Li-Fi Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (LEDs, Photodetectors / Optical Sensors, Microcontrollers (MCU), LED Drivers / Transmitters, Receivers, Software, Others), by Transmission Type (Unidirectional, Bidirectional), by Networking Type (Point-to-Point, Point-to-Multipoint), by Application (Indoor Networking, Location-Based Services (LBS), Smart Lighting, Automotive Communication, In-Flight / Aircraft Communication, Underwater Communication, Disaster & Emergency Communication, Others), by End User (Residential, Commercial, Industrial)

| Status : Published | Published On : Mar, 2026 | Report Code : VRICT5222 | Industry : ICT & Media | Available Format :

|

Page : 190 |

Li-Fi Market Overview

The Li-Fi (Light Fidelity) market which was valued at approximately USD 1.6 billion in 2025 and is estimated to reach around USD 2.3 billion in 2026, is projected to reach close to USD 31.8 billion by 2035, expanding at a CAGR of about 33.6% during the forecast period from 2026 to 2035.

The market is gaining strong momentum in 2025 as global digital activity reaches unprecedented levels and existing wireless networks face mounting capacity constraints. Globally, an estimated 6 billion people—about three-quarters of the world’s population—are using the Internet in 2025, up from 5.8 billion in 2024, according to official data from the International Telecommunication Union (ITU). This rapid expansion of connected users is intensifying demand for faster, more secure, and spectrum-efficient wireless communication technologies.

Li-Fi addresses this challenge by transmitting data through visible light, leveraging the vast, unlicensed optical spectrum rather than congested radio frequencies. By integrating communication directly into LED lighting infrastructure, Li-Fi enables high-speed, low-latency, and interference-free connectivity—particularly valuable in dense indoor environments, industrial facilities, and mission-critical settings where reliability and security are non-negotiable. Unlike traditional wireless signals, light-based communication remains physically contained, significantly enhancing data protection. As governments and enterprises accelerate investments in broadband access, smart buildings, and energy-efficient lighting, Li-Fi is emerging as a powerful complementary technology that expands network capacity while reducing pressure on RF spectrum. In 2025, this convergence of global connectivity growth and infrastructure readiness is positioning Li-Fi as a strategic enabler of the next phase of digital transformation.

Li Fi Market Dynamics

Market Trends

A key trend in 2026 for wireless communication is the increasing adoption of Light Fidelity (Li‑Fi) as a complementary connectivity layer to existing broadband networks. Unlike traditional Wi‑Fi that relies on radio frequencies, Li‑Fi transmits data via visible light from LEDs, enabling ultra‑fast, secure, and interference‑free communication, especially in high‑density environments like offices, healthcare facilities, and transport hubs. Governments worldwide are prioritizing digital infrastructure upgrades, reflected in India’s broadband subscriber base surpassing 100 crore (1 billion) in late 2025, signaling robust demand for faster and more reliable network solutions. As broadband penetration grows, technologies like Li‑Fi are emerging as trendsetters by leveraging existing LED lighting for data transmission, opening new channels for connectivity alongside 4G/5G networks that reached over 85% population coverage in 2025. This trend aligns with smart city and digital inclusion agendas targeting resilient, future‑ready urban ecosystems.

Growth Drivers

One major driver for the LiFi market is the explosive growth in Internet and broadband adoption driven by government-led digital initiatives. In India alone, broadband connections grew from 6.1 crore in 2014 to nearly 99.56 crore in 2025, expanding by over 1,500% and demonstrating massive demand for high-speed data delivery. This rapid expansion of broadband infrastructure drives demand for next-generation communication technologies like LiFi, which can deliver higher data rates, low latency, and improved network security. Rising digital traffic, with average monthly wireless data usage exceeding 24 GB per user, further underscores the need for high-capacity alternatives to complement existing WiFi and 5G networks. In addition, the growing focus on remote work, online education, telemedicine, and digital government services is increasing pressure on networks to perform reliably in both urban and rural areas. LiFi thus emerges as a timely solution for enterprises and smart infrastructure projects needing ultra-reliable connectivity, while also supporting IoT expansion and smart city initiatives.

Market Restraints / Challenges

A significant challenge for the LiFi market is the lack of global standardization and widespread device compatibility, which can slow largescale adoption. While LiFi technologies show promise for ultrafast data transmission, there is currently no universally adopted regulatory framework or standardized protocol across nations and industries. This fragmentation means that multiple proprietary solutions exist, leading to compatibility issues between LiFi access points and enduser devices. Without interoperable standards, integration with existing network infrastructure and smooth crossvendor deployment remains difficult, increasing both deployment complexity and cost. Moreover, most consumer devices today — such as smartphones, laptops, and tablets — do not natively support LiFi receivers, requiring additional hardware or aftermarket adapters to enable connectivity. These limitations make it challenging for enterprises to justify replacing or augmenting existing WiFi networks with LiFi, delaying widespread commercial adoption. Efforts toward standardization and integration will be critical to overcome this barrier and unlock broader ecosystem potential.

Market Opportunities

The LiFi market presents a significant opportunity in the integration of smart city infrastructure and IoT networks. As urban areas adopt digitalized infrastructure, LED lighting systems are increasingly deployed in public spaces, transport hubs, and commercial buildings. Retrofitting these LEDs with LiFi transmitters enables dual functionality—lighting and high-speed data transmission—without major additional infrastructure costs. LiFi’s inherent resistance to electromagnetic interference makes it ideal for sensitive environments such as hospitals, manufacturing units, and public transport, where traditional RF-based communication may be limited. With the rapid rise of connected devices and IoT applications, LiFi offers secure, low-latency, and high-capacity wireless networks. By enabling seamless integration into enterprise and urban systems, LiFi can play a pivotal role in building future-ready smart cities and digital ecosystems, creating new avenues for adoption across industries and public services.

Global Li-Fi Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.6 Billion |

|

Revenue Forecast in 2035 |

USD 31.8 Billion |

|

Growth Rate |

33.6% |

|

Segments Covered in the Report |

Component, Transmission Type, Application, End User, |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Fsona Networks Corporation, General Electric Company, LG Innotek, Lucibel, LVX System, Oledcomm, Koninklijke Philips N.V, pureLi-Fi, Sunpartner Technologies, Signify Holding, Velmenni, Wipro Limited |

|

Customization |

Available upon request |

Li Fi Market Segmentation

By Component

LEDs (LightEmitting Diodes) represent the largest category, with a market share of about 35% in 2025, as they serve both illumination and data transmission functions. Every LiFi system relies on LEDs to modulate visible light for transmitting digital information while simultaneously lighting spaces, making them indispensable for indoor, commercial, and industrial applications. Their high energy efficiency, long lifespan, and cost-effectiveness have encouraged widespread deployment in smart buildings, public infrastructure, and urban networks. Globally, governments are integrating LED-based smart lighting in smart cities and energy conservation initiatives, further promoting adoption. As the backbone of LiFi hardware, LEDs maintain a dominant market share due to their dual functionality, versatility, and compatibility with emerging wireless and IoT solutions across industries worldwide.

Photodetectors and optical sensors are currently the fastest-growing category with a CAGR of 33.8% during the forecast period. Since they are essential for receiving and converting modulated light signals into electrical data. As LiFi systems evolve to support higher speeds, longer distances, and complex network topologies, advanced photodetectors with improved sensitivity and signal-to-noise performance are increasingly required. The growth is fueled by rising deployments in industrial automation, smart offices, healthcare, and IoT-connected devices, where reliable data reception is critical. With increasing focus on high-speed optical communication infrastructure worldwide, photodetectors are experiencing accelerated innovation and demand. Their role in enabling robust, low-latency, and interference-free LiFi networks positions this component as the fastest-growing segment in the market.

By Transmission Type

In the LiFi market, unidirectional transmission currently represents the largest category with a market share of 65% in 2025, as it is widely adopted in applications where data primarily flows from the transmitter to the receiver, such as in indoor lighting, signage, and public displays. This mode leverages LEDs to send high-speed data to photodetectors without requiring a return channel, simplifying system design and reducing costs. Its broad deployment is favored in commercial buildings, retail spaces, and industrial facilities, where lighting infrastructure can double as a communication medium. Unidirectional systems are easier to implement at scale and support high-speed data streaming, making them the most dominant choice globally. Their reliability, cost-effectiveness, and compatibility with existing LED lighting infrastructure ensure continued market leadership in the LiFi ecosystem.

Bidirectional LiFi transmission is the fastest-growing category during the forecast period because it enables two-way communication, essential for interactive applications, IoT integration, and real-time data exchange. Unlike unidirectional systems, bidirectional setups allow devices to both send and receive data, supporting complex enterprise, industrial, and smart city use cases. The rise of remote work, IoT adoption, and smart infrastructure is fueling demand for bidirectional systems, which provide low-latency, secure, and interference-resistant networks. Advances in optical sensors, microcontrollers, and system integration are driving faster adoption. As organizations and governments increasingly deploy intelligent lighting and IoT-enabled environments, bidirectional LiFi solutions are becoming critical for creating robust, interactive, and scalable digital communication networks worldwide.

By Application

Indoor networking is the largest application category in the global LiFi market. This category holds an estimated market share of 35% in 2026, driven by widespread adoption in offices, hospitals, universities, and industrial complexes. LiFi leverages LED lighting to transmit high-speed data while minimizing electromagnetic interference, making it highly suitable for environments sensitive to radio frequencies. Integration with IoT devices, enterprise networks, and smart building infrastructure ensures scalable, cost-effective, and secure deployments. The ability to deliver low-latency, reliable connectivity across multiple sectors reinforces its dominance. With the growing trend of smart buildings and connected enterprises, indoor networking remains the backbone of LiFi applications, providing the foundation for other services and future expansions across the global market.

Location-based services (LBS) are the fastest-growing application category in the LiFi market, projected to expand at a CAGR of 33.9% from 2026 to 2035. LiFi enables centimeter-level indoor positioning, which is crucial for airports, shopping malls, hospitals, and museums, where GPS is less effective. This high precision supports real-time navigation, targeted marketing, and interactive data delivery, enhancing user experience and operational efficiency. The growing deployment of IoT-enabled smart environments and connected public spaces globally is fueling demand. LiFi’s high-speed, low-latency, and interference-resistant capabilities make it ideal for LBS, positioning it as the fastest-growing segment with strong adoption potential across commercial, industrial, and public sector applications worldwide.

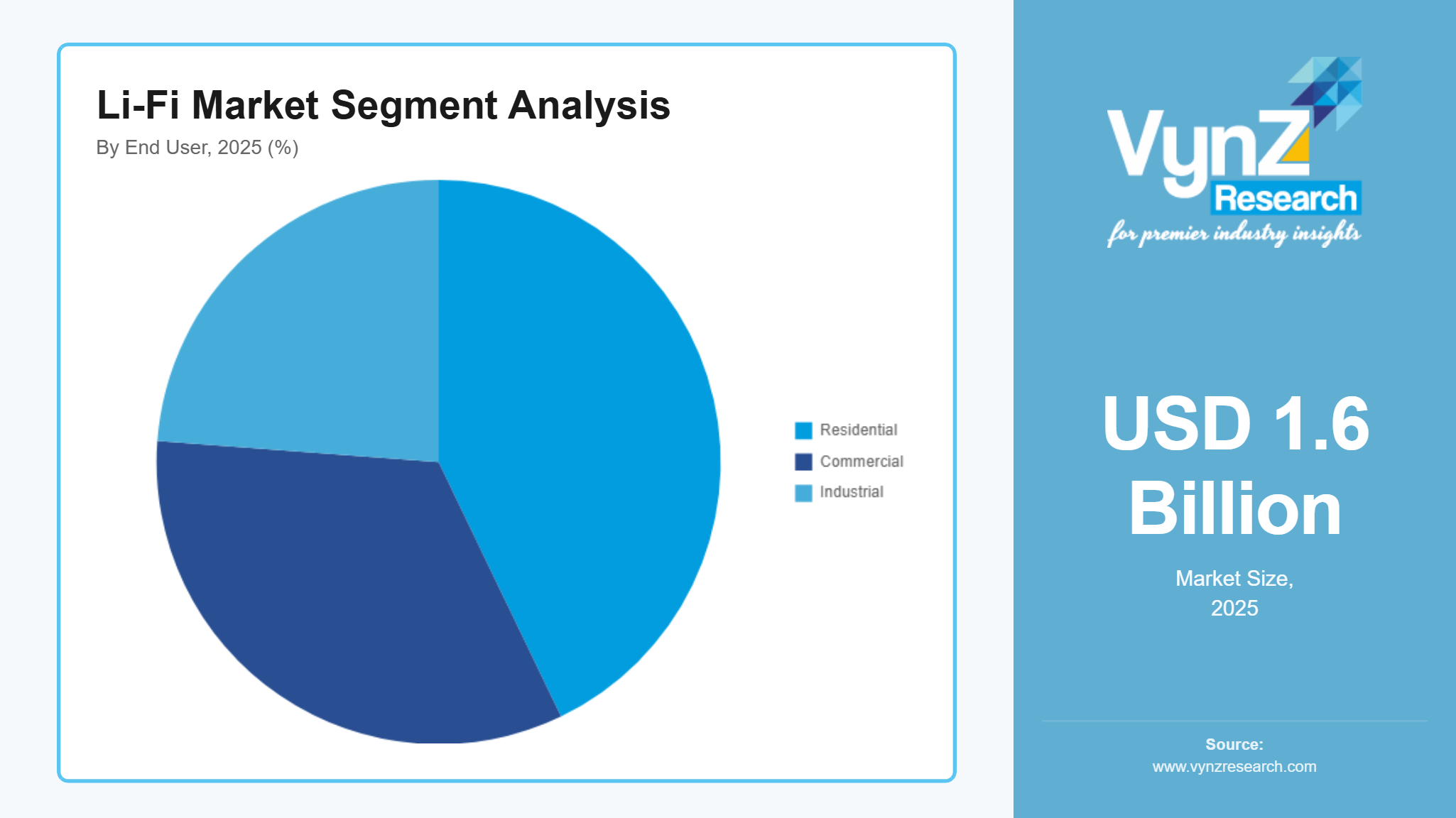

By End User

Commercial end-users represent the largest segment in the global LiFi market, holding an estimated market share of about 45% in 2026. This category includes offices, educational institutions, hospitals, retail spaces, and public facilities where high-speed, secure, and low-latency wireless communication is critical. LiFi leverages LED lighting to transmit data while minimizing electromagnetic interference, making it ideal for environments sensitive to radio frequencies. The integration of smart lighting, IoT devices, and enterprise networks further reinforces adoption. Growing demand for connected workplaces, digital campuses, and smart public infrastructure ensures the commercial sector remains the primary driver of LiFi deployments globally, providing consistent and scalable opportunities for manufacturers and solution providers.

Residential users are the fastest-growing segment in the LiFi market, projected to grow at a CAGR of 33.7% from 2026 to 2035. Increasing adoption of smart homes, IoT-enabled devices, and home automation systems is driving demand for high-speed, secure, and interference-free wireless communication. LiFi enables ultra-fast data transmission using LED lighting while offering improved network security compared to traditional Wi-Fi, which appeals to homeowners concerned about privacy. Growth is further fueled by rising consumer awareness of smart home technologies and connected living solutions, making residential users a key emerging segment in the global LiFi market, with significant potential for future expansion and new product innovations.

Regional Insights

Asia Pacific

The Asia Pacific LiFi market is poised for unprecedented growth, driven by rapid urbanization, smart city initiatives, and surging IoT adoption. Nations like China, Japan, South Korea, and India are investing aggressively in next-generation digital infrastructure, integrating LiFi into commercial, industrial, and public environments. The region’s appetite for high-speed, secure, and interference-free connectivity positions it as the fastest-growing hub for innovative wireless solutions. With governments and enterprises prioritizing smart lighting, industrial automation, and connected public spaces, Asia Pacific is set to lead the market in expansion, offering transformative opportunities for solution providers seeking to capitalize on emerging technology adoption and the evolving digital economy.

Europe

Europe’s LiFi market reflects steady, strategic growth, anchored in strong research capabilities, regulatory support, and sustainability-driven initiatives. Countries such as Germany, France, and the UK are integrating LiFi into connected transport, industrial automation, and smart building infrastructures, blending high-speed data transmission with energy-efficient lighting solutions. European enterprises value the technology for its reliability, security, and compliance with regulatory standards, creating long-term, sustainable deployments. While growth is measured compared to Asia Pacific, Europe’s focus on precision, interoperability, and innovative integration positions it as a critical market for both commercial and public-sector adoption, offering significant opportunities for LiFi solution providers seeking high-value, enterprise-grade deployments.

North America

North America continues to hold the largest share of the global LiFi market, driven by mature technological infrastructure, early adoption, and enterprise demand for secure high-speed networks. The United States and Canada are at the forefront of deploying LiFi in healthcare, smart buildings, educational campuses, and industrial complexes, leveraging advanced LED-based systems. Strong R&D ecosystems, robust public-private collaborations, and a focus on cutting-edge wireless and IoT integration reinforce the region’s dominance. Enterprises in North America are prioritizing ultra-reliable, low-latency, and interference-resistant communication, making it the go-to region for LiFi adoption and innovation, securing its position as the largest and most influential market globally.

Rest of the World

The rest of the world, encompassing Latin America, the Middle East, and Africa, is emerging as a promising frontier for LiFi technology. While current adoption is modest, governments and enterprises are increasingly exploring high-speed, interference-free connectivity for public infrastructure, healthcare, education, and industrial applications. In Latin America, countries such as Brazil and Mexico are embracing digital transformation to modernize smart buildings and connected campuses. The Middle East is investing in LiFi integration for smart cities, airports, and commercial hubs, aligned with ambitious urban development visions. In Africa, pilot deployments are demonstrating the potential for LiFi in educational and urban connectivity solutions, despite infrastructure challenges. As digital ecosystems mature, this region represents a high-growth opportunity for solution providers seeking early-mover advantages and scalable innovation in emerging markets.

Competitive Landscape / Company Insights

The global LiFi market is moderately fragmented, with a mix of established technology leaders and emerging startups driving innovation across hardware, software, and integrated solutions. Companies are competing through strategic partnerships, product development, and pilot deployments in commercial, industrial, and public sectors. Key players focus on developing high-speed, secure, and low-latency LiFi systems, while differentiating through enhanced LED modules, photodetectors, microcontrollers, and software platforms. Innovation is accelerated by collaborations with research institutions, smart city programs, and IoT initiatives, enabling the commercialization of scalable and enterprise-ready solutions. While North America and Europe currently host leading market incumbents, the Asia Pacific is emerging as a competitive hub due to the rapid adoption of smart infrastructure and digital transformation projects. As the market evolves, companies capable of integrating LiFi into smart buildings, industrial automation, and connected urban ecosystems will capture a significant share and shape the next generation of wireless communication solutions.

Mini Profiles

pureLiFi is the global leader in LiFi technology, creating high-speed wireless data solutions using light for enterprise, defense, and ISP applications.

Signify Holding is the world leader in connected LED lighting, integrating LiFi into smart buildings and IoT systems to deliver secure, high-speed wireless communication. LG Innotek a South Korean electronics manufacturer, supplies optical and communication components supporting LiFi devices and advanced optical transmission technologies.

Oledcomm is a French LiFi company offering secure, interference-free optical communication systems for defense, enterprise, and industrial applications.

Velmenni develops LiFi mesh networks and optical wireless systems for high-speed data transfer in environments unsuitable for RF or wired networks.

Key Players

- Fsona

- Networks Corporation

- General Electric Company

- LG

- Innotek

- Lucibel

- LVX System

- Oledcomm

- Koninklijke Philips N.V

- pureLi-Fi

- Sunpartner Technologies

- Signify Holding

- Velmenni

- Wipro Limited

Recent Developments

January 2026 - pureLiFi announced at CES 2026 the North American debut of its nextgen LiFi solutions the Bridge XC system and the LiFi Cube Mini — aimed at delivering highspeed broadband connectivity via light for consumer and enterprise use, showcasing the company’s enhanced LiFi product portfolio.

October 2025 - Signify Holding and Intelligent Waves announced the launch of a new joint venture called IllumiConn, designed to advance secure optical wireless communications for defense and government applications. The collaboration combines Signify’s LiFi and freespace optics expertise with Intelligent Waves’ cybersecurity and network engineering capabilities.

June 2025 - Signify announced that its Trulifi 6004 LiFi system became the first in the world to meet the U.S. NIST’s FIPS 1403 cryptographic validation, significantly enhancing secure LiFi deployment in offices, healthcare, and highsecurity environments.

Global Li-Fi Market Coverage

Component Insight and Forecast 2026 - 2035

- LEDs

- Photodetectors / Optical Sensors

- Microcontrollers (MCU)

- LED Drivers / Transmitters

- Receivers

- Software

- Others

Transmission Type Insight and Forecast 2026 - 2035

- Unidirectional

- Bidirectional

Networking Type Insight and Forecast 2026 - 2035

- Point-to-Point

- Point-to-Multipoint

Application Insight and Forecast 2026 - 2035

- Indoor Networking

- Location-Based Services (LBS)

- Smart Lighting

- Automotive Communication

- In-Flight / Aircraft Communication

- Underwater Communication

- Disaster & Emergency Communication

- Others

End User Insight and Forecast 2026 - 2035

- Residential

- Commercial

- Industrial

Global Li-Fi Market by Region

- North America

- By Component

- By Transmission Type

- By Networking Type

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Transmission Type

- By Networking Type

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Transmission Type

- By Networking Type

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Transmission Type

- By Networking Type

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Li-Fi Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Transmission Type

1.2.3. By

Networking Type

1.2.4. By

Application

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. LEDs

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Photodetectors / Optical Sensors

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Microcontrollers (MCU)

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. LED Drivers / Transmitters

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Receivers

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Software

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Others

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.2. By Transmission Type

5.2.1. Unidirectional

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Bidirectional

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Networking Type

5.3.1. Point-to-Point

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Point-to-Multipoint

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Indoor Networking

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Location-Based Services (LBS)

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Smart Lighting

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Automotive Communication

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. In-Flight / Aircraft Communication

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Underwater Communication

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Disaster & Emergency Communication

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

5.4.8. Others

5.4.8.1. Market Definition

5.4.8.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Residential

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Commercial

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Industrial

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Transmission Type

6.3. By

Networking Type

6.4. By

Application

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Transmission Type

7.3. By

Networking Type

7.4. By

Application

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Transmission Type

8.3. By

Networking Type

8.4. By

Application

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Transmission Type

9.3. By

Networking Type

9.4. By

Application

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Fsona Networks Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

General Electric Company

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

LG Innotek

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Lucibel

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

LVX System

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Oledcomm

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Koninklijke Philips N.V

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

pureLi-Fi

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Sunpartner Technologies

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Signify Holding

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Velmenni

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Wipro Limited

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Li-Fi Market