Middle East Smart Cities Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Solution (Smart Citizen Services, Smart Transportation, Smart Utilities, Smart Environment, Smart Buildings, Others), by Component (Hardware, Software, Services), by Technology (Artificial Intelligence & Machine Learning, Cloud Computing, IoT (Internet of Things), Machine-To-Machine (M2M) Communications, Others)

| Status : Published | Published On : Mar, 2026 | Report Code : VRICT5225 | Industry : ICT & Media | Available Format :

|

Page : 145 |

Middle East Smart Cities Market Overview

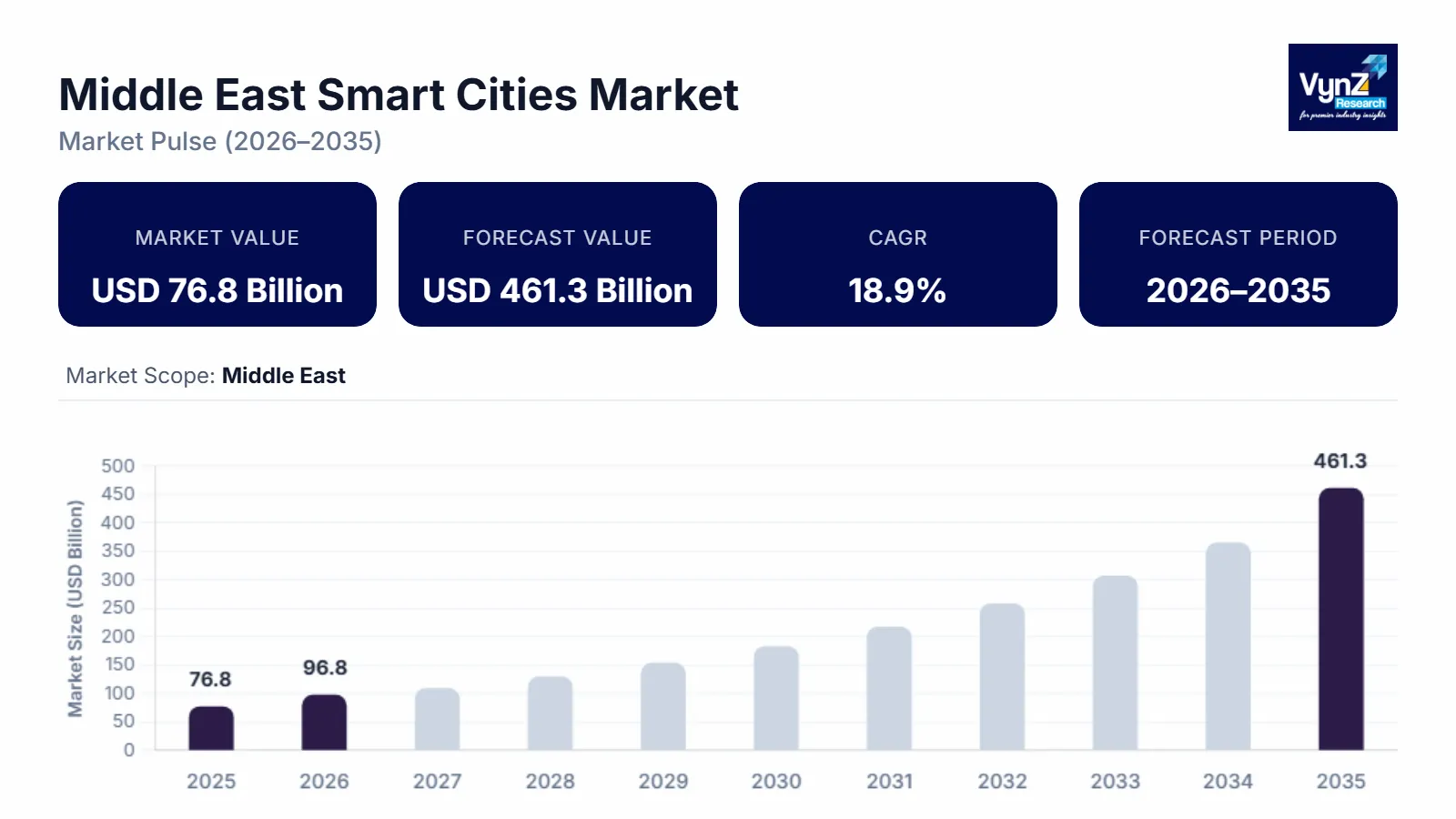

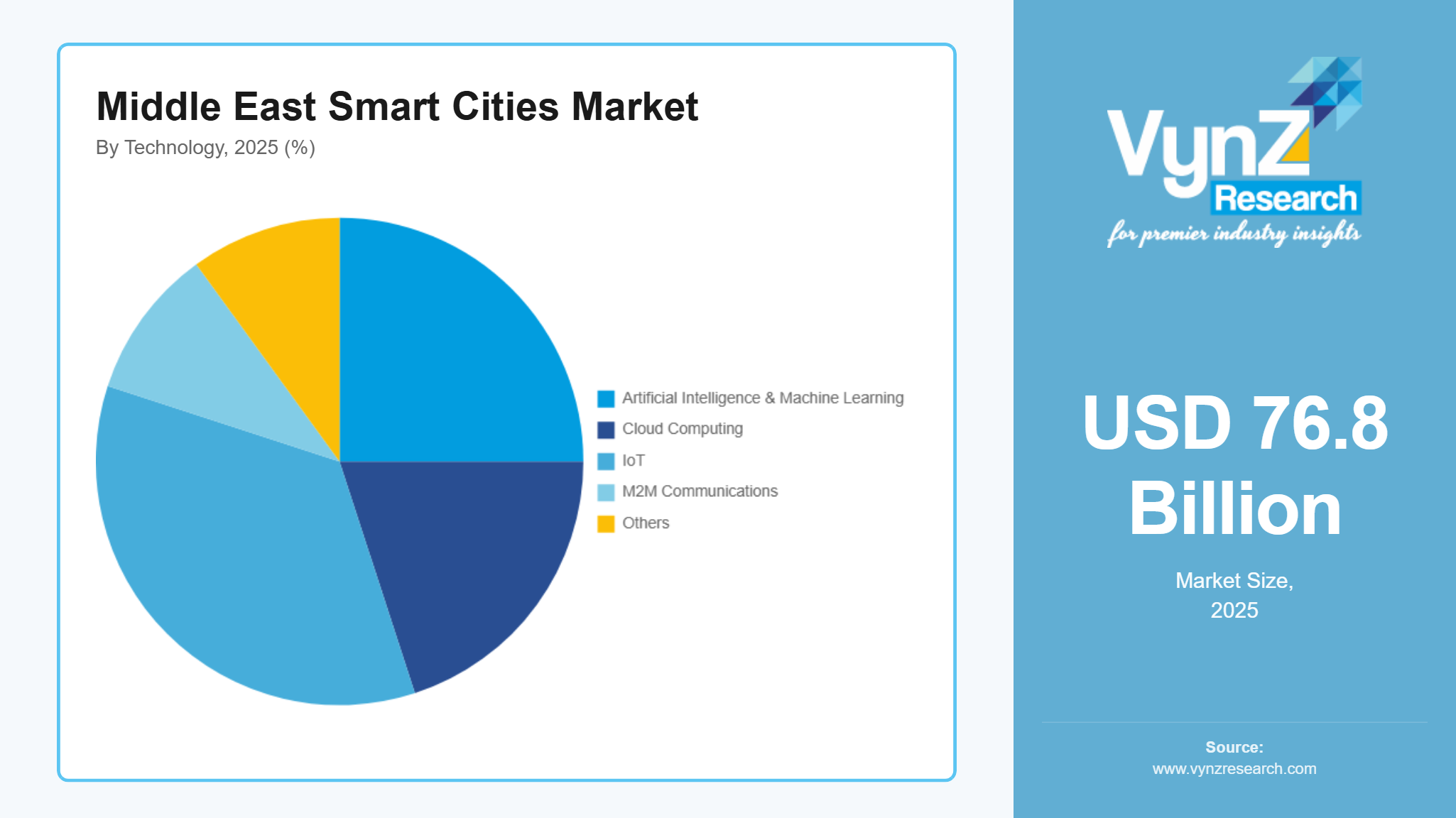

The Middle East smart cities market, which was valued at approximately USD 76.8 billion in 2025 and is estimated to reach around USD 96.8 billion in 2026, is projected to reach close to USD 461.3 billion by 2035, expanding at a CAGR of about 18.9% during the forecast period from 2026 to 2035.

The market is surging forward, propelled by visionary government strategies and a pressing need for sustainable urban evolution. Ambitious national agendas, such as Saudi Arabia's Vision 2030 and the UAE's forward-thinking blueprints, are channeling billions into intelligent infrastructure, fostering economic diversification beyond oil reliance. Rapid urbanization, with populations swelling in megacities like Dubai and Riyadh, demands innovative solutions for efficient resource management, from AI-driven traffic systems to renewable energy grids.

Technological leaps in IoT, 5G, and data analytics are enabling seamless connectivity, enhancing citizen experiences while addressing climate challenges through eco-friendly designs. This growth is amplified by robust public-private partnerships, attracting global investors and tech giants eager to capitalize on a projected multi-billion-dollar opportunity. As the region pivots toward resilience and innovation, smart cities promise not just efficiency, but a blueprint for prosperous, livable futures—inviting forward-thinking enterprises to join this transformative journey.

Middle East Smart Cities Market Dynamics

Market Trends

In the Middle East smart cities landscape, a pivotal trend is the swift integration of digital technologies into core urban infrastructure, transforming how cities manage resources, mobility, and services for enhanced efficiency and resilience. Governments are prioritizing AI, IoT, and data platforms to create interconnected ecosystems that anticipate needs and optimize operations in real time. For instance, Saudi Arabia's telecommunications and technology market reached SAR 190 billion by the end of 2025, with projections to hit SAR 199 billion in 2026, underscoring the rapid scaling of digital backbone essential for smart initiatives. Additionally, the National Single Sign-On Platform linked over 945 government and private platforms in 2025, enabling access for 1.1 million new users and reaching a total of 27 million, facilitating seamless citizen-government interactions. Qatar's Digital Agenda 2030 further amplifies this by aiming for a cumulative economic boost of 40 billion QAR through digital adoption by 2030, fostering innovative urban models.

Growth Drivers

The main driver of a growing energy management market has been governmental policies that promote energy efficiency and sustainable development of the built environment. National and regional governments have developed increasingly strict building codes, performance standards, and incentives for the use of energy-efficient design, materials, and systems. The regulatory framework established by national and regional authorities to support these energy security objectives includes reducing dependence on traditional energy supplies and mitigating peak loads on the grid. As the focus among stakeholders has increased with respect to reducing lifecycle costs and improving environmental performance, there has also been an increase in the adoption of energy-conscious practices by developers, investors, and facility managers, which has generated consistent demand for energy management technologies across all segments, including commercial, residential, and institutional, as According to the International Energy Agency, global investment in energy efficiency reached USD 660 billion in 2024 driven by strong policy support.

The primary driver fueling the Middle East smart cities market is substantial government funding coupled with strategic national visions that prioritize innovation and economic diversification. These policies channel resources into cutting-edge infrastructure, propelling urban transformation at an unprecedented pace. Saudi Arabia's FY2026 budget allocates SAR 35 billion to the infrastructure and transportation sector, encompassing digital government, AI, and industrial cities to support smart development. Complementing this, Dubai's 2026 fiscal plan projects revenues of AED 107.7 billion, including AED 5 billion in reserves, to advance digital transformation and AI under the Dubai Economic Agenda D33, aiming to double GDP by 2033. Qatar's initiatives, targeting 26,000 new ICT jobs by 2030, reinforce this drive through programs like the National Skilling Programme, set to train 50,000 individuals in advanced digital skills by 2025. Such commitments not only mitigate oil dependency but ignite private sector collaboration, creating vibrant ecosystems where technology elevates quality of life, boosts productivity, and ensures long-term prosperity. This forward-thinking approach empowers businesses to innovate confidently, drawing global partners eager to contribute to a region redefining urban excellence.

Market Restraints / Challenges

A significant challenge in the Middle East smart cities market is managing the strain on resources and bolstering cybersecurity amid explosive digital expansion, which could hinder seamless implementation if not addressed proactively. As connectivity surges, vulnerabilities rise, demanding robust safeguards alongside infrastructure scaling. In Saudi Arabia, biometric services conducted over 850,000 daily checks and 70,000 registrations in 2025, highlighting the scale of data handling that requires fortified protections. The kingdom's electronic gates served 8.3 million passengers in 2025, amplifying the need for secure, integrated systems to prevent disruptions. UAE projections show airport passenger traffic reaching 159 million by end-2025, a 7.5% growth, intensifying demands on smart mobility networks and risk management. Overcoming this involves strategic investments in resilient frameworks, talent development, and cross-border collaborations to ensure trust and continuity. By turning these hurdles into catalysts for innovation, stakeholders can fortify cities against threats, sustaining growth while safeguarding citizens and assets in an increasingly interconnected world. This resilience will ultimately differentiate leaders, inviting enterprises to partner in building secure, future-proof urban environments.

Market Opportunities

The Middle East smart cities market presents a compelling opportunity for economic diversification via sustainable, tech-infused urban solutions that reduce environmental impact while unlocking new revenue streams and fostering innovation. By embracing renewables, efficient resource management, and green innovations, governments are creating fertile ground for investment, job creation, and cross-sector partnerships beyond traditional industries. Initiatives across the region emphasize smart energy systems, advanced mobility, and eco-friendly urban planning, enabling enterprises to develop cutting-edge applications in IoT-integrated infrastructure, data-driven sustainability, and intelligent logistics. This shift opens doors for businesses to pioneer solutions in renewable-powered grids, waste optimization, and low-carbon developments, attracting global talent and capital to build resilient ecosystems. Qatar's focus on a booming digital economy through widespread technology adoption drives productivity gains and new market entries in smart services. Similarly, UAE and Saudi Arabia's emphasis on AI, cloud, and sustainable urban models positions the region as a hub for transformative projects like transit-oriented designs and intelligent city platforms. Embracing this opportunity allows forward-thinking organizations to lead in high-growth areas, forging strategic alliances that deliver profitability, ecological balance, and lasting client value in an evolving, innovation-rich landscape.

Middle East Smart Cities Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 76.8 Billion |

|

Revenue Forecast in 2035 |

USD 461.3 Billion |

|

Growth Rate |

18.9% |

|

Segments Covered in the Report |

Solution, Component, Technology |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Saudi Arabia, UAE, Rest of the MEA |

|

Key Companies |

Cisco Systems, Inc., Huawei Investment & Holding Co., Ltd., International Business Machines Corporation, Siemens AG, Schneider Electric SE, Honeywell International Inc., Microsoft Corporation, Oracle Corporation, ABB Ltd., Telefonaktiebolaget LM Ericsson, SAP SE, and Accenture plc |

|

Customization |

Available upon request |

Middle East Smart Cities Market Segmentation

By Solution

Smart transportation stands as the largest and fastest-growing category in the region. This category holds an estimated market share of 30% in 2025. Mega-projects prioritize intelligent mobility to manage surging urban populations and reduce congestion in expanding cities. Governments focus on integrated systems for traffic optimization, autonomous vehicles, and seamless public transit, aligning with goals for sustainable connectivity and economic hubs. This segment leads due to high-priority investments in roadways, railways, and smart logistics that support trade, tourism, and daily urban flow. Its rapid expansion stems from urgent needs to enhance safety, lower emissions, and enable efficient movement amid rapid development, positioning it as a cornerstone for resilient, future-ready cities that attract global partnerships and investment.

By Component

Software emerges as the largest and fastest-growing segment within the market. This category holds an estimated market share of 45% in 2025 and is growing at a CAGR of 19.4% during the forecast period. Advanced platforms enable real-time data processing, predictive analytics, and integrated management across urban systems, powering everything from governance to resource allocation. Governments emphasize software-driven solutions to create interconnected ecosystems that improve decision-making and service delivery. This dominance arises from the need for scalable, adaptable tools that unify hardware and deliver actionable insights for sustainability and efficiency. Its accelerated growth reflects the shift toward digital-first strategies, where software unlocks innovation in AI applications, cloud integration, and citizen interfaces, fostering agile urban environments that evolve with technological advances and deliver measurable value to stakeholders.

By Technology

IoT (Internet of Things) is the largest and fastest-growing technology category. This category has an estimated market share of 35% in 2025. It forms the foundational layer for connected infrastructure, enabling sensors, devices, and networks to collect vast data for intelligent urban operations across energy, mobility, and environment. Regional priorities highlight IoT's role in creating responsive systems that optimize resources and enhance livability in ambitious developments. As the backbone of smart ecosystems, IoT leads due to widespread deployment in monitoring, automation, and real-time control, supporting sustainability targets. Its explosive growth is fueled by expanding connectivity and the imperative for data-driven efficiency, empowering cities to innovate dynamically and position the region as a global frontrunner in tech-enabled urban transformation.

Regional Insights

Saudi Arabia

The Middle East smart cities market by geography features Saudi Arabia as the largest and fastest-growing category, propelled by the scale and ambition of national transformation efforts under Vision 2030. Massive flagship projects integrate advanced technologies across vast urban developments, driving comprehensive adoption in transportation, utilities, buildings, and citizen services. This dominance stems from strategic resource allocation toward digital infrastructure, sustainability, and economic diversification on an unparalleled level, creating extensive implementation scope and attracting global collaborations. The kingdom's expansive initiatives set regional benchmarks for innovation and resilience, offering unparalleled opportunities for enterprises to engage in high-impact, scalable solutions that redefine urban landscapes and deliver enduring value in a rapidly evolving market.

UAE

UAE stands as a highly influential and dynamically growing geography in the Middle East smart cities market, renowned for its pioneering, high-ranking urban models in Dubai and Abu Dhabi. Proactive emirate-level strategies weave cutting-edge technologies into governance, mobility, sustainability, and public services, establishing global standards for efficient, livable cities. This leadership arises from forward-thinking policies that accelerate AI, IoT, and digital ecosystem adoption nationwide, fostering seamless citizen experiences and operational excellence. The UAE's vibrant, innovation-focused environment draws international expertise, capital, and partnerships, providing rich avenues for solutions in smart transportation, utilities, buildings, and citizen-centric applications. This positions the nation as a beacon of progressive urbanization, inspiring businesses to contribute to transformative projects that elevate quality of life and global competitiveness.

Rest of the Middle East

The rest of the Middle East represents an emerging and progressively expanding geography in the smart cities market, encompassing diverse nations pursuing tailored digital and sustainable urban advancements. Governments in these areas focus on addressing localized challenges through targeted initiatives in connectivity, resource management, and public services, gradually building momentum toward integrated smart ecosystems. Growth is supported by regional aspirations for modernization, economic resilience, and improved livability amid urbanization pressures. While varying in scale, these markets offer promising entry points for customized solutions in transportation, utilities, and citizen engagement, with increasing emphasis on collaborative frameworks and technology transfer. This segment holds significant potential for forward-looking enterprises to pioneer adaptable innovations, forge meaningful partnerships, and support inclusive urban progress across a broader, multifaceted regional landscape.

Competitive Landscape / Company Insights

The Middle East smart cities market exhibits a moderately fragmented competitive landscape, characterized by a blend of dominant global technology leaders and influential regional participants. This fragmentation arises from the market's reliance on diverse, large-scale national projects that demand specialized expertise across hardware, software, services, and localized integration, preventing full consolidation while encouraging strategic alliances.

International firms leverage their scale, innovation, and proven track records to win major bids, while regional telecom giants (e.g., in Saudi Arabia and the UAE) provide critical connectivity and customization. Public-private partnerships dominate, enabling knowledge transfer, rapid deployment, and alignment with visions like Vision 2030 and UAE digital agendas. Competition intensifies around sustainability, cybersecurity, interoperability, and citizen-focused outcomes, with ongoing collaborations and joint ventures signaling gradual maturation. This vibrant, opportunity-rich environment empowers enterprises to differentiate through tailored expertise, build strategic relationships, and capture significant value in the region's transformative urban evolution.

Mini Profiles

Cisco Systems, Inc. delivers critical infrastructure for the AI era, fusing networking, security, observability, and collaboration. It offers a leading portfolio of innovations in networking, security, cloud, and more to connect organizations securely.

Huawei Investment & Holding Co., Ltd. is a global leader in ICT infrastructure and smart devices, founded in 1987. It serves over three billion people in 170+ countries, aiming for a fully connected, intelligent world.

International Business Machines Corporation (IBM) provides consulting, software, infrastructure, and hybrid cloud/AI solutions via Red Hat. It blends intelligence and innovation to improve business, society, and human experience.

Siemens AG accelerates customer transformations with industrial AI for efficiency, sustainability, and smart infrastructure. It combines real and digital worlds to support factories, cities, transport, and digitalization.

Schneider Electric SE leads in energy technology, electrifying, automating, and digitalizing industries, buildings, and grids. It enables open, interconnected ecosystems and ranks among the world’s most sustainable companies.

Key Players

- Cisco Systems, Inc.

- Huawei Investment & Holding Co., Ltd.

- International Business Machines Corporation

- Siemens AG

- Schneider Electric SE

- Honeywell International Inc.

- Microsoft Corporation

- Oracle Corporation

- ABB Ltd

- Telefonaktiebolaget LM Ericsson

- SAP SE

- Accenture plc

Recent Developments

February 2026 - Siemens AG opened a new Digital Industries Software office in Saudi Arabia to accelerate digital transformation, supporting Vision 2030 through faster local innovation, customer service, and co-creation in smart infrastructure.

February 2026 - Siemens AG forged a strategic partnership with Al-Futtaim Real Estate to propel digital transformation and sustainability in real estate across the UAE and Saudi Arabia. The collaboration involves distributing Siemens' fire alarm and building management systems, integrating smart building technologies, and supporting training programs to drive intelligent, efficient, and environmentally responsible urban environments in alignment with regional smart city and net-zero goals.

February 2026 - International Business Machines Corporation (IBM) collaborated with the Saudi Water Authority to launch the AI-powered H2O Platform, accelerating water sector transformation with real-time intelligence for sustainable management aligned with Vision 2030.

May 2025 - Cisco Systems, Inc. expanded its partnership with Saudi Arabia's HUMAIN AI enterprise to build scalable, secure AI infrastructure, supporting smart cities, healthcare, education, and government digitization under Vision 2030.

February 2025 - Huawei Investment & Holding Co., Ltd. partnered with King Abdullah Financial District (KAFD) in Saudi Arabia to advance smart city innovation, deploying WiFi-7, 5G-A, AI, IoT, and cloud technologies for digital infrastructure and sustainable urban platforms.

Middle East Smart Cities Market Coverage

Solution Insight and Forecast 2026 - 2035

- Smart Citizen Services

- Smart Transportation

- Smart Utilities

- Smart Environment

- Smart Buildings

- Others

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Technology Insight and Forecast 2026 - 2035

- Artificial Intelligence & Machine Learning

- Cloud Computing

- IoT (Internet of Things)

- Machine-To-Machine (M2M) Communications

- Others

Middle East Smart Cities Market by Region

- Saudi Arabia

- By Solution

- By Component

- By Technology

- UAE

- By Solution

- By Component

- By Technology

- Rest of the MEA

- By Solution

- By Component

- By Technology

Table of Contents for Middle East Smart Cities Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Solution

1.2.2. By

Component

1.2.3. By

Technology

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Middle Market Estimate and Forecast

4.1. Middle Market Overview

4.2. Middle Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Solution

5.1.1. Smart Citizen Services

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Smart Transportation

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Smart Utilities

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Smart Environment

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Smart Buildings

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Others

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.2. By Component

5.2.1. Hardware

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Software

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Services

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Artificial Intelligence & Machine Learning

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cloud Computing

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. IoT (Internet of Things)

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Machine-To-Machine (M2M) Communications

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Others

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

6. Saudi Arabia Market Estimate and Forecast

6.1. By

Solution

6.2. By

Component

6.3. By

Technology

7. UAE Market Estimate and Forecast

7.1. By

Solution

7.2. By

Component

7.3. By

Technology

8. Rest of the MEA Market Estimate and Forecast

8.1. By

Solution

8.2. By

Component

8.3. By

Technology

9. Company Profiles

9.1.

Cisco Systems, Inc.

9.1.1.

Snapshot

9.1.2.

Overview

9.1.3.

Offerings

9.1.4.

Financial

Insight

9.1.5.

Recent

Developments

9.2.

Huawei Investment & Holding Co., Ltd.

9.2.1.

Snapshot

9.2.2.

Overview

9.2.3.

Offerings

9.2.4.

Financial

Insight

9.2.5.

Recent

Developments

9.3.

International Business Machines Corporation

9.3.1.

Snapshot

9.3.2.

Overview

9.3.3.

Offerings

9.3.4.

Financial

Insight

9.3.5.

Recent

Developments

9.4.

Siemens AG

9.4.1.

Snapshot

9.4.2.

Overview

9.4.3.

Offerings

9.4.4.

Financial

Insight

9.4.5.

Recent

Developments

9.5.

Schneider Electric SE

9.5.1.

Snapshot

9.5.2.

Overview

9.5.3.

Offerings

9.5.4.

Financial

Insight

9.5.5.

Recent

Developments

9.6.

Honeywell International Inc.

9.6.1.

Snapshot

9.6.2.

Overview

9.6.3.

Offerings

9.6.4.

Financial

Insight

9.6.5.

Recent

Developments

9.7.

Microsoft Corporation

9.7.1.

Snapshot

9.7.2.

Overview

9.7.3.

Offerings

9.7.4.

Financial

Insight

9.7.5.

Recent

Developments

9.8.

Oracle Corporation

9.8.1.

Snapshot

9.8.2.

Overview

9.8.3.

Offerings

9.8.4.

Financial

Insight

9.8.5.

Recent

Developments

9.9.

ABB Ltd

9.9.1.

Snapshot

9.9.2.

Overview

9.9.3.

Offerings

9.9.4.

Financial

Insight

9.9.5.

Recent

Developments

9.10.

Telefonaktiebolaget LM Ericsson

9.10.1.

Snapshot

9.10.2.

Overview

9.10.3.

Offerings

9.10.4.

Financial

Insight

9.10.5.

Recent

Developments

9.11.

SAP SE

9.11.1.

Snapshot

9.11.2.

Overview

9.11.3.

Offerings

9.11.4.

Financial

Insight

9.11.5.

Recent

Developments

9.12.

Accenture plc

9.12.1.

Snapshot

9.12.2.

Overview

9.12.3.

Offerings

9.12.4.

Financial

Insight

9.12.5.

Recent

Developments

10. Appendix

10.1. Exchange Rates

10.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Middle East Smart Cities Market