Next-Generation Ultrasound System Market Overview

The global Next-Generation Ultrasound Systems Market was valued at USD 8.9 billion in 2023 and is projected to reach USD 22.6 billion by 2030 and is anticipated to witness a CAGR of 9.3% during the forecast period 2025-2030. The next-generation ultrasound system is a device that helps integrate imaging diagnostics into a clinical segment. This device is useful for diagnostic work more efficiently using varied technological aspects. The next-generation ultrasound system is better in terms of quality, affordability, and flexibility than the standard ultrasound system. Owing to the increase in investment for the development of healthcare infrastructure, rising evidence for effective and lucrative results in treatment and diagnosis assistance will propel the growth of the global next-generation ultrasound systems market.

The COVID-19 pandemic has negatively impacted the global next-generation ultrasound system market owing to lockdown, movement restrictions, strict regulations about the opening of production units, private clinics, and other labs. Moreover, disruption in the supply chain, less number skilled staff, recruitment challenges for clinical trials will adversely affect the global next-generation ultrasound system market.

Market Segmentation

Insight by Product Type

Based on product type, the next-generation ultrasound systems market is segmented into diagnostic ultrasound systems and therapeutic ultrasound systems. The therapeutic ultrasound systems further are divided into high-intensity focused ultrasound, extracorporeal shock wave lithotripsy, and Doppler ultrasound. Doppler ultrasound is anticipated to witness the largest share during the forecast period as it can show sharper images in a short period.

Insight by Application

On the basis of application, the global next-generation ultrasound systems market is divided into the cardiovascular system, Vascular Imaging, Obstetrics and Gynecology Imaging, Lung Imaging, Urology Imaging, Orthopedics/Musculoskeletal Imaging, and other imaging. General imaging is anticipated to contribute to the largest share during the forecast period 2021-2027 owing to the rising prevalence of cancer globally, technological development in ultrasound-based diagnosis and treatment, rising market availability and physician preference for HIFU in cancer treatment, growing adoption of focused ultrasound in disease therapies will propel the growth of the global next-generation ultrasound systems market.

Insight by Technology

Based on the technology, the global next-generation ultrasound systems market is divided into 4D/3D ultrasound systems, 2D ultrasound systems, and others (Fusion Imaging Tissue Harmonic Imaging). 4D/3D ultrasound adopts the latest technologies and provides the best image quality for difficult patients and provides a full spectrum of every available function.

Insight by Portability

Based on portability, the next-generation ultrasound systems market is divided into cart/trolley-based systems, handheld devices & wearable, and portable systems. Cart/Trolley-based systems are anticipated to witness the largest share during the forecast period 2025-2030 owing to the rapid usage of technically developed systems globally and mounting adoption of ultrasound systems in acute care settings and emergency care in hospitals, healthcare institutions, and clinics.

Insight by End-User

The global next-generation ultrasound system is divided into hospitals, diagnostics laboratories, and imaging centers, clinics, ambulatory surgical centers, and others. The hospitals are the fastest-growing segment owing to the rising number of patients requiring ultrasound-based medical procedures, growing adoption of minimally invasive diagnostic and surgical procedures, and easy availability of diagnosis.

Global Next-Generation Ultrasound System Market Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 8.9 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 22.6 Billion

|

|

Growth Rate

|

9.3%

|

|

Segments Covered in the Report

|

By Product Type, By Application, By Technology, By Portability, By End-User

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

North America, Europe, Asia-Pacific, Middle East, and Rest of the World

|

Industry Dynamics

Industry Trends

The expansion of ultrasound systems in applications and teleoperated ultrasound systems are the key trends in the next-generation ultrasound systems market.

Growth Drivers

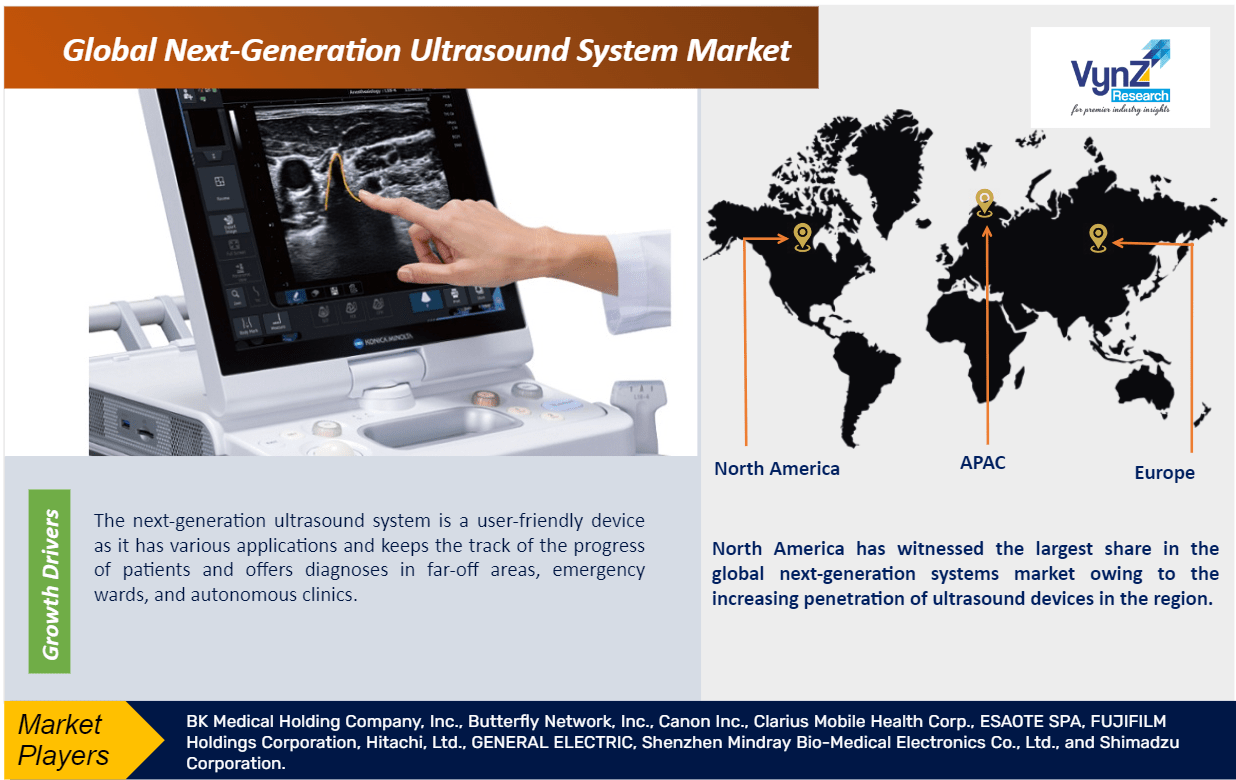

The next-generation ultrasound system is a user-friendly device as it has various applications and keeps the track of the progress of patients and offers diagnoses in far-off areas, emergency wards, and autonomous clinics. Moreover, with the advent of the point-of-care ultrasound system, integration of AI in ultrasound systems, and rising cases of chronic diseases are the main factors driving the growth of the next-generation ultrasound systems market. Moreover, the rising technological development like real-time 3D and 4D ultrasound, high portability, growing entry of industry players, mounting investment in the advancement of healthcare infrastructure will further fuel the growth of the next-generation ultrasound system market.

Challenges

Challenges faced by the next-generation ultrasound system market include limitations owing to resolution and quality of images, product recalls shortage of skilled technicians and rising end-user preference for refurbished equipment.

Opportunities

Enhancing the ultrasound workflow and development in ultrasound technology will create promising opportunities for the companies involved in the global next-generation ultrasound systems market.

Geographic Overview

North America has witnessed the largest share in the global next-generation systems market owing to the increasing penetration of ultrasound devices in the region. Moreover, the usage of portable devices by end-users, spiraling investments by market players to launch innovative and new products, rising prevalence of chronic diseases, and growing healthcare expenditure will bolster the growth of the global next-generation ultrasound system market in the region. Asia-Pacific is projected to have remarkable growth during the forecast period in the global next-generation ultrasound system market owing to the rising prominence of devices in the region.

Competitive Insight

The industry players in the global next-generation ultrasound system market are entering into various strategies such as product launch and enhancement, joint ventures, collaborations and partnerships, product approvals, mergers & acquisitions to establish a strong foothold in the market.

Mindray introduced the novel ME series of portable ultrasound systems to fight the COVID-19 pandemic. These systems feature smart fluid management solutions, comprehensive disinfection solutions, convenient and agile mobility, intuitive interface, and flexible battery solutions to help clinicians address diagnostic challenges and make rapid decisions. The ME series is available in Europe and selected countries.

Hitachi launched ARIETTA 750, a new model in the ARIETTA diagnostic ultrasound series.

Some of the key players operating in the next-generation ultrasound systems market: BK Medical Holding Company, Inc., Butterfly Network, Inc., Canon Inc., Clarius Mobile Health Corp., ESAOTE SPA, FUJIFILM Holdings Corporation, Hitachi, Ltd., GENERAL ELECTRIC, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., and Shimadzu Corporation.

The Next-Generation Ultrasound Systems Market report offers a comprehensive market segmentation analysis along with an estimation for the forecast period 2025–2030.

Segments Covered in the Report

- By Product Type

- Diagnostic Ultrasound Systems

- Therapeutic Ultrasound Systems

- High-Intensity Focused Ultrasound

- Extracorporeal Shock Wave Lithotripsy

- Doppler Ultrasound

- By Application

- Cardiovascular System

- Vascular Imaging

- Obstetrics and Gynaecology Imaging

- Lung Imaging

- Urology Imaging

- Orthopaedics/Musculoskeletal Imaging

- Other Imaging

- By Technology

- 4D/3D Ultrasound Systems

- 2D Ultrasound Systems

- Others (Fusion Imaging Tissue Harmonic Imaging)

- By Portability

- Cart/Trolley-Based Systems

- Handheld Devices & Wearable

- Portable Systems

- By End-User

- Hospitals, Diagnostics Laboratories, and Imaging Centers

- Clinics

- Ambulatory Surgical Centers

- Others

Region Covered in the Report

- North America

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific (APAC)

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Rest of the World (RoW)

- Brazil

- Saudi Arabia

- South Africa

- U.A.E.

- Other Countries

.png "Next Generation Ultrasound System Market Size and Market Analysis")

Source: VynZ Research