Pediatric Medical Device Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Diagnostic Devices, Monitoring Devices, Therapeutic Devices, Surgical Devices, Respiratory Devices, Cardiovascular Devices, Neonatal Care Devices, Drug Delivery Devices, Others), by Age Group (Neonates (0–28 days), Infants (1–12 months), Children (1–12 years), Adolescents (13–18 years)), by Application (Cardiology, Respiratory Care, Neonatal Care, Orthopedics, Neurology, General Surgery, Others), by End User (Hospitals, Pediatric Clinics, Neonatal Intensive Care Units (NICUs), Ambulatory Surgical Centres (ASCs), Home Healthcare), by Technology (Conventional Devices, Smart / Connected Devices (IoT-enabled))

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1332 | Industry : Healthcare | Available Format :

|

Page : 190 |

Pediatric Medical Device Market Overview

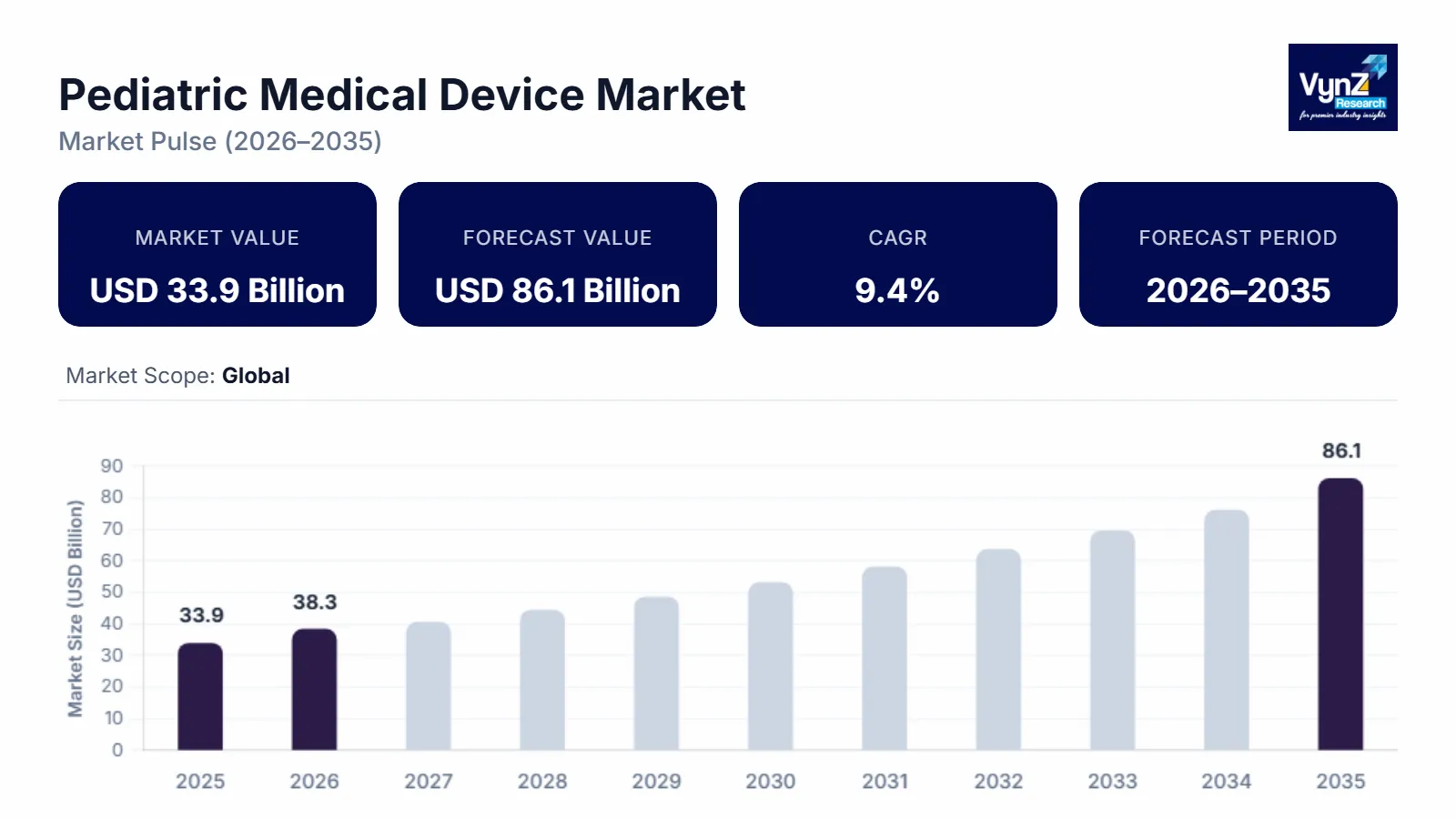

The pediatric medical device market, which was valued at approximately USD 33.9 billion in 2025 and is estimated to reach around USD 38.3 billion in 2026, is projected to reach close to USD 86.1 billion by 2035, expanding at a CAGR of about 9.4% during the forecast period from 2026 to 2035.

The pediatric medical device industry has been primarily influenced by the interplay of two primary factors: demographics and clinical needs, and technology innovation. As the number of births increases globally, especially in many developing countries, it is also expected that there will be an increase in the population of premature babies due to improved survival rates resulting from new advances in neonatal care. Both of these trends create a larger pool of patients who have unique infant and childhood physiology characteristics that necessitate small-sized medical equipment for their use, thereby fuelling growth in both neonatal and pediatric markets. There is also a trend towards increased incidence of chronic or congenital conditions (e.g., cardiovascular defects, asthma, etc.) among children.

In addition to needing early and timely diagnosis of these conditions, they may also need to be monitored continuously and treated over extended periods. Therefore, this growing trend in chronic/congenital disease creates significant opportunities for companies focused on developing diagnostic, monitoring, and therapeutic products for children. Additionally, there is a growing trend towards earlier prevention and intervention in medicine generally, which will help to foster continued growth in demand for high-quality and user-friendly medical technologies for children.

Pediatric Medical Device Market Dynamics

Market Trends

The use of a child-sized design for products, as well as an increase in the use of digital technology, are examples of major trends that are shaping the pediatric medical device marketplace. This includes the integration of digital features or connectivity into diagnostic devices used in neonatal and pediatric units within the hospital setting. The use of these technologies can result in quicker recognition of deteriorating patient status and enable more consistent monitoring of patients with chronic diseases. Additionally, there will be increased utilisation of minimally invasive surgical techniques in various areas such as pediatric cardiology, urology, and general surgery. As this occurs, it will create a greater demand for small-diameter catheters, guidewires, endoscopic instruments, etc., and image-guided devices to assist in visualisation during surgical procedures. Further, hospitals and children's speciality centres are making investments in advanced neonatal and pediatric respiratory support systems, infusion technologies, and portable diagnostic testing systems to enhance their ability to provide quality critical care services to patients. In some cases, government-funded infrastructure improvements have been implemented in developing countries. For example, the National Health Mission in India has indicated that facilities throughout the country are being expanded to include newborn care. According to the NHM, as of September 2019, there were 602 Special Newborn Care Units (SNCUs) established across the country, along with 2,228 Newborn Stabilisation Units (NBSUs), and 16,968 Newborn Care Corners (NBCCs). These SNCUs, NBSUs, and NBCCs will continue to drive purchases of neonatal and pediatric care equipment. These developments will all contribute to reducing complications associated with treatment and improving the health outcome for pediatric patients.

Growth Drivers

The primary growth drivers of the pediatric medical device industry are increased neonatal and pediatric illness, better access to specialised pediatric care, and growing needs for devices that are appropriate for size and validation for children versus being used “off-label” from adult applications. The clinical demand for devices is also supported by the ongoing relevance of newborn/neonatal care: as of 2024, UNICEF estimates there were 2.3 million children who died within the first month of life, and as such, there is a need for effective technologies for neonatal monitoring, respiratory assistance, warming, infusion, and infection control. Additionally, chronic or lifelong use of devices will be required for many congenital conditions; i.e., according to the U.S. Centres for Disease Control and Prevention, nearly 1% of all births (approximately 40,000 annually in the United States) result in a child with a congenital heart defect, which supports both diagnostic and therapeutic pediatric cardiology intervention demands. From a market-enabling perspective, regulatory and innovation incentives to develop more pediatric-labelled products will continue to grow the number of available pediatric-labelled devices; the U.S. FDA's Pediatric Device Consortia (PDC) Grant programme has had an approximate $6 million annual budget since its inception and was re-authorised in FYs 23 through 27 via the Food & Drug Omnibus Reform Act of 2022. This grant programme provides financial resources for developing pediatric medical device technology and advisory services to advance pediatric medical device projects. All of these factors continue to support clinical demand for pediatric-specific medical devices at hospitals, pediatric speciality clinics, and in-home-based care.

Market Restraints / Challenges

Some of the biggest hurdles in developing products for the Pediatric Medical Device Market consist of a smaller population that is eligible for treatment within each product category, the necessity to prove the safety and performance of products in multiple age/weight bands of paediatrics, as well as the operational complexities associated with conducting clinical studies on children. The development of pediatric-specific products must account for growth, anatomy of the pediatric patient, and differing physiology as compared to adult patients. These factors will make development costs greater than those associated with adult products, manufacturing complexity, and the costs associated with acquiring approval from regulatory agencies. Hospitals often use adapted versions of adult products due to the lack of available pediatric-specific products for many product categories; this creates usability issues and increases the burden of risk management. Additionally, there is significant variability associated with reimbursement and procurement constraints for manufacturers who produce higher-cost implantable and advanced monitoring systems. Finally, there are supply chain continuity issues related to specialised components (miniaturised sensors, pediatric-sized consumables, biocompatible materials); these can impact lead times and serviceability.

Market Opportunities

The increased adoption of in-home pediatric care equipment represents an enormous opportunity in the pediatric medical device space, as families seek to leverage the convenience and personalised nature of at-home delivery. In Europe, the new EU4Health Programme (2021–2027), which will be funded with almost €5.3 billion, aims to improve the quality of the overall healthcare system, increase the use of digital health technology, and enhance remote care delivery. Due to the high frequency of hospital visits associated with caring for a child's illness or condition, parents and caregivers are increasingly looking for ways to manage their child's health from the comfort of their own homes. Portable monitors, home-use ventilators, wearable sensors, and smart medication dispensing devices enable effective management of common chronic conditions like respiratory disorders, congenital diseases, and post-surgery recovery. As part of its Healthy China 2030 initiative, the Chinese government has made significant investments in the development of digital healthcare. The promotion of “internet hospitals” and remote monitoring systems has been one of the most important initiatives. With public and private investment in digital health infrastructure exceeding $10 billion in recent years, it is expected that there will be rapid adoption of in-home-based technologies related to pediatric wearables and remote diagnostics.

Global Pediatric Medical Device Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 33.9 Billion |

|

Revenue Forecast in 2035 |

USD 86.1 Billion |

|

Growth Rate |

9.4% |

|

Segments Covered in the Report |

Product Type, Age Group, Application, End User, Technology |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Key Companies |

Medtronic plc, Abbott Laboratories, Johnson & Johnson (DePuy Synthes), Koninklijke Philips N.V., GE HealthCare, Siemens Healthineers AG, Stryker Corporation, Boston Scientific Corporation, Baxter International Inc., Becton, Dickinson and Company (BD) |

|

Customization |

Available upon request |

Pediatric Medical Device Market Segmentation

By Product Type

Diagnostic devices are the largest category, with a market share of about 20% in 2025, due to the widespread use of diagnostic technologies such as imaging, point-of-care testing, and screening technologies throughout both neonatal and pediatric care delivery pathways. Due to their reliance on diagnostic technology for early identification of congenital defects, determination of whether an infection exists, or continuing monitoring of a child's chronic disease, hospitals and pediatric speciality centres will continue to experience recurrent demand for diagnostic equipment that is capable of pediatric patients, including pediatric imaging systems, ultrasound, and other appropriate diagnostic consumables.

Neonatal care devices are the fastest-growing category, with a CAGR of 9.6% during the forecast period, owing to sustained investment in NICU capability and the ongoing need for advanced thermoregulation, monitoring, respiratory support, and infusion technologies tailored to premature and critically ill newborns. Demand is further supported by the modernisation of neonatal units, improved clinical protocols, and the adoption of safer, more precise devices designed for very low birth-weight infants. As neonatal survival and quality-of-care metrics remain a priority for health systems, neonatal care-focused devices are expected to see strong growth across both mature and emerging markets.

By Age Group

Children (1–12 years) are the largest category, with a market share of about 35% in 2025, due to high utilisation rates of diagnostic, monitoring, and surgical devices across routine pediatric care, chronic disease management, and elective procedures. Hospitals and speciality centres provide treatment for a wide range of conditions among children in this age band, which generates recurring demand for capable imaging and monitoring systems, as well as orthopaedic supports that are properly sized for children, along with consumables and accessories appropriate for their size. Expansion of pediatric speciality services and accessibility of properly sized equipment will continue to encourage use.

Neonates (0–28 days) are the fastest-growing category during the forecast period; this growth is being fuelled by a continued commitment from hospitals to increase the number of beds available in their neonatal intensive care units (NICUs). Additionally, there is an increased demand for various medical equipment used to monitor patients; provide respiratory support; control body temperature (thermoregulation); and administer medication through IV lines. The overall trend for this age group includes the widespread implementation of new technology, as well as updates to current clinical practices, which will be more effective at providing safer and more accurate treatments for babies born with extremely low birth weights.

By Application

Neonatal care is the largest category, with a market share of about 25% in 2025, due to high-acuity medical devices being utilised primarily within NICUs for managing premature and critically ill newborns. The primary users of neonatal equipment are hospitals and children's speciality facilities that use neonatal technology (monitoring, respiratory support, thermoregulation, and infusion/drug delivery) to treat the multitude of clinical challenges associated with neonatal care. As such, there will be continued purchases of neonatal-capable systems as well as neonatal consumables. In addition, investments in NICU infrastructure, education and training of NICU staff, and standardisation of care pathways will also drive the purchase of new or updated systems as existing ones are replaced.

Cardiology is the fastest-growing category during the forecast period, as a result of the ongoing need for diagnosing and treating congenital heart disease, as well as pediatric arrhythmia, using an interventional approach. This growth can be attributed to: increased access to pediatric echocardiography and imaging, an increase in catheter-based intervention when it is deemed to be clinically acceptable, and an increase in availability of pediatric-sized catheters, guidewires and monitoring solutions.

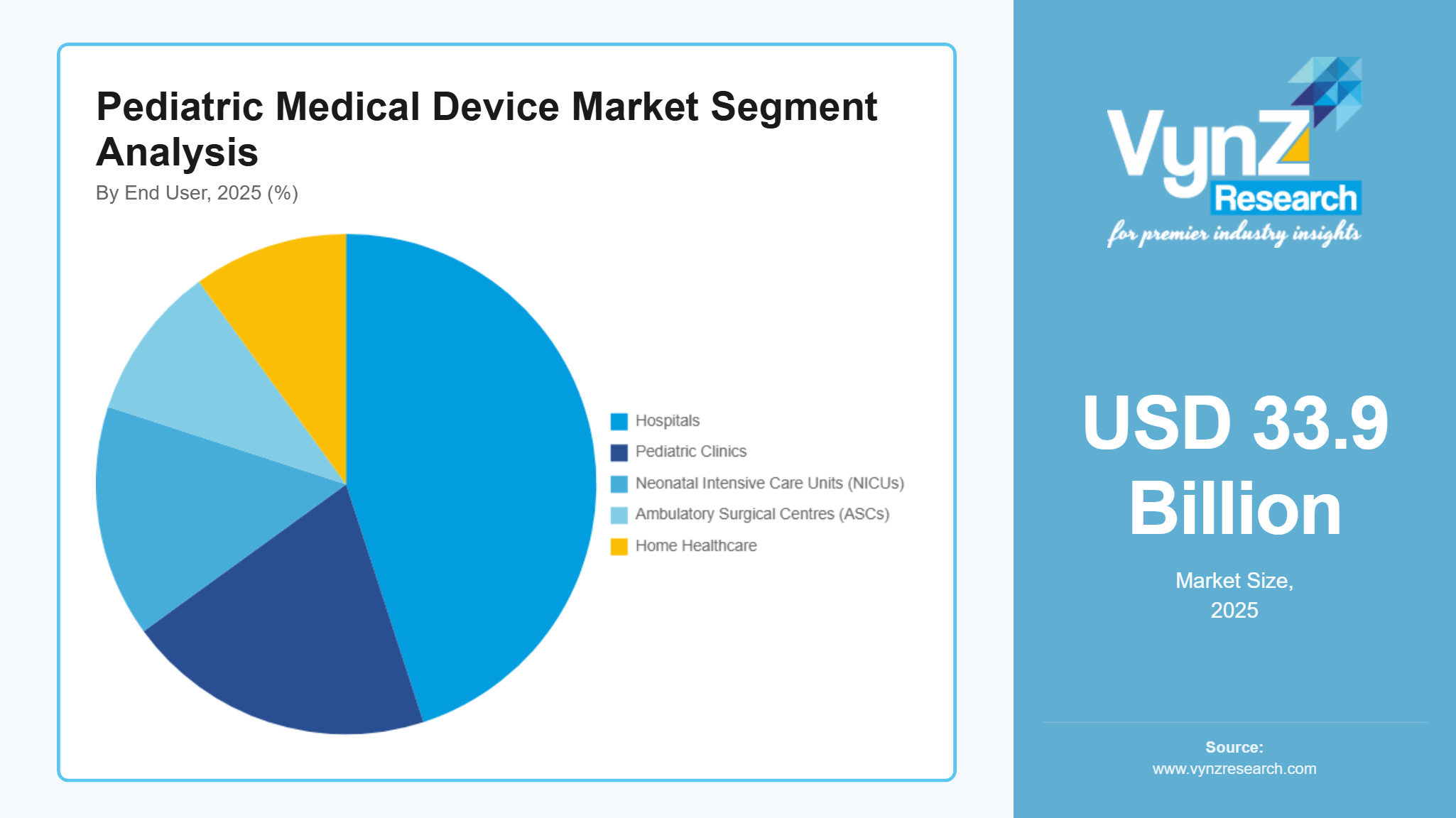

By End User

Hospitals are the largest category, with a market share of about 45% in 2025, as they offer a concentration of NICU/PICU beds, pediatric radiology services, pediatric surgery, and cardiology services requiring high-acuity devices and specific pediatric consumables. In addition, hospitals and children's hospitals provide ongoing purchasing of critical care and monitoring products such as ventilators, monitors, infusion pumps, and pediatric-specific device attachments, which are supported by service agreements and the use of common platforms. The continued development of pediatric specialities and quality-of-care programmes will continue to support the top-line contribution of hospitals to overall market revenue.

Home healthcare is the fastest-growing category during the forecast period, due to increasing use of portable and connected monitoring devices for home-based respiratory support in select cases, structured post-discharge follow-up pathways for chronic pediatric conditions and telehealth programs and device design that provide carer training and improve safety and usability outside acute-care environments.

By Technology

Conventional devices are the larger category, with a market share of about 70% in 2025, as they have been widely adopted in hospitals and clinics throughout the world for their use in diagnostic, monitoring, respiratory, surgical, and neonatal care systems. Traditional pediatric platforms provide reliable performance, standardise clinical protocols, and offer a wide variety of pediatric-capable configurations and consumables. In addition to being used for routine replacements and maintenance of existing equipment, traditional pediatric platforms will continue to be needed for future upgrades to continuing infrastructure in the NICU/PICU and pediatric units.

Smart/connected devices are the faster-growing category, with a CAGR of 9.9% during the forecast period, as a result of an increase in the use of patient monitoring technologies for remote patients, improved compatibility of medical equipment with hospital information systems, as well as analytics technology that enables clinicians to identify potential issues sooner than they could historically in Neonatal Intensive Care Units (NICUs) and pediatric units. The demand for smart/connected medical equipment has also increased due to advancements in miniaturising sensors, improving software functionality, as well as enhanced cybersecurity and regulatory compliance, allowing for safe deployment of connected technologies.

Regional Insights

North America

North America accounted for approximately 36% of the market in 2025, driven by advanced pediatric healthcare infrastructure, high adoption of NICU/PICU technologies, and strong presence of specialized children’s hospitals across the United States and Canada. Strong demand from major healthcare hubs continues to support market growth, particularly for pediatric imaging, respiratory care, monitoring, and minimally invasive surgical devices. According to the U.S. FDA, the Pediatric Device Consortia (PDC) Grant Program continues to provide annual funding support for pediatric medical device innovation and commercialization activities.

Government initiatives, combined with rising demand for advanced neonatal and pediatric care technologies, are encouraging investments in pediatric monitoring systems, diagnostic imaging equipment, and specialized surgical devices across the region.

Asia-Pacific

Asia Pacific accounted for approximately 29% of the market in 2025, supported by large pediatric populations, improving healthcare infrastructure, and increasing investments in maternal and child healthcare services across China, India, Japan, and Southeast Asia. Increasing adoption across neonatal intensive care units, pediatric hospitals, and specialty care centers is driving consistent demand for respiratory care, monitoring, imaging, and bedside diagnostic devices. According to the Government of India, the Scheme for Strengthening the Medical Device Industry includes investments of nearly ₹500 crore to support medical device manufacturing, infrastructure, clinical research, and medical device parks.

Government healthcare programs, rising NICU expansion projects, and growing adoption of connected and portable pediatric monitoring technologies are further accelerating regional market growth.

Europe

Europe accounted for approximately 18% of the market in 2025, driven by established healthcare systems, high standards of neonatal and pediatric care, and continuous investments in hospital modernization across Germany, France, the United Kingdom, Italy, and Nordic countries. Demand remains strong for pediatric monitoring systems, neonatal respiratory devices, diagnostic imaging equipment, and pediatric cardiology technologies. According to the European Union, the Horizon Europe Program allocated approximately €8.2 billion toward healthcare research and innovation initiatives supporting advanced medical technologies.

Growth in Europe is supported by increasing investments in pediatric specialty care, expansion of neonatal care capabilities, and rising adoption of technologically advanced pediatric medical devices.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, accounted for approximately 7% of the market in 2025, supported by improving healthcare infrastructure, rising birth rates, and increasing focus on maternal and child healthcare programs. Countries such as Brazil, Mexico, Saudi Arabia, and South Africa are investing in neonatal monitoring systems, ventilators, and pediatric diagnostic equipment to strengthen pediatric care capabilities.

Government healthcare investments, expansion of private hospital networks, and international initiatives focused on reducing infant and child mortality are expected to support long-term demand for pediatric-specific medical devices across these regions. Collectively, the above-mentioned regional markets account for nearly 90% of the global pediatric medical devices market, while the remaining share is distributed among smaller developing markets worldwide.

Competitive Landscape / Company Insights

The pediatric medical device industry has a moderate level of fragmentation. There are many different large med-tech organisations globally that have developed products for pediatric patients and their families. In addition, there are several large imaging- and monitoring-focused med-tech organisations. As well, there are smaller organisations that specialise in providing devices for pediatric and neonatal patient populations. Medtronic plc, Abbott Laboratories, Koninklijke Philips N.V., GE HealthCare, and Siemens Healthineers AG all operate in this space. They provide both the devices and the consumables necessary to perform diagnostic testing, monitor patients, image patients, provide respiratory care, administer drugs via infusion pumps, and deliver some forms of cardiovascular and surgical treatments for infants and young children. The major competitors in the pediatric medical device industry also benefit from having scale (global) and service networks. In addition, they have the advantage of being able to offer fully integrated device ecosystems, which allows them to be competitive within the pediatric medical device space, especially within high-acuity hospital environments like NICUs and PICUs. Competitors to the larger medical device and healthcare technology providers focus on creating products or developing services that address specific needs or opportunities in the pediatric medical device marketplace. Examples of areas of competition include neonatal respiratory support, consumables, and thermoregulation for use in NICUs, accessories for pediatric monitoring, pediatric orthopaedic solutions, and software-enabled monitoring and workflow solutions.

Mini Profiles

Medtronic plc is a global medical technology company with offerings across cardiovascular, surgical, and monitoring domains, including products used in pediatric and neonatal care settings, depending on the indication and configuration.

Abbott Laboratories provides medical devices and diagnostics, including cardiovascular and point-of-care testing technologies that are utilised in pediatric care, depending on clinical indication and product configuration.

Koninklijke Philips N.V. offers hospital patient monitoring, imaging, and clinical informatics technologies that support neonatal and pediatric care workflows in many healthcare settings.

GE HealthCare provides diagnostic imaging and ultrasound systems as well as monitoring solutions that are widely deployed in pediatric and neonatal care for diagnosis and patient management.

Siemens Healthineers AG supplies imaging, diagnostics, and related healthcare technologies used in pediatric care pathways, including radiology and ultrasound applications that support diagnosis and treatment planning.

Key Players

- Medtronic plc

- Abbott Laboratories

- Johnson & Johnson

- Koninklijke Philips N.V.

- GE HealthCare

- Siemens Healthineers AG

- Stryker Corporation

- Boston Scientific Corporation

- Baxter International Inc.

- Becton, Dickinson and Company

Recent Developments

In December 2025, Abbott announced that its Amplatzer Piccolo Delivery System received U.S. FDA clearance and CE Mark to help optimize procedures for premature babies with patent ductus arteriosus (PDA), strengthening its neonatal and pediatric structural heart portfolio.

In May 2025, GE HealthCare announced that the U.S. FDA approved a pediatric indication for Option (perflutren protein-type A microspheres), an ultrasound-enhancing agent to improve echocardiogram image quality and diagnostic confidence in pediatric patients.

In March 2026, Medtronic announced U.S. FDA clearance for its Stealth Axis surgical system for cranial and ENT procedures, reflecting ongoing development of advanced surgical technologies relevant to pediatric operating room environments, depending on indication and use setting.

In February 2026, Koninklijke Philips N.V. introduced the Snuggle flexible pediatric MRI coil for its 3.0T MRI systems, designed to improve imaging comfort, efficiency, and diagnostic precision for pediatric patients.

In January 2026, Siemens Healthineers AG expanded its pediatric imaging and AI-enabled monitoring capabilities through upgrades to its pediatric ultrasound and diagnostic workflow solutions aimed at improving neonatal and pediatric care efficiency in hospitals and specialty centers.

Global Pediatric Medical Device Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Diagnostic Devices

- Monitoring Devices

- Therapeutic Devices

- Surgical Devices

- Respiratory Devices

- Cardiovascular Devices

- Neonatal Care Devices

- Drug Delivery Devices

- Others

Age Group Insight and Forecast 2026 - 2035

- Neonates (0–28 days)

- Infants (1–12 months)

- Children (1–12 years)

- Adolescents (13–18 years)

Application Insight and Forecast 2026 - 2035

- Cardiology

- Respiratory Care

- Neonatal Care

- Orthopedics

- Neurology

- General Surgery

- Others

End User Insight and Forecast 2026 - 2035

- Hospitals

- Pediatric Clinics

- Neonatal Intensive Care Units (NICUs)

- Ambulatory Surgical Centres (ASCs)

- Home Healthcare

Technology Insight and Forecast 2026 - 2035

- Conventional Devices

- Smart / Connected Devices (IoT-enabled)

Global Pediatric Medical Device Market by Region

- North America

- By Product Type

- By Age Group

- By Application

- By End User

- By Technology

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Age Group

- By Application

- By End User

- By Technology

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Age Group

- By Application

- By End User

- By Technology

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Age Group

- By Application

- By End User

- By Technology

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Pediatric Medical Device Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Age Group

1.2.3. By

Application

1.2.4. By

End User

1.2.5. By

Technology

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Diagnostic Devices

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Monitoring Devices

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Therapeutic Devices

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Surgical Devices

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Respiratory Devices

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Cardiovascular Devices

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Neonatal Care Devices

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Drug Delivery Devices

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.1.9. Others

5.1.9.1. Market Definition

5.1.9.2. Market Estimation and Forecast to 2035

5.2. By Age Group

5.2.1. Neonates (0–28 days)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Infants (1–12 months)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Children (1–12 years)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Adolescents (13–18 years)

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Cardiology

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Respiratory Care

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Neonatal Care

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Orthopedics

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Neurology

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. General Surgery

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. Others

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Pediatric Clinics

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Neonatal Intensive Care Units (NICUs)

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Ambulatory Surgical Centres (ASCs)

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Home Healthcare

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By Technology

5.5.1. Conventional Devices

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Smart / Connected Devices (IoT-enabled)

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Age Group

6.3. By

Application

6.4. By

End User

6.5. By

Technology

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Age Group

7.3. By

Application

7.4. By

End User

7.5. By

Technology

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Age Group

8.3. By

Application

8.4. By

End User

8.5. By

Technology

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Age Group

9.3. By

Application

9.4. By

End User

9.5. By

Technology

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Medtronic plc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Abbott Laboratories

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Johnson & Johnson

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Koninklijke Philips N.V.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

GE HealthCare

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Siemens Healthineers AG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Stryker Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Boston Scientific Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Baxter International Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Becton, Dickinson and Company

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Pediatric Medical Device Market