AI Driven Predictive Maintenance Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Offering (Software, Services), by Deployment Mode (Cloud Based, On Premises), by Solution Type (Integrated, Standalone), by Technique (Vibration analysis, Oil analysis, Others), by Organization Size (Large Enterprises, Small And Medium Enterprises), by End Use (Manufacturing, Energy and Utilities, Transportation and Logistics, Healthcare, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRICT5228 | Industry : ICT & Media | Available Format :

|

Page : 171 |

AI Driven Predictive Maintenance Market Overview

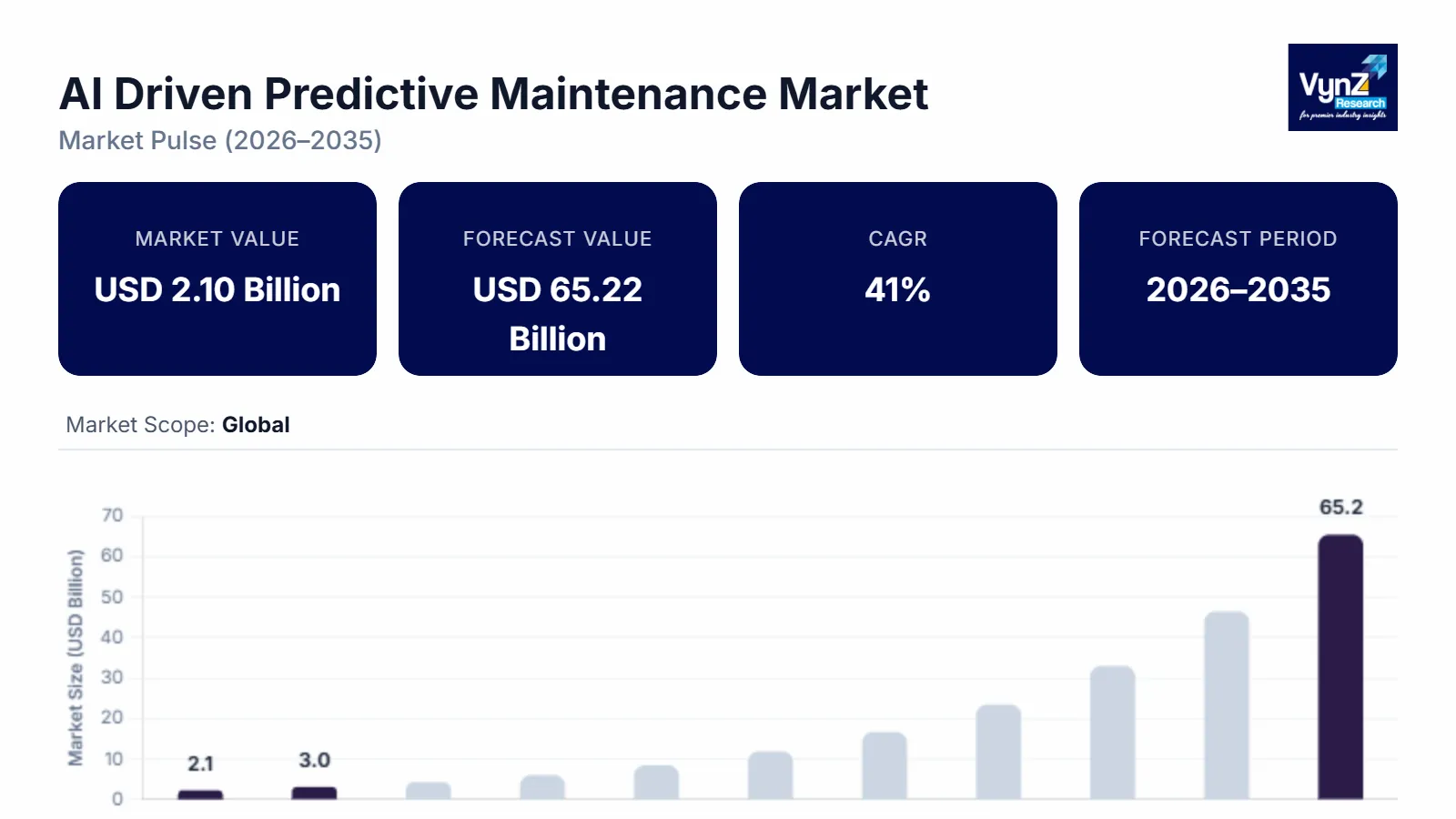

The global AI driven predictive maintenance market which was valued at approximately USD 2.10 billion in 2025 and is estimated to rise further up to almost USD 2.95 billion by 2026, is projected to reach around USD 65.22 billion in 2035, expanding at a CAGR of about 41% during the forecast period from 2026 to 2035.

The predictive maintenance market driven by artificial intelligence technology experiences rapid growth because industrial automation becomes more widespread, businesses adopt artificial intelligence to monitor their assets and companies need to reduce their operational downtime during manufacturing processes. The market experiences growth because all industries undergo digital transformation while businesses adopt cloud-based monitoring systems and require advanced analytics solutions together with their increasing use of integrated predictive maintenance systems.

The market expansion across major regions including the United States, Germany and China results from two factors which include the rising need for real-time equipment diagnostics and the ongoing development of smart manufacturing systems which receive support from World Health Organization initiatives to build resilient healthcare systems and enhance digital system efficiency.

AI Driven Predictive Maintenance Market Dynamics

Market Trends

The industry experiences essential technological transformations together with changes in industrial purchasing behavior because asset intensive sectors now use intelligent monitoring systems. The market experiences its main shift through businesses adopting cloud based predictive maintenance systems which offer real time operational insights at lower expenses while enabling system scalability. International Organization for Standardization frameworks together with industrial digitalization initiatives establish required data sharing protocols plus required procedures for monitoring equipment conditions and managing asset life cycles, which enable manufacturers to implement these systems throughout their production systems.

The rising use of advanced analytics and machine learning based diagnostic systems is becoming a new trend because digital technologies continue to spread and industrial automation systems develop. The market developments create new solution capacities that lead businesses to concentrate on developing complete solutions which bring predictive insights together with additional service models, which change how competition operates within the industry. Intelligent maintenance technology adoption receives a boost from industrial transformation programs which the government supports across multiple areas including the United States, Germany, and China.

Growth Drivers

The market grows because industrial automation systems become more popular while smart manufacturing technologies get implemented throughout various business sectors including energy production, automotive manufacturing and healthcare equipment monitoring. The market experiences rapid growth because businesses invest more money into building digital infrastructure, establishing industrial IoT networks and deploying advanced analytics systems. The World Economic Forum reports together with its frameworks show how predictive maintenance helps businesses achieve better operational results through decreased operational downtime while increasing overall productivity.

The rising focus on cost efficiency together with asset performance optimization will drive greater system adoption throughout various business sectors. Enterprises will continue to demand AI enabled maintenance solutions throughout the forecast period because they value operational reliability and predictive insights. Government supported smart industry initiatives and digital transformation programs in regions including Japan and India are further strengthening adoption through infrastructure development and policy alignment.

Market Restraints / Challenges

The market has positive growth prospects but it faces various obstacles which will restrict its market expansion. The advanced analytics platform costs together with its integration difficulties create barriers for small and medium enterprises which restrict their market access. National Institute of Standards and Technology reports show that organizations face deployment challenges because outdated industrial systems lack proper data exchange methods and standardized data protocols which control their operation.

The solution providers face operational difficulties because they depend on their skilled workforce and their expensive technology systems. Data science experts together with artificial intelligence specialists and industrial system specialists create operational difficulties because they need specialized knowledge. Economic fluctuations together with the various levels of digital readiness will decrease market adoption because of existing uncertainties which will affect the market performance.

Market Opportunities

The market offers substantial growth potential through the development of smart manufacturing ecosystems and digital asset management systems which industrial IoT technology and real time monitoring systems now drive. Companies which develop predictive maintenance platforms that customers can customize to their needs while their systems deliver high performance will gain additional customers from industrial businesses that want to increase their operational productivity. The European Commission supports government initiatives which develop digital transformation roadmaps to help businesses implement intelligent industrial solutions throughout their operations.

The growing digital infrastructure investments between artificial intelligence systems, edge computing platforms and automation technology platforms create business opportunities which lead to operational improvements. The market will continue to grow because machine learning model improvements, remote monitoring tool development and automated diagnostic advancements will increase customer engagement which improves deployment efficiency.

Global AI Driven Predictive Maintenance Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 2.10 Billion |

|

Revenue Forecast in 2035 |

USD 65.22 Billion |

|

Growth Rate |

41% |

|

Segments Covered in the Report |

Offering, Deployment Mode, Solution Type, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Middle East and Africa, Latin America |

|

Key Companies |

C3.ai, General Electric, Honeywell, IBM, KCF Technologies, Microsoft, Oracle, ONYX Insight, PTC, Siemens |

|

Customization |

Available upon request |

AI Driven Predictive Maintenance Market Segmentation

By Offering

The AI driven predictive maintenance market in 2025 reached its highest revenue through software which generated approximately 57% of total earnings because industrial operations needed real time analytics and enterprises required system integration. Digital transformation initiatives with standardization frameworks the International Organization for Standardization supports through structured data exchange and asset lifecycle management, promote further adoption of technology by businesses.

The period between now and the forecasted future will see services achieve their highest growth rate of 42% because system integration and consulting and maintenance support become more necessary. Enterprises are moving toward service driven models because industrial environments become more complex and they need to track their operations constantly.

By Deployment Mode

The market share of cloud-based deployment reached its peak in 2025 when it generated almost 61% of segment revenue because its customers benefited from its scalability and cost efficient and remote accessibility functions. The industrial sector is seeing quick adoption of digital infrastructure and cloud ecosystems because Indian and Chinese economies are developing industrially.

The demand for on premises deployment is increasing steadily at 38% because critical industries need data security and regulatory compliance. The controlled deployment environments which sectors handling advanced operational data choose to use, maintain their continuous demand for these specialized environments.

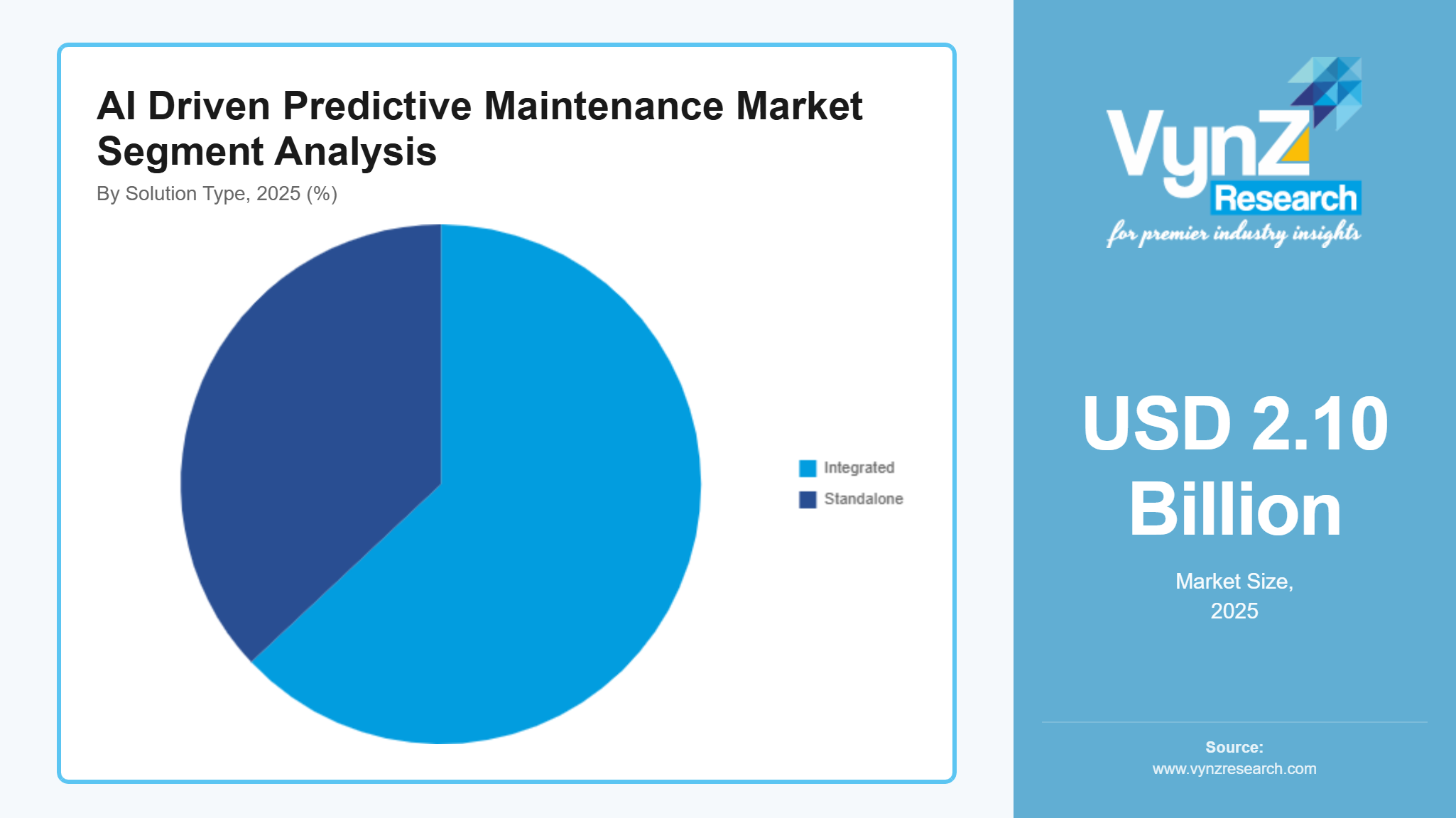

By Solution Type

The integrated solutions market reached its highest value in 2025 when it generated approximately 63% of total segment revenue because businesses needed to create centralized monitoring systems and complete asset performance management systems. Smart manufacturing initiatives and industrial automation programs in Germany support the technology adoption process.

Standalone solutions are expected to grow at a faster pace, with a CAGR of 40%, supported by cost efficiency and ease of deployment among small and medium enterprises. The mid-scale industrial sector grows through digital technology implementation, which helps the segment to expand.

By End Use

The manufacturing sector generated 38% of total market revenue in 2025, because factories operated their equipment at high levels while automation technology became more common. The industry sector adopts new technologies through government industrial development programs and their operational efficiency development programs.

The energy and utilities sectors, along with other industrial areas, will expand most rapidly because their infrastructure reliability needs and digital monitoring system growth will create a market that grows at 41% during the upcoming years. The growth of various end use industries receives support from critical infrastructure investments and efficiency optimization efforts.

Regional Insights

North America

The market in North America reached 33% market share by 2025 according to market estimates. The region's industrial growth results from its modern industrial facilities and its early use of AI technology and its many industries that depend on automation. The manufacturing and energy sectors in New York, Houston and Chicago establish predictive maintenance solutions throughout their industrial base. The National Institute of Standards and Technology together with government institutions develops standards and rules to support advanced maintenance technology implementation which helps the market grow in this area.

Europe

The European market 2025 showed a 26% share which manufacturers can achieve through established production systems and their efforts to enhance industrial performance. The automotive, energy, and heavy industries of Germany, France, and Italy have implemented predictive maintenance solutions at their facilities. The European Commission introduced digital transformation programs together with policy frameworks to create smart manufacturing systems and automated production processes which drive businesses to implement advanced monitoring systems. The region experiences continuous demand because industries increase their use of digital platforms and industrial analytics systems.

Asia Pacific

Asia Pacific held a 22% market share in 2025 because China, India and Japan rapidly grow their manufacturing capacity and their industrial sectors start using digital technologies. Beijing, Mumbai and Tokyo function as industrial centers which enable the use of predictive maintenance software in their respective areas. The government digital infrastructure programs and industrial modernization initiatives backing industrial modernization programs have resulted in faster technology adoption across all sectors. The Ministry of Economy, Trade and Industry together with other governmental bodies establish programs which drive industrial sectors to implement advanced maintenance solutions.

Rest of the World

The market distribution showed that the Rest of the World which consists of Latin America, the Middle East and Africa reaching 19% market share by 2025. The region experiences economic growth because businesses invest more in industrial facilities and they adopt automation systems at a slow pace while they learn about better ways to run their operations. Resource-based industries and energy sectors in emerging markets have started using predictive maintenance systems at their initial facilities. The government support programs for industrial development and infrastructure projects drive technology adoption in major industries. The remaining market demand not specifically covered by North America, Europe, and Asia Pacific is included within this segment, ensuring the overall regional distribution remains balanced within the global market structure.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with the presence of global and regional players who compete through their technological innovations, pricing methods and their efforts to expand into new markets. Companies are increasingly investing in research and development, artificial intelligence capabilities and digital platforms to strengthen their market position. The National Institute of Standards and Technology and other organizations have developed industry guidelines and interoperability frameworks that promote standardized solutions. Strategic partnerships and advanced analytics integration drive competitive differentiation in essential markets.

Mini Profiles

C3.ai focuses on enterprise AI driven predictive maintenance solutions, supported by strong digital capabilities, scalable platforms, and strategic partnerships that enhance operational efficiency across industrial sectors.

General Electric operates in industrial and infrastructure segments, emphasizing performance optimization, asset reliability, and advanced analytics solutions for large scale energy and manufacturing environments.

Honeywell leverages integrated automation systems and industrial IoT capabilities to expand market presence, supported by strong global distribution networks and advanced engineering expertise.

IBM focuses on AI enabled predictive maintenance platforms, supported by cloud infrastructure, data analytics expertise, and strong enterprise relationships across multiple industries.

Microsoft operates in digital and cloud based industrial solutions, emphasizing scalable platforms, data integration, and advanced analytics to enhance predictive maintenance capabilities across enterprises.

Key Players

- C3.ai

- General Electric

- Honeywell

- IBM

- KCF Technologies

- Microsoft

- Oracle

- ONYX Insight

- PTC

- Siemens

Recent Developments

In March 2026, Microsoft enhanced its cloud based predictive maintenance capabilities through Azure AI integrations, enabling real time asset monitoring and improved operational efficiency across industrial environments. The update focuses on scalable analytics and digital twin integration for advanced maintenance planning.

In January 2026, Oracle expanded its AI driven asset management solutions, strengthening predictive maintenance capabilities within enterprise applications. The development supports improved equipment reliability and data driven decision making across manufacturing and energy sectors.

In February 2026, KCF Technologies advanced its wireless vibration monitoring systems, enabling more precise predictive maintenance for rotating equipment. The initiative focuses on improving early fault detection and reducing operational downtime.

In April 2025, ONYX Insight expanded its predictive analytics platform for wind energy assets, enhancing condition monitoring and failure prediction capabilities. The development supports improved asset performance and lifecycle management in renewable energy operations.

In October 2025, C3.ai strengthened its enterprise AI applications for predictive maintenance, focusing on large scale industrial deployments. The company continues to enhance data driven insights and operational optimization through advanced AI models.

Global AI Driven Predictive Maintenance Market Coverage

Offering Insight and Forecast 2026 - 2035

- Software

- Services

Deployment Mode Insight and Forecast 2026 - 2035

- Cloud Based

- On Premises

Solution Type Insight and Forecast 2026 - 2035

- Integrated

- Standalone

Technique Insight and Forecast 2026 - 2035

- Vibration analysis

- Oil analysis

- Others

Organization Size Insight and Forecast 2026 - 2035

- Large Enterprises

- Small And Medium Enterprises

End Use Insight and Forecast 2026 - 2035

- Manufacturing

- Energy and Utilities

- Transportation and Logistics

- Healthcare

- Others

Global AI Driven Predictive Maintenance Market by Region

- North America

- By Offering

- By Deployment Mode

- By Solution Type

- By Technique

- By Organization Size

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Offering

- By Deployment Mode

- By Solution Type

- By Technique

- By Organization Size

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Offering

- By Deployment Mode

- By Solution Type

- By Technique

- By Organization Size

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Offering

- By Deployment Mode

- By Solution Type

- By Technique

- By Organization Size

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for AI Driven Predictive Maintenance Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Offering

1.2.2. By

Deployment Mode

1.2.3. By

Solution Type

1.2.4. By

Technique

1.2.5. By

Organization Size

1.2.6. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Offering

5.1.1. Software

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Deployment Mode

5.2.1. Cloud Based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. On Premises

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Solution Type

5.3.1. Integrated

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Standalone

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Technique

5.4.1. Vibration analysis

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Oil analysis

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Others

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Organization Size

5.5.1. Large Enterprises

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Small And Medium Enterprises

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.6. By End Use

5.6.1. Manufacturing

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Energy and Utilities

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Transportation and Logistics

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. Healthcare

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

5.6.5. Others

5.6.5.1. Market Definition

5.6.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Offering

6.2. By

Deployment Mode

6.3. By

Solution Type

6.4. By

Technique

6.5. By

Organization Size

6.6. By

End Use

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Offering

7.2. By

Deployment Mode

7.3. By

Solution Type

7.4. By

Technique

7.5. By

Organization Size

7.6. By

End Use

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Offering

8.2. By

Deployment Mode

8.3. By

Solution Type

8.4. By

Technique

8.5. By

Organization Size

8.6. By

End Use

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Offering

9.2. By

Deployment Mode

9.3. By

Solution Type

9.4. By

Technique

9.5. By

Organization Size

9.6. By

End Use

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

C3.ai

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

General Electric

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Honeywell

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

IBM

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

KCF Technologies

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Microsoft

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Oracle

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

ONYX Insight

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

PTC

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Siemens

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

AI Driven Predictive Maintenance Market