Edge AI Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Device (Smartphones, Smart Cameras, Robots, Autonomous Vehicles, Wearables, Smart Speakers, Industrial IoT Devices, Drones), by Application (Video Surveillance, Autonomous Vehicles, Remote Monitoring, Predictive Maintenance, Access Management, Energy Management, Telemetry), by Vertical (Healthcare, Manufacturing, Automotive, Retail, Energy and Utilities, Telecommunications, Government and Public Sector, Consumer Electronics, Aerospace and Defense, BFSI)

| Status : Published | Published On : May, 2026 | Report Code : VRICT5233 | Industry : ICT & Media | Available Format :

|

Page : 145 |

Edge AI Market Overview

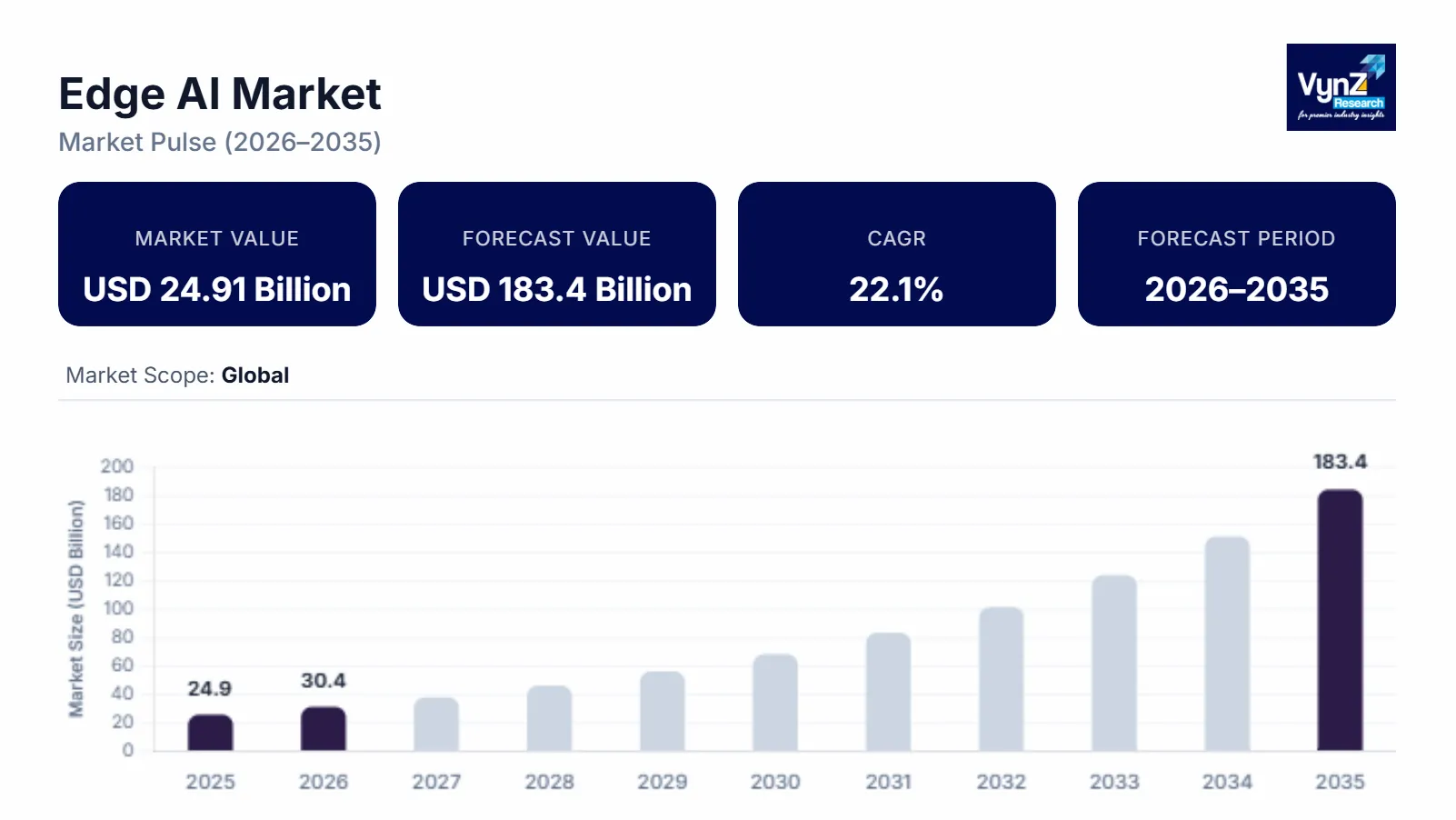

The global edge AI market which was valued at approximately USD 24.91 billion in 2025 and is estimated to rise further up to almost USD 30.41 billion by 2026, is projected to reach around USD 183.4 billion in 2035, expanding at a CAGR of about 22.1% during the forecast period from 2026 to 2035.

The market grows due to widespread deployment of artificial intelligence on edge devices to meet the rising demand for low latency data processing. Industrial automation tech is getting more adopted while AI enabled IoT systems and real time analytics solutions are getting more integrated. The increasing need for autonomous systems, smart surveillance, predictive maintenance and connected devices is pushing the industry expansion worldwide.

Investments into semiconductor innovation, smart manufacturing infrastructure and digital transformation drivers support market momentum in key areas like North America, Europe and Asia Pacific. Government backed AI development programs, cybersecurity frameworks and industrial modernization are also helping organizations sharpen edge computing and roll out scalable artificial intelligence infrastructure across commercial settings and public sector environments.

Edge AI Market Dynamics

Market Trends

Real-time data handling, intelligent edge computing and AI enabled device tuning are changing rapidly due to the rising use of low latency AI inference setups to increase operational efficiency and reduce reliance on the cloud. More AI powered IoT gadgets are being rolled out in manufacturing, automotive, and healthcare. There is also an emerging movement where edge AI is getting blended with 5G connectivity and industrial automation platforms because digitalization keeps accelerating and semiconductors keep improving.

Growth Drivers

The market is growing due to the steady spread of connected devices and industrial IoT infrastructure creating higher demand in manufacturing, automotive, healthcare and smart city use cases. Higher investments in smart factories, autonomous operations, and digital infrastructure upgrades are giving the market extra lift across regions. Enterprises are emphasizing data privacy, low latency processing, operational efficiency. When companies focus on real time analytics, predictive maintenance and automation functions, the need for edge AI hardware and software increases. There are also government backed AI innovation programs and semiconductor spending that help keep momentum for the longer run.

Market Restraints / Challenges

High deployment costs, semiconductor supply chain dependence and the growing complexity of AI integration lower margins and make adoption harder, especially for small and medium sized enterprises. Cybersecurity and data governance worries are adding extra operational pressure. Relying on advanced semiconductor manufacturing knowhow and need for trained AI talent creates friction for technology vendors and system integrators. Meanwhile infrastructure spending keeps rising, hardware boundaries show up, and interoperability issues appear delaying deployments and restricting scalability.

Market Opportunities

There are opportunities in autonomous systems, industrial automation and AI powered smart device ecosystems due to the rising demand for real time analytics and smarter processing. Providers that deliver energy saving processors, scalable edge computing platforms and tailored AI acceleration mechanisms will get more business from manufacturing, healthcare, and transportation teams. Another strong opening is in AI enabled smart city infrastructure and connected mobility solutions. As investments in digital transformation and intelligent monitoring continue to rise, long term commercial potential is getting clearer. Better 5G connectivity, embedded AI processors, and automated analytics platforms should also drive improved operational efficiency and stronger customer engagement across enterprise settings.

Global Edge AI Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 24.91 Billion |

|

Revenue Forecast in 2035 |

USD 183.4 Billion |

|

Growth Rate |

22.1% |

|

Segments Covered in the Report |

Component, Device, Application, Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

ADLINK Technology Inc., Alphabet Inc., Amazon.com Inc., Gorilla Technology Group, Intel Corporation, International Business Machines Corporation, Microsoft Corporation, Nutanix Inc., Synaptics Incorporated, Viso.ai |

|

Customization |

Available upon request |

Edge AI Market Segmentation

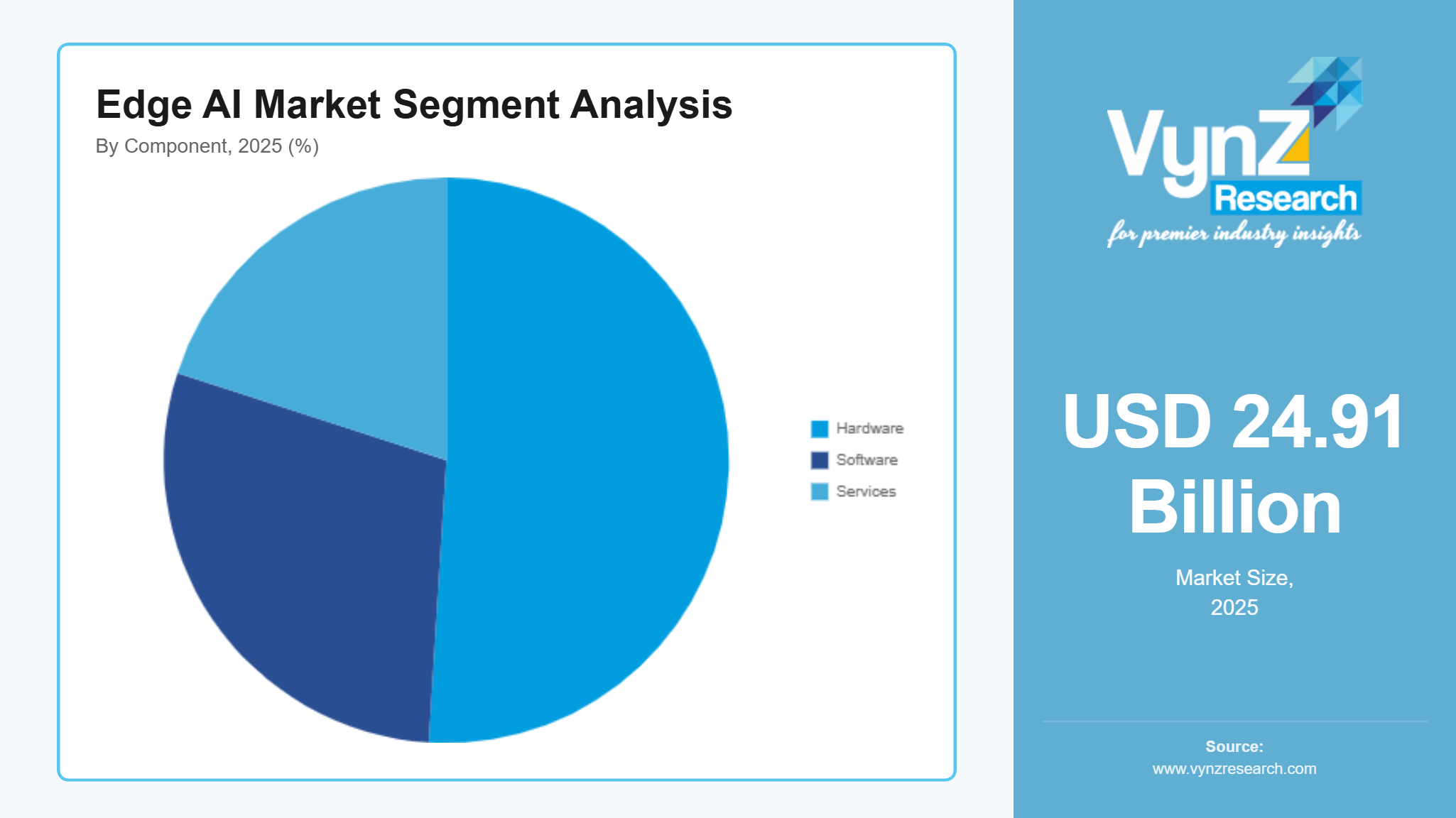

By Component

Hardware took up about 51% of total revenue in 2025 because more and more AI processors are being rolled out, along with edge servers, smart sensors, and embedded computing chips, especially across industrial automation, autonomous systems, and connected device ecosystems. At the same time, more money is flowing into semiconductor manufacturing, AI acceleration technologies, and low power computing infrastructure, pushing hardware demand. Government backed efforts for semiconductor development and industrial modernization across North America and Asia Pacific are also helping the segment maintain a long-term growth curve.

Software is forecast to grow the quickest over the forecast window, with an estimated CAGR of 29.1% from 2026 to 2035 due to rising enterprise interest in AI inference platforms, edge analytics tools and intelligent device management solutions. Cloud edge orchestration systems are getting more tightly integrated and real time machine learning apps are spreading across manufacturing, healthcare, and automotive, which increases software adoption.

By Device

Smart cameras were the biggest contributor in 2025, with nearly 27% of total segment revenue due to ongoing rollouts for intelligent surveillance, industrial monitoring, traffic management and public safety uses. Computer vision technologies are being adopted more widely and AI enabled image processing systems are showing up in both commercial and government settings which increases demand. Public spending on smart city infrastructure and digital security modernization programs is another factor, making it easier to scale edge AI camera systems.

Autonomous vehicles are expected to grow the fastest, with an estimated CAGR of 24.8% from 2026 to 2035. This expansion is mainly powered by increased investments in connected mobility, advanced driver assistance system, and real time navigation technologies. As AI enabled transportation infrastructure and vehicle automation platforms keep getting adopted across developed economies, the segment expands more quickly.

By Application

Video surveillance held the largest portion of the market in 2025, about 31% of segment revenue. Demand is rising because companies and public sector organizations want more intelligent monitoring systems, facial recognition technologies and automated threat detection capabilities. Cybersecurity worries and smart infrastructure spending are also pushing more AI powered edge surveillance platforms into the field globally. Government supported public safety efforts and urban security modernization programs continue to deepen market penetration across major economies.

Predictive maintenance is projected to register the fastest growth during the forecast period, with an estimated CAGR of 23.6% from 2026 to 2035, driven by broader industrial automation adoption, stronger emphasis on operational efficiency and more deployment of real time asset monitoring systems. Manufacturing firms are increasingly putting money into AI enabled predictive analytics, mainly to cut downtime, boost equipment performance, and lower maintenance costs.

By Vertical

Manufacturing accounted for the largest share of the edge AI market in 2025, contributing roughly 26% of total revenue due to strong adoption of industrial automation systems, smart factory technologies and AI driven quality monitoring solutions. More investment in digital manufacturing infrastructure, robotics integration and connected industrial environments is accelerating edge AI deployment across production sites worldwide. Government supported industrial digitization programs and smart manufacturing initiatives are also reinforcing adoption across both developed and emerging economies.

Healthcare and automotive are expected to show the fastest growth during the forecast period, with estimated CAGR levels of around 24.2% and 23.9% respectively from 2026 to 2035 driven by AI enabled diagnostics, remote patient monitoring systems, autonomous driving technologies and connected mobility platforms. Continued investment in intelligent healthcare infrastructure and advanced transportation technologies is helping long term segment expansion.

Regional Insights

North America

North America accounted for approximately 36% of the market in 2025, driven by advanced semiconductor infrastructure, strong enterprise AI adoption and increasing investments in industrial automation technologies. High demand from major technology hubs including California, Texas and Toronto continues to support market expansion across smart manufacturing, autonomous systems, and cloud edge computing applications. Government backed investments in artificial intelligence development, cybersecurity modernization and semiconductor manufacturing initiatives are further accelerating deployment of intelligent edge computing solutions across commercial and public sector environments.

Europe

Europe represented approximately 24% of the market in 2025. The regional landscape is witnessing steady growth due to increasing industrial automation, smart factory modernization, and stronger regulatory support for secure AI deployment. Countries including Germany, France and the UK are experiencing rising adoption of edge AI solutions across automotive, manufacturing, and healthcare sectors. Investments in digital infrastructure, energy efficient computing systems and connected mobility technologies continue to support long term market expansion across the region.

Asia Pacific

Asia Pacific accounted for nearly 19% of the market in 2025, supported by rapid digitalization, expanding semiconductor manufacturing capacity and increasing investments in connected device ecosystems across China, India, Japan and South Korea. Technology hubs such as Beijing, Shenzhen, Tokyo and Bengaluru continue to witness strong deployment of AI enabled industrial automation, smart surveillance and intelligent consumer electronics solutions. Government supported smart city initiatives and industrial digitization programs are also strengthening regional growth opportunities.

Rest of the World

The Rest of the World, including Latin America, the Middle East, and Africa, represented approximately 14% of the market in 2025. Growth across these regions is supported by increasing internet penetration, rising investments in digital infrastructure, and gradual adoption of AI enabled monitoring and automation technologies. The remaining market share not specifically covered by North America, Europe, and Asia Pacific is included within this segment, representing emerging economies with long term growth potential.

Competitive Landscape / Company Insights

The market is highly competitive, with the presence of global semiconductor manufacturers, cloud computing providers, and artificial intelligence platform developers focusing on innovation, strategic partnerships and geographic expansion. Companies are increasingly investing in AI accelerator technologies, edge computing infrastructure and advanced semiconductor research to strengthen their market position. Government supported digital transformation programs, industrial automation initiatives, and semiconductor manufacturing investments are further encouraging enterprises to expand intelligent edge processing capabilities and develop scalable AI driven solutions across commercial and industrial environments.

Mini Profiles

ADLINK Technology Inc. focuses on edge computing platforms and AI enabled industrial hardware solutions, supported by strong embedded systems expertise, industrial automation capabilities, and expanding partnerships across smart manufacturing environments.

Alphabet Inc. operates in premium artificial intelligence and cloud computing segments, emphasizing scalable AI infrastructure, advanced machine learning technologies, and integrated digital ecosystems supporting enterprise and consumer applications globally.

Amazon.com Inc. focuses on cloud-based edge AI infrastructure and intelligent computing services, supported by extensive global distribution networks, scalable data center operations, and strong enterprise technology integration capabilities.

Gorilla Technology Group leverages AI powered video analytics, smart surveillance technologies, and cybersecurity solutions to expand market presence across transportation, public safety, and intelligent infrastructure management applications globally.

Intel Corporation focuses on advanced semiconductor technologies and AI acceleration platforms, supported by strong research capabilities, enterprise computing leadership, and increasing investments in intelligent edge processing and automation solutions.

Key Players

- ADLINK Technology Inc.

- Alphabet Inc.

- Amazon.com, Inc.

- Gorilla Technology Group

- Intel Corporation

- International Business Machines Corporation

- Microsoft Corporation

- Nutanix, Inc.

- Synaptics Incorporated

- Viso.ai

Recent Developments

In January 2025, International Business Machines Corporation expanded enterprise edge AI capabilities through advanced hybrid cloud and AI integration solutions designed for industrial automation and real time analytics applications. The initiative strengthened the company’s position in intelligent edge computing and enterprise AI deployment environments.

In March 2025, Microsoft Corporation introduced enhanced edge AI and cloud orchestration capabilities supporting low latency analytics, industrial IoT processing, and intelligent automation workloads. The expansion focused on improving scalable AI deployment across manufacturing, healthcare, and enterprise infrastructure systems.

In June 2025, Nutanix Inc. strengthened its AI infrastructure portfolio with new enterprise AI platform capabilities supporting distributed edge computing and intelligent workload management. The company focused on improving scalable inference processing and secure AI deployment across hybrid cloud environments.

In October 2025, Synaptics Incorporated launched Astra SL2600 multimodal edge AI processors designed for intelligent IoT and connected device applications. The new processors supported advanced on device inference, robotics, industrial automation, and AI powered smart system deployment across edge environments.

In March 2026, Viso.ai expanded its computer vision and edge AI platform capabilities to support real time video analytics, industrial monitoring, and intelligent automation applications. The development focused on improving scalable AI deployment and centralized management across enterprise edge computing environments.

Global Edge AI Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Device Insight and Forecast 2026 - 2035

- Smartphones

- Smart Cameras

- Robots

- Autonomous Vehicles

- Wearables

- Smart Speakers

- Industrial IoT Devices

- Drones

Application Insight and Forecast 2026 - 2035

- Video Surveillance

- Autonomous Vehicles

- Remote Monitoring

- Predictive Maintenance

- Access Management

- Energy Management

- Telemetry

Vertical Insight and Forecast 2026 - 2035

- Healthcare

- Manufacturing

- Automotive

- Retail

- Energy and Utilities

- Telecommunications

- Government and Public Sector

- Consumer Electronics

- Aerospace and Defense

- BFSI

Global Edge AI Market by Region

- North America

- By Component

- By Device

- By Application

- By Vertical

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Device

- By Application

- By Vertical

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Device

- By Application

- By Vertical

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Device

- By Application

- By Vertical

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Edge AI Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Device

1.2.3. By

Application

1.2.4. By

Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Device

5.2.1. Smartphones

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Smart Cameras

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Robots

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Autonomous Vehicles

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Wearables

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Smart Speakers

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.2.7. Industrial IoT Devices

5.2.7.1. Market Definition

5.2.7.2. Market Estimation and Forecast to 2035

5.2.8. Drones

5.2.8.1. Market Definition

5.2.8.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Video Surveillance

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Autonomous Vehicles

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Remote Monitoring

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Predictive Maintenance

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Access Management

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Energy Management

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. Telemetry

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

5.4. By Vertical

5.4.1. Healthcare

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Manufacturing

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Automotive

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Retail

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Energy and Utilities

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Telecommunications

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Government and Public Sector

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

5.4.8. Consumer Electronics

5.4.8.1. Market Definition

5.4.8.2. Market Estimation and Forecast to 2035

5.4.9. Aerospace and Defense

5.4.9.1. Market Definition

5.4.9.2. Market Estimation and Forecast to 2035

5.4.10. BFSI

5.4.10.1. Market Definition

5.4.10.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Device

6.3. By

Application

6.4. By

Vertical

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Device

7.3. By

Application

7.4. By

Vertical

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Device

8.3. By

Application

8.4. By

Vertical

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Device

9.3. By

Application

9.4. By

Vertical

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

ADLINK Technology Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Alphabet Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Amazon.com, Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Gorilla Technology Group

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Intel Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

International Business Machines Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Nutanix, Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Synaptics Incorporated

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Viso.ai

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Edge AI Market