Gambling Software Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Software Type (Sports Betting Software, Casino Software, Poker Software, Lottery Software, Bingo Software, Others), by Deployment Type (Cloud-Based, On-Premise), by Device (Mobile, Desktop)

| Status : Published | Published On : Mar, 2026 | Report Code : VRICT5223 | Industry : ICT & Media | Available Format :

|

Page : 195 |

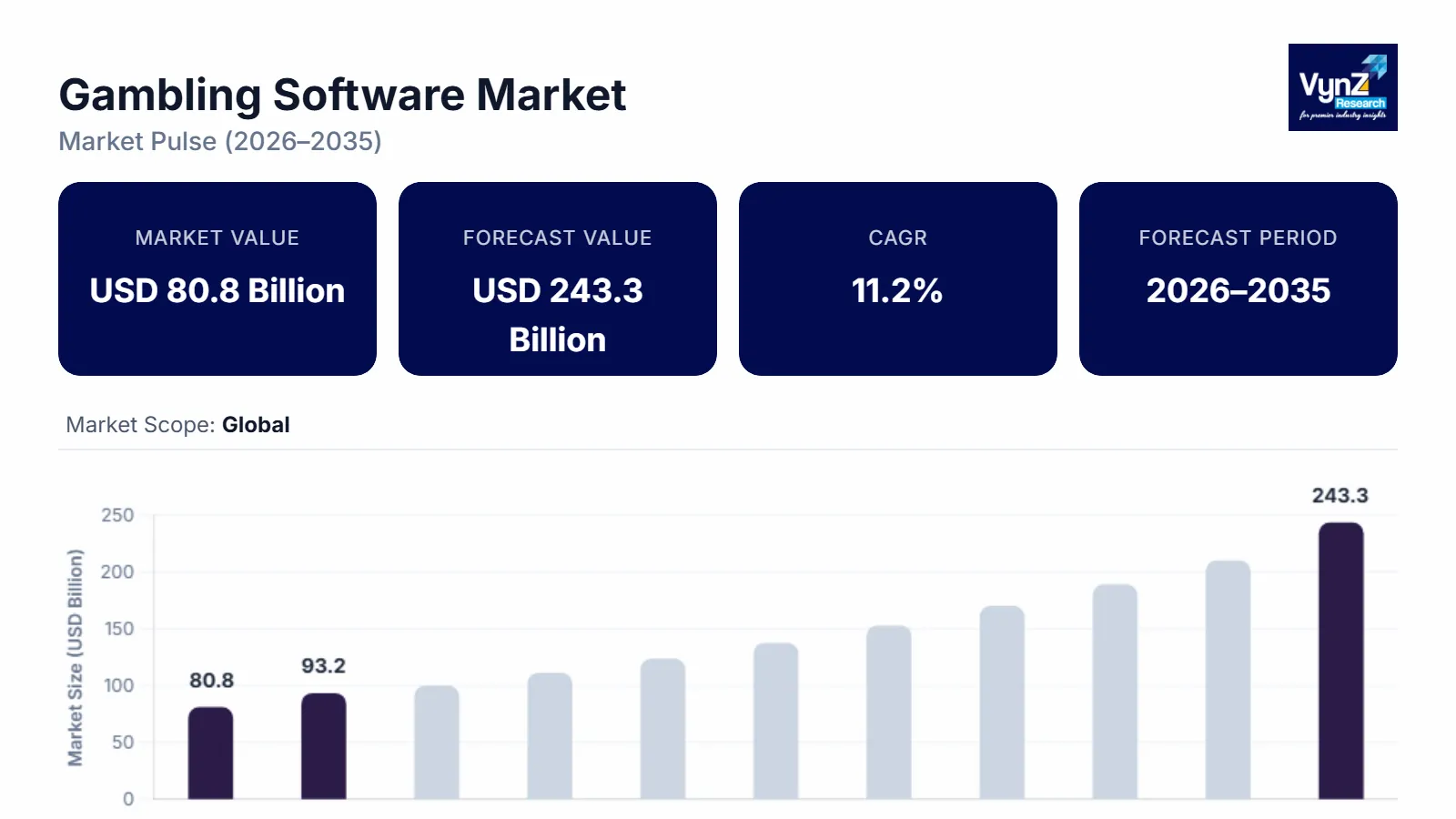

Gambling Software Market Overview

The gambling software market which was valued at approximately USD 80.8 billion in 2025 and is estimated to reach around USD 93.2 billion in 2026, is projected to reach close to USD 243.3 billion by 2035, expanding at a CAGR of about 11.2% during the forecast period from 2026 to 2035.

The gambling software market is expanding rapidly as digital infrastructure reshapes how wagering and gaming experiences are created, delivered, and monetized. Operators are increasingly shifting from traditional systems to flexible, software-driven platforms that enable faster market entry, real-time personalization, and seamless omnichannel experiences. Advances in cloud computing, data analytics, and artificial intelligence are allowing providers to optimize game performance, manage risk more effectively, and engage players with highly tailored content. Simultaneously, the global surge in mobile usage has transformed gambling into an always-accessible activity, significantly increasing player participation and lifetime value. Regulatory modernization in key markets is further accelerating demand for compliant, secure, and scalable software solutions.

Additionally, heightened competition among operators is driving continuous investment in innovative game mechanics, immersive interfaces, and advanced security frameworks. Together, these forces are positioning gambling software as a critical enabler of growth, efficiency, and differentiation across the global gaming ecosystem.

Gambling Software Market Dynamics

Market Trends

A defining trend in the gambling software market is the sustained rise of online gambling participation, driven by widespread digital adoption and regulatory transparency. According to official statistics from the Gambling Commission’s Gambling Survey for Great Britain Wave 1 (2025), 38 % of adults reported participating in online gambling activities in the past four weeks — a level consistent with prior years and reflecting entrenched digital behaviour. This illustrates that nearly two in five adults now interact with digital wagering platforms regularly, underscoring the market’s shift away from purely brick-and-mortar play. The prevalence of mobile and web-based access, enhanced by secure identity verification and seamless payment systems, continues to draw diverse demographics. As software evolves to support personalised content, real-time engagement, and immersive interfaces, online participation establishes a structural backbone for long-term market expansion, signalling a fundamental transformation in how wagering products are consumed and monetised.

Growth Drivers

A major driver for the gambling software market is the economic momentum generated through regulated online gambling activity. Official UK government data published in the UK betting and gaming statistics for April - August 2025 shows that total betting and gaming receipts reached £1,786 million, representing a 9 % increase compared to the same period in the prior year. This growth underscores how structured oversight and licensed digital platforms contribute meaningfully to public revenue through duties such as Remote Gaming Duty and Lottery Duty. Governments are increasingly recognising this value, aligning taxation frameworks with digital channel performance while mandating compliance, responsible gaming measures, and enhanced data protection. The assured flow of regulated revenue incentivises operators to invest in advanced gambling software - from secure identity systems to predictive analytics - that both comply with governmental standards and attract players with seamless digital experiences. This convergence of fiscal benefits and technology investment is accelerating market expansion globally.

Market Restraints / Challenges

One of the most significant challenges facing the gambling software market is navigating an increasingly complex and fragmented regulatory landscape while maintaining player trust. Governments across regions are tightening oversight around responsible gaming, data protection, advertising standards, and financial transparency. These evolving requirements demand continuous software updates, jurisdiction-specific compliance frameworks, and robust monitoring systems, all of which increase development time and operational costs. For software providers, aligning platforms with diverse regulatory expectations often changing with little notice can slow innovation and complicate global scalability. At the same time, public scrutiny around gambling-related harm places pressure on operators to embed ethical design principles, such as player protection tools, real-time risk monitoring, and transparent reporting mechanisms. Failure to meet these expectations can result in reputational damage and regulatory penalties. As competition intensifies, balancing compliance, security, and innovation without compromising user experience remains a critical hurdle, requiring strategic foresight and deep regulatory expertise.

Market Opportunities

A compelling opportunity for the gambling software market lies in the continued expansion of regulated online wagering across jurisdictions that previously lacked clear governance. For example, U.S. states that have sanctioned online casinos and sports betting saw record online revenue of $27.1 billion in 2025, with states collecting more than $6 billion in taxes on online gambling revenue. This demonstrates substantial untapped potential where legal frameworks are solidifying and public reporting provides transparency. As more regions establish licencing pathways and fiscal regimes that support regulated play, software vendors can capitalise by delivering compliant, secure, and scalable platforms tailored for local requirements. Investments in cloud-native architectures, advanced fraud prevention, and mobile-first user interfaces further enable rapid deployment into emerging markets. By aligning product offerings with evolving regulations and government priorities including player protection and responsible gaming features, the software industry is positioned to serve expanding legal ecosystems and capture high-growth opportunities.

Global Gambling Software Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 80.8 Billion |

|

Revenue Forecast in 2035 |

USD 243.3 Billion |

|

Growth Rate |

11.2% |

|

Segments Covered in the Report |

Software Type, Deployment Type, Device |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Playtech plc, Evolution AB, International Game Technology PLC, Novomatic, SOFTSWISS, Flutter Entertainment plc, Entain plc, Bet365, Evoke plc, Betsson AB |

|

Customization |

Available upon request |

Gambling Software Market Segmentation

By Software Type

Casino software represents the largest category, with an estimated market share of about 40% in 2025, due to its ability to deliver consistent engagement and diversified revenue streams. Unlike single-event wagering, casino platforms support continuous play through slots, live dealer games, and digital table games, resulting in higher session frequency and sustained user interaction. Operators prioritize casino software because it allows extensive customization, localized themes, and scalable content libraries that appeal to a wide demographic. The integration of loyalty programs, bonus engines, and player analytics further enhances retention and lifetime value. From an operational perspective, casino platforms are adaptable across multiple regulatory environments, making them easier to deploy globally. This combination of broad appeal, operational flexibility, and monetization efficiency positions casino software as the dominant revenue contributor in the market.

Sports betting software is the fastest-growing category with a CAGR of 11.7% in the coming years, as wagering shifts toward real-time, data-driven experiences. Live and in-play betting formats demand sophisticated platforms capable of processing high-frequency data, dynamic odds adjustments, and instant user interactions. The growing popularity of sports content, including esports and virtual sports, has accelerated the need for advanced betting engines that support multiple markets simultaneously. Sports betting platforms also benefit from strong engagement during major sporting events, driving spikes in user activity and platform traffic. Operators increasingly invest in features such as cash-out options, personalized odds, and interactive interfaces to differentiate their offerings. As consumers seek immersive, fast-paced betting experiences, sports betting software continues to expand at a pace unmatched by other software types.

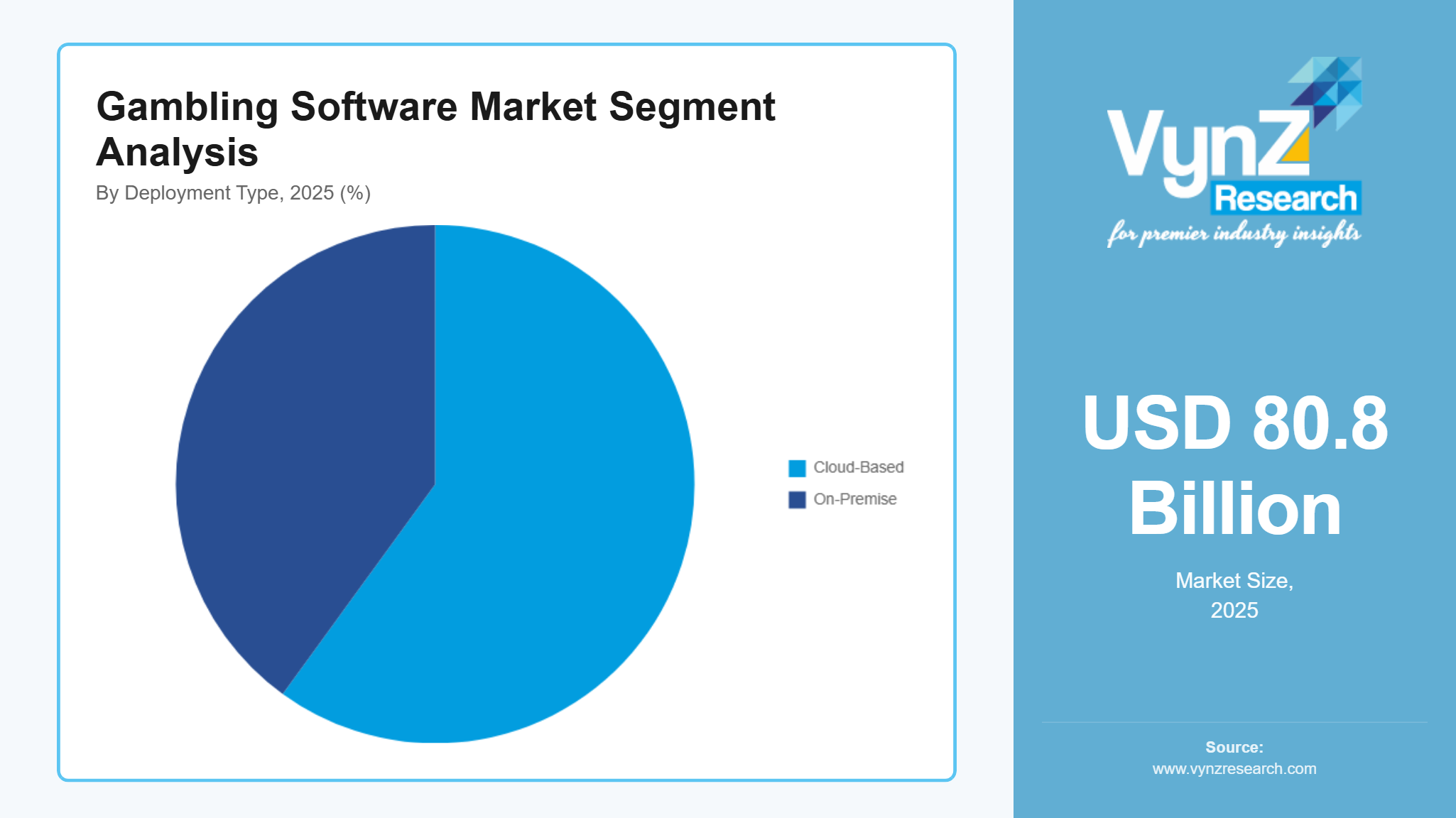

By Deployment Type

Cloud-based deployment is the largest as well as rapidly growing category in the market due to its operational efficiency and scalability. Cloud infrastructure allows operators to manage large user volumes, peak betting activity, and real-time data processing without significant capital investment. It supports rapid deployment across multiple regions while enabling seamless software updates and centralized management. Cloud platforms also enhance security, disaster recovery, and system reliability—critical factors in regulated gambling environments. For software providers, cloud deployment enables modular development, easier integration with third-party services, and faster innovation cycles. As competition intensifies, the ability to scale quickly and optimize performance in real time has made cloud-based deployment the preferred foundation for modern gambling platforms.

By Device

Mobile devices represent both the largest and fastest-growing category in the gambling software market, driven by consumer demand for convenience and instant access. Smartphones have become the primary channel for sports betting, casino gaming, and lottery participation, enabling engagement anytime and anywhere. Mobile platforms support features such as live betting, personalized notifications, and seamless digital payments, significantly improving user experience and retention. Operators increasingly adopt mobile-first design strategies to align with evolving user behavior. As gambling continues to shift toward on-demand digital experiences, mobile devices remain the central growth driver shaping platform development and long-term market expansion.

Regional Insights

Asia Pacific

Asia Pacific is the fastest-growing region in the gambling software market, fueled by rapid digitalization, expanding internet access, and rising smartphone adoption. The region’s large population base and growing middle class are driving increased participation in online gaming and betting platforms. Operators are increasingly investing in mobile-first and cloud-native solutions to capture this expanding user base. Localization, multilingual interfaces, and region-specific compliance features are critical to success. As regulatory frameworks continue to evolve across select markets, demand for flexible, scalable gambling software is accelerating, positioning Asia Pacific as the primary engine of future market growth.

Europe

Europe remains a highly established and regulated market for gambling software, characterized by strong adoption of online casinos, sports betting, and lottery platforms. The region benefits from mature regulatory frameworks that emphasize player protection, data security, and responsible gaming practices. European operators place significant emphasis on compliance-driven innovation, investing in advanced security tools, identity verification systems, and analytics. Mobile and cloud-based platforms are widely adopted, supporting omnichannel experiences. While growth is moderate compared to emerging regions, Europe continues to generate stable demand for sophisticated gambling software, making it a strategically important and technologically advanced regional market.

North America

North America held the largest market share of around 35% in 2025, driven by advanced digital infrastructure, high consumer spending power, and widespread adoption of online wagering platforms. The region benefits from strong demand for sports betting, casino gaming, and lottery software supported by sophisticated payment systems and data-driven platforms. Operators in North America prioritize technology innovation, focusing on real-time analytics, personalized user experiences, and secure cloud-based architectures. Regulatory clarity in several jurisdictions has encouraged investment in compliant, scalable software solutions. Additionally, intense competition among operators is accelerating platform modernization, positioning North America as the most mature and revenue-dominant region in the global gambling software market.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, represents a high-potential emerging market for gambling software. These regions are witnessing increasing digital connectivity, improving mobile penetration, and growing interest in online gaming platforms. In Latin America, gradual regulatory developments are opening opportunities for licensed operators and compliant software providers. The Middle East and Africa, while more conservative in regulatory approach, are seeing rising demand for digital gaming solutions aligned with local laws and cultural considerations. Operators entering these markets prioritize scalable, cloud-based platforms that support flexible compliance and localization. As legal frameworks evolve and digital adoption deepens, these regions are expected to contribute significantly to long-term global market expansion.

Competitive Landscape / Company Insights

The gambling software market is moderately fragmented, characterized by the presence of a mix of established global technology providers and specialized regional players competing across multiple product categories. Market participants differentiate themselves through platform reliability, regulatory compliance capabilities, scalability, and the ability to support diverse gambling formats such as sports betting, casino gaming, and lotteries. Competition is increasingly centered on innovation, with vendors investing in cloud-native architectures, advanced analytics, and personalized user engagement tools to strengthen their value propositions.

Strategic partnerships, platform integrations, and geographic expansion are commonly adopted to enhance market reach and accelerate deployment timelines. At the same time, compliance expertise and responsible gaming features have become critical competitive factors, as operators seek software solutions that align with evolving regulatory expectations. As digital gambling adoption intensifies, companies that combine technological agility with deep regulatory understanding are best positioned to strengthen their competitive standing and secure long-term contracts with operators globally.

Mini Profiles

Evolution AB develops and licenses B2B live casino and online gaming solutions for operators worldwide. The company specializes in live dealer games and integrated casino systems for regulated markets.

International Game Technology PLC provides gaming technology across lotteries, digital gaming, sports betting, and gaming machines. The company serves operators and governments in regulated jurisdictions globally.

SOFTSWISS is an iGaming software provider offering online casino and sportsbook platforms. Its solutions support secure, scalable, and modular gambling operations for operators worldwide.

Flutter Entertainment plc is a global sports betting and gaming group operating online and retail brands across multiple regulated markets. The company focuses on technology-led growth and responsible gaming.

Betsson AB is an international gaming group operating online casino and sportsbook brands. The company emphasizes sustainable growth, customer experience, and regulated market expansion.

Key Players

- Playtech plc

- Evolution AB

- International Game Technology PLC

- Novomatic

- SOFTSWISS

- Flutter Entertainment plc

- Entain plc

- Bet365

- Evoke plc

- Betsson AB

Recent Developments

February 2026 - SOFTSWISS announced that it will outline its Latin America growth strategy at SBC Summit Rio 2026, reflecting its expanding footprint as regulated betting frameworks emerge in Brazil and other markets.

January 2026 - International Game Technology PLC confirmed it will showcase its global gaming, digital, and FinTech portfolio at ICE Barcelona 2026, featuring award-winning RISE55 and RISE32 gaming cabinets and other high-performance solutions

December 2025 - Flutter Entertainment plc announced the launch of FanDuel Predicts, a new nationwide product offering financial, economic and commodity prediction contracts alongside sports markets. The initiative expands Flutter’s product suite and is expected to drive customer engagement and future growth.

July 2025 - Evolution AB announced that it has entered into a multi-year global licensing agreement with Hasbro, a leading games, IP, and toy company, becoming Hasbro’s exclusive partner for developing and delivering online live casino and slot games based on MONOPOLY and other Hasbro Games titles.

Global Gambling Software Market Coverage

Software Type Insight and Forecast 2026 - 2035

- Sports Betting Software

- Casino Software

- Poker Software

- Lottery Software

- Bingo Software

- Others

Deployment Type Insight and Forecast 2026 - 2035

- Cloud-Based

- On-Premise

Device Insight and Forecast 2026 - 2035

- Mobile

- Desktop

Global Gambling Software Market by Region

- North America

- By Software Type

- By Deployment Type

- By Device

- By Country - U.S., Canada, Mexico

- Europe

- By Software Type

- By Deployment Type

- By Device

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Software Type

- By Deployment Type

- By Device

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Software Type

- By Deployment Type

- By Device

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Gambling Software Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Software Type

1.2.2. By

Deployment Type

1.2.3. By

Device

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Software Type

5.1.1. Sports Betting Software

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Casino Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Poker Software

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Lottery Software

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Bingo Software

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Others

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.2. By Deployment Type

5.2.1. Cloud-Based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. On-Premise

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Device

5.3.1. Mobile

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Desktop

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Software Type

6.2. By

Deployment Type

6.3. By

Device

6.3.1.

U.S. Market Estimate and Forecast

6.3.2.

Canada Market Estimate and Forecast

6.3.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Software Type

7.2. By

Deployment Type

7.3. By

Device

7.3.1.

Germany Market Estimate and Forecast

7.3.2.

France Market Estimate and Forecast

7.3.3.

U.K. Market Estimate and Forecast

7.3.4.

Italy Market Estimate and Forecast

7.3.5.

Spain Market Estimate and Forecast

7.3.6.

Russia Market Estimate and Forecast

7.3.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Software Type

8.2. By

Deployment Type

8.3. By

Device

8.3.1.

China Market Estimate and Forecast

8.3.2.

Japan Market Estimate and Forecast

8.3.3.

India Market Estimate and Forecast

8.3.4.

South Korea Market Estimate and Forecast

8.3.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Software Type

9.2. By

Deployment Type

9.3. By

Device

9.3.1.

Brazil Market Estimate and Forecast

9.3.2.

Saudi Arabia Market Estimate and Forecast

9.3.3.

South Africa Market Estimate and Forecast

9.3.4.

U.A.E. Market Estimate and Forecast

9.3.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Playtech plc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Evolution AB

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

International Game Technology PLC

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Novomatic

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

SOFTSWISS

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Flutter Entertainment plc

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Entain plc

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Bet365

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Evoke plc

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Betsson AB

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Gambling Software Market