Artificial Intelligence (AI) in Manufacturing Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Deployment Mode (On-Premise, Cloud-Based), by Application (Predictive Maintenance, Quality Inspection and Defect Detection, Production Planning and Scheduling, Supply Chain Optimization, Energy Management), by End User (Discrete Manufacturing, Process Manufacturing), by Region (North America, Asia Pacific, Europe, Other Regions)

| Status : Published | Published On : Jan, 2026 | Report Code : VRICT5203 | Industry : ICT & Media | Available Format :

|

Page : 210 |

Artificial Intelligence in Manufacturing Market Overview

The global artificial intelligence (AI) in manufacturing market which was valued at approximately USD 12.4 billion in 2025 and is estimated to reach around USD 18.6 billion in 2026, is projected to reach around USD 295.8 billion by 2035, expanding at a CAGR of about 36% during the forecast period from 2026 to 2035. Market expansion is primarily supported by accelerating adoption of predictive maintenance, real-time analytics, and AI-driven supply chain optimization across manufacturing operations in developed and emerging industrial economies.

Adoption is supported by manufacturers’ focus on operational efficiency, quality control, and reduction of production downtime, aligned with formal AI and industrial automation initiatives such as the United States National Institute of Standards and Technology (NIST) AI Manufacturing Program, the European Union Horizon Europe industrial AI projects, and India’s National AI Mission. These programs facilitate deployment of AI-enabled robotics, computer vision systems, and smart factory solutions while promoting research, workforce development, and standardization of AI technologies in manufacturing ecosystems. AI integration enables predictive equipment maintenance, optimized resource utilization, and autonomous production decision-making, enhancing overall productivity and competitiveness. Public investment programs and policy frameworks across Asia-Pacific, North America, and Europe continue to sustain demand from automotive, electronics, aerospace, and heavy machinery manufacturing sectors.

Artificial Intelligence in Manufacturing Market Dynamics

Market Trends

The AI in manufacturing industry is undergoing a strategic shift toward intelligent automation and data-driven production processes, aligned with industrial modernization programs promoted by public and government agencies. Initiatives such as the United States National Institute of Standards and Technology (NIST) AI Manufacturing Program, the European Union Horizon Europe industrial AI projects, and India’s National AI Mission emphasize predictive maintenance, robotics integration, and standardized AI protocols to enhance operational efficiency, reduce downtime, and optimize resource utilization. This trend is accelerating the adoption of AI-driven production planning and quality monitoring systems across manufacturing facilities globally.

Manufacturers are increasingly deploying machine learning algorithms, computer vision technologies, and AI-enabled supply chain management tools to improve real-time visibility, demand forecasting, and fault detection, consistent with national industrial transformation strategies in regions such as the United States, Europe, and Asia-Pacific. Government-backed research funding, public-private AI innovation labs, and policy frameworks supporting Industry 4.0 adoption are reinforcing demand for smart factories capable of autonomous decision-making, flexible production scheduling, and energy-efficient operations. These developments are driving companies to prioritize integrated AI solutions, advanced analytics, and workforce upskilling, thereby redefining competitive dynamics within the global manufacturing sector.

Growth Drivers

Globally, manufacturers are increasingly transitioning from manual and semi-automated production processes toward AI-enabled, data-driven manufacturing architectures. The deployment of predictive maintenance solutions, computer vision systems, and AI-driven robotics enhances operational efficiency, reduces production downtime, and improves product quality while enabling seamless integration across production lines. Government-backed programs such as the United States National Institute of Standards and Technology (NIST) AI Manufacturing Program, the European Union Horizon Europe industrial AI initiatives, and India’s National AI Mission provide funding, standardized protocols, and research support, which facilitate widespread adoption of AI technologies across manufacturing facilities.

The accelerated adoption of Industry 4.0 frameworks is another primary growth driver. Increasing investments in smart factory infrastructure, automation equipment, and digital twin technologies enable manufacturers to optimize resource utilization, forecast demand accurately, and maintain production flexibility under variable market conditions. AI integration supports predictive analytics, real-time monitoring, and autonomous decision-making, enhancing responsiveness to operational disruptions and supply chain fluctuations.

In addition, enterprises are deploying AI-enabled supply chain management and energy optimization tools that allow continuous process monitoring, early fault detection, and reduction of operational costs. These solutions improve throughput, energy efficiency, and lifecycle performance of critical assets while minimizing downtime. Public investment initiatives and industrial innovation hubs across regions such as Asia-Pacific, North America, and Europe continue to strengthen adoption, supporting long-term competitiveness and sustainability in global manufacturing operations.

Market Restraints / Challenges

Despite strong growth prospects, the market landscape faces certain challenges that may limit expansion. High capital investment requirements for AI-enabled robotics, predictive maintenance systems, computer vision technologies, and supporting software platforms remain a primary restraint. Government reports such as the United States National Institute of Standards and Technology (NIST) AI Manufacturing Program Guidelines and India’s National AI Mission 2025 highlight that small and medium-sized enterprises, particularly in developing economies, encounter budget constraints and limited access to skilled personnel, which can slow technology adoption.

Dependence on advanced AI algorithms, cloud infrastructure, and specialized sensors poses operational challenges for manufacturers and technology providers. Reliance on imported AI hardware, proprietary software platforms, and external expertise can result in higher costs, delivery delays, and integration complexities, especially during periods of economic uncertainty or supply chain disruptions. Furthermore, the integration of AI in manufacturing necessitates robust cybersecurity frameworks to protect sensitive operational data, ensure secure machine-to-machine communication, and comply with national standards such as the U.S. NIST Cybersecurity Framework and the European Union’s NIS2 Directive. Continuous monitoring, system upgrades, and risk mitigation strategies are essential to manage cyber threats and operational vulnerabilities, increasing project complexity and lifecycle costs.

Market Opportunities

The AI in manufacturing market presents significant opportunities in smart factory deployment, particularly driven by technological advancements and the growing adoption of Industry 4.0 frameworks. Companies offering modular, scalable, and AI-enabled solutions are well-positioned to capture incremental demand from automotive, electronics, aerospace, and heavy machinery manufacturers. Government reports such as the United States National Institute of Standards and Technology (NIST) AI Manufacturing Program and India’s National AI Mission 2025 highlight strategic investments in AI research, workforce development, and automation infrastructure, which are creating favorable conditions for accelerated adoption in both developed and emerging economies.

Another key opportunity lies in AI-driven predictive maintenance and supply chain optimization, where rising investments in digital tools, analytics platforms, and machine learning applications are creating avenues for higher operational efficiency and long-term client engagement. Public-private innovation hubs, including the European Union Horizon Europe industrial AI initiatives, promote collaborative research and pilot programs that enable manufacturers to implement smart production lines, enhance real-time monitoring, and reduce operational costs. Advancements in AI-enabled robotics, energy management, and autonomous decision-making systems are expected to strengthen manufacturing resilience, improve resource utilization, and enhance competitiveness across regions such as Asia-Pacific, North America, and Europe.

Global Artificial Intelligence in Manufacturing Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 12.4 Billion |

|

Revenue Forecast in 2035 |

USD 295.8 Billion |

|

Growth Rate |

36% |

|

Segments Covered in the Report |

By Component, By Deployment Mode, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Asia Pacific, Europe, Other Regions |

|

Key Companies |

Siemens AG, IBM Corporation, ABB Ltd., Rockwell Automation, NVIDIA Corporation, General Electric, Mitsubishi Electric, Fanuc Corporation, Intel Corporation, SAP SE |

|

Customization |

Available upon request |

Artificial Intelligence in Manufacturing Market Segmentation

By Component

Hardware is estimated to account for approximately 46% of total market revenue in 2025. This reflects the essential role of industrial sensors, edge AI devices, vision systems, and AI-enabled robotics that form the physical foundation of intelligent manufacturing environments. Hardware demand remains strong due to high deployment volumes across production lines, inspection stations, and automated material handling systems, particularly in large-scale manufacturing facilities.

Software solutions contribute around 34% of market revenue, supported by growing adoption of machine learning platforms, production analytics, digital twins, and AI-based quality management systems. This segment is expected to register a higher growth rate of about 45% during the forecast period, driven by manufacturers’ focus on real-time decision-making, process optimization, and predictive maintenance capabilities.

Services represent approximately 20% of total revenue, encompassing system integration, consulting, model training, and lifecycle support. Service demand continues to expand at nearly 41%, as manufacturers require specialized expertise to deploy, customize, and maintain AI solutions across complex production environments.

By Deployment Mode

On-premise deployment accounted for an estimated 58% of market revenue in 2025, as manufacturers prioritize data security, low-latency processing, and direct control over production-critical AI applications. On-premise solutions remain dominant in regulated and asset-intensive industries, where operational continuity and intellectual property protection are critical considerations.

Cloud-based deployment represents approximately 42% of the market and is witnessing faster growth at nearly 47% during the forecast period. This growth is driven by scalability, lower upfront costs, and increasing availability of industrial-grade cloud platforms. Hybrid architectures are gaining traction as manufacturers integrate cloud analytics with on-site systems to balance performance and flexibility.

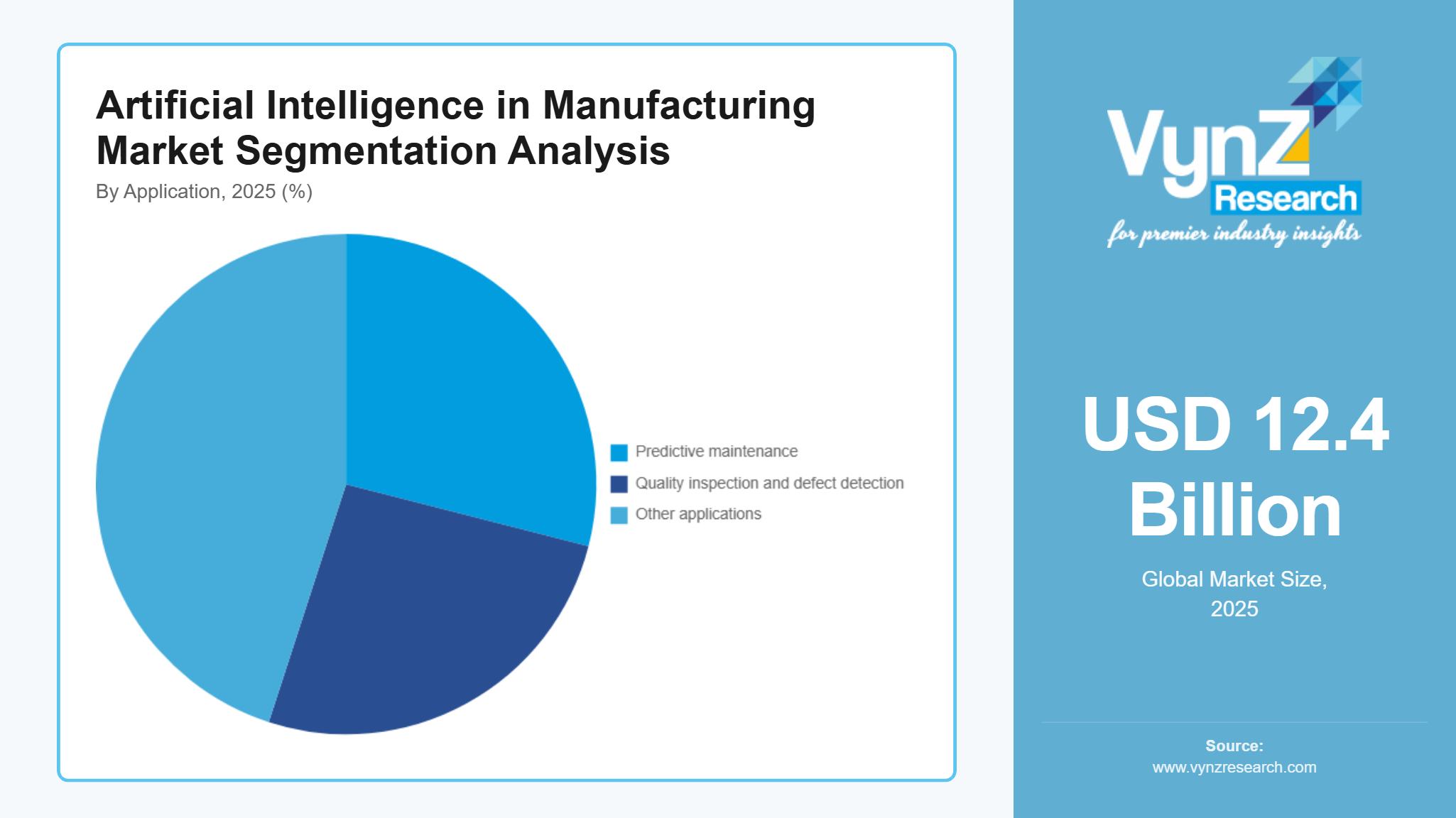

By Application

Predictive maintenance is estimated to hold around 29% of total market revenue in 2025, reflecting widespread adoption of AI to reduce unplanned downtime and extend equipment lifecycles. This segment continues to expand steadily, supported by measurable cost savings and improved asset utilization across manufacturing plants.

Quality inspection and defect detection contribute approximately 26%, driven by increased deployment of computer vision systems for real-time monitoring and compliance with stringent quality standards. This application area is expected to grow at about 44%, supported by demand for higher production accuracy and reduced material waste.

Other applications, including production planning, supply chain optimization, and energy management, collectively account for nearly 45% of the market, supported by integrated AI platforms that deliver cross-functional operational insights.

By End User

Discrete manufacturing industries account for approximately 61% of total market revenue in 2025, supported by high adoption across automotive, electronics, and aerospace manufacturing. These industries benefit from AI-enabled automation, precision manufacturing, and real-time quality control, which directly improve productivity and cost efficiency.

Process manufacturing represents around 39% of the market and is expected to grow at a faster rate of nearly 42% during the forecast period. Growth is driven by increasing use of AI in chemicals, pharmaceuticals, food and beverages, and metals, where continuous process optimization, energy efficiency, and predictive analytics are critical to maintaining operational stability and regulatory compliance.

Regional Insights

North America

North America is estimated to account for approximately 26% of the global AI in manufacturing market in 2025. Growth is driven by early adoption of advanced automation, strong digital infrastructure, and sustained investment in smart manufacturing technologies. The United States leads regional adoption, supported by federal initiatives such as the U.S. Department of Commerce led Manufacturing USA program and the National Institute of Standards and Technology AI Manufacturing Program, which promote AI integration, interoperability standards, and workforce upskilling. Strong demand from automotive, aerospace, electronics, and industrial equipment manufacturing hubs across California, Texas, Michigan, and Ohio continues to support market expansion through large-scale deployment of predictive analytics, robotics, and computer vision systems.

Asia Pacific

Asia Pacific is projected to account for approximately 32% of the market in 2025, representing the largest regional share. Rapid industrialization, high-volume manufacturing, and government-led digital transformation initiatives are key growth drivers. China continues to invest heavily under national programs such as Made in China 2025, emphasizing AI-enabled automation and intelligent factories. In India, initiatives including the National AI Mission, Digital India, and smart manufacturing policies under the Ministry of Heavy Industries are accelerating AI adoption across automotive, electronics, and process manufacturing. Japan and South Korea further support growth through robotics leadership and AI-driven production optimization, reinforcing regional dominance.

Europe

Europe represents approximately 20% of the AI in manufacturing market in 2025. Adoption is supported by strong regulatory alignment, sustainability targets, and industrial modernization programs. European Union initiatives such as Horizon Europe and national Industry 4.0 strategies in Germany, France, Italy, and the United Kingdom promote AI-driven automation, energy efficiency, and digital twins across manufacturing operations. Regulatory frameworks focusing on ethical AI deployment, data protection, and cybersecurity further shape adoption patterns. Strong demand from automotive, machinery, and pharmaceutical manufacturing clusters continues to drive steady regional growth.

Other Regions

The remaining regions collectively contribute approximately 22% of the global AI in manufacturing market. These regions include Latin America, the Middle East, and parts of Africa, where adoption is supported by gradual industrial modernization, government-backed digital economy programs, and foreign direct investment in manufacturing capacity. Although market penetration remains lower compared with North America, Asia Pacific, and Europe, increasing focus on automation, cost efficiency, and productivity enhancement positions these regions as long-term growth opportunities. The remaining share reflects contributions from regions not covered individually in the above analysis.

Competitive Landscape / Company Insights

The AI in manufacturing market is moderately to highly competitive, with global and regional players emphasizing technology innovation, solution scalability, and geographic expansion. Key companies such as Siemens, ABB, IBM, Microsoft, Rockwell Automation, and Fanuc are investing in AI platforms, industrial analytics, and smart automation to strengthen their market presence. Adoption is supported by government-backed initiatives including the U.S. National Institute of Standards and Technology AI Manufacturing Program, the European Union Horizon Europe framework, and India’s National AI Mission, which encourage deployment of secure, interoperable, and productivity-driven AI solutions across manufacturing facilities in North America, Europe, and Asia Pacific.

Mini Profiles

Siemens AG has been adding AI features to its automation tools so factories can monitor machines more closely and avoid unnecessary energy waste. Many users find it easier to adopt these updates because Siemens already fits into their existing setups.

ABB Ltd has been improving its robotics and motion equipment with small AI adjustments that make movements more accurate and safer. Factories prefer ABB because the systems adapt quickly when production needs change or when different batches come through.

Rockwell Automation uses AI inside its control platforms to spot issues earlier and keep production running without sudden stoppages. Plants shifting from older machinery often choose Rockwell because it lets them upgrade to smarter systems without disrupting daily work.

IBM Corporation offers data-driven AI platforms that study factory patterns, detect risks, and support better planning. Its learning-based systems help maintenance teams make faster, clearer decisions across industrial environments.

NVIDIA Corporation provides GPUs and edge processors that power real-time analytics and vision systems inside factories. Its computing platforms support defect detection, automation, and rapid data processing on the shop floor.

Key Players

- Siemens AG

- IBM Corporation

- ABB Ltd.

- Rockwell Automation

- NVIDIA Corporation

- General Electric

- Mitsubishi Electric

- Fanuc Corporation

- Intel Corporation

- SAP SE

Recent Developments

Jan 2026 - Fanuc Corporation has formally partnered with NVIDIA to bring ‘physical AI’ into mainstream manufacturing in a move set to shape the next generation of smart factories. FANUC robots shall be integrated with NVIDIA's state-of-the-art AI computing stack, including on-robot systems like NVIDIA Jetson and simulation platforms like NVIDIA Isaac Sim. FANUC has also added support for ROS 2, an open-source robotics platform that allows Python programming which makes it easier for companies and developers to build AI-driven robotics applications on top of FANUC's dependable industrial hardware.

May 2025 - In a significant push for digital transformation in the region, Mitsubishi Electric is enhancing its Factory Automation (FA) with AI and robotics for Asia-Pacific, concentrating on energy savings and precision. This is probably through partnerships like the one with Realtime Robotics, integrating advanced control for smarter, more efficient factories in line with goals to reduce energy use and address labor shortages.

August 2025 - By improving its edge AI processors for manufacturing applications most notably with the introduction of its Intel Core Ultra Series 3 processors at CES 2026 Intel Corporation has in reality solidified its position in industrial AI. For smart factory installations, these CPUs are made to provide quicker inference, reduced latency, and increased dependability.

Global Artificial Intelligence in Manufacturing Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Deployment Mode Insight and Forecast 2026 - 2035

- On-Premise

- Cloud-Based

Application Insight and Forecast 2026 - 2035

- Predictive Maintenance

- Quality Inspection and Defect Detection

- Production Planning and Scheduling

- Supply Chain Optimization

- Energy Management

End User Insight and Forecast 2026 - 2035

- Discrete Manufacturing

- Process Manufacturing

Region Insight and Forecast 2026 - 2035

- North America

- Asia Pacific

- Europe

- Other Regions

Global Artificial Intelligence in Manufacturing Market by Region

- North America

- By Component

- By Deployment Mode

- By Application

- By End User

- By Region

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Deployment Mode

- By Application

- By End User

- By Region

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Deployment Mode

- By Application

- By End User

- By Region

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Deployment Mode

- By Application

- By End User

- By Region

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Artificial Intelligence in Manufacturing Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Deployment Mode

1.2.3. By

Application

1.2.4. By

End User

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Deployment Mode

5.2.1. On-Premise

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Cloud-Based

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Predictive Maintenance

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Quality Inspection and Defect Detection

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Production Planning and Scheduling

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Supply Chain Optimization

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Energy Management

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Discrete Manufacturing

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Process Manufacturing

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. North America

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Asia Pacific

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Europe

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Other Regions

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Deployment Mode

6.3. By

Application

6.4. By

End User

6.5. By

Region

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Deployment Mode

7.3. By

Application

7.4. By

End User

7.5. By

Region

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Deployment Mode

8.3. By

Application

8.4. By

End User

8.5. By

Region

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Deployment Mode

9.3. By

Application

9.4. By

End User

9.5. By

Region

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Siemens AG

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

IBM Corporation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

ABB Ltd.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Rockwell Automation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

NVIDIA Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

General Electric

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Mitsubishi Electric

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Fanuc Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Intel Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

SAP SE

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Artificial Intelligence in Manufacturing Market