Customer-facing Technology Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Technology (Artificial intelligence, Augmented reality and virtual reality, Internet of things, Big data analytics, Cloud computing), by Deployment Mode (On premise, Cloud based), by Application (Customer experience management, Customer relationship management, Workforce engagement, Marketing automation, Sales and support systems), by End Use (Retail and e commerce, Banking financial services and insurance, Healthcare, Telecommunications, Travel and hospitality, Others), by Region (North America, Europe, Asia Pacific, Rest of the World)

| Status : Published | Published On : May, 2026 | Report Code : VRICT5232 | Industry : ICT & Media | Available Format :

|

Page : 156 |

Customer-facing Technology Market Overview

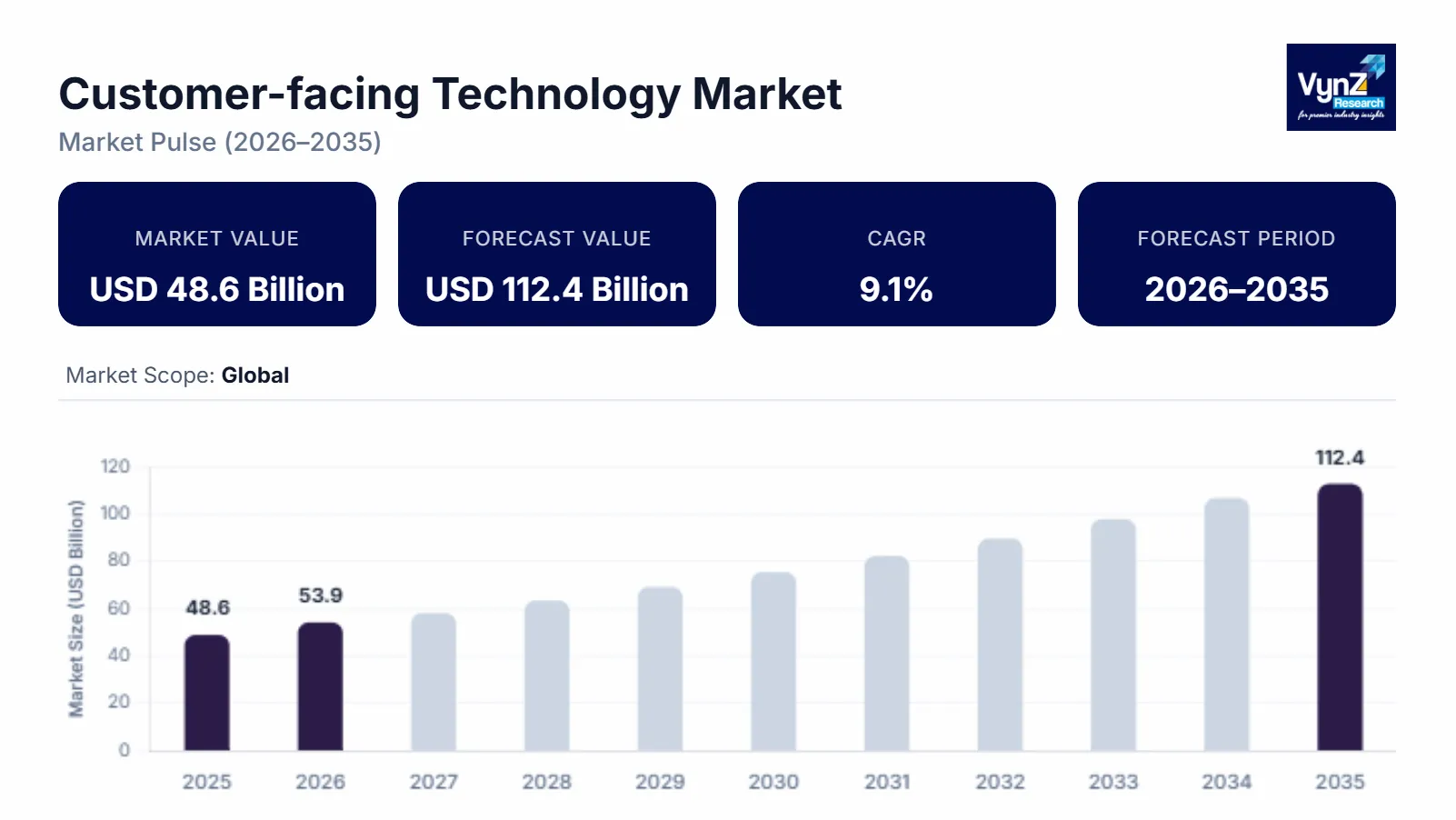

The customer facing technology market which was valued at approximately USD 48.6 billion in 2025 and is estimated to rise further up to almost USD 53.9 billion by 2026, is projected to reach around USD 112.4 billion in 2035, expanding at a CAGR of about 9.1% during the forecast period from 2026 to 2035.

The market expands because retail and service industries undergo digital transformation, businesses use AI with data analytics to enhance customer engagement, and customers demand personalized experiences which work across multiple channels. The growing popularity of contactless payments together with the need for instant service, drives organizations to implement new technologies across their crucial operations. The market expands in North America, Europe, and Asia Pacific because businesses need better customer experience management and they keep investing in digital infrastructure which receives financial support from public and institutional initiatives.

The World Health Organization and global development institutions provide reports that show how digital system strengthening and technology-based service delivery development assist customer interaction systems through their implementation of digital systems. Government programs that support digital payment systems and smart retail frameworks together with AI-powered service platforms establish stronger market presence, while enterprises expand their automation and analytics budget which leads to continuous industry growth.

Customer-facing Technology Market Dynamics

Market Trends

The technology industry which serves customers through its digital platforms shows major changes in how people use technology and interact with businesses by adopting more digital channels and automated customer service systems. The market receives its primary directional force from companies that develop customer engagement platforms through their application of artificial intelligence and machine learning technologies. The current transition period matches worldwide digital adoption patterns which international development organizations identified as essential since intelligent systems help multiple fields achieve better service delivery through their improved accessibility and quick response times. The development of contactless and self-service technologies shows an upward trend because of two factors which include expanding digital network usage and new consumer needs for speedy and convenient service options.

Growth Drivers

The market expands because all three major business sectors banking, retail and service industries undergo fast digital evolution which creates continuous demand for both enterprise software and customer service technologies. The digital economy grows as organizations increase their digital infrastructure investments while smart service ecosystem development takes place through governmental digital economy development policies and technology service delivery systems. Global organizations report that digital infrastructure and digital inclusion in both developed and developing countries show continuous improvement which leads to increased technology adoption. The customer experience optimization trend drives technology adoption because organizations use more resources to enhance customer experience.

Market Restraints / Challenges

The market shows positive growth trends yet the industry must navigate several critical hurdles which will prevent its business expansion. The high costs required to implement and establish advanced analytics systems and AI-based systems create financial challenges which disrupt business operations in particular for small and medium-sized businesses. Organizations face operational difficulties because they need to comply with data privacy and cybersecurity regulations which create additional costs and restrict their ability to deploy systems in flexible ways. The solution providers face operational problems since they need both advanced technological systems and highly trained workers to maintain their business operations. The practice of using both outside technology suppliers and specialized expertise leads to business difficulties because it increases expenses while restricting business growth in areas that have weak digital capabilities.

Market Opportunities

The market provides major growth potential through digital engagement platform development in emerging markets which experience rising internet access and need better online service delivery. The market presence of businesses that deliver affordable and flexible services will expand as they meet the rising needs of small businesses and digital growth businesses. Market expansion through government-backed digital transformation programs and infrastructure investment will boost public internet access. Advanced analytics and automation-based customer interaction systems create new business opportunities because all companies currently invest in intelligent integrated systems which help their businesses achieve greater operational efficiency and sustain customer relationships.

Global Customer-facing Technology Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 48.6 Billion |

|

Revenue Forecast in 2035 |

USD 112.4 Billion |

|

Growth Rate |

9.1% |

|

Segments Covered in the Report |

Component, Technology, Deployment Mode, Application, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Adobe Inc., Amazon Web Services Inc., Cisco Systems Inc., Google LLC, IBM Corporation, Microsoft Corporation, Oracle Corporation, Salesforce Inc., SAP SE, Zendesk Inc. |

|

Customization |

Available upon request |

Customer-Facing Technology Market Segmentation

By Component

The software market achieved the highest market share in 2025 when it generated about 46% of overall revenue. Its widespread acceptance of customer engagement platforms, analytics tools, and AI driven applications across retail, banking, and service industries fuels that major market power. The ongoing business shift towards digital systems and unified customer management solutions creates higher market requirements. The adoption of cloud services and data driven solutions through government digital transformation programs and policy frameworks establishes a solid foundation for software solution growth in both developed and developing regions.

The services sector will experience the highest expansion rate through its projected 9.8% compound annual growth rate during the 2026 to 2035 evaluation period. The demand for system integration, consulting, and managed services drives this growth because organizations require those services to improve their customer interaction technology implementation and operational efficiency. Organizations choose to outsource specific functions because their digital environments have become more complex and require ongoing technological upgrades. The public sector programs which support digital skill development together with enterprise modernization initiatives help to increase growth within the specific market segment.

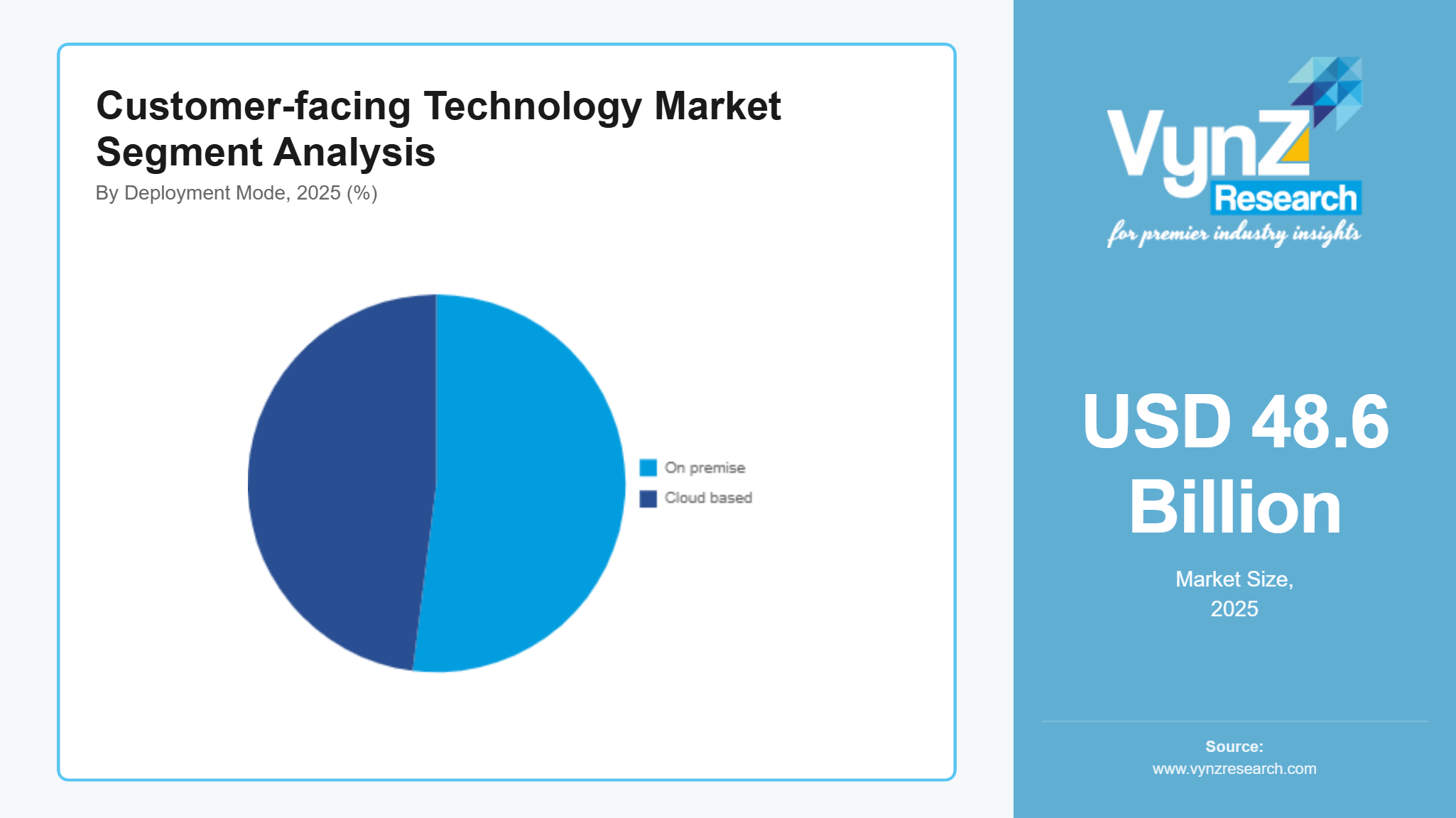

By Deployment Mode

The market share for on-premise deployment reached 52% in 2025 because it held the majority of the market. Organizations prefer on-premise systems because they provide better control over their data and security compliance and they enable customized solutions which banks and healthcare organizations require in their regulated markets. Organizations in critical operational sectors continue to adopt secure on-premise systems because government and institutional authorities have established data protection regulations which safeguard sensitive data.

The cloud-based deployment method experiences rapid expansion which will reach an estimated 10.2% CAGR throughout the upcoming period. The increasing rate of digital transformation together with the scalability and cost efficiency which cloud systems deliver serves as the primary force behind growth. The expansion of government-supported cloud initiatives together with digital infrastructure investments enables companies to implement flexible systems which allow remote access. The operational performance of organizations improves through cloud systems which now include analytics and artificial intelligence functionalities for better customer connections.

By Technology

The artificial intelligence market share in 2025 reached its highest point when it constituted about 34% of total market revenue. Organizations use chatbots and recommendation engines and predictive analytics extensively because those tools improve customer experience together with operational efficiency. National strategies that support artificial intelligence deployment and digital innovation development strengthen their use across different business sectors.

The augmented and virtual reality market will expand the fastest according to its projected 9.6% compound annual growth rate throughout the upcoming period. The retail and service sectors have increased their use of immersive customer engagement technologies together with product visualization technologies which drive market expansion. Public institutions support digital infrastructure development through innovation programs which enable businesses to test and develop their technologies, resulting in more applications and wider market access.

By Application

Customer experience management held the largest share in 2025 when it generated approximately 38% of overall market revenue. The platform which enables user interaction handles customer experience management as the main solution which organizations throughout the world use to increase user satisfaction and retention and brand loyalty through integrated engagement platforms. The public programs which support digital service delivery together with customer-oriented systems drive market adoption across different industries.

Marketing automation will become the leading market segment through its projected 9.4% compound annual growth rate during the evaluation period. The market expands according to customer growth which requires targeted campaigns and real-time analytics and personalized communication strategies. Data-driven marketing and digital outreach program investments which financial institutions support through their digitalization efforts lead to market growth in the sector. The segment growth at small and medium enterprises will rise because budget-friendly solutions now become more available.

By End Use

The retail and e-commerce sector generated the most revenue in 2025 when it accounted for approximately 36% of total market sales. The market leadership position exists because digitalization progresses rapidly and online transactions increase while customers expect smooth interactions with brands across multiple platforms. The government-backed digital payment systems together with e-commerce development projects will increase market penetration of this segment.

The healthcare sector will achieve the fastest expansion through a 9.7% compound annual growth rate during the upcoming evaluation period. The increasing rate of digital patient engagement tool adoption together with telehealth platform use and automated service deployment drives the growth of the digital healthcare market. Global health organizations report that healthcare institutions use customer facing technologies to develop their digital health infrastructure and patient-centered care models.

Regional Insights

North America

North America held approximately 32% of the customer facing technology market in 2025 because its robust digital infrastructure, high enterprise technology investments and early customer engagement technology adoption drive market growth. New York, San Francisco, and Toronto as major urban centers experience ongoing growth in retail and banking and service sector deployments. Government backed institutions report substantial progress in digital economy growth and cloud technology usage which enables businesses to implement customer interaction platforms throughout their operations. The government programs which promote artificial intelligence development and data governance together with digital service delivery systems establish a foundation for businesses to invest in advanced customer facing solutions. The regional market continues to grow because businesses invest in omnichannel retail systems and digital payment ecosystems while they focus on developing personalized customer experiences together with real time customer engagement tools.

Europe

Europe provided approximately 26% of market share in 2025. The region grows because its regulatory systems force businesses to become compliant with digital solutions while its customers demand greater protection of their data and personal information. The financial services sector, retail market and public sector services in Germany, the United Kingdom and France demonstrate constant adoption of customer engagement technologies. The region continues its digital transformation process while it connects its digital assets with other countries through institutional reports. Public initiatives which promote secure digital infrastructure and standardized data protection practices enable organizations to adopt solutions that meet compliance requirements while maintaining scalability. The market grows because enterprises increase their investments in smart retail systems and digital public services while they implement analytics driven platforms to boost their operational efficiency and improve customer satisfaction.

Asia Pacific

The market reached approximately 21% share in 2025 because urbanization, internet access and digital economic growth drive expansion in China, India and Japan. The main digital commerce and technology-based customer engagement centers of the region have developed into major cities that include Beijing, Mumbai and Tokyo. International development organizations report that the region has made substantial progress in building digital infrastructure and expanding mobile connectivity. The digital payment development, smart city creation and technology advancement government initiatives are driving industries to adopt customer facing solutions. The market grows because e commerce platforms and smartphone adoption and enterprise spending on automation and analytics increase in the region.

Rest of the World

The rest of the global market reached approximately 19% share in 2025 including Latin America, the Middle East and Africa. The regions expand because businesses increase their digital activities, build better infrastructure and people learn about technology-based customer engagement solutions. Digital platforms are being adopted by major cities across these regions but their overall usage remains lower than in developed countries. Government programs that improve digital connectivity and promote financial inclusion enable businesses to gradually adopt customer interaction technologies. The market presence of mobile services and digital payment systems has grown because these services and systems have become more widely accepted. Emerging regions with long term growth potential and developing digital ecosystems make up the segment which contains the rest of the market share after North America and Europe and Asia Pacific.

Competitive Landscape / Company Insights

The market demonstrates a moderate level of competition because both global and regional companies attempt to compete through their innovative product development, their pricing methods and their efforts to expand into new markets. Companies are making higher investments in research and development together with digital capabilities to improve their market competitiveness. The competitive strategies of businesses now depend on their emphasis of artificial intelligence together with cloud integration and data analytics. Digital transformation initiatives that receive government support together with policy frameworks for technology adoption create an environment that promotes innovation, while the increasing need of enterprises for secure scaling solutions drives up competition in all major regions of the market.

Mini Profiles

Adobe Inc. focuses on customer experience management and digital marketing solutions, supported by strong brand recognition and integrated cloud platforms enabling personalized engagement and scalable enterprise adoption across global markets.

Amazon Web Services Inc. operates in mass and enterprise segments, emphasizing scalable cloud infrastructure, performance efficiency, and flexible deployment models to support customer facing applications and data driven engagement systems.

Cisco Systems Inc. leverages strong networking expertise and strategic partnerships to expand market presence, offering secure communication platforms and integrated solutions that enhance real time customer interaction and enterprise connectivity.

Google LLC focuses on analytics, artificial intelligence, and cloud-based engagement tools, supported by extensive digital reach and data driven capabilities enabling advanced personalization and customer insight generation.

IBM Corporation operates in enterprise and niche segments, emphasizing advanced analytics, hybrid cloud solutions, and artificial intelligence driven platforms to enhance customer engagement and operational efficiency.

Key Players

- Adobe Inc.

- Amazon Web Services Inc.

- Cisco Systems Inc.

- Google LLC

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Salesforce Inc.

- SAP SE

- Zendesk Inc.

Recent Developments

In May 2025, Salesforce Inc. announced plans to acquire Informatica for approximately USD 8 billion to strengthen its data integration capabilities. The move supports its broader agentic AI strategy and enhances enterprise data management capabilities.

In October 2025, Zendesk Inc. introduced new artificial intelligence driven features to enhance customer service automation and engagement. These developments focused on improving response efficiency and enabling scalable customer interaction platforms.

In April 2025, Oracle Corporation advanced its artificial intelligence capabilities through new automation focused solutions in enterprise applications. The company emphasized autonomous AI integration to improve business process efficiency and customer interaction systems.

In August 2025, Cisco Systems Inc. expanded its digital communication and networking solutions to support real time customer engagement platforms. The company focused on enhancing secure connectivity and integrated service delivery capabilities across enterprise environments.

In October 2025, SAP SE strengthened its customer experience portfolio by integrating advanced analytics and cloud-based engagement tools. These enhancements aim to support data driven decision making and improve personalized customer interaction across industries.

Global Customer-facing Technology Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Technology Insight and Forecast 2026 - 2035

- Artificial intelligence

- Augmented reality and virtual reality

- Internet of things

- Big data analytics

- Cloud computing

Deployment Mode Insight and Forecast 2026 - 2035

- On premise

- Cloud based

Application Insight and Forecast 2026 - 2035

- Customer experience management

- Customer relationship management

- Workforce engagement

- Marketing automation

- Sales and support systems

End Use Insight and Forecast 2026 - 2035

- Retail and e commerce

- Banking financial services and insurance

- Healthcare

- Telecommunications

- Travel and hospitality

- Others

Region Insight and Forecast 2026 - 2035

- North America

- Europe

- Asia Pacific

- Rest of the World

Global Customer-facing Technology Market by Region

- North America

- By Component

- By Technology

- By Deployment Mode

- By Application

- By End Use

- By Region

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Technology

- By Deployment Mode

- By Application

- By End Use

- By Region

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Technology

- By Deployment Mode

- By Application

- By End Use

- By Region

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Technology

- By Deployment Mode

- By Application

- By End Use

- By Region

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Customer-facing Technology Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Technology

1.2.3. By

Deployment Mode

1.2.4. By

Application

1.2.5. By

End Use

1.2.6. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Artificial intelligence

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Augmented reality and virtual reality

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Internet of things

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Big data analytics

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Cloud computing

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Deployment Mode

5.3.1. On premise

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cloud based

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Customer experience management

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Customer relationship management

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Workforce engagement

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Marketing automation

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Sales and support systems

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By End Use

5.5.1. Retail and e commerce

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Banking financial services and insurance

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Healthcare

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Telecommunications

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Travel and hospitality

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Others

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.6. By Region

5.6.1. North America

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Europe

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Asia Pacific

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. Rest of the World

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Technology

6.3. By

Deployment Mode

6.4. By

Application

6.5. By

End Use

6.6. By

Region

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Technology

7.3. By

Deployment Mode

7.4. By

Application

7.5. By

End Use

7.6. By

Region

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Technology

8.3. By

Deployment Mode

8.4. By

Application

8.5. By

End Use

8.6. By

Region

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Technology

9.3. By

Deployment Mode

9.4. By

Application

9.5. By

End Use

9.6. By

Region

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Adobe Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amazon Web Services Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Cisco Systems Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Google LLC

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

IBM Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Microsoft Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Oracle Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Salesforce Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

SAP SE

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Zendesk Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Customer-facing Technology Market