capacity hospital beds, supported by customized designs that address the needs of specialized medical facilities.

Medline Industries operates in large scale healthcare supply and equipment segments, emphasizing cost efficiency, broad product availability, and integrated supply chain capabilities that support hospitals and clinical facilities across international markets.

Key Players

- Arjo Huntleigh (Division of Getinge AB)

- Gendron Inc.

- Joerns Healthcare

- LINET Group

- Malvestio

- S.P.A.

- Medline Industries

- Paramount Bed Holdings Co., Ltd.

Recent Developments

In March 2026, Medline signed a supply agreement with Better Life Medical & Surgical Supply, allowing the provider to access Medline’s portfolio of medical-surgical products, durable medical equipment, and distribution services to improve delivery efficiency for healthcare customers.

In June 2025, Paramount Bed introduced a new ICU bed with a motorized drive system designed to support patient transport within hospitals while improving safety and operational efficiency for healthcare staff.

Table of Contents for Europe Isolation Beds Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Usage

1.2.3. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Manual

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Electric

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Hydraulic

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Pneumatic

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Usage

5.2.1. Critical

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Bariatric

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Medical Surgery

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Pediatric

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Maternal

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By End Use

5.3.1. General & Acute Care Hospitals

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Multi-Specialty Hospitals

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Specialized Hospitals

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Ambulatory Surgical Centers

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Others

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Type

6.2. By

Usage

6.3. By

End Use

7. U.K. Market Estimate and Forecast

7.1. By

Type

7.2. By

Usage

7.3. By

End Use

8. France Market Estimate and Forecast

8.1. By

Type

8.2. By

Usage

8.3. By

End Use

9. Italy Market Estimate and Forecast

9.1. By

Type

9.2. By

Usage

9.3. By

End Use

10. Spain Market Estimate and Forecast

10.1. By

Type

10.2. By

Usage

10.3. By

End Use

11. Russia Market Estimate and Forecast

11.1. By

Type

11.2. By

Usage

11.3. By

End Use

12. Rest of Europe Market Estimate and Forecast

12.1. By

Type

12.2. By

Usage

12.3. By

End Use

13. Company Profiles

13.1.

Arjo Huntleigh (Division of Getinge AB)

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Gendron Inc.

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Joerns Healthcare

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

LINET Group

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Malvestio S.P.A.

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Medline Industries

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Paramount Bed Holdings Co., Ltd.

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Europe Isolation Beds Market Coverage

Type Insight and Forecast 2026 - 2035

- Manual

- Electric

- Hydraulic

- Pneumatic

Usage Insight and Forecast 2026 - 2035

- Critical

- Bariatric

- Medical Surgery

- Pediatric

- Maternal

End Use Insight and Forecast 2026 - 2035

- General & Acute Care Hospitals

- Multi-Specialty Hospitals

- Specialized Hospitals

- Ambulatory Surgical Centers

- Others

Europe Isolation Beds Market by Region

- Germany

- By Type

- By Usage

- By End Use

- U.K.

- By Type

- By Usage

- By End Use

- France

- By Type

- By Usage

- By End Use

- Italy

- By Type

- By Usage

- By End Use

- Spain

- By Type

- By Usage

- By End Use

- Russia

- By Type

- By Usage

- By End Use

- Rest of Europe

- By Type

- By Usage

- By End Use

Vynz Research know in your business needs, you required specific answers pertaining to the market, Hence, our experts and analyst can provide you the customized research support on your specific needs.

After the purchase of current report, you can claim certain degree of free customization within the scope of the research.

Please let us know, how we can serve you better with your specific requirements to your research needs. Vynz research promises for quick reversal for your current business requirements.

- Arjo Huntleigh (Division of Getinge AB)

- Gendron Inc.

- Joerns Healthcare

- LINET Group

- Malvestio S.P.A.

- Medline Industries

- Paramount Bed Holdings Co., Ltd.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: 1 888 253 3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Isolation Beds Market