India Artificial Intelligence Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Technology (Machine Learning, Natural Language Processing (NLP), Computer Vision, Robotics & Automation, Expert Systems, Generative AI), by Deployment Mode (On-Premises, Cloud), by Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), by End User Industry (Healthcare & Life Sciences, BFSI, IT & ITES, Retail & Consumer Goods, Manufacturing, Automotive & Transportation, Government & Public Sector, Telecom, Energy & Utilities, Others)

| Status : Published | Published On : Mar, 2026 | Report Code : VRICT5224 | Industry : ICT & Media | Available Format : | Page : 125 |

India Artificial Intelligence Market Overview

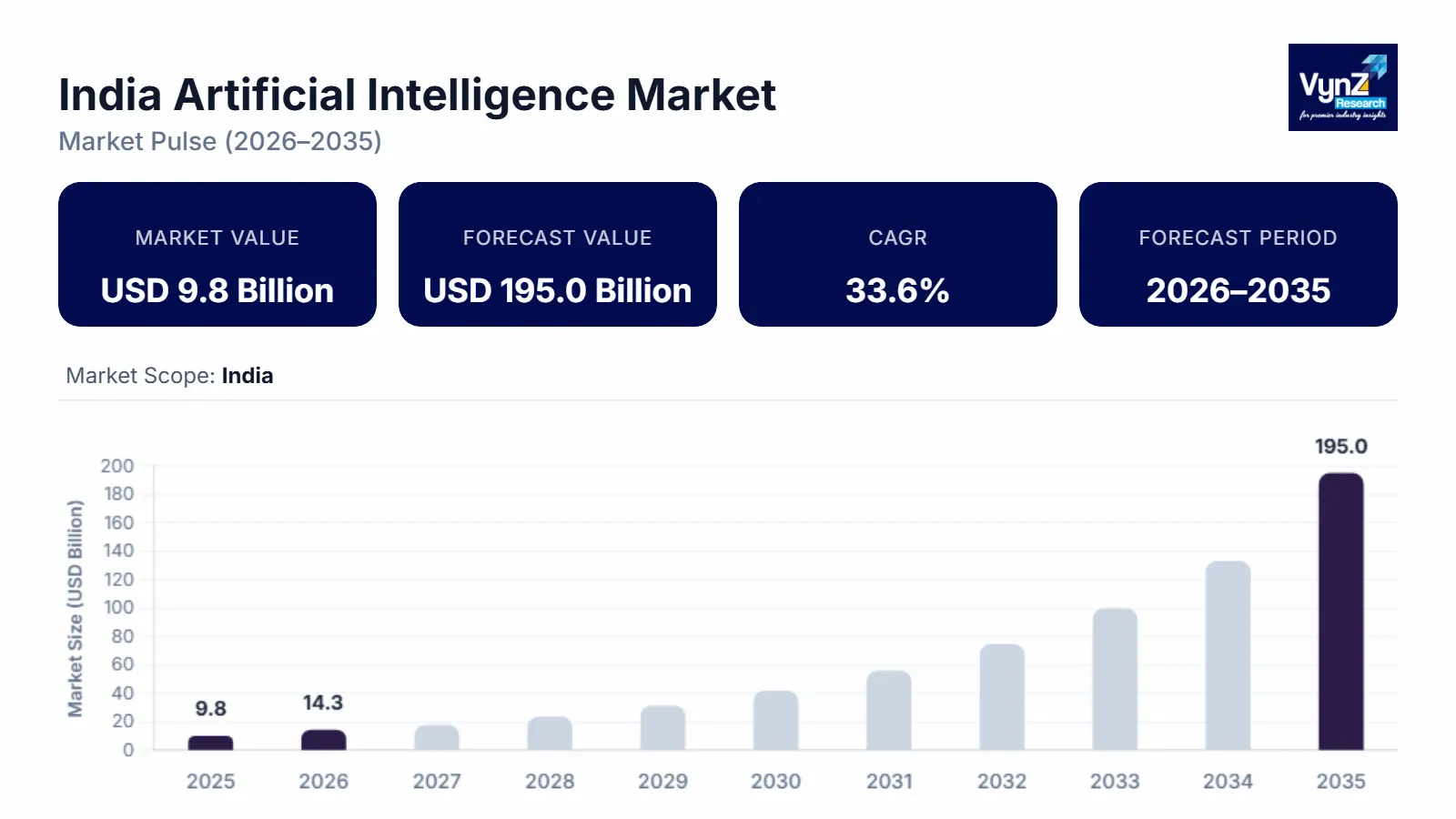

The India artificial intelligence market which was valued at approximately USD 9.8 billion in 2025 and is estimated to reach around USD 14.3 billion in 2026, is projected to reach close to USD 195.0 billion by 2035, expanding at a CAGR of about 33.6% during the forecast period from 2026 to 2035.

The India artificial intelligence market is driven by strong government support, rapid digital transformation, and increasing adoption of advanced technologies across multiple industries. Government initiatives such as Digital India, make in India, and the National Strategy for Artificial Intelligence are encouraging investments in AI research, innovation, and infrastructure development. The growing use of AI in sectors such as healthcare, banking, retail, manufacturing, and telecommunications is significantly contributing to market expansion, as organizations aim to improve efficiency, automation, and decision-making capabilities. The rising demand for data analytics, cloud computing, and machine learning solutions is further accelerating the adoption of AI technologies in the country. In addition, the increasing number of startups and technology companies focusing on AI-based solutions is strengthening the innovation ecosystem in India. The expansion of 5G networks and the availability of large volumes of digital data are also supporting the growth of AI applications. Furthermore, increasing investments from global technology companies and strong growth in the IT services sector are creating favorable conditions for the development of the artificial intelligence market in India.

India Artificial Intelligence Market Dynamics

Market Trends

The rise of generative AI adoption across industries is one of the most significant trends driving the growth of the India artificial intelligence market. Businesses are increasingly using generative AI tools to automate content creation, software development, customer interaction, and data analysis, which helps improve productivity and reduce operational costs. IT services companies in India are integrating generative AI into coding, testing, and technical support processes to enhance efficiency and deliver faster solutions to global clients. In the banking and financial sector, generative AI is being used for intelligent chatbots, document processing, and personalized financial recommendations. The Government of India has significantly accelerated generative AI adoption through the IndiaAI Mission, under which more than ₹10,300 crore has been allocated to build national AI infrastructure, support startups, and develop indigenous AI models. The mission focuses on providing large-scale computing power, including over 38,000 GPUs made available to researchers, startups, and enterprises to enable development of advanced AI and generative AI applications across industries. Media, marketing, and e-commerce companies are adopting generative AI for automated content generation, advertising optimization, and customer engagement. In addition, startups in India are developing generative AI platforms for language translation, voice recognition, and regional language applications, increasing accessibility across diverse user groups. The growing availability of cloud computing and large datasets is making it easier for organizations to deploy generative AI solutions at scale.

Growth Drivers

The expansion of AI in healthcare and medical research is a major growth driver of the India artificial intelligence market, as hospitals, research institutions, and healthcare technology companies are increasingly adopting advanced AI-based solutions to improve patient care and operational efficiency. Artificial intelligence is widely used in medical imaging, diagnostics, and disease prediction, helping doctors detect conditions such as cancer, cardiovascular disorders, and neurological diseases at an early stage. The IndiaAI–National Cancer Grid (NCG) Cancer AI & Technology Challenge (CATCH) program includes direct government-supported funding for AI healthcare projects, where selected proposals receive pilot grants of up to ₹50 lakh per project to develop and test AI solutions in cancer screening, diagnostics, treatment support, and hospital operations. AI-powered tools are also being used for patient data management, remote monitoring, and telemedicine, which is especially important in India due to the large population and limited access to healthcare facilities in rural areas. In medical research, AI is accelerating drug discovery, clinical trials, and genomic analysis by processing large volumes of data in a shorter time. Healthcare startups in India are developing AI platforms for symptom checking, virtual health assistants, and personalized treatment recommendations. The growing adoption of electronic health records and digital health platforms is further supporting the use of AI technologies. In addition, government initiatives promoting digital healthcare infrastructure are encouraging hospitals and research centers to invest in artificial intelligence solutions.

Market Restraints / Challenges

The shortage of skilled AI professionals is one of the major challenges affecting the growth of the India artificial intelligence market, as the demand for experts in machine learning, data science, natural language processing, and robotics is increasing rapidly across industries. Many organizations in India are facing difficulties in hiring qualified professionals who have practical experience in developing and deploying advanced AI solutions. Although the country has a large IT workforce, only a small percentage of professionals have specialized skills required for artificial intelligence and deep learning technologies. This skill gap makes AI implementation slower and increases the cost of hiring talent, especially for startups and small enterprises. In addition, experienced AI professionals are often recruited by global technology companies, leading to strong competition for talent in the domestic market. Limited availability of advanced AI training programs and industry-focused education also contributes to the shortage of skilled workers. Companies are therefore required to invest heavily in employee training and upskilling programs to support AI adoption.

Market Opportunities

The rising demand for AI in healthcare and telemedicine is creating significant growth opportunities in the India artificial intelligence market, as the country is focusing on improving healthcare access, efficiency, and quality of services. Artificial intelligence is increasingly used in telemedicine platforms for remote consultations, symptom analysis, and patient monitoring, which helps provide medical support to people living in rural and remote areas. AI-powered diagnostic tools are enabling faster detection of diseases through medical imaging, predictive analytics, and automated report generation, reducing the workload on healthcare professionals. The growing adoption of digital health records and online healthcare services is also supporting the integration of AI technologies in hospitals and clinics. In addition, telemedicine has gained strong importance due to the need for cost-effective and accessible healthcare solutions for a large population. Healthcare startups in India are developing AI-based virtual assistants, chatbots, and personalized treatment platforms, creating new business opportunities. Government initiatives promoting digital health infrastructure and e-health services are further encouraging the use of AI in the healthcare sector.

India Artificial Intelligence Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 9.8 Billion |

|

Revenue Forecast in 2035 |

USD 195.0 Billion |

|

Growth Rate |

33.6% |

|

Segments Covered in the Report |

Component, Technology, Deployment Mode, Enterprise Size, End User Industry |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North, South, West, East |

|

Key Companies |

Tata Consultancy Services Limited, Infosys Limited, Wipro Limited, HCL Technologies Limited, Tech Mahindra Limited, Persistent Systems Limited, Tata Elxsi Limited, Fractal Analytics Inc., Affle (India) Limited, Zensar Technologies Limited, Microsoft Corporation, International Business Machines Corporation |

|

Customization |

Available upon request |

India Artificial Intelligence Market Segmentation

By Component

Software is the largest category with a market share of about 40% in 2025, owing to the extensive use of AI software platforms, machine learning frameworks, and analytics tools across multiple industries in India. Most organizations adopt AI through software solutions because they are easier to deploy using cloud infrastructure without requiring heavy hardware investment. IT services, banking, healthcare, and retail sectors widely use AI software for automation, customer analytics, and decision support systems. The strong presence of India’s IT industry also supports high demand for AI development platforms and enterprise software. Continuous updates, scalability, and subscription-based models further increase software adoption. The rapid growth of SaaS and AI-as-a-Service platforms strengthens this segment. Large enterprises prefer software-based AI solutions for flexibility and cost efficiency.

Services is the fastest-growing category with a CAGR of 33.8% during the forecast period, driven by the increasing need for AI consulting, system integration, training, and managed services in India. Many organizations lack in-house AI expertise, which creates strong demand for professional service providers. Companies are seeking support for AI implementation, customization, and maintenance to ensure smooth deployment. The rise of cloud-based AI solutions is also increasing the need for integration and support services. Startups and SMEs are especially dependent on external service providers for AI adoption. The expansion of digital transformation projects across industries further boosts service demand. Global technology firms and Indian IT companies are offering AI services to domestic and international clients.

By Technology

Machine Learning is the largest category with a market share of about 30% in 2025, as it forms the core technology behind most artificial intelligence applications used in India. Machine learning is widely used in banking, healthcare, retail, telecom, and manufacturing for predictive analytics, recommendation systems, and fraud detection. Organizations prefer machine learning because it can process large volumes of data and improve performance over time. The availability of big data and cloud computing platforms supports the widespread adoption of this technology. Indian IT companies heavily use machine learning in automation and data-driven services. It is also the foundation for advanced technologies such as generative AI and computer vision. Continuous research and development in ML algorithms further strengthen its dominance.

Generative AI is the fastest-growing category with a CAGR of 33.9% during the forecast period, driven by the rapid adoption of AI tools for content generation, coding, chatbots, and business automation. Companies in India are increasingly using generative AI to improve productivity and reduce operational costs. IT services firms are integrating generative AI into software development and customer support processes. Media, marketing, and e-commerce companies use it for automated content creation and personalization. The availability of large language models and cloud-based AI platforms makes adoption easier. Startups in India are also developing generative AI solutions for regional languages and voice applications.

By Deployment Mode

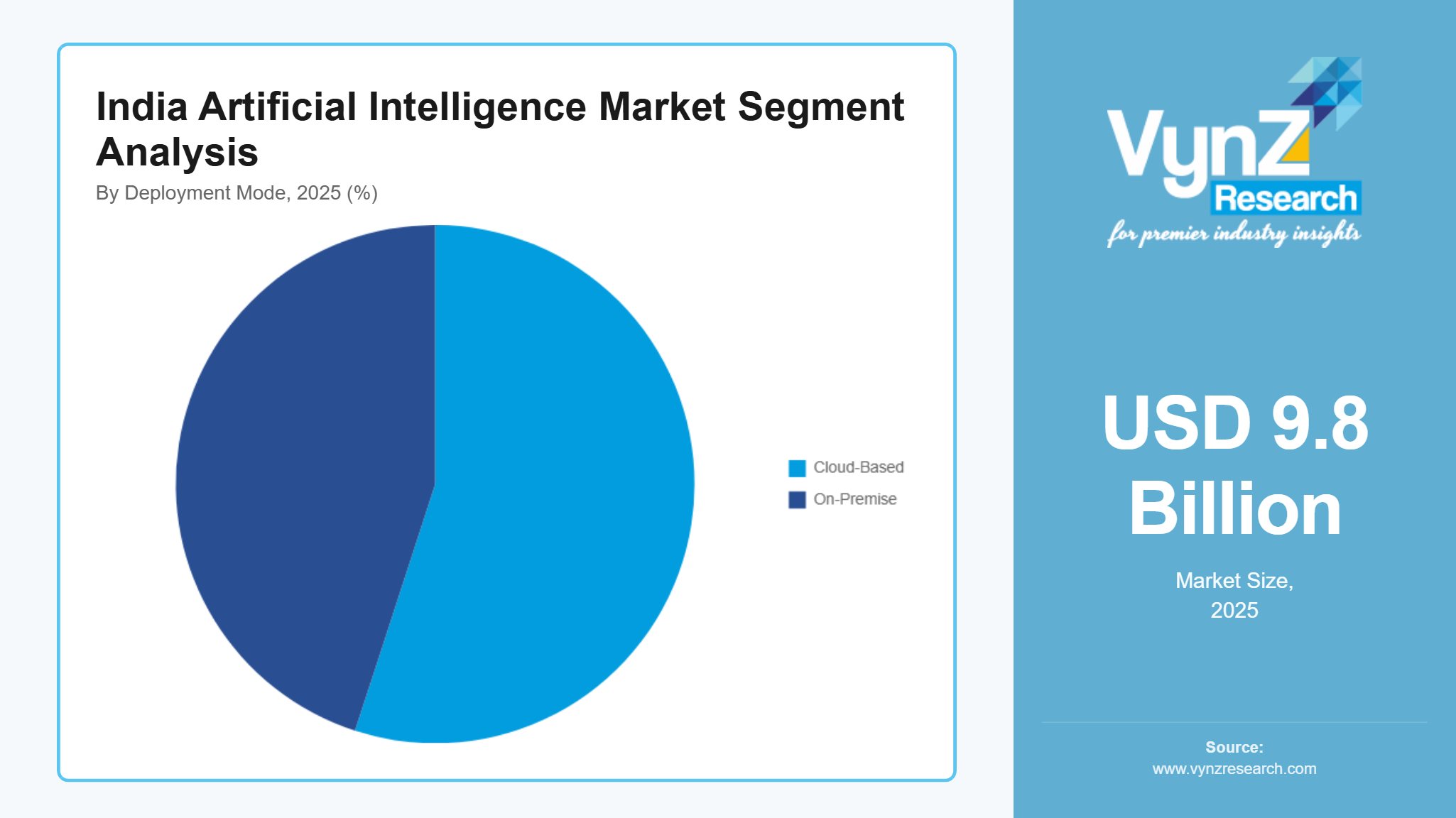

Cloud is the largest category with a market share of about 65% in 2025 and is also the fastest-growing category with a CAGR of 40.1% during the forecast period, because most organizations in India prefer cloud deployment for artificial intelligence due to lower infrastructure cost, high scalability, and faster implementation. Cloud platforms allow companies to access AI tools without investing in expensive hardware, making them highly suitable for both large enterprises and SMEs. IT companies, startups, and digital businesses widely use cloud-based AI for analytics, automation, and application development. The rapid expansion of public cloud providers and data centers in India is further supporting adoption. Cloud deployment enables easy updates, remote access, and integration with big data and IoT platforms. Government digital initiatives and smart infrastructure projects are also increasing the use of cloud-based AI systems. In addition, the growing popularity of AI-as-a-Service and SaaS models is encouraging companies to shift from on-premises systems to cloud platforms.

By Enterprise Size

Large Enterprises is the largest category with a market share of about 60% in 2025, owing to their strong financial capability and high investment in advanced technologies such as artificial intelligence, big data, and automation. Large organizations in banking, IT, telecom, and manufacturing are early adopters of AI to improve efficiency and customer experience. They have access to large datasets, which makes AI implementation more effective. These companies also invest in in-house AI teams and research programs. Digital transformation strategies in large enterprises strongly support AI adoption. Integration of AI with existing enterprise systems further increases demand. Global companies operating in India also contribute to high usage.

Small & Medium Enterprises (SMEs) is the fastest-growing category during the forecast period, driven by the increasing availability of affordable cloud-based AI solutions in India. SMEs are adopting AI to improve productivity, customer service, and marketing efficiency without heavy investment. The growth of SaaS platforms allows smaller companies to access advanced AI tools easily. Government programs supporting digitalization of small businesses are also encouraging adoption. Startups are increasingly using AI for automation and data analysis. Competitive pressure is forcing SMEs to adopt new technologies to remain efficient. The expansion of fintech, e-commerce, and online services further supports growth.

By End User Industry

IT & ITES is the largest category with a market share of about 25% in 2025, because India has a strong IT services industry that heavily uses artificial intelligence for automation, analytics, and software development. IT companies integrate AI into customer support, cybersecurity, cloud services, and enterprise applications. The presence of major global technology firms and outsourcing companies increases demand for AI solutions. Continuous innovation in software development also supports AI adoption. IT service providers use AI to deliver faster and more efficient solutions to clients worldwide. The availability of skilled developers in the IT sector further strengthens this segment. Digital transformation projects across industries also rely on IT companies.

Healthcare & Life Sciences is the fastest-growing category during the forecast period, driven by the increasing use of AI in diagnostics, medical imaging, telemedicine, and drug research in India. Hospitals and health-tech companies are adopting AI to improve patient care and reduce operational costs. The need for better healthcare access in rural areas is increasing the use of AI-based telemedicine platforms. AI helps in faster disease detection and personalized treatment planning. Startups are developing AI tools for virtual health assistants and data analysis. Government focus on digital health infrastructure also supports adoption. Growing healthcare data is making AI more useful in research and clinical decision making.

Regional Insights

North

North holds a significant share in the India artificial intelligence market, supported by the strong presence of IT services, government institutions, and growing startup ecosystems in cities such as Delhi-NCR, Noida, Gurugram, and Chandigarh. The region benefits from high adoption of digital technologies across public sector projects, fintech companies, and enterprise software firms. Government departments and public sector organizations are increasingly using artificial intelligence for e-governance, surveillance, and smart city initiatives. The Government of India announced in the Union Budget 2025–26 an allocation of ₹500 crore for establishing a Centre of Excellence in Artificial Intelligence for Education, aimed at strengthening AI research, skill development, and innovation in India. The presence of major research institutes and engineering universities also supports AI talent development. Increasing investment in data centers and cloud infrastructure is strengthening regional capabilities. BFSI and telecom companies in the region are actively deploying AI for analytics and automation.

South

South is the largest and fastest-growing region in the India artificial intelligence market, driven by the strong concentration of IT companies, technology parks, and global capability centers in cities such as Bengaluru, Hyderabad, Chennai, and Pune. The region is considered the technology hub of India, with high adoption of artificial intelligence in software development, cloud computing, and data analytics services. Many global technology companies and Indian IT firms operate major R&D centers in this region, creating strong demand for AI solutions. Google announced an investment of about USD 15 billion over five years to build a large artificial intelligence hub in Visakhapatnam, India, which will include gigawatt-scale data center infrastructure, energy systems, and fiber-optic connectivity to support advanced AI computing. Startups focused on machine learning, robotics, and generative AI are rapidly growing in South India. The availability of skilled professionals and advanced digital infrastructure supports faster technology adoption. Increasing investment in smart manufacturing, healthcare technology, and fintech platforms is also driving demand. Government support for innovation and startup funding further accelerates regional growth.

West

West represents a major commercial and financial hub in the India artificial intelligence market, with strong adoption of AI in banking, financial services, manufacturing, and e-commerce industries. Cities such as Mumbai, Pune, and Ahmedabad are key centers for fintech, industrial automation, and enterprise technology solutions. Financial institutions in Mumbai are increasingly using AI for fraud detection, risk analysis, and customer analytics. The presence of large manufacturing clusters in Maharashtra and Gujarat is driving the use of AI in robotics, predictive maintenance, and supply chain optimization. The region also has a growing startup ecosystem focused on AI-based business solutions. Increasing investments in digital transformation by large enterprises are supporting market expansion. Cloud adoption among SMEs is also rising in this region.

East

East is witnessing gradual growth in the India artificial intelligence market, supported by increasing digitalization, government technology projects, and expansion of IT services in cities such as Kolkata, Bhubaneswar, and Patna. The region is slowly adopting artificial intelligence in education, healthcare, and public administration to improve efficiency and service delivery. Government initiatives promoting digital infrastructure and smart city development are creating new opportunities for AI deployment. The growth of startups and IT training institutes is helping build technical skills in the region. Industries such as mining, logistics, and agriculture are beginning to use AI for data analysis and automation. Although the level of adoption is lower compared to South and West India, investment in technology infrastructure is increasing. Expansion of internet connectivity and cloud services is also supporting growth.

Competitive Landscape / Company Insights

The India Artificial Intelligence Market is moderately fragmented, characterized by the presence of global technology companies, large Indian IT service providers, and a rapidly growing number of AI-focused startups offering specialized solutions across industries. Major companies such as Tata Consultancy Services Limited, Infosys Limited, Wipro Limited, and HCL Technologies Limited hold strong positions due to their extensive service portfolios, strong client base, and expertise in cloud computing, data analytics, and machine learning solutions. These companies provide AI consulting, system integration, and enterprise automation services to domestic as well as international clients, strengthening their market presence.

Global technology firms including International Business Machines Corporation, Microsoft Corporation, Google LLC, and Amazon Web Services, Inc. play a major role in the market by providing AI platforms, cloud infrastructure, and advanced machine learning tools widely used by enterprises in India. These companies benefit from strong R&D capabilities, continuous innovation, and large investments in data centers and AI research programs. At the same time, Indian startups such as Fractal Analytics Inc., Haptik, Mad Street Den, and Yellow.ai are gaining attention by developing AI-based solutions for customer service, computer vision, conversational AI, and analytics. Increasing collaboration between IT companies, startups, and government institutions is further strengthening the competitive environment, while continuous investment in generative AI, automation, and industry-specific AI applications is shaping the future of the artificial intelligence market in India.

Mini Profiles

Tata Consultancy Services Limited is one of the leading IT services and consulting companies in India, offering a wide range of artificial intelligence, machine learning, and data analytics solutions across industries. The company provides AI-driven platforms for automation, predictive analytics, and enterprise decision-making, serving sectors such as banking, healthcare, retail, and manufacturing.

Infosys Limited is a major global technology services firm with strong capabilities in artificial intelligence, cloud computing, and digital transformation. The company delivers AI-powered solutions through its automation and analytics platforms, helping organizations improve operational efficiency, customer experience, and business intelligence.

Wipro Limited is a prominent IT and consulting company providing advanced artificial intelligence and automation services to enterprises worldwide. Its AI offerings include cognitive computing, natural language processing, and robotic process automation, widely used in healthcare, finance, telecom, and energy sectors.

HCL Technologies Limited is a global technology company specializing in AI, cloud, and engineering services for large enterprises. The company develops AI-based solutions for predictive maintenance, cybersecurity, digital operations, and smart manufacturing, supporting clients in multiple industries.

Tech Mahindra Limited provides artificial intelligence and data analytics solutions focused on telecom, banking, healthcare, and smart city projects. The company uses AI for network automation, customer experience management, and intelligent business process services, strengthening its presence in digital transformation projects.

Key Players

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- HCL Technologies Limited

- Tech Mahindra Limited

- Persistent Systems Limited

- Tata Elxsi Limited

- Fractal Analytics Inc.

- Affle (India) Limited

- Zensar Technologies Limited

- Microsoft Corporation

- International Business Machines Corporation

Recent Developments

January 2026 – Tata Consultancy Services Limited announced the expansion of its artificial intelligence and cloud capabilities through new AI-driven enterprise solutions designed to support automation, predictive analytics, and digital transformation projects across banking, healthcare, and manufacturing sectors in India.

December 2025 – Infosys Limited introduced new generative AI and machine learning services under its digital innovation portfolio, aimed at helping enterprises improve customer experience, software development efficiency, and data-driven decision-making through advanced AI platforms.

October 2025 – Microsoft Corporation expanded its AI and cloud infrastructure in India by increasing data center capacity and launching new AI services on its cloud platform, supporting startups, government projects, and large enterprises adopting artificial intelligence solutions.

August 2025 – Wipro Limited launched enhanced AI-powered automation and cognitive computing solutions for telecom, financial services, and healthcare industries, focusing on improving operational efficiency and enabling intelligent business process management.

July 2025 – International Business Machines Corporation announced new collaborations with Indian enterprises and research institutions to develop AI-based analytics, cybersecurity, and hybrid cloud solutions, strengthening its presence in enterprise artificial intelligence deployments.

India Artificial Intelligence Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Technology Insight and Forecast 2026 - 2035

- Machine Learning

- Natural Language Processing (NLP)

- Computer Vision

- Robotics & Automation

- Expert Systems

- Generative AI

Deployment Mode Insight and Forecast 2026 - 2035

- On-Premises

- Cloud

Enterprise Size Insight and Forecast 2026 - 2035

- Large Enterprises

- Small & Medium Enterprises (SMEs)

End User Industry Insight and Forecast 2026 - 2035

- Healthcare & Life Sciences

- BFSI

- IT & ITES

- Retail & Consumer Goods

- Manufacturing

- Automotive & Transportation

- Government & Public Sector

- Telecom

- Energy & Utilities

- Others

India Artificial Intelligence Market by Region

- North

- By Component

- By Technology

- By Deployment Mode

- By Enterprise Size

- By End User Industry

- South

- By Component

- By Technology

- By Deployment Mode

- By Enterprise Size

- By End User Industry

- West

- By Component

- By Technology

- By Deployment Mode

- By Enterprise Size

- By End User Industry

- East

- By Component

- By Technology

- By Deployment Mode

- By Enterprise Size

- By End User Industry

Table of Contents for India Artificial Intelligence Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Technology

1.2.3. By

Deployment Mode

1.2.4. By

Enterprise Size

1.2.5. By

End User Industry

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. India Market Estimate and Forecast

4.1. India Market Overview

4.2. India Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Machine Learning

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Natural Language Processing (NLP)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Computer Vision

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Robotics & Automation

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Expert Systems

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Generative AI

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Deployment Mode

5.3.1. On-Premises

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cloud

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Enterprise Size

5.4.1. Large Enterprises

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Small & Medium Enterprises (SMEs)

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By End User Industry

5.5.1. Healthcare & Life Sciences

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. BFSI

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. IT & ITES

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Retail & Consumer Goods

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Manufacturing

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Automotive & Transportation

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.5.7. Government & Public Sector

5.5.7.1. Market Definition

5.5.7.2. Market Estimation and Forecast to 2035

5.5.8. Telecom

5.5.8.1. Market Definition

5.5.8.2. Market Estimation and Forecast to 2035

5.5.9. Energy & Utilities

5.5.9.1. Market Definition

5.5.9.2. Market Estimation and Forecast to 2035

5.5.10. Others

5.5.10.1. Market Definition

5.5.10.2. Market Estimation and Forecast to 2035

6. North Market Estimate and Forecast

6.1. By

Component

6.2. By

Technology

6.3. By

Deployment Mode

6.4. By

Enterprise Size

6.5. By

End User Industry

7. South Market Estimate and Forecast

7.1. By

Component

7.2. By

Technology

7.3. By

Deployment Mode

7.4. By

Enterprise Size

7.5. By

End User Industry

8. West Market Estimate and Forecast

8.1. By

Component

8.2. By

Technology

8.3. By

Deployment Mode

8.4. By

Enterprise Size

8.5. By

End User Industry

9. East Market Estimate and Forecast

9.1. By

Component

9.2. By

Technology

9.3. By

Deployment Mode

9.4. By

Enterprise Size

9.5. By

End User Industry

10. Company Profiles

10.1.

Tata Consultancy Services Limited

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Infosys Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Wipro Limited

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

HCL Technologies Limited

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Tech Mahindra Limited

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Persistent Systems Limited

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Tata Elxsi Limited

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Fractal Analytics Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Affle (India) Limited

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Zensar Technologies Limited

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Microsoft Corporation

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

International Business Machines Corporation

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

India Artificial Intelligence Market