Carbon Management Software Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Solution Type (Software platforms, Services, Analytics tools, Integration solutions), by Deployment Mode (Cloud based, On premise), by Enterprise Size (Small and medium enterprises, Large enterprises), by End Use (Manufacturing, Energy and utilities, IT and telecom, BFSI, Transportation)

| Status : Published | Published On : May, 2026 | Report Code : VRICT5234 | Industry : ICT & Media | Available Format :

|

Page : 156 |

Carbon Management Software Market Overview

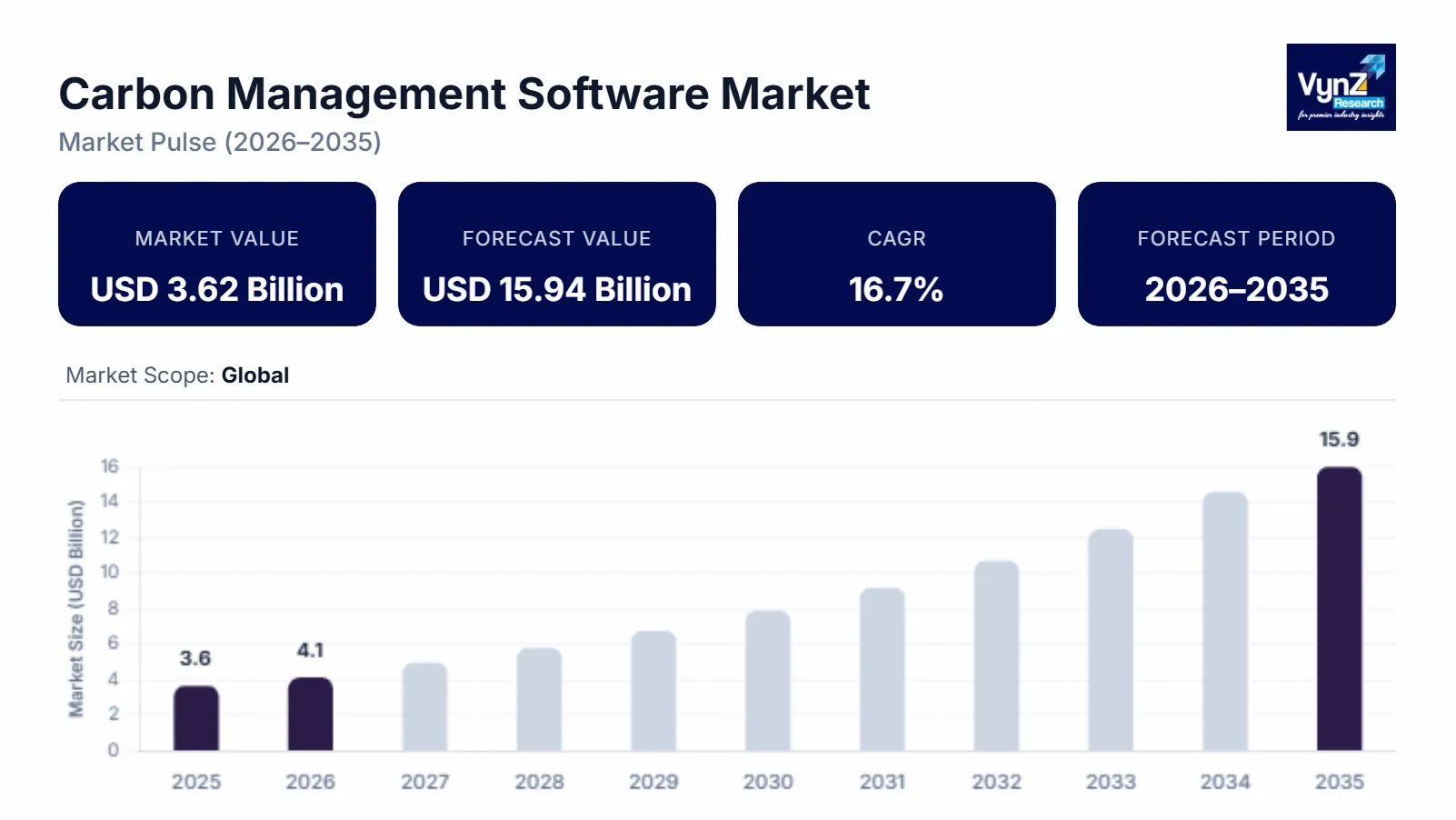

The Carbon Management Software market which was valued at approximately USD 3.62 billion in 2025 and is estimated to rise further up to almost USD 4.08 billion by 2026, is projected to reach around USD 15.94 billion by 2035, expanding at a CAGR of about 16.7% during the forecast period from 2026 - 2035.

Market growth is driven by mounting regulatory pressure for carbon disclosure, ESG compliance and wider corporate decarbonization efforts. There is a higher adoption of real time emissions monitoring and analytics platforms alongside a steady shift toward AI enabled carbon accounting and cloud-based sustainability tools due to the rising need for credible measurements across Scope 1, Scope 2, and Scope 3 emissions monitoring and continual investments linked with national level climate action policies, net zero commitments and sustainability reporting frameworks. This is helping broader expansion in key regions like North America, Europe, and Asia Pacific. This momentum is further enabled by government backed requirements for climate disclosure and by international environmental agreements.

Carbon Management Software Market Dynamics

Market Trends

In the industry there are some notable shifts in tech usage and enterprise sustainability procurement patterns. One key trend pushing the market forward is the rapid integration of AI driven emissions tracking platforms which is promoting real time monitoring, efficiency improvement, and sustainability driven compliance reporting. Another emerging trend is the increasing adoption of cloud-based carbon accounting and ESG reporting system supported by regulatory alignment and digital transformation efforts inside enterprise sustainability frameworks. These developments are pushing product offerings toward integrated sustainability dashboards, automated emissions reporting, and data driven decarbonization solutions.

Growth Drivers

The growth of the market is largely supported by rising global regulatory pressure for carbon transparency and emissions reporting which is generating consistent demand across corporate sustainability and industrial compliance use cases. More investments in enterprise digital transformation and environmental monitoring infrastructure are helping expand the market at a steady pace. Corporate commitment to net zero targets and ESG driven investment strategies is another major factor boosting adoption. As enterprises prioritize regulatory compliance, cost efficiency in emissions reduction and sustainability performance optimization, the demand for carbon accounting and management platforms is expected to stay firm during the forecast period. Government backed climate action policies and international environmental reporting standards are also reinforcing enterprise level adoption.

Market Restraints / Challenges

Even with favorable growth prospects, the market still has restraints that can slow things down. High implementation costs and complex emissions data standardization requirements continue to affect adoption among small and medium enterprises, especially where internal IT bandwidth is limited. Data accuracy and integration challenges turn into operational headaches for software providers. Dependence on external enterprise data systems, combined with inconsistent sustainability reporting infrastructure, cause compliance gaps, integration delays, and scalability limitations.

Market Opportunities

There are opportunities in AI enabled sustainability analytics platforms since companies are leaning harder into automated carbon tracking and predictive emissions modeling. Vendors that provide scalable and user-friendly carbon accounting solutions are positioned to capture incremental demand from enterprises across manufacturing, energy, and IT sectors. Another strong opportunity is digital ESG ecosystem integration, where rising investments in regulatory reporting automation and sustainability intelligence platforms are creating openings for higher value enterprise solutions. Improvements in IoT based emissions monitoring, blockchain enabled traceability and cloud native sustainability tools are also expected to increase reporting accuracy and improve enterprise adoption rates.

Global Carbon Management Software Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.62 Billion |

|

Revenue Forecast in 2035 |

USD 15.94 Billion |

|

Growth Rate |

16.7% |

|

Segments Covered in the Report |

Solution Type, Deployment Mode, Enterprise Size, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Amazon Web Services Inc., Arm Limited, Fujitsu, HCL Technologies Limited, IBM Corporation, Intel Corporation, Microsoft, NVIDIA Corporation, Oracle, Qualcomm Technologies Inc. |

|

Customization |

Available upon request |

Carbon Management Software Market Segmentation

By Solution Type

The software platforms segment held the biggest market share in 2025, roughly 46% of total revenue, helped by broad enterprise take up for emissions tracking, ESG reporting, and regulatory compliance management across industrial and corporate areas. That centralized carbon accounting setup keeps making this segment dominant for organizations rolling out sustainability frameworks worldwide.

Services are expected to show the quickest growth, around 17.8% over the forecast window, mostly pushed by rising appetite for consulting, implementation, and managed sustainability offerings. With carbon disclosure rules getting more complicated and with enterprises needing customized, end to end integration, the service side adoption is also getting a boost in both developed and emerging markets.

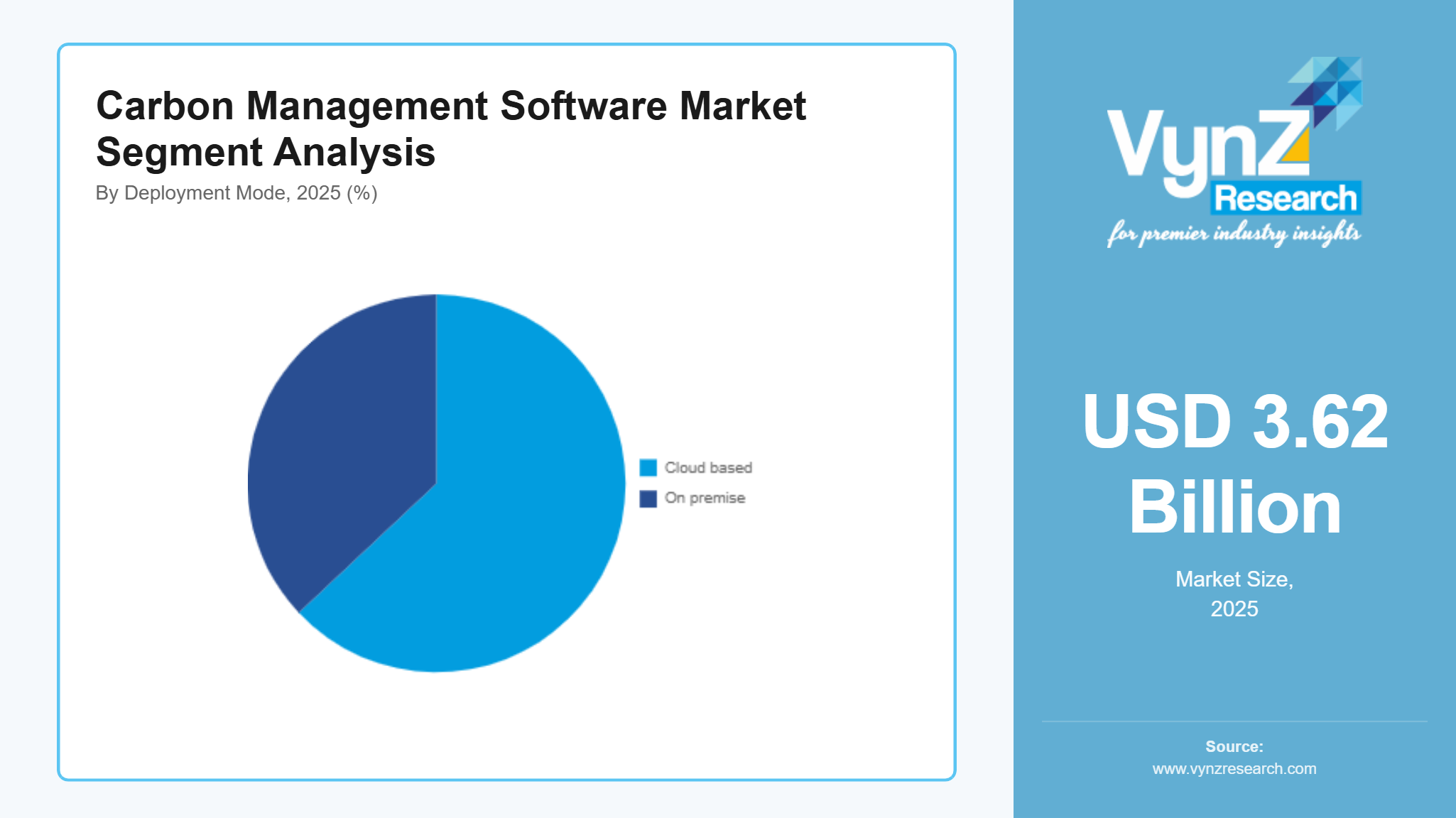

By Deployment Mode

Cloud based solutions took the majority in 2025, about 63% of the market, because firms keep inclined toward scalability, faster real time data access, and cheaper, streamlined ESG reporting routines. The spread of SaaS sustainability platforms among multinational corporations is still reinforcing the cloud lead.

On-premise deployment is moving ahead more slowly, at about 13.9%, driven by strict data security needs and regulatory compliance obligations inside tightly regulated industries. The combo of hybrid deployment models, mixing cloud flexibility with on premise control, is quietly helping adoption rise for sensitive sectors like banking and government institutions.

By Enterprise Size

Large enterprises generated the highest revenue share in 2025, roughly 58%, because they face major ESG reporting commitments, have complex global supply chain emissions tracking and must meet heavy regulatory compliance demands. These organizations keep investing in advanced carbon management platforms to match sustainability targets and reporting mandates.

Small and medium enterprises are forecast to grow fastest, around 19.3% during the forecast period, enabled by more regulatory understanding, affordability tied to cloud-based solutions and simplified ESG reporting toolsets. As cost conscious subscription-based platforms become easier to adopt, SMEs can fold sustainability monitoring into everyday business operations, without building big infrastructure.

By End Use

Manufacturing led the market in 2025, accounting for about 31% of total revenue, mainly because it has high emissions intensity, tight regulatory supervision and ongoing decarbonization initiatives across industrial activities. The extra push to meet global emissions standards is also keeping adoption steady in this slice.

Energy and utilities are expected to register the fastest growth rate near 18.6%, backed by the larger scale shift toward renewable energy systems, grid modernization and carbon neutrality targets. More spending on emissions monitoring infrastructure and regulatory supported decarbonization programs is further increasing software adoption across this area.

Regional Insights

North America

North America accounted for approximately 37% of the market in 2025, driven by strict regulatory compliance frameworks, early ESG adoption and strong enterprise digital transformation across the United States and Canada. Major industrial and corporate hubs such as New York, California, Texas and Ontario continue to support large scale deployment of carbon accounting platforms. Government backed climate disclosure regulations, including mandatory emissions reporting frameworks and net zero commitments, are encouraging enterprises to invest in advanced sustainability software solutions. Increasing corporate demand for transparent carbon reporting and integration of AI based ESG analytics tools is further strengthening regional market performance across finance, energy, and manufacturing sectors.

Europe

The Europe market is witnessing steady growth due to strong regulatory enforcement under climate neutrality policies, aggressive decarbonization targets and industrial sustainability transformation across Germany, France, the United Kingdom and Nordic countries. The region accounted for approximately 31% of the market in 2025, supported by widespread adoption of ESG reporting standards and carbon pricing mechanisms. Increasing implementation of government backed sustainability reporting directives and corporate climate disclosure mandates is driving consistent demand. Strong adoption across automotive manufacturing, energy transition projects, and financial services is further supporting regional expansion, with enterprises prioritizing real time emissions monitoring and compliance automation.

Asia Pacific

Growth in Asia Pacific is supported by rapid industrialization, expanding digital infrastructure and increasing government focus on carbon neutrality targets across China, India, Japan and South Korea. The region accounted for approximately 22% of the market in 2025, driven by rising ESG awareness and growing adoption of sustainability reporting frameworks in large enterprises. Government led climate action policies, national carbon reduction programs and increasing investments in green energy transition projects are further accelerating adoption. Expanding industrial output and growing pressure on manufacturing and energy sectors to comply with emissions monitoring standards are strengthening long term market opportunities across the region.

Rest of the World

Latin America, the Middle East, and Africa collectively accounted for approximately 10% of the market in 2025, driven by gradual ESG adoption, emerging regulatory frameworks, and increasing investments in digital sustainability infrastructure. Growth in countries such as Brazil, Mexico, South Africa and Gulf Cooperation Council economies is supported by rising corporate sustainability awareness and government led climate initiatives. Expansion of smart city programs, energy diversification strategies and digital transformation in industrial sectors is further supporting market penetration.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with the presence of global and regional players focusing on platform innovation, regulatory compliant ESG solutions and geographic expansion across enterprise sustainability ecosystems. Companies are increasingly investing in advanced analytics capabilities, AI driven carbon accounting tools and cloud based digital sustainability infrastructure to strengthen their market position. Government backed climate disclosure mandates, net zero regulatory frameworks and international sustainability reporting standards are further shaping competitive dynamics and accelerating adoption of enterprise grade emissions management solutions across industries.

Mini Profiles

Amazon Web Services Inc. focuses on cloud computing infrastructure and enterprise grade sustainability and carbon management integrated services, supported by strong global distribution strength and hyperscale data center network enabling scalable digital solutions.

Arm Limited operates in premium semiconductor architecture segments, emphasizing energy efficient chip design and high-performance computing frameworks that support cloud infrastructure, AI workloads, and next generation enterprise digital transformation ecosystems globally.

Fujitsu leverages strategic partnerships and enterprise IT solutions to expand market presence, focusing on integrated cloud services, digital transformation platforms, and sustainability driven enterprise systems across industrial and government sectors.

HCL Technologies Limited focuses on IT services and digital engineering solutions, supported by strong cost efficiency and global delivery model enabling scalable enterprise transformation, cloud adoption, and advanced analytics integration across multiple industries.

IBM Corporation operates in premium enterprise technology segments, emphasizing hybrid cloud architecture, AI driven analytics platforms, and carbon intelligent computing solutions designed for large scale enterprise modernization and sustainability transformation initiatives.

Key Players

- Amazon Web Services, Inc.

- Arm Limited

- Fujitsu

- HCL Technologies Limited

- IBM Corporation

- Intel Corporation

- Microsoft

- NVIDIA Corporation

- Oracle

- Qualcomm Technologies, Inc.

Recent Developments

In August 2025, Intel Corporation expanded its data center focused AI and sustainability computing roadmap by enhancing energy efficient processor architectures. The initiative supports enterprise level workload optimization and improved efficiency in large scale cloud and analytics environments.

In January 2026, Microsoft upgraded its cloud sustainability and emissions tracking capabilities within Azure integrated ESG reporting systems. The development strengthens enterprise carbon accounting accuracy and supports regulatory aligned climate disclosure requirements across global organizations.

In December 2025, NVIDIA Corporation introduced next generation AI optimized GPU platforms designed to improve data center energy efficiency and computational performance. The advancement supports sustainable high-performance computing and reduces power intensity in large scale AI workloads.

In November 2025, Oracle enhanced its enterprise cloud sustainability tools by integrating advanced emissions tracking and carbon reporting features within its cloud infrastructure. The update improves regulatory compliance and supports enterprise level decarbonization reporting requirements.

In September 2025, Qualcomm Technologies Inc. strengthened its AI and edge computing semiconductor portfolio with improved energy efficient processing solutions. The development supports low power high performance applications across mobile, automotive, and connected device ecosystems with sustainability focused design improvements.

Global Carbon Management Software Market Coverage

Solution Type Insight and Forecast 2026 - 2035

- Software platforms

- Services

- Analytics tools

- Integration solutions

Deployment Mode Insight and Forecast 2026 - 2035

- Cloud based

- On premise

Enterprise Size Insight and Forecast 2026 - 2035

- Small and medium enterprises

- Large enterprises

End Use Insight and Forecast 2026 - 2035

- Manufacturing

- Energy and utilities

- IT and telecom

- BFSI

- Transportation

Global Carbon Management Software Market by Region

- North America

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Carbon Management Software Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Solution Type

1.2.2. By

Deployment Mode

1.2.3. By

Enterprise Size

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Solution Type

5.1.1. Software platforms

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Analytics tools

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Integration solutions

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Deployment Mode

5.2.1. Cloud based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. On premise

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Enterprise Size

5.3.1. Small and medium enterprises

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Large enterprises

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Manufacturing

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Energy and utilities

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. IT and telecom

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. BFSI

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Transportation

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Solution Type

6.2. By

Deployment Mode

6.3. By

Enterprise Size

6.4. By

End Use

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Solution Type

7.2. By

Deployment Mode

7.3. By

Enterprise Size

7.4. By

End Use

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Solution Type

8.2. By

Deployment Mode

8.3. By

Enterprise Size

8.4. By

End Use

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Solution Type

9.2. By

Deployment Mode

9.3. By

Enterprise Size

9.4. By

End Use

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Amazon Web Services, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Arm Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Fujitsu

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

HCL Technologies Limited

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

IBM Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Intel Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

NVIDIA Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Oracle

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Qualcomm Technologies, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Carbon Management Software Market