Artificial Intelligence of Things (AIoT) Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Deployment Mode (Cloud Based, On Premise, Hybrid), by Technology (Machine Learning, Natural Language Processing, Computer Vision, Context Aware Computing), by Connectivity (Wired, Wireless), by End Use (Manufacturing, Healthcare, Retail and E Commerce, BFSI, IT and Telecommunications, Energy and Utilities, Transportation and Logistics, Agriculture, Smart Cities and Infrastructure)

| Status : Published | Published On : Apr, 2026 | Report Code : VRICT5229 | Industry : ICT & Media | Available Format :

|

Page : 210 |

AIoT Market Overview

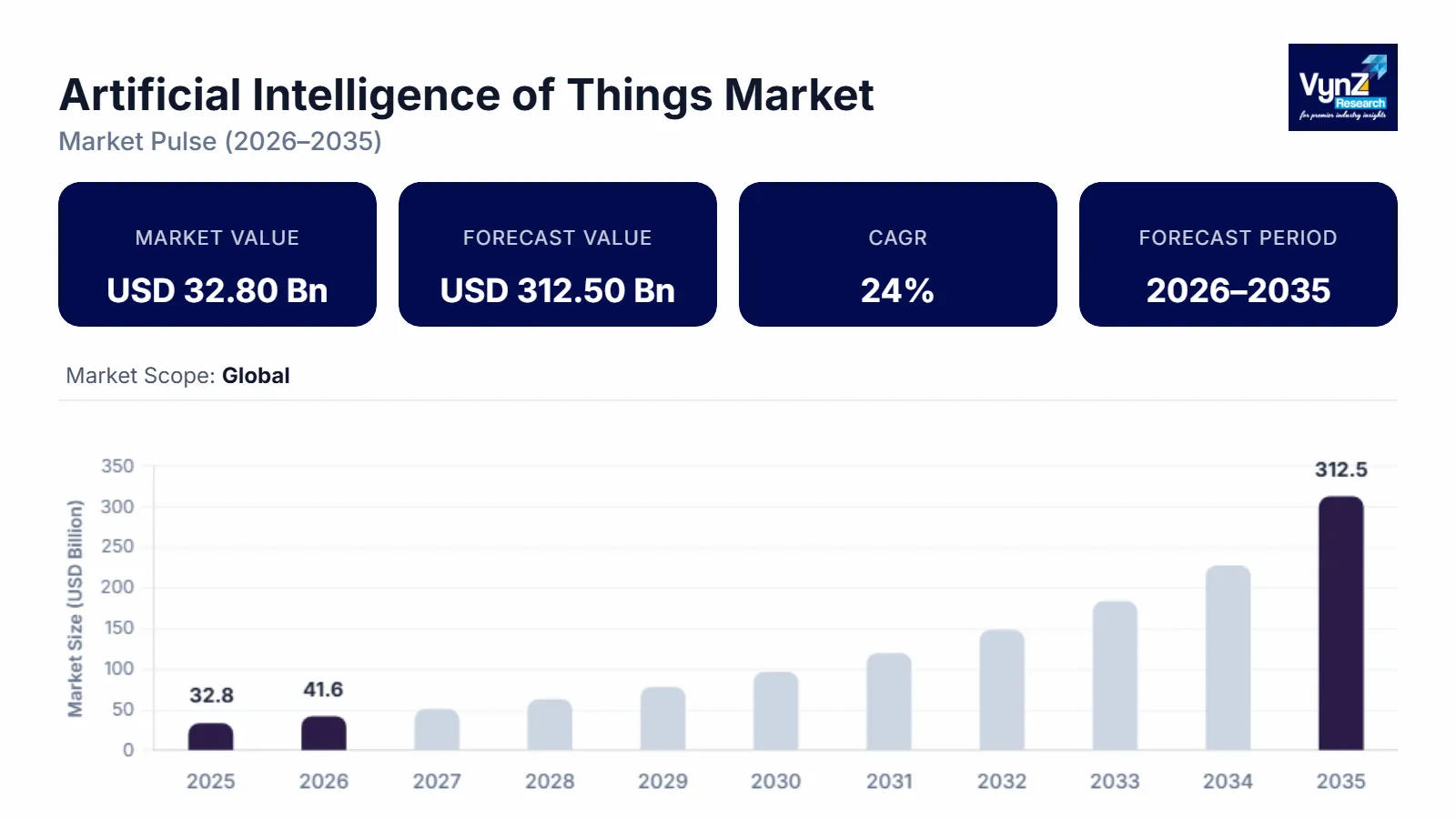

The global artificial intelligence of things (AIoT) market which was valued at approximately USD 32.80 billion in 2025 and is estimated to rise further up to almost USD 41.60 billion by 2026, is projected to reach around USD 312.50 billion in 2035, expanding at a CAGR of about 24% during the forecast period from 2026 to 2035.

The market expands because companies now use artificial intelligence to build better connected devices while industrial processes need real-time data analysis and there is growing demand for edge computing systems together with intelligent automation systems. The market keeps growing because of increased need for smart manufacturing, connected healthcare systems and autonomous infrastructure together with ongoing funding for digital transformation programs and smart city projects which governments are implementing.

The artificial intelligence Internet of Things ecosystem receives vital support from governmental programs and policy frameworks which establish operational boundaries for three major regions that include Asia Pacific, North America, and Europe. The World Health Organization supports initiatives which demonstrate how connected health technologies and AI driven monitoring systems help healthcare delivery and disease surveillance. Government funding for industrial digitization, IoT infrastructure development and AI innovation has led to faster enterprise technology adoption. The national strategies which focus on Industry 4.0, digital public infrastructure and smart urban development will lead to extensive implementation of their respective initiatives which will result in sustained market growth.

Artificial Intelligence of Things Market Dynamics

Market Trends

The market is currently undergoing major technological changes which companies are adopting through their use of connected systems that enable real-time data processing and automatic intelligent systems. The market currently experiences its most decisive transformation through increased edge AI adoption which companies use to achieve their industrial and healthcare operations through low-latency processing, improved data protection and operational effectiveness.

The World Health Organization supports digital health frameworks which healthcare organizations use to establish their monitoring systems which create demand for AI-based IoT solutions in connected care environments. The market now sees a new trend emerge which connects AIoT systems with 5G networks through companies that develop digital infrastructure to match the growing number of connected devices which results in market competition changes through companies developing integrated platforms with intelligent analytics.

Growth Drivers

The market grows through smart infrastructure and industrial automation system deployment which creates continuous demand across manufacturing, healthcare and smart city operations. The market expansion receives acceleration from rising digital infrastructure investments and Industry 4.0 funding while connected ecosystems show particular growth in regions that prioritize those systems. The organization expands its capacity to make data-based decisions which enables all organizations to become more successful.

AIoT platforms will experience steady demand throughout the forecast period because enterprises focus on improving their operational efficiency, predictive maintenance and resource optimization processes. Government-backed programs that promote digital transformation through smart city missions and healthcare programs which work with global digital health strategies help increase adoption in both public and private sectors.

Market Restraints / Challenges

The market should experience market growth but it will encounter several obstacles that will restrict its development. Data security problems together with regulatory difficulties prevent widespread implementation in industries that manage sensitive data such as healthcare and critical infrastructure. The World Health Organization defined policy frameworks which require AIoT solutions to meet the compliance requirements for creating secure digital health systems that work with other digital health systems.

Enterprises face operational difficulties because they must handle both high implementation expenses and equipment operational needs. The market faces economic instabilities because companies depend on three main operational elements of advanced semiconductor components and cloud infrastructure and skilled workforce to control their operational costs.

Market Opportunities

The market provides important chances for development through connected healthcare systems and smart urban infrastructure which face escalating need for remote monitoring systems, predictive analytics tools and intelligent resource management systems. Healthcare providers and industrial enterprises and public sector organizations will need AIoT solutions which companies develop and offer through their highly scalable operational capabilities.

Digital public infrastructure development offers major business opportunities through smart city projects and intelligent transportation systems which create new funding paths for permanent business expansion. AI-driven analytics together with automation platforms and edge computing solutions will create system enhancements which lead to more efficient systems and better user experiences. Government-supported digital transformation strategies and public investment programs aligned with global health and infrastructure development frameworks are further expected to drive sustained market expansion.

Global AIoT Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 32.80 Billion |

|

Revenue Forecast in 2035 |

USD 312.50 Billion |

|

Growth Rate |

24% |

|

Segments Covered in the Report |

Component, Deployment Mode, Technology, Connectivity, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Amazon Web Services, Cisco Systems, Google, Hewlett Packard Enterprise, IBM, Intel, Microsoft, NVIDIA, Oracle, SAP |

|

Customization |

Available upon request |

Artificial Intelligence of Things Market Segmentation

By Component

The market share distribution in 2025 showed that hardware held the highest value with 46% revenue share which resulted from the extensive sensor, edge device and connectivity infrastructure installation in industrial and smart systems. The manufacturing and infrastructure projects create strong demand which fuels technology adoption through government digital and industrial transformation programs.

Software will experience the highest growth between 2026 and 2035 because it will reach a compound annual growth rate of 26.8%. The demand for AI platforms and analytics tools and IoT management systems enables organizations to make decisions in real time which creates growth opportunities for these technologies. The demand for enterprise deployment solutions drives the market for services which are growing at a 23.5% compound annual growth rate.

By Deployment Mode

The cloud-based deployment system achieved the highest market share in 2025 because it provided 52% of total revenue through its ability to scale and deliver cost savings while enabling centralized data access. The trend toward digital infrastructure adoption and enterprise cloud strategy implementation continues to strengthen market leadership.

Hybrid deployment will achieve the highest growth rate during the forecast period with an estimated 25.9% compound annual growth rate because organizations require both data security and operational flexibility. The on-premise deployment method will experience a growth rate of 21.7% because it meets the data control needs of critical infrastructure and regulated sectors.

By Technology

The machine learning technology generated the highest revenue share for the industry segment because it accounted for 44% of total revenue through its usage in predictive analytics and automation across multiple industries.

Computer vision will experience the fastest growth rate between 2026 and 2035 when it will reach a 27.4% compound annual growth rate because of its use in surveillance and quality inspection and autonomous systems. Natural language processing and context aware computing show steady growth rates of 24.1% and 23.6% respectively because these technologies gain more applications in intelligent interaction systems.

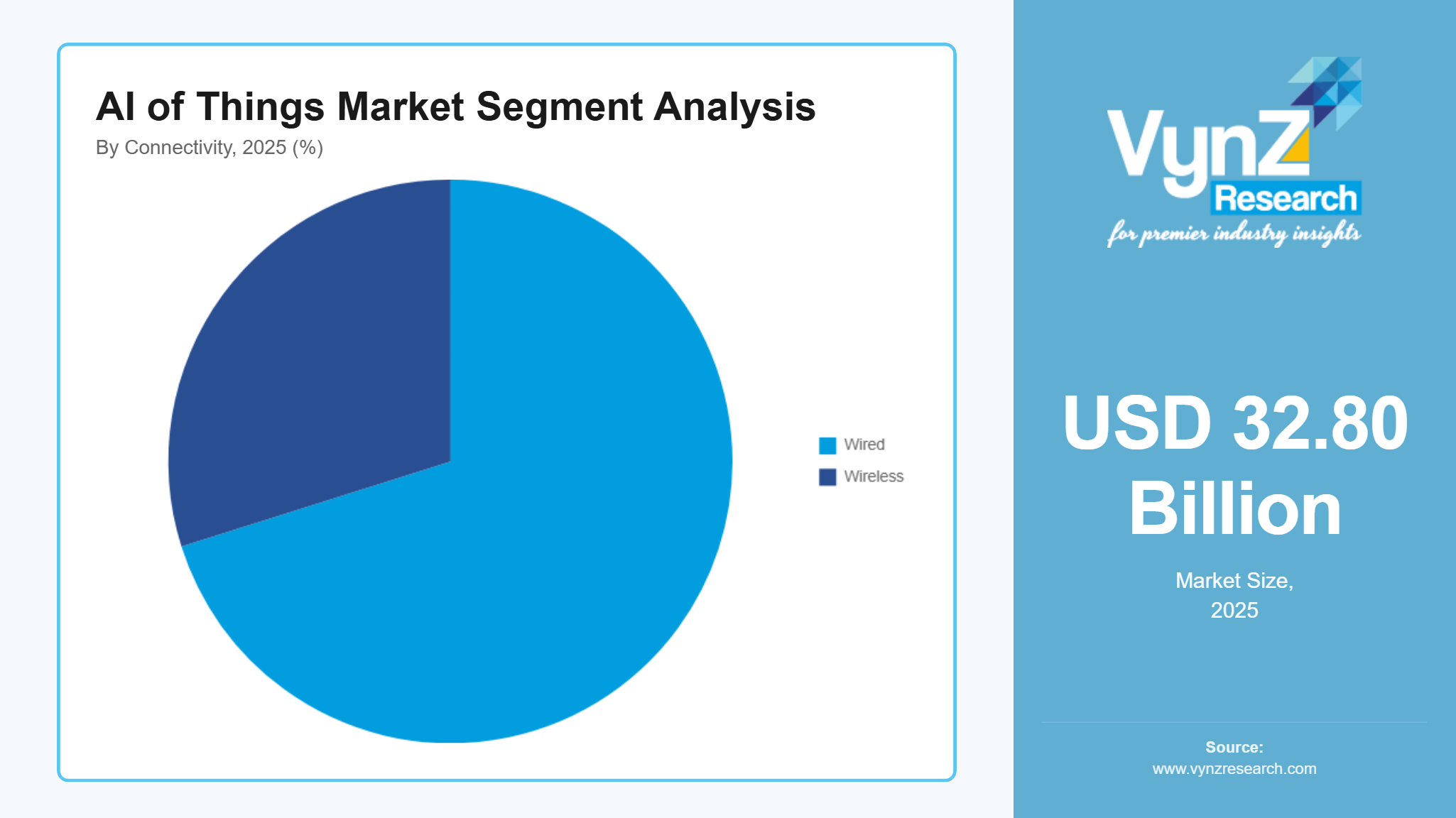

By Connectivity

Wired technologies dominated the market in 2025 because they generated 61% revenue share through increased adoption of connected devices in different industrial sectors and smart infrastructure systems.

Wireless technologies will follow the fastest growth trajectory because they will reach a 26.3% compound annual growth rate during the forecast period due to the expanding advanced communication networks and digital connectivity initiatives. The industrial sector needs wired connectivity solutions which deliver dependable and secure data transmission for operational purposes.

By End User

The manufacturing sector maintained its revenue leadership position in 2025 by generating 29% of total revenue through industrial automation and predictive maintenance solutions.

The healthcare sector will expand the most between 2026 and 2035, at 27.1 CAGR, because medical devices and remote monitoring systems now use connected technology. Digital health initiatives find support from organizations like World Health Organization which helps improve their adoption rate. The market continues to grow because sectors increase their investments to build intelligent infrastructure and data-driven systems.

Regional Insights

North America

The market in North America reached 30% market share in 2025 because of its digital infrastructure, business AI adoption and funding for connected technology development. AI integrated IoT systems are being implemented at high rates in New York, San Francisco and Toronto throughout their manufacturing and healthcare and smart infrastructure sectors. The combination of data security standards and interoperability standards leads to stronger industry adoption of these technologies.

Europe

The 2025 market contained 25% of its total value from European contributions. The region expands its boundaries through strong regulatory systems which protect data privacy and allow industrial automation to spread throughout Germany, the United Kingdom and France. Berlin, London, and Paris operate as essential centers for AIoT technology implementation in manufacturing and transportation and smart city projects.

Asia Pacific

The Asia Pacific market reached 25% of its total value by 2025 because of industrial growth, digital infrastructure progress and smart technology adoption in China, India and Japan. Major cities such as Beijing, Mumbai, and Tokyo are emerging as key centers for AIoT deployment across manufacturing, healthcare, and urban infrastructure projects.

Rest of the World

The market for 2025 for the Rest of the World achieved 20% of its total value from Latin America, the Middle East and Africa. The development of these regions advances through rising digital infrastructure investments, urban development work and the implementation of connected technologies in emerging economies. São Paulo, Dubai and Johannesburg serve as major cities where AIoT solutions begin to operate their industrial and infrastructure applications.

Competitive Landscape / Company Insights

The market operates as a competitive battleground which features global and regional companies that pursue platform development, strategic alliance building and market territory expansion. Companies are increasingly investing in research and development together with cloud integration and edge intelligence capabilities to build their competitive strength in the market. The National Institute of Standards and Technology together with its supporting organizations creates policy frameworks and digital standards which help organizations implement safe and interoperable systems. AI driven analytics and connected systems continue to evolve which creates stronger competitive pressure between different industries.

Mini Profiles

Amazon Web Services focuses on cloud based AIoT platforms and analytics, supported by global infrastructure, strong developer ecosystem, and scalable services enabling enterprise adoption across industries.

Cisco Systems operates in enterprise and industrial segments, emphasizing network security, connectivity solutions, and integrated IoT architectures to support large scale digital transformation initiatives.

Google leverages advanced AI capabilities, cloud platforms, and data analytics to expand market presence, supported by strong digital ecosystem and continuous innovation in intelligent solutions.

Hewlett Packard Enterprise focuses on edge computing, hybrid cloud, and data infrastructure, supported by enterprise customer base and strong presence in industrial and commercial digital transformation projects.

IBM operates in enterprise and consulting segments, emphasizing AI platforms, hybrid cloud solutions, and industry specific applications to enhance operational efficiency and data driven decision making.

Key Players

- Amazon Web Services

- Cisco Systems

- Hewlett Packard Enterprise

- IBM

- Intel

- Microsoft

- NVIDIA

- Oracle

- SAP

Recent Developments

In January, 2026, Amazon Web Services expanded its AIoT capabilities by enhancing IoT Core and integrating advanced edge intelligence through SageMaker Edge. These upgrades improved real time device analytics and scalable deployment across industrial environments.

In March, 2026, IBM advanced enterprise AIoT deployments by expanding Watson based edge intelligence solutions. The development focused on enabling real time analytics and automation across manufacturing and energy sectors.

In January, 2026, Microsoft strengthened its Azure IoT platform by introducing AI Copilot features for predictive maintenance and smart infrastructure applications. This enhancement supports improved decision making and operational efficiency in connected systems.

In February, 2026, NVIDIA upgraded its edge AI portfolio with new GPU solutions optimized for IoT and industrial workloads. These advancements enhance processing capabilities for real time analytics and autonomous systems.

In March, 2026, Cisco Systems continued expanding its AIoT ecosystem through enhanced networking and connectivity solutions supporting intelligent infrastructure. The company focused on enabling secure and scalable deployments across enterprise and industrial applications.

Global AIoT Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Deployment Mode Insight and Forecast 2026 - 2035

- Cloud Based

- On Premise

- Hybrid

Technology Insight and Forecast 2026 - 2035

- Machine Learning

- Natural Language Processing

- Computer Vision

- Context Aware Computing

Connectivity Insight and Forecast 2026 - 2035

- Wired

- Wireless

End Use Insight and Forecast 2026 - 2035

- Manufacturing

- Healthcare

- Retail and E Commerce

- BFSI

- IT and Telecommunications

- Energy and Utilities

- Transportation and Logistics

- Agriculture

- Smart Cities and Infrastructure

Global AIoT Market by Region

- North America

- By Component

- By Deployment Mode

- By Technology

- By Connectivity

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Deployment Mode

- By Technology

- By Connectivity

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Deployment Mode

- By Technology

- By Connectivity

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Deployment Mode

- By Technology

- By Connectivity

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for AIoT Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Deployment Mode

1.2.3. By

Technology

1.2.4. By

Connectivity

1.2.5. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Deployment Mode

5.2.1. Cloud Based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. On Premise

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Hybrid

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Machine Learning

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Natural Language Processing

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Computer Vision

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Context Aware Computing

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Connectivity

5.4.1. Wired

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Wireless

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By End Use

5.5.1. Manufacturing

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Healthcare

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Retail and E Commerce

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. BFSI

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. IT and Telecommunications

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Energy and Utilities

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.5.7. Transportation and Logistics

5.5.7.1. Market Definition

5.5.7.2. Market Estimation and Forecast to 2035

5.5.8. Agriculture

5.5.8.1. Market Definition

5.5.8.2. Market Estimation and Forecast to 2035

5.5.9. Smart Cities and Infrastructure

5.5.9.1. Market Definition

5.5.9.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Deployment Mode

6.3. By

Technology

6.4. By

Connectivity

6.5. By

End Use

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Deployment Mode

7.3. By

Technology

7.4. By

Connectivity

7.5. By

End Use

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Deployment Mode

8.3. By

Technology

8.4. By

Connectivity

8.5. By

End Use

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Deployment Mode

9.3. By

Technology

9.4. By

Connectivity

9.5. By

End Use

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Amazon Web Services

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Cisco Systems

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Google

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Hewlett Packard Enterprise

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

IBM

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Intel

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

NVIDIA

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Oracle

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

SAP

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

AIoT Market