Gaming Device Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product (PC Gaming Hardware, Console Gaming Hardware, Components & Internal Hardware, VR, Handheld/Portable Gaming Devices), by Price (Budget, Mid-Range, Premium, Flagship), by Distribution Channel (Online, Offline), by End User (Casual/Hobbyist Gamers, Core/ Enthusiast Gamers, eSports & Competitive Gamers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRICT5226 | Industry : ICT & Media | Available Format :

|

Page : 185 |

Gaming Device Market Overview

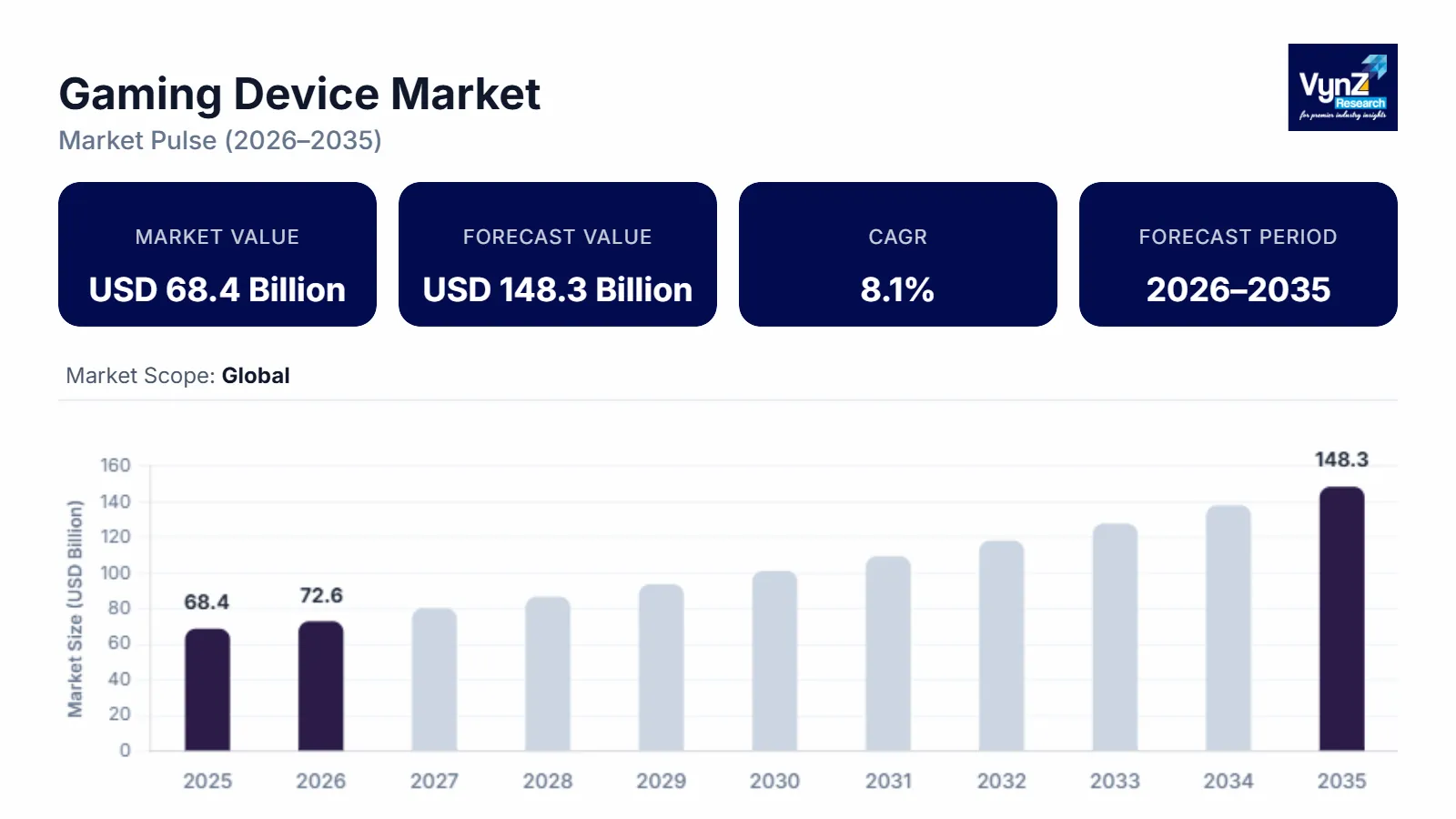

The gaming device market which was valued at approximately USD 68.4 billion in 2025 and is estimated to reach around USD 72.6 billion in 2026, is projected to reach approximately USD 148.3 billion by 2035, expanding at a CAGR of about 8.1% during the forecast period from 2026 to 2035.

The market grows because global demand for immersive digital entertainment experiences, consumer spending on interactive gaming equipment, advancements in graphics processing power, and connectivity technology are all increasing. The high-performance gaming consoles, dedicated gaming laptops, advanced graphics cards and peripheral devices have become more common, which helps users experience better engagement during casual gaming and competitive gaming in professional settings.

The national digital economy strategies of multiple countries include plans for developing interactive entertainment technologies and advanced semiconductor manufacturing capabilities, which will create gaming hardware for gaming production. The International Telecommunication Union and various national digital development authorities report that public broadband access, cloud infrastructure improvements and low latency network development create better conditions for people to use advanced gaming equipment. The structural developments together with expanding gaming communities and rising multiplayer online gaming participation are driving demand in key technology centers such as the United States, China, Japan and South Korea, which have digital entertainment ecosystems and advanced consumer electronics industries that drive hardware innovation and market development.

Gaming Device Market Dynamics

Market Trends

The market is undergoing fundamental changes through new technology use and different ways consumers interact with products and shifts in how people expect devices to operate. It is experiencing two main forces because gamers now need high performance gaming systems that include advanced graphics processing units with artificial intelligence powered optimization and real-life display technologies. The International Telecommunication Union (ITU) and the U.S. Federal Communications Commission (FCC) release public digital infrastructure reports which show that high speed broadband networks and low latency connectivity systems have expanded rapidly to support advanced gaming console systems.

The digital distribution platforms of cloud gaming ecosystems are being developed to create new systems which enable players to access their games from different devices. Government programs for digital transformation include the European Commission Digital Strategy and the Ministry of Industry and Information Technology (China) technology development programs which require funding for semiconductor technology advancement and high-performance computing technology development. Device manufacturers now develop products based on their new focus on advanced cooling systems and customizable controller designs as well as cross platform product features which create new methods of product development and market competition in the gaming device sector.

Growth Drivers

The global esports market growth and consumer spending growth on interactive entertainment products have both helped the gaming device market to grow. The structured esports programs and digital entertainment initiatives which receive support from the U.S. Department of Commerce and the Ministry of Culture, Sports and Tourism of South Korea show that esports have gained institutional recognition as a legitimate competitive sport. Professional gaming consoles, high refresh rate monitors and specialized gaming accessories experience steady demand because these products are essential for competitive gaming and streaming platforms.

Digital connectivity expansion and smartphone ecosystem development have emerged as critical factors which drive gaming device adoption. The International Telecommunication Union (ITU) and UNESCO digital culture initiatives report that more people can now play games because better internet access and digital literacy skills have improved their access to digital games. Consumers who want the best gaming experience create an ongoing demand for high performance graphics processors, virtual reality gaming systems and specialized gaming controllers, which in turn drives market growth for the long term.

Market Restraints / Challenges

The semiconductor supply chain issues and the concentration of manufacturing operations make it difficult for the market to operate despite its positive growth potential. The U.S. Department of Commerce Semiconductor Supply Chain Review and OECD reports show that gaming hardware production requires advanced semiconductor fabrication facilities which only exist in specific countries. The semiconductor supply chain disruptions result in higher production expenses, lower device supply and decreased gaming hardware manufacturer profits.

Device makers and distributors face operational difficulties because of the complex regulatory requirements and trade policy regulations which impact their ability to do business. The World Trade Organization (WTO) and national technology authorities publish technology trade reports which show that tariffs on electronic components and export controls on advanced chips create procurement uncertainties and pricing pressures. Businesses face delivery delays because they rely on imported chipsets, display components, memory modules which create scalability problems for their operations during global economic downturns.

Market Opportunities

The market presents significant opportunities in immersive gaming technologies and next generation hardware ecosystems. Government innovation initiatives such as the U.S. National Science Foundation digital technology programs and the Japan Ministry of Economy, Trade and Industry semiconductor development initiatives are promoting research in graphics processing, virtual reality systems, and interactive entertainment technologies. High performance gaming devices need to be developed to enable advanced rendering capabilities and real time simulation environments and interactive streaming platforms.

The opportunity to expand gaming usage exists because emerging digital economies show rising internet access rates which attract young people who want affordable gaming products. The International Telecommunication Union (ITU) and World Bank Digital Development Program report that digital infrastructure funding for Southeast Asia, Latin America and Middle East regions has improved internet access and device availability. Companies who sell modular gaming consoles, mid-range gaming laptops and cloud compatible devices can meet rising demand while creating lasting relationships with customers in the expanding digital entertainment industry.

Global Gaming Device Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 68.4 Billion |

|

Revenue Forecast in 2035 |

USD 148.3 Billion |

|

Growth Rate |

8.1% |

|

Segments Covered in the Report |

Product, Price, Distribution Channel, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Acer Inc., Advanced Micro Devices, Inc. (AMD), ASUSTeK Computer Inc., Corsair Gaming, Inc., Intel Corporation, Logitech International S.A., Microsoft Corporation, Nintendo Co., Ltd., NVIDIA Corporation, Sony Group Corporation |

|

Customization |

Available upon request |

Gaming Device Market Segmentation

By Product

The market in 2025 displayed its highest sales through PC gaming hardware which represented 46% of total market revenue. The segment maintains its leading position because of ongoing market demand for advanced gaming systems and desktop systems with unique configurations and premium gaming accessories. The industry experiences expansion through the rising use of competitive gaming platforms together with high resolution gaming displays which perform best with powerful processing systems. The International Telecommunication Union (ITU) and U.S. Federal Communications Commission (FCC) digital entertainment statistics show that broadband Internet access and gaming activities both grow in tandem, which drives sales of gaming computers and their accessories within professional and amateur gaming communities.

There PC Gaming Hardware further classified into followings

- Gaming Laptops

- Gaming Desktops

- Custom/DIY PC

- Peripherals

- Gaming Monitors

- Gaming Keyboards

- Gaming Mice

- Gaming Headsets

The console gaming hardware market will show consistent growth with a projected compound annual growth rate of 7.2% throughout the upcoming forecast period. The market for mainstream customers has improved through ongoing upgrades of gaming hardware together with new console models that feature cutting edge processors and graphical capabilities.

There Console Gaming Hardware further classified into followings

- Playstation

- Xbox

The market for handheld and portable gaming devices will expand at a compound annual growth rate of 8.3% because more people want to have entertainment systems that they can take anywhere and enjoy both portable and hybrid gaming modes.

The market for components together with internal gaming hardware will expand at a growth rate of 7.8% throughout the entire prediction period. The market demand for advanced gaming technology has increased because gamers now seek better processing power and improved graphics performance through high-performance graphics processing units central processing units advanced cooling solutions and high-speed memory modules.

There Components & Internal Hardware further classified into followings

- CPUs

- GPUs

- Motherboards

- RAM

- Storage (SSD, HDD)

- Power Supplies

- Cooling Systems (Air, Liquid)

- Cases

- Others

There VR further classified into followings

- VR Headset

- MR Headset

There Handheld/Portable Gaming Devices further classified into followings

- Steam Deck

- ROG ALLY

- Nintendo

- Others

By Price

The market in 2025 experienced its highest sales through the mid-range segment which generated approximately 41% of total market revenue. The segment provides users with both good performance and affordable pricing, thus attracting a wide range of recreational and dedicated gamers. The segment continues to grow because customers demand gaming laptops, monitors and peripherals that deliver excellent performance while remaining affordable. The Organization for Economic Co-operation and Development (OECD) consumer electronics adoption reports show that mid-priced gaming hardware remains the most widely purchased category among global gaming consumers.

The premium and flagship segments will experience faster growth throughout the forecast period, which will result in the two segments attaining CAGRs of 8.4% and 8.9% respectively. High-end gaming devices experience market growth because customers want to use displays with high refresh rates and advanced graphics performance, and they want to play virtual reality gaming technologies.

Budget gaming devices maintain stable demand, particularly in emerging economies where affordability remains a key purchasing factor. The segment will grow at a compound annual growth rate of 6.8% until the end of the forecast period, driven by the rising number of people who play games online and the expanding digital networks.

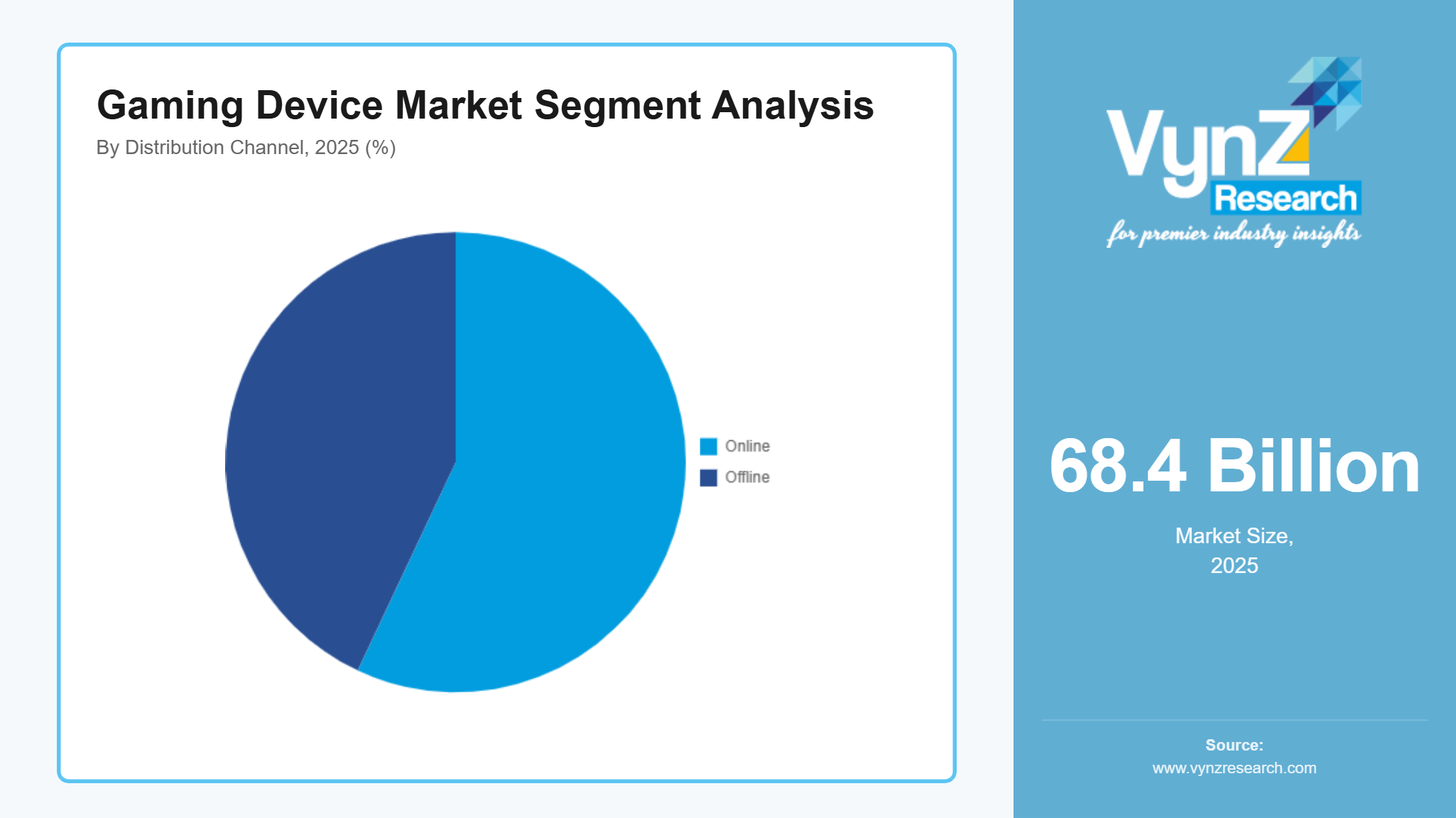

By Distribution Channel

The market in 2025 generated its highest revenue through offline retail channels which accounted for 57% of total earnings. Customers still depend on electronics retail shops and dedicated PC hardware stores to verify product details receive technical help and access post-purchase product assistance. The U.S. Department of Commerce reports on government digital commerce show that physical retail stores continue to play a vital role in high-value consumer electronics sales especially for gaming hardware which needs customers to determine its operational compatibility and performance capabilities.

There Offline further classified into followings

- Electronics Retail Stores

- IT & PC Speciality Stores

The market for online distribution channels will experience greater expansion because these channels will increase at an approximate compound annual growth rate of 8.6% during the assessment period. The worldwide market for gaming devices and components has become more accessible because e-commerce platforms have expanded and manufacturers now operate direct online stores.

There Online further classified into followings

- OEM Online Stores

- E-Commerce Retailers

By End User

Casual and hobbyist gamers represented the leading segment of the gaming device market in 2025 with their share of total market revenue reaching 49%. The segment benefits from a rapidly expanding global gaming population and rising accessibility of digital gaming platforms. The International Telecommunication Union (ITU) found that more people can access online gaming because internet users have increased and better broadband connectivity exists, especially for young people who use mobile devices as their primary digital platforms.

The core and enthusiast gaming market will expand at a 7.9% CAGR during the forecast period because gamers want systems with better graphics and immersive gameplay. The growth of esports in South Korea and Japan has created competitive gaming environments which lead to increased esports participation among digital sports competitors.

The esports and competitive gaming segment will achieve the highest growth rate, which will reach 9.2% CAGR until 2035. The South Korean Ministry of Culture, Sports and Tourism and the U.S. Department of Commerce digital entertainment programs have started to recognize esports as a legitimate institutional entity which leads to increased investments in professional gaming facilities.

There eSports and Competitive Gaming further classified into followings

- Creator -gamers

- Hybrid Users

Regional Insights

North America

The North American market reached a 2025 market share of 34% because consumers spent heavily on digital entertainment and advanced gaming technology ecosystems existed in the region. The United States produces the most gaming industry development because its major cities Los Angeles, San Francisco and Seattle serve as key gaming development centers and esports team bases and hardware development sites. The U.S. Department of Commerce reports show that the interactive entertainment industry and advanced semiconductor manufacturing sector continue to grow because both sectors drive market needs for gaming consoles, gaming computers and specialized gaming accessories.

The regional gaming hardware ecosystem receives additional support from government programs that promote digital innovations and semiconductor manufacturing activities. The U.S. CHIPS and Science Act introduce programs that enhance domestic semiconductor manufacturing capabilities which directly benefit the gaming processor and graphics chip supply chain. The Federal Communications Commission (FCC) released digital infrastructure data which shows that broadband service reaches most of North America while users can access fast internet which supports widespread use of cloud-based gaming and advanced gaming systems.

Asia Pacific

The market in Asia Pacific region reached a 30% market share for 2025 but this area now develops into one of the fastest expanding parts of the world because of its massive gaming population and developing esports ecosystems. The key markets for this region include China, Japan and South Korea while the cities of Seoul, Tokyo and Shanghai function as important centers for both gaming technology development and esports competition. The digital economy reports from China and South Korea show that the government now recognizes gaming and esports as essential digital industries for strategic development.

Public policies that support technological innovation and fast internet connectivity will increase the need for high-performance gaming equipment. The International Telecommunication Union (ITU) reports that the Asia Pacific region continues to expand its broadband network and digital services throughout the area. These improvements enable wider use of high-performance gaming systems, virtual reality devices, and portable gaming consoles across both casual and competitive gaming communities.

Europe

Europe accounts for 17% of the market in 2025 because established consumer electronics markets and increasing digital entertainment technology investments support its growth. Germany, the United Kingdom and France all provide essential contributions to the market which centers on Berlin, London and Paris as vital hubs for gaming industry development and esports activities. The European Commission Digital Strategy reports show that digital transformation and interactive entertainment technology innovation need to advance for gaming hardware and advanced computing devices to achieve market demand.

The region receives better support from government programs which focus on building digital infrastructure and creative industries to develop its entire gaming ecosystem. The European Commission leads broadband expansion programs and digital innovation initiatives which will enhance network connectivity and support high-performance computing systems. The industry reports that advanced gaming laptops, gaming consoles and gaming peripherals receive better adoption when both consumers and professional gamers use them.

Rest of the World

The Rest of the World includes Latin America, the Middle East and Africa which together make up 19% of the gaming device market for 2025. Rising internet access, growing youth demographics and people adopting digital entertainment services drive the development of these areas. The cities of São Paulo, Dubai and Johannesburg have developed into key markets for both gaming hardware sales and esports events. The World Bank Digital Development Program and International Telecommunication Union (ITU) reports show that digital infrastructure and mobile network availability have both improved in these regions.

Government programs that promote digital inclusion and technology adoption will create better gaming environments for emerging economies. The improvement of broadband networks together with digital literacy programs will enable more people to access gaming platforms and consumer electronics devices.

Competitive Landscape / Company Insights

The market has a competitive landscape which ranges from moderate competition to fierce battles between global and regional companies who compete through product development, pricing methods and market expansion efforts. Leading manufacturers are investing in advanced graphics processing technologies, immersive gaming hardware, and high-performance computing capabilities to strengthen their market position. Digital infrastructure expansion programs which the U.S. Department of Commerce has identified and the semiconductor development initiatives of the U.S. CHIPS and Science Act and ITU connectivity enhancements combine to create an environment which drives hardware demand and promotes industry innovation for next generation gaming devices.

Mini Profiles

Acer Inc. focuses on high-performance gaming laptops and desktops, supported by strong global distribution networks, recognized gaming brands such as Predator, and continuous hardware innovation that strengthens its presence in competitive gaming markets.

Corsair Gaming, Inc. operates in premium gaming hardware segments, emphasizing performance, customization, and high-quality peripherals including keyboards, headsets, and memory components, supported by strong brand recognition among enthusiast and esports gaming communities.

Intel Corporation leverages advanced semiconductor manufacturing and strategic partnerships with PC manufacturers to expand market presence, offering high-performance processors that power gaming computers and support advanced graphics and computing workloads.

NVIDIA Corporation focuses on graphics processing technologies and AI-driven gaming platforms, supported by extensive developer ecosystems, strong R&D capabilities, and global adoption of its GPUs across gaming computers, consoles, and cloud gaming infrastructures.

Sony Group Corporation operates in premium gaming ecosystems through its PlayStation platform, emphasizing immersive gaming experiences, exclusive content, and advanced console hardware supported by strong brand recognition and global gaming distribution networks.

Key Players

- Acer Inc.

- Advanced Micro Devices, Inc. (AMD)

- ASUSTeK

- Computer Inc.

- Corsair Gaming, Inc.

- Intel Corporation

- Logitech International S.A.

- Microsoft Corporation

- Nintendo Co., Ltd.

- NVIDIA Corporation

- Sony Group Corporation

Recent Developments

In March 2026, NVIDIA and Thinking Machines Lab has announced a multiyear strategic agreement to enable Thinking Machines' frontier model training and platforms that provide scalable, configurable AI by deploying at least one gigawatt of next-generation NVIDIA Vera Rubin systems. Early next year is when the NVIDIA Vera Rubin platform is expected to be deployed. Along with expanding access to frontier AI and open models for businesses, academic institutions, and the scientific community, the cooperation also aims to create training and serving systems for NVIDIA architectures.

In September 2026, ASUSTeK Computer Inc. revealed the "ASUS Dual GeForce RTX 5060 Ti 16GB GDDR7 White OC Edition that comes with the NVIDIA GeForce RTX 5060 Ti 16GB. Its backplate, has ventilation slots, which offers steady performance even when used for extended periods of time. In its white version, it has a 2.5-slot arrangement and two fans. The freshly introduced "ASUS Dual GeForce RTX 5060 Ti 16GB GDDR7 White OC Edition" increases cooling efficiency and ensures outstanding compatibility with its 2.5-slot architecture. It may also supply more air than a typical fan because it has an Axial-tech fan with a dual ball bearing mechanism. Additionally, it has 0dB Technology, which automatically turns off the fans when the GPU temperature drops below.

In August 2025, Acer collaborated with Plumage Solutions to increase local production of IT gear at the new facility in Puducherry. The investment is a component of Acer India's localization strategy, that aims to meet demand from urban and growing markets, lessen reliance on imports and increase domestic production. The collaboration marks a significant step in Acer’s commitment to the ‘Make in India’ mission as it is established under the Government of India’s Production Linked Incentive (PLI) Scheme for IT Hardware. Acer will be able to offer competitive pricing points, cut delivery times, and increase supply chain efficiency thanks to the Puducherry facility.

Global Gaming Device Market Coverage

Product Insight and Forecast 2026 - 2035

- PC Gaming Hardware

- Console Gaming Hardware

- Components & Internal Hardware

- VR

- Handheld/Portable Gaming Devices

Price Insight and Forecast 2026 - 2035

- Budget

- Mid-Range

- Premium

- Flagship

Distribution Channel Insight and Forecast 2026 - 2035

- Online

- Offline

End User Insight and Forecast 2026 - 2035

- Casual/Hobbyist Gamers

- Core/ Enthusiast Gamers

- eSports & Competitive Gamers

Global Gaming Device Market by Region

- North America

- By Product

- By Price

- By Distribution Channel

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Product

- By Price

- By Distribution Channel

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product

- By Price

- By Distribution Channel

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product

- By Price

- By Distribution Channel

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Gaming Device Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product

1.2.2. By

Price

1.2.3. By

Distribution Channel

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product

5.1.1. PC Gaming Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Console Gaming Hardware

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Components & Internal Hardware

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. VR

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Handheld/Portable Gaming Devices

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Price

5.2.1. Budget

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Mid-Range

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Premium

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Flagship

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Distribution Channel

5.3.1. Online

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Offline

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Casual/Hobbyist Gamers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Core/ Enthusiast Gamers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. eSports & Competitive Gamers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product

6.2. By

Price

6.3. By

Distribution Channel

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product

7.2. By

Price

7.3. By

Distribution Channel

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product

8.2. By

Price

8.3. By

Distribution Channel

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product

9.2. By

Price

9.3. By

Distribution Channel

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Acer Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Advanced Micro Devices, Inc. (AMD)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

ASUSTeK Computer Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Corsair Gaming, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Intel Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Logitech International S.A.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Nintendo Co., Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

NVIDIA Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Sony Group Corporation

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Gaming Device Market