Ultrasound Guided Regional Anesthesia Market Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Type (Linear Probe, Curved Array Probe), by Technology (Interscalene, Supraclavicular, Femoral, Transversus Abdominis Plane, Others), by End Use (Hospitals, Ambulatory Surgical Centers, Others)

| Status : Published | Published On : Mar, 2026 | Report Code : VRHC1326 | Industry : Healthcare | Available Format :

|

Page : 185 |

Ultrasound Guided Regional Anesthesia Market Overview

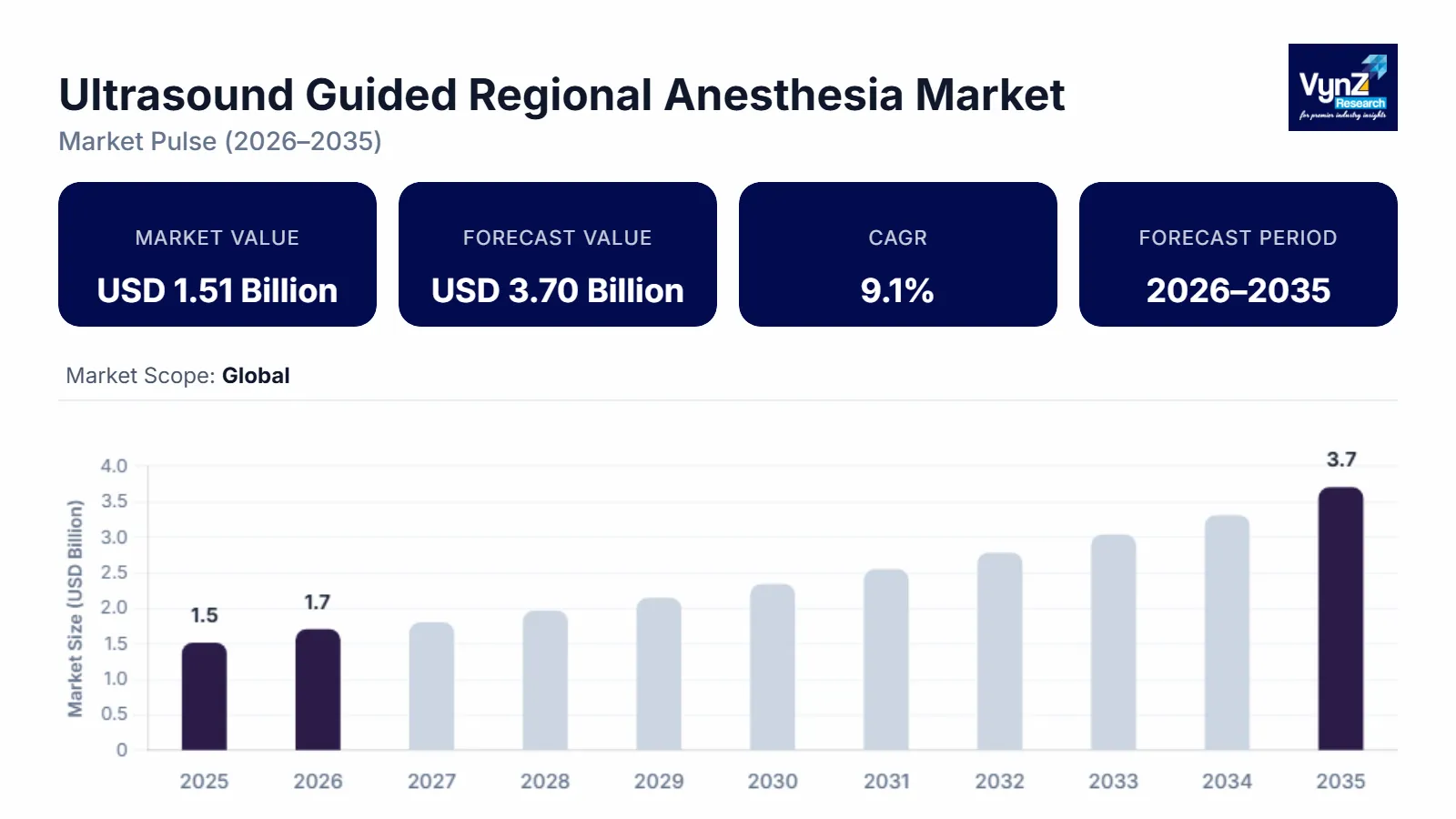

The ultrasound-guided regional anesthesia market which was valued at approximately USD 1.51 billion in 2025 and is estimated to reach around USD 1.7 billion in 2026, is projected to reach close to USD 3.7 billion by 2035, expanding at a CAGR of about 9.1% during the forecast period from 2026 to 2035.

The market is expanding as healthcare systems increasingly prioritize precision, safety, and efficiency in perioperative care. Ultrasound guidance has transformed regional anesthesia from a technique reliant on anatomical estimation into a highly visual, controlled procedure, significantly improving clinical confidence and outcomes. This shift is strongly aligned with the growing emphasis on enhanced recovery protocols, opioid-sparing pain management, and shorter hospital stays.

Rising surgical volumes—particularly in orthopedics and minimally invasive procedures—are accelerating demand for accurate nerve localization and consistent block success. At the same time, the rapid growth of ambulatory surgical centers is driving adoption of portable, high-performance ultrasound platforms that support fast patient turnover without compromising safety. Technological progress, including improved probe resolution, ergonomic designs, and real-time imaging enhancements, is further strengthening clinician adoption across experience levels.

Ultrasound Guided Regional Anesthesia Market Dynamics

Market Trends

An influential trend reshaping the anesthesia landscape is the global shift toward opioid-sparing pain management strategies. In response to escalating public health concerns, governments and health agencies are prioritizing techniques that reduce reliance on systemic opioid administration, which historically contributed to significant morbidity. For example, U.S. government data shows that opioid-related overdose deaths remain a critical public health burden, with tens of thousands of fatalities annually, even as recent declines suggest the impact of comprehensive interventions. In this context, ultrasound-guided regional anesthesia (UGRA) offers a safer alternative by providing targeted nerve blocks that control postoperative pain without high opioid dosages. Beyond improved safety profiles, UGRA enhances patient satisfaction and reduces hospital length of stay by facilitating early ambulation. This broad, clinically supported move away from generalized analgesia toward precision nerve blockade is driving rapid adoption of ultrasound guidance in perioperative and chronic pain settings, making it a standard of care in many healthcare systems committed to reducing opioid dependence.

Growth Drivers

The adoption of ultrasound-guided regional anesthesia is strongly driven by rising global surgical volumes and enhanced recovery after surgery (ERAS) protocols endorsed by government health agencies. Aging populations and the increasing prevalence of chronic conditions such as osteoarthritis are resulting in higher numbers of orthopedic, general, and minimally invasive procedures worldwide. Governments and national health systems emphasize optimized perioperative care pathways that reduce complications and accelerate recovery, directly aligning with the advantages of UGRA techniques. Real-time imaging enables precise nerve localization, significantly reducing procedural risks and variability associated with traditional landmark-based approaches. Public health data from U.S. government sources highlights the persistent challenge of postoperative pain and complications, which can extend hospital stays and increase healthcare costs, reinforcing the need for evidence-based pain management alternatives. UGRA fits within these clinical and policy imperatives by promoting opioid-minimized analgesia, improved functional outcomes, and optimized resource utilization—making it a preferred choice across high-volume surgical centers and national health systems aiming to elevate care quality while controlling costs.

Market Restraints / Challenges

Despite its clinical and economic potential, the widespread adoption of ultrasound-guided regional anesthesia faces a significant challenge: workforce competency and training gaps. Unlike traditional general anesthesia techniques, UGRA requires specialized skills in ultrasound interpretation, needle guidance, and procedural integration that are not yet universally standardized in medical education curricula. Many countries’ public health infrastructure still lacks comprehensive, government-supported training frameworks for anesthesiologists and perioperative nurses, limiting the technique’s consistent application. Moreover, access to advanced ultrasound training—especially in rural or resource-constrained settings—is uneven, compounding disparities in quality of care. This gap hinders broader clinical acceptance and can slow the pace of guideline adoption even as government and professional societies champion evidence-based practices. While clinical outcomes associated with UGRA are well documented in research contexts, translating these into real-world practice requires sustained investment in training programs, simulation platforms, and certification pathways. Addressing these systemic educational deficits is critical to overcoming the workforce barrier and unlocking the full potential of ultrasound-guided anesthesia in global healthcare delivery.

Market Opportunities

One of the most compelling opportunities for the ultrasound-guided regional anesthesia market lies in its integration into national pain management and surgical care guidelines. With public health agencies increasingly focused on improving perioperative outcomes and reducing opioid reliance, there is a growing mandate to embed precision imaging techniques such as UGRA into formal clinical protocols. Government health bodies worldwide are prioritizing evidence-based approaches that deliver measurable patient safety benefits, creating fertile ground for national adoption of ultrasound guidance in nerve blockade procedures. Furthermore, investments in point-of-care ultrasound (POCUS) infrastructure within public hospitals and ambulatory surgical centers present a strategic lever for expanding access to advanced anesthesia services. Countries that institutionalize UGRA within national standard treatment guidelines and funding frameworks stand to enhance surgical care quality while mitigating chronic pain and opioid dependence—a linkage substantiated by sustained public health focus on safer analgesia models. This policy alignment not only advances public health objectives but also opens new pathways for scalable technology adoption, clinician training initiatives, and long-term clinical impact assessment.

Global Ultrasound Guided Regional Anesthesia Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.51 Billion |

|

Revenue Forecast in 2035 |

USD 3.7 Billion |

|

Growth Rate |

9.1% |

|

Segments Covered in the Report |

Type, Technology, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

GE Healthcare, Koninklijke Philips N.V., Siemens Healthineers AG, FUJIFILM SonoSite, Inc., Mindray Medical International Limited, B. Braun Melsungen AG, Canon Medical Systems Corporation, Samsung Medison Co., Ltd., Esaote SPA., Konica Minolta, Inc., Medtronic plc, Vygon |

|

Customization |

Available upon request |

Ultrasound Guided Regional Anesthesia Market Segmentation

By Type

Linear probes are the largest category in the market, with a market share of around 60% in 2025, due to their dominant role in high-volume clinical settings. They provide superior image resolution for superficial nerve structures, making them essential for common orthopedic and peripheral nerve block procedures performed in hospitals and surgical centers worldwide. Public health data from the OECD Health at a Glance 2025 highlights accelerated growth in ambulatory and same-day surgeries across member countries, underscoring broad clinical demand for reliable imaging tools. As government systems prioritize efficiency and patient outcomes, linear probes continue to command the greatest revenue share and clinical preference, cementing their position as a core revenue driver in regional anesthesia markets.

Curved array probes are the fastest-growing category as anesthesia techniques expand beyond superficial nerve blocks into deeper and more complex anatomical regions. Their ability to deliver wider fields of view and deeper tissue penetration makes them particularly valuable for abdominal, pelvic, and lower-limb procedures. As surgical case complexity increases and patient populations become more diverse, clinicians are increasingly relying on curved array probes to achieve accurate nerve localization in challenging scenarios. Additionally, advancements in probe design and image processing are improving usability, further accelerating adoption. This growing clinical reliance positions curved array probes as a key growth driver within the ultrasound-guided regional anesthesia market.

By Technology

Interscalene block is the largest technology category, with an estimated market share of about 25% in 2025, reflecting its central role in shoulder and upper-extremity surgeries. These procedures frequently require precise and reliable pain control to support early mobilization and functional recovery. Ultrasound guidance enhances the accuracy of interscalene blocks, reducing variability and improving clinical confidence. The technique has become well-established across anesthesia practices due to its proven effectiveness and compatibility with modern perioperative care pathways. As demand for orthopedic interventions continues to rise, interscalene blocks remain a foundational nerve block technique, securing their position as the most widely utilized and clinically entrenched technology segment.

The transversus abdominis plane (TAP) block is the fastest-growing technology category with a CAGR of 9.5% during the forecast period, driven by increasing emphasis on effective postoperative pain management for abdominal and minimally invasive surgeries. Ultrasound guidance has significantly improved the safety and consistency of TAP blocks, making them more accessible across varied clinical environments. These blocks support multimodal analgesia strategies by reducing reliance on systemic medications while maintaining strong pain control. As healthcare providers focus on enhanced recovery protocols and patient-centric outcomes, TAP blocks are gaining rapid acceptance. Their expanding role across both inpatient and outpatient surgical pathways positions them as a high-growth technology within the regional anesthesia landscape.

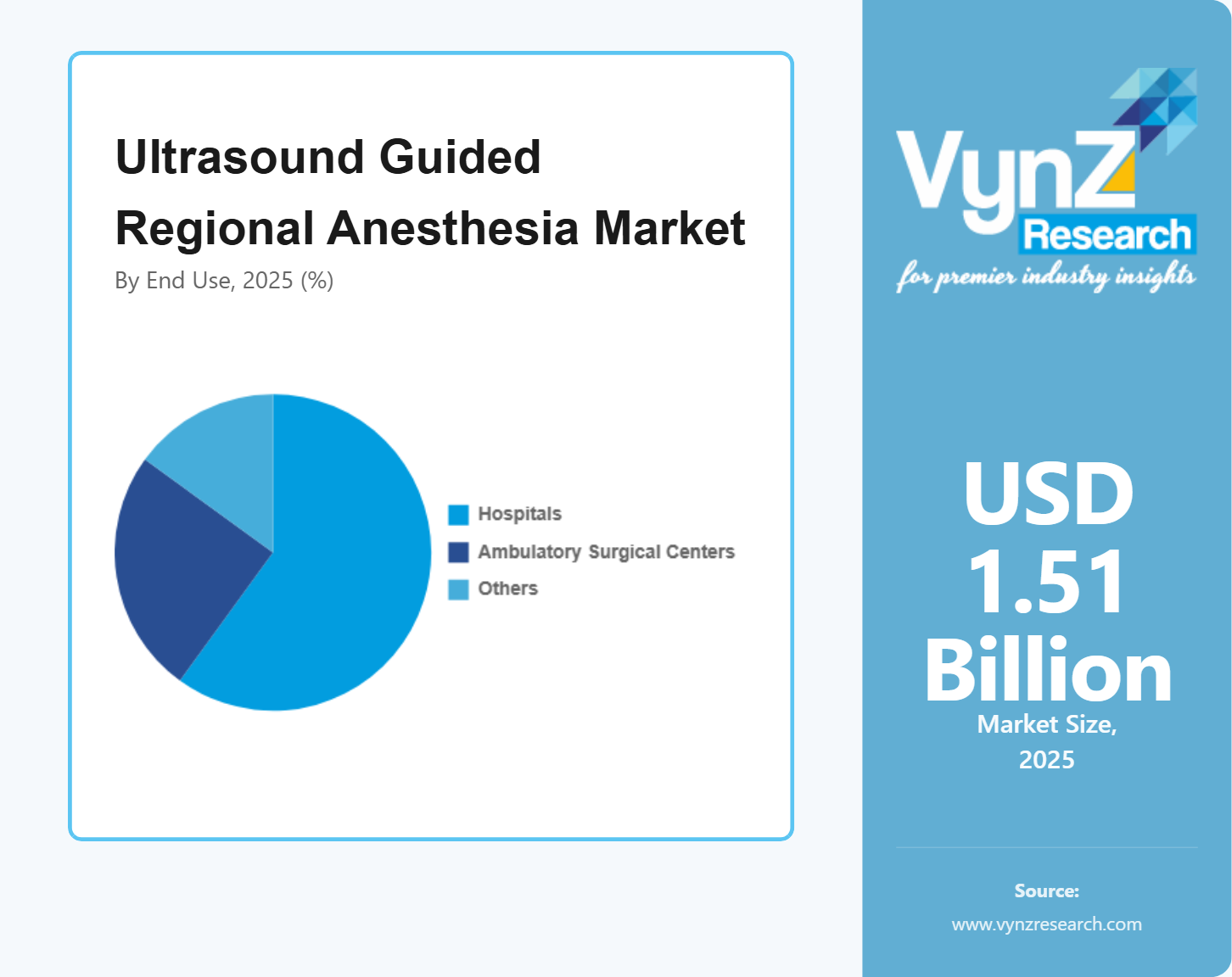

By End Use

Hospitals remain the largest end-use category, with an estimated market share of approx. 65% in 2025, due to their high surgical throughput, advanced infrastructure, and multidisciplinary case complexity. Government healthcare spending data consistently shows that hospitals receive the largest share of public health funding for surgical and anesthesia services. For example, CMS National Health Expenditure projections updated in 2025 confirm that hospital-based surgical care continues to dominate public healthcare utilization. Hospitals are also primary centers for trauma, orthopedic, and high-risk procedures where ultrasound guidance enhances safety and outcomes. This concentration of demand, combined with capital purchasing capacity, ensures hospitals remain the central revenue anchor for the market.

Ambulatory surgical centers are the fastest-growing end-use category as healthcare delivery shifts toward outpatient, efficiency-driven care models. These centers prioritize rapid recovery, streamlined workflows, and predictable pain control - key advantages offered by ultrasound-guided regional anesthesia. Portable ultrasound systems and standardized nerve block protocols are particularly well suited to the operational needs of ambulatory settings. As surgical procedures continue to migrate from inpatient facilities to outpatient environments, ambulatory centers are increasingly adopting advanced anesthesia technologies to enhance throughput and patient experience. This evolution positions ambulatory surgical centers as a critical growth engine for the market.

Regional Insights

Asia Pacific

The Asia Pacific region is the fastest-growing markets for ultrasound-guided regional anesthesia, driven by expanding healthcare infrastructure, rising surgical volumes, and increasing investment in advanced perioperative care. Countries such as China, India, Japan, and South Korea are rapidly adopting image-guided anesthesia to improve surgical outcomes and reduce opioid use. While North America and Europe remain larger in absolute market size, Asia Pacific’s growth rate outpaces them due to government health modernization programs, growing middle-class demand for quality surgical care, and rising numbers of outpatient and orthopedic procedures. As public hospitals and private health systems invest in diagnostic imaging, APAC is poised to become a key long-term growth engine.

Europe

In Europe, ultrasound-guided regional anesthesia holds a substantial market position, supported by mature healthcare systems and strong clinical adoption across both public and private sectors. Countries such as Germany, the United Kingdom, and France are leaders in integrating advanced perioperative imaging into standard protocols to enhance patient safety and improve postoperative recovery. Although Europe is slightly smaller than North America in overall market size, it remains a major regional hub due to high procedural volumes and well-established reimbursement frameworks. Growing emphasis on opioid-reducing pain strategies and enhanced recovery pathways continues to reinforce demand, making Europe a stable and strategically important market.

North America

North America is the largest regional market for ultrasound-guided regional anesthesia owing to advanced healthcare infrastructure, broad clinical adoption, and high procedural volumes across hospitals and ambulatory surgical centers. The United States leads clinical practice standards due to strong integration of imaging guidance in anesthesia curricula and widespread procedural use. Government health data regularly highlights increasing outpatient surgery utilization and quality outcomes tracking, reflecting the regional priority on evidence-based care. Canada also contributes with expanding access to advanced perioperative technologies. This combination of clinical leadership, technology adoption, and established reimbursement mechanisms cements North America’s position as the dominant regional market.

Rest of the World

The rest of the world, encompassing Latin America, the Middle East, and Africa, represents a rapidly evolving category of the ultrasound-guided regional anesthesia market with strong growth potential. These regions are characterized by expanding healthcare access, rising surgical frequencies, and increasing government commitments to modernize clinical services. Although they currently trail North America, Europe, and Asia Pacific in absolute market size, investments in hospital infrastructure and diagnostic imaging are accelerating adoption. In parts of Latin America and the Gulf Cooperation Council countries, national health strategies are prioritizing enhanced surgical care and pain management protocols, making ultrasound guidance increasingly relevant. Sub-Saharan Africa and other emerging healthcare markets are also showing nascent demand, driven by private hospital growth and rising awareness of advanced anesthesia techniques.

Competitive Landscape / Company Insights

The competitive landscape of the ultrasound-guided regional anesthesia market is moderately fragmented, characterized by the presence of established medical imaging companies alongside specialized anesthesia-focused players. Market competition is shaped by continuous product innovation, clinical performance differentiation, and the ability to integrate ultrasound systems seamlessly into perioperative workflows. Leading participants compete on image quality, probe versatility, portability, and ease of use, while also strengthening their positions through training support and long-term service offerings.

At the same time, niche manufacturers and emerging players are gaining traction by focusing on compact systems, cost-efficient solutions, and technology tailored for ambulatory and resource-constrained settings. Strategic partnerships with hospitals, surgical centers, and academic institutions are increasingly used to drive adoption and brand loyalty. As clinical demand expands across both mature and emerging healthcare markets, competition is expected to intensify, with success driven by innovation speed, clinical credibility, and the ability to scale across diverse care environments.

Mini Profiles

GE Healthcare provides medical imaging, ultrasound, and digital solutions that support diagnosis, monitoring, and precision care across hospitals and surgical environments worldwide.

Koninklijke Philips N.V. is a global health technology company delivering integrated solutions in imaging, ultrasound, and patient monitoring to improve clinical outcomes and care efficiency

Siemens Healthineers AG develops advanced imaging, diagnostics, and digital healthcare solutions that enable data-driven clinical decision-making across care pathways.

Mindray Medical International Limited designs and manufactures medical devices including ultrasound systems and patient monitoring solutions for hospitals and healthcare providers globally.

FUJIFILM SonoSite, Inc. focuses on portable and point-of-care ultrasound systems designed for fast, reliable imaging in perioperative and critical care settings.

Key Players

- GE Healthcare

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- FUJIFILM SonoSite, Inc.

- Mindray Medical International Limited

- B. Braun Melsungen AG

- Canon Medical Systems Corporation

- Samsung Medison Co., Ltd.

- Esaote SPA

- Konica Minolta, Inc.

- Medtronic plc

- Vygon

Recent Developments

February 2026 - Koninklijke Philips N.V. entered local manufacturing partnerships in Indonesia with PT PHC Indonesia and PT Graha Teknomedika to produce advanced ultrasound systems and hospital patient monitoring solutions domestically, expanding access and local industry capability.

December 2025 - Koninklijke Philips N.V. agreed to acquire SpectraWAVE Inc., a specialist in next-generation coronary imaging and AI-enabled physiological assessment, further expanding its image-guided therapy portfolio and AI-driven technologies.

December 2025 - Mindray Medical International Limited introduced the Resona A20 ultra-premium ultrasound system, featuring intelligent automation and advanced imaging tools designed to enhance diagnostic precision and workflow efficiency.

November 2025 - GE HealthCare announced plans to acquire Intelerad, a cloud-based medical imaging software provider, for USD 2.3 billion to strengthen its outpatient imaging and enterprise software capabilities.

Global Ultrasound Guided Regional Anesthesia Market Coverage

Type Insight and Forecast 2026 - 2035

- Linear Probe

- Curved Array Probe

Technology Insight and Forecast 2026 - 2035

- Interscalene

- Supraclavicular

- Femoral

- Transversus Abdominis Plane

- Others

End Use Insight and Forecast 2026 - 2035

- Hospitals

- Ambulatory Surgical Centers

- Others

Global Ultrasound Guided Regional Anesthesia Market by Region

- North America

- By Type

- By Technology

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Technology

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Technology

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Technology

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Ultrasound Guided Regional Anesthesia Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Technology

1.2.3. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Linear Probe

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Curved Array Probe

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Interscalene

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Supraclavicular

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Femoral

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Transversus Abdominis Plane

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Others

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By End Use

5.3.1. Hospitals

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Ambulatory Surgical Centers

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Others

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Technology

6.3. By

End Use

6.3.1.

U.S. Market Estimate and Forecast

6.3.2.

Canada Market Estimate and Forecast

6.3.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Technology

7.3. By

End Use

7.3.1.

Germany Market Estimate and Forecast

7.3.2.

France Market Estimate and Forecast

7.3.3.

U.K. Market Estimate and Forecast

7.3.4.

Italy Market Estimate and Forecast

7.3.5.

Spain Market Estimate and Forecast

7.3.6.

Russia Market Estimate and Forecast

7.3.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Technology

8.3. By

End Use

8.3.1.

China Market Estimate and Forecast

8.3.2.

Japan Market Estimate and Forecast

8.3.3.

India Market Estimate and Forecast

8.3.4.

South Korea Market Estimate and Forecast

8.3.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Technology

9.3. By

End Use

9.3.1.

Brazil Market Estimate and Forecast

9.3.2.

Saudi Arabia Market Estimate and Forecast

9.3.3.

South Africa Market Estimate and Forecast

9.3.4.

U.A.E. Market Estimate and Forecast

9.3.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

GE Healthcare

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Koninklijke Philips N.V.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Siemens Healthineers AG

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

FUJIFILM SonoSite, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Mindray Medical International Limited

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

B. Braun Melsungen AG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Canon Medical Systems Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Samsung Medison Co., Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Esaote SPA

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Konica Minolta, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Medtronic plc

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Vygon

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Ultrasound Guided Regional Anesthesia Market