Laboratory Automation Systems Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Equipment, Software, Services), by Automation Approach (Modular Automation, Total Laboratory Automation (TLA)), by Application (Clinical Diagnostics, Drug Discovery & Development, Genomics, Proteomics, Others), by End User (Pharmaceutical & Biotechnology Companies, Hospitals & Clinical / Reference Laboratories, Research & Academic Institutes, Others)

| Status : Published | Published On : Mar, 2026 | Report Code : VRHC1327 | Industry : Healthcare | Available Format :

|

Page : 190 |

Laboratory Automation Systems Market Overview

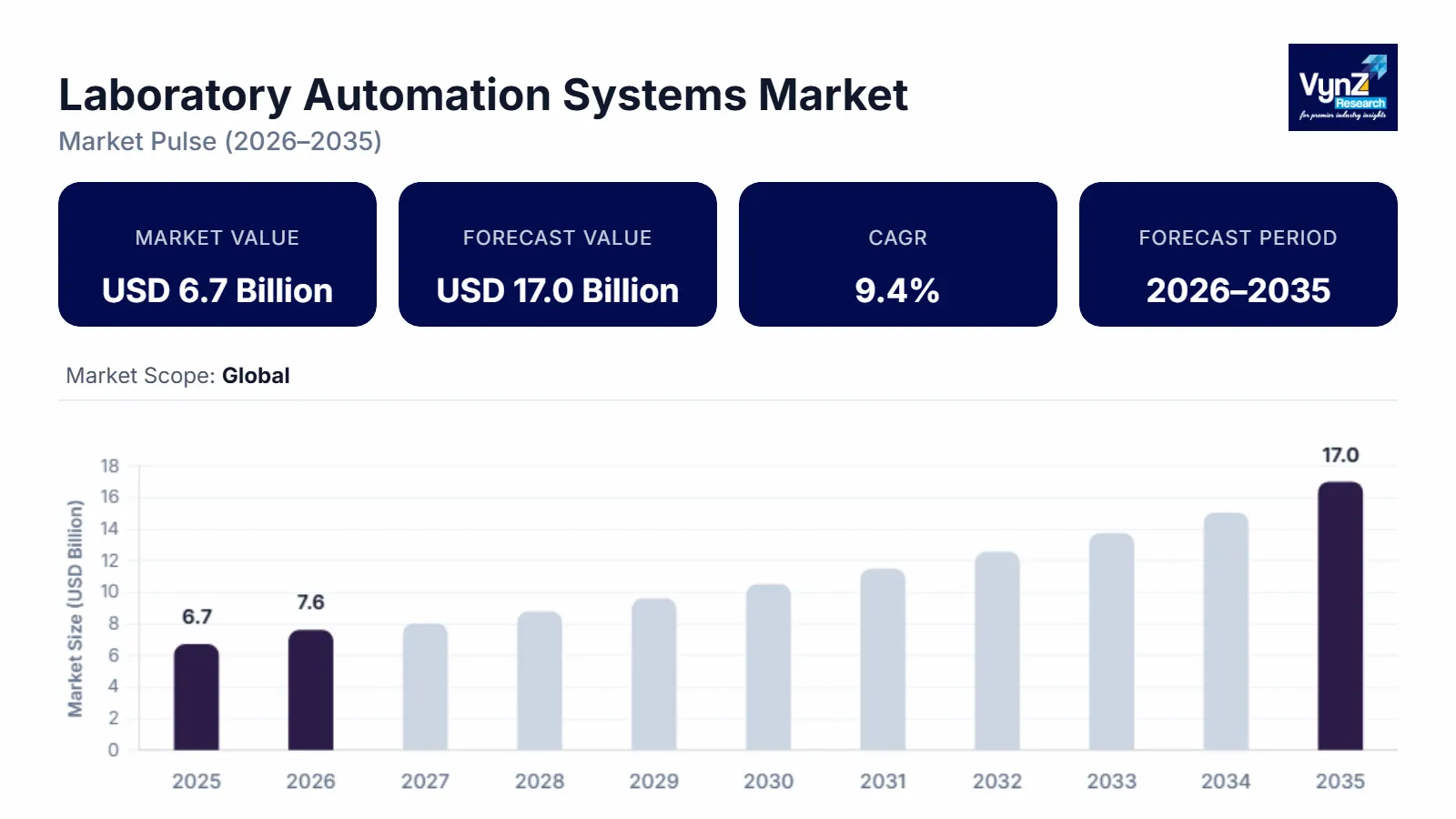

The laboratory automation systems market which was valued at approximately USD 6.7 billion in 2025 and is estimated to reach around USD 7.6 billion in 2026, is projected to reach close to USD 17.0 billion by 2035, expanding at a CAGR of about 9.4% during the forecast period from 2026 to 2035.

The market is experiencing robust growth, driven by the increasing demand for high-throughput, accurate, and reproducible laboratory operations across clinical, pharmaceutical, and research sectors. Rising investments in drug discovery, genomics, and proteomics, coupled with the growing prevalence of chronic diseases and diagnostic testing, are prompting laboratories to adopt automated solutions to enhance efficiency and reduce human error. Advancements in robotic systems, liquid handling technologies, and integrated software platforms enable seamless workflow optimization, real-time data management, and regulatory compliance.

Additionally, the global shift toward personalized medicine and precision therapeutics is creating a need for laboratories capable of handling large, complex datasets with speed and accuracy. Cost pressures and competitive landscapes are further encouraging organizations to streamline operations through automation, reducing turnaround times and operational overhead. Collectively, these factors position laboratory automation as a critical growth driver in modern life sciences and healthcare infrastructure, with long-term market expansion poised to accelerate.

Laboratory Automation Systems Market Dynamics

Market Trends

A major trend in the laboratory automation systems market is the widespread digitalization of laboratory workflows to enhance throughput, accuracy, and connectivity. Governments are increasingly recognizing the central role of laboratory systems in public health infrastructure. In the United States, clinical and public health laboratories carry out more than 15 billion diagnostic tests annually, underscoring the volume of work that modern laboratories must process to inform prevention, treatment, and disease surveillance. To keep pace with growing test volumes and stringent quality standards, laboratories are integrating automated liquid handling, robotic sample processing, and laboratory information management systems that reduce manual intervention, improve data integrity, and enable real‑time decision‑making. This shift toward digital workflows aligns with national priorities in disease preparedness and diagnostic readiness, as governments seek to minimize reporting lags and ensure consistent quality across decentralized health networks. Enhanced automation also supports pandemic response infrastructure by enabling laboratories to scale operations rapidly without proportionally increasing staff.

Growth Drivers

A key driver of the laboratory automation systems market is the expanding scale of pharmaceutical research and precision medicine initiatives. Government health agencies are increasingly directing funding toward advanced therapeutic research, underpinning automation demand. For example, the U.S. National Institutes of Health budget for biomedical research in 2025 was over $46 billion, reinforcing government commitment to innovation. Automated systems enable highthroughput screening, rapid genomic and proteomic analysis, and robust data integrity, which are essential for accelerating drug discovery and tailored therapies. As regulatory frameworks evolve to emphasize data traceability, reproducibility, and quality assurance, automation technologies become indispensable. This convergence of research intensity and regulatory expectation drives laboratory investment in automated liquid handlers, robotic arms, and integrated software platforms, helping laboratories meet increasing workloads with precision and efficiency.

Market Restraints / Challenges

A key challenge in the laboratory automation systems market is the significant upfront investment and technical complexity involved in deploying automated platforms. Laboratories must allocate resources for equipment, software, training, and system integration, which can be particularly difficult for smaller or resource-constrained facilities. Integrating new automation solutions with legacy instruments and existing workflows often requires careful process redesign, validation, and regulatory compliance, adding to implementation complexity. Resistance to organizational change and the need for skilled personnel further slow adoption. Overcoming these challenges requires modular and scalable solutions, streamlined installation processes, and comprehensive training programs that reduce operational disruption while maximizing the efficiency and accuracy benefits of automation.

Market Opportunities

Emerging markets present a significant growth opportunity for laboratory automation systems as healthcare and research infrastructure expands. Decentralized laboratories, community hospitals, and regional testing centers increasingly require scalable, compact, and efficient automation platforms to handle high volumes of testing and data management. Vendors offering modular systems, cloud-enabled software, and remote support can tap into these under-served markets. Expanding adoption in emerging regions not only addresses unmet diagnostic demand but also supports improved workflow efficiency, faster turnaround times, and higher-quality results, positioning automation providers for long-term growth in both public health and research-focused laboratories.

Global Laboratory Automation Systems Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.7 Billion |

|

Revenue Forecast in 2035 |

USD 17.0 Billion |

|

Growth Rate |

9.4% |

|

Segments Covered in the Report |

Type, Automation Approach, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Abbott Laboratories, Danaher Corporation (Beckman Coulter, Inc.), Thermo Fisher Scientific Inc., Agilent Technologies, Inc., F. Hoffmann-La Roche Ltd., Tecan Trading AG, PerkinElmer AES, QIAGEN GMBH, Becton, Dickinson and Company (BD), Siemens Healthineers, Hamilton Company, and Eppendorf Group |

|

Customization |

Available upon request |

Laboratory Automation Systems Market Segmentation

By Type

Equipment is the largest category in the laboratory automation systems market, with a market share of around 55% in 2025, driven by its foundational role in enabling automated workflows across testing and research environments. Automated liquid handlers, robotic arms, and plate handling systems form the hardware backbone that transforms sample processing, reagent delivery, and highthroughput testing. Laboratories invest in equipment first, as these systems directly improve accuracy, reduce manual errors, and increase throughput in clinical diagnostics and drug development. The breadth of applications for equipment—from clinical chemistry analyzers to storage and retrieval systems—ensures widespread adoption across institutional and commercial labs. As test volumes rise and precision requirements tighten worldwide, equipment continues to generate the largest revenue share in the automation market due to its indispensable role in modern laboratory operations.

There equipment further classified into followings

- Automated Workstations

- Automated Liquid Handling Systems

- Automated Plate Handling Systems

- Robotic Arms / Standalone Robots

- Automated Storage & Retrieval Systems

Within the type segment, Software is the fastestgrowing category as laboratories seek advanced data management, workflow orchestration, and decision support tools. Laboratory Information Management Systems (LIMS), integration middleware, and AIdriven analytics platforms streamline complex workflows by reducing manual tracking, enabling realtime data visibility, and improving compliance with quality standards. Digital platforms facilitate interoperability between instruments, ensure traceability of results, and support remote access — critical capabilities in multisite research and clinical networks. With the rise of precision medicine and genomics, software solutions are becoming integral to handling large data sets, integrating laboratory instruments, and automating reporting. Investments in software grow rapidly as institutions prioritize efficiency gains, regulatory compliance, and scalability, making it the fastestexpanding segment in the automation ecosystem.

By Automation Approach

Total Laboratory Automation (TLA) holds the largest share of about 60% in 2025 within the automation approach segment because it integrates complete laboratory workflows from sample receipt through analysis and reporting. TLA systems eliminate most manual handling steps, significantly boost throughput, and enhance reproducibility. They are especially prevalent in highvolume clinical labs, central testing facilities, and large research institutions that demand consistent performance and data quality. Fully integrated systems reduce turnaround times, standardize processes, and support realtime tracking of specimens, which are essential in environments that process thousands of tests per day. As healthcare and research organizations aim to consolidate laboratory functions and improve operational efficiency, TLA maintains its dominance by delivering comprehensive automation that addresses both preanalytical and analytical needs across multiple departments.

Modular Automation is the fastestgrowing category with a CAGR of 9.6% during the forecast period, as laboratories in emerging markets and smaller facilities adopt flexible solutions tailored to specific tasks. Modular systems allow targeted automation — such as liquid handling, sample sorting, or plate handling without the cost and complexity of full TLA deployment. Laboratories can incrementally upgrade workflows, manage budget constraints, and customize automation to suit unique applications. This adaptability makes modular solutions attractive for research labs, academic institutions, and decentralized diagnostic centers that require scalable investments. As demand increases for taskspecific automation that improves accuracy and throughput without full system integration, modular automation is expanding rapidly, often serving as an entry point into broader automation ecosystems.

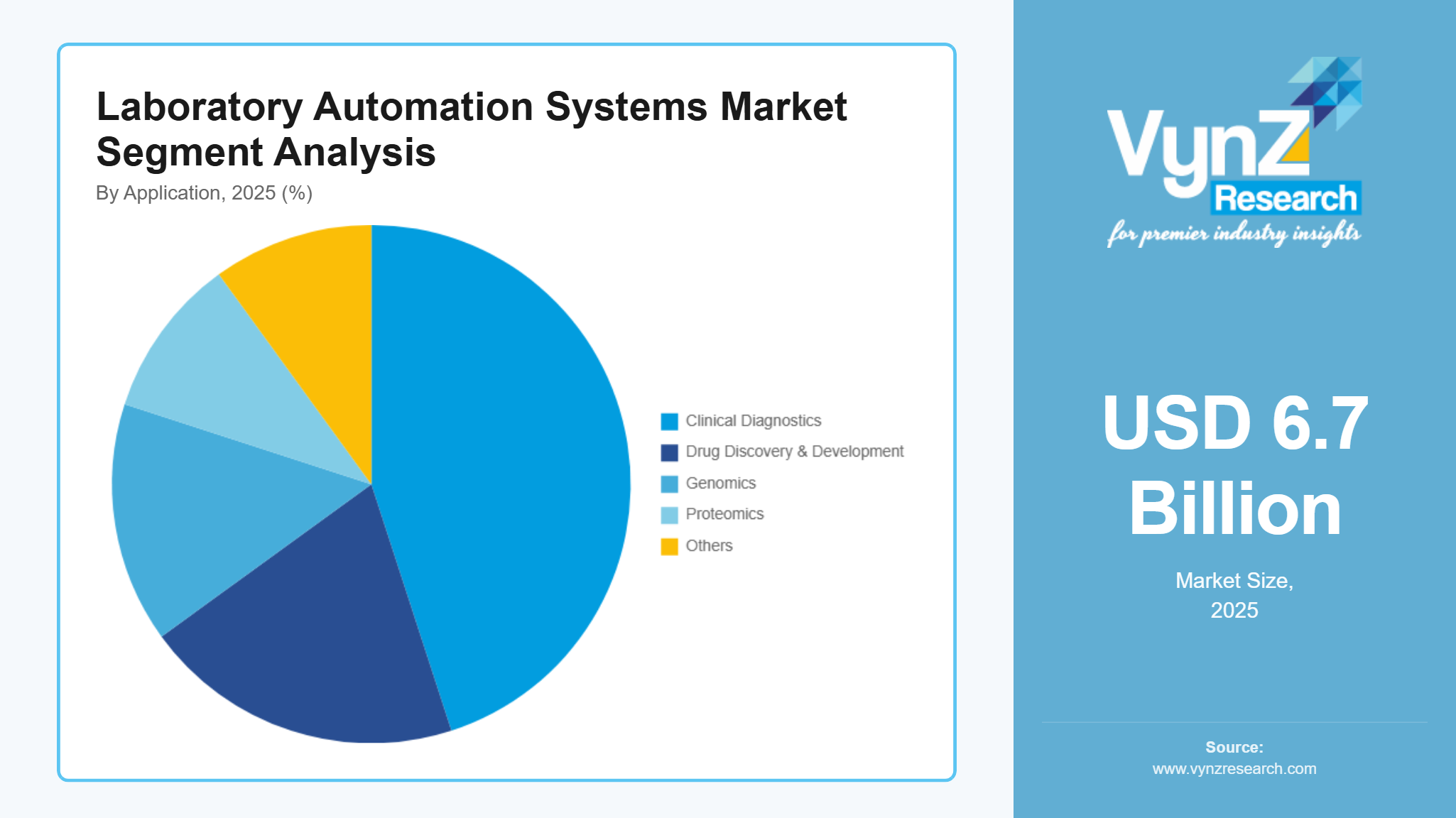

By Application

Clinical Diagnostics is the largest application category with an estimated share of 45% in 2025, due to the sheer volume of routine and urgent testing performed globally. Clinical laboratories generate diagnostics that influence a vast majority of medical decisions, encompassing chemistry panels, hematology, immunoassays, and infectious disease screening. Automated systems help these facilities handle high daily test volumes while improving result accuracy and timeliness. The emphasis on rapid diagnostic turnaround in patient care, emergency settings, and public health surveillance fuels continuous investment in automated analyzers and integrated platforms. As healthcare systems worldwide modernize and demand for routine and complex diagnostics grows, clinical diagnostics remains the dominant application area for automation technologies.

Genomics is the fastest‑growing category as the cost of sequencing continues to fall and demand for precision medicine increases. Genomic workflows are inherently data‑intensive and involve multiple repetitive steps — from sample preparation through data analysis — making them prime candidates for automation. Automated systems streamline these processes, reduce human error, and significantly accelerate throughput. With rising interest in personalized therapies, cancer profiling, and population‑scale sequencing projects, labs are prioritizing automated genomic platforms. The ability to handle large datasets and integrate with advanced bioinformatics tools further boosts automation adoption in this segment. As genomics expands into clinical care and research across diverse geographies, it is set to outpace other application categories in growth.

By End User

Pharmaceutical & biotechnology companies represent the largest enduser category for laboratory automation systems due to their extensive use of automated infrastructure in research, discovery, and production. These organizations rely on automation to accelerate compound screening, molecular analysis, and highthroughput testing, ensuring rapid progression from early discovery to clinical candidate selection. Automation enhances data reliability, reduces human error, and shortens development cycles — all critical for competitive innovation. As pharmaceutical pipelines expand and biotech firms explore complex modalities such as gene and cell therapies, automation investments grow proportionately. Their sustained budgets and strategic focus on operational efficiency position this enduser group as the largest market segment for automation solutions.

Research & academic institutes are the fastestgrowing enduser category, with a CAGR of 9.9% in the coming years, as these institutions increasingly adopt automated technologies to meet rising research complexity and data demands. Academic research has diversified into genomics, proteomics, and systems biology, requiring highthroughput workflows that are impractical to manage manually. Automation accelerates experimental cycles, enables large dataset handling, and frees researchers to focus on discovery rather than routine tasks. Growing government funding for scientific research, collaboration with industry, and integration of automation into graduate training programs further fuel adoption. These institutes are rapidly incorporating modular and targeted automation solutions, driving significant growth in this segment as laboratories transform into more efficient, dataintensive environments.

Regional Insights

Asia Pacific

Asia Pacific is the fastestgrowing region in the laboratory automation systems market, driven by rapid expansion in healthcare infrastructure, rising R&D investment, and expanding diagnostic services. Countries such as China, India, Japan, and South Korea are upgrading national laboratory networks and integrating automation to support drug discovery, genomics, and public health testing. Governments across the region are increasing support for life sciences innovation and quality laboratory services, creating fertile ground for automation vendors. Growing middleclass populations and rising demand for precision medicine further accelerate adoption. As a result, Asia Pacific is witnessing the swiftest growth rates globally, outpacing mature markets due to newly established facilities and increasing automation penetration in both clinical and research settings.

Europe

Europe remains a key market for laboratory automation systems, characterized by strong regulatory frameworks, wellestablished healthcare systems, and significant research activity. Countries across the EU are investing in laboratory modernization as part of broader public health strategy, emphasizing quality assurance, interoperability, and digital transformation. While growth is steadier compared to North America and Asia Pacific, Europe’s emphasis on compliance and standardization drives demand for advanced automation solutions that support traceability, data integrity, and integrated workflows. The region’s rich academic and pharmaceutical ecosystems further reinforce automation adoption. As healthcare providers transition to more efficient, datacentric operations, Europe continues to contribute a substantial share of global automation revenues.

North America

North America stands as the largest regional market for laboratory automation systems, propelled by strong healthcare infrastructure, high R&D expenditure, and widespread adoption of advanced technologies. Clinical diagnostic laboratories, pharmaceutical companies, and academic research centers invest heavily in automation to improve accuracy, throughput, and compliance. Government initiatives such as the U.S. National Institutes of Health’s biomedical research funding totaling over $46 billion in 2025 - underscore longterm public commitment to science and innovation. This robust funding environment, combined with a dense network of research institutions and regulatory support for digital health, cements North America’s position as the dominant region in both automation deployment and market value.

Rest of the World

The rest of the world, encompassing Latin America, the Middle East, and Africa, represents a rapidly emerging market for laboratory automation systems, fueled by expanding healthcare access, rising research initiatives, and public health modernization. Governments across these regions are increasingly prioritizing diagnostic capacity and lab readiness to respond to infectious disease outbreaks and chronic health challenges. In Latin America, national health programs are investing in enhanced laboratory networks to improve diagnostic coverage. Middle Eastern countries are funding biotechnology hubs and research institutions, while African public health agencies are strengthening laboratory infrastructure as part of strategic disease control initiatives. Although automation adoption levels are currently lower than in North America or Europe, the demand trajectory is steep due to rising clinical testing volumes, expanding academic research activity, and growing private sector participation. This makes the Rest of World an important future growth frontier with longterm potential.

Competitive Landscape / Company Insights

The global laboratory automation systems market is moderately consolidated, dominated by a mix of multinational corporations and specialized technology providers. Key players such as Thermo Fisher Scientific, Hamilton Company, Agilent Technologies, hold significant market share through extensive product portfolios, global distribution networks, and strategic partnerships. These companies focus on continuous innovation, offering integrated automated workstations, robotic arms, liquid handling systems, and advanced laboratory software to address diverse applications in clinical diagnostics, drug discovery, and genomics. Smaller regional and niche players contribute to market diversity, particularly in modular automation and specialized applications, fostering competitive pricing and localized solutions. Market competition is also driven by mergers and acquisitions, product launches, and collaborative agreements with research institutions and hospitals. With rising demand for efficiency, accuracy, and digital integration, companies that deliver scalable, flexible, and technologically advanced solutions are positioned to gain long-term leadership in this evolving market.

Mini Profiles

Abbott Laboratories is a global healthcare company providing advanced diagnostic instruments and technologies for clinical laboratories and hospitals, helping deliver accurate and timely results across various testing applications.

Thermo Fisher Scientific Inc. offers laboratory automation, analytical instruments, software, and services that streamline workflows, reduce manual steps, and improve productivity in life sciences research and clinical diagnostics.

Agilent Technologies, Inc. delivers laboratory instruments, software, and integrated solutions supporting life sciences, diagnostics, and applied markets, enabling precise analytical results and efficient workflows.

Tecan Trading AG provides automated liquid handling and laboratory automation platforms that improve efficiency, consistency, and quality in research, drug discovery, and clinical diagnostics workflows.

F. Hoffmann-La Roche Ltd., through Roche Diagnostics, develops diagnostic instruments, automation systems, and software enabling laboratories to enhance throughput, accuracy, and clinical insight across diverse testing areas.

Key Players

- Abbott Laboratories

- Danaher Corporation (Beckman Coulter, Inc.)

- Thermo Fisher Scientific Inc.

- Agilent Technologies, Inc.

- F. Hoffmann-La Roche Ltd.

- Tecan Trading AG

- PerkinElmer AES

- QIAGEN GMBH

- Becton, Dickinson and Company (BD)

- Siemens Healthineers

- Hamilton Company

- Eppendorf Group

Recent Developments

February 2026 - Agilent Technologies, Inc. showcased a suite of nextgeneration automated solutions and workflow innovations at the SLAS2026 International Conference & Exhibition in Boston. The showcase featured advanced imaging enhancements, AIpowered lab optimization tools, and complianceready software modules designed to help laboratories accelerate discovery, improve data quality, and streamline operational productivity.

November 2025 - Abbott Laboratories announced plans to acquire Exact Sciences, a leader in at‑home and laboratory cancer screening tests such as Cologuard and Oncotype DX, in a transaction valued at roughly $21 billion.

October 2025 - Thermo Fisher Scientific Inc. announced a definitive agreement to acquire Clario Holdings, Inc., a leading provider of clinical trial endpoint data solutions, for approximately $8.88 billion in cash. The transaction enhances Thermo Fisher’s digital capabilities in clinical research data and analytics, positioning the company to better support pharmaceutical and biotech customers.

July 2025 - Thermo Fisher Scientific Inc. announced it would acquire Sanofi’s sterile fillfinish manufacturing site in Ridgefield, New Jersey, strengthening local production capacity for critical medicines and expanding partnership with the French pharmaceutical company. The expanded facility supports increased manufacturing needs for pharma and biotech customers in the U.S., improving responsiveness to demand and enriching Thermo Fisher’s service portfolio.

Global Laboratory Automation Systems Market Coverage

Type Insight and Forecast 2026 - 2035

- Equipment

- Software

- Services

Automation Approach Insight and Forecast 2026 - 2035

- Modular Automation

- Total Laboratory Automation (TLA)

Application Insight and Forecast 2026 - 2035

- Clinical Diagnostics

- Drug Discovery & Development

- Genomics

- Proteomics

- Others

End User Insight and Forecast 2026 - 2035

- Pharmaceutical & Biotechnology Companies

- Hospitals & Clinical / Reference Laboratories

- Research & Academic Institutes

- Others

Global Laboratory Automation Systems Market by Region

- North America

- By Type

- By Automation Approach

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Automation Approach

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Automation Approach

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Automation Approach

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Laboratory Automation Systems Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Automation Approach

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Equipment

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Automation Approach

5.2.1. Modular Automation

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Total Laboratory Automation (TLA)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Clinical Diagnostics

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Drug Discovery & Development

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Genomics

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Proteomics

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Others

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Pharmaceutical & Biotechnology Companies

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Hospitals & Clinical / Reference Laboratories

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Research & Academic Institutes

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Others

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Automation Approach

6.3. By

Application

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Automation Approach

7.3. By

Application

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Automation Approach

8.3. By

Application

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Automation Approach

9.3. By

Application

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Abbott Laboratories

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Danaher Corporation (Beckman Coulter, Inc.)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Thermo Fisher Scientific Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Agilent Technologies, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

F. Hoffmann-La Roche Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Tecan Trading AG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

PerkinElmer AES

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

QIAGEN GMBH

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Becton, Dickinson and Company (BD)

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Siemens Healthineers

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Hamilton Company

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Eppendorf Group

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Laboratory Automation Systems Market