Ocean-based Carbon Dioxide Removal Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Biological Approaches, Chemical Pathways, Electrochemical and Engineering Solutions, Storage and Hybrid Configurations), by Technology (Seaweed Cultivation and Sinking, Ocean Alkalinity Enhancement, Electrochemical Removal and Direct Ocean Capture, Biochar and Enhanced Mineralization), by Application (Carbon Sequestration and Offsetting, Oil and Gas & Power Generation, Government and Regulatory Programs, Coastal Protection and Biodiversity), by End Use (Industrial Users, Power Generation and Utilities, Government and Regulatory Bodies, Environmental Organizations and Research Institutes, Private Sector Corporates and Agricultural Stakeholders), by Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa)

| Status : Published | Published On : Apr, 2026 | Report Code : VRICT5227 | Industry : ICT & Media | Available Format :

|

Page : 160 |

Ocean-based Carbon Dioxide Removal Market Overview

The Ocean-based Carbon Dioxide Removal Market which was valued at approximately USD 0.85 billion in 2025 and is estimated to rise further up to almost USD 1.1 billion in 2026, is projected to reach around USD 3.2 billion in 2035, expanding at a CAGR of about 13% during the forecast period from 2026 to 2035.

The market is gaining structural momentum due to rising global carbon mitigation commitments, accelerating marine based sequestration research, and expanding climate finance mechanisms which support scalable negative emission technologies. The commercial deployment of ocean alkalinity enhancement, seaweed-based sequestration and electrochemical marine capture solutions has been strengthened through their growing use in pilot and early-stage facilities.

International climate governance frameworks and public climate financing programs provide strong backing to the market. The Intergovernmental Panel on Climate Change has emphasized the necessity of durable carbon removal pathways to achieve net zero targets while the United Nations Environment Program highlights the importance of nature based and ocean mediated sequestration in long term mitigation portfolios. The United States, Norway and Japan are using government-backed initiatives from their national decarbonization strategies to support funding for marine carbon capture demonstration projects. The expansion of voluntary carbon markets and rising corporate net zero commitments are driving demand across North America, Europe and Asia Pacific because regulatory clarity and environmental monitoring standards are advancing structured deployment.

Ocean-based Carbon Dioxide Removal Market Dynamics

Market Trends

The ocean-based carbon dioxide removal industry undergoes major technological transformations and regulatory changes in its operational systems. The market trend of ocean alkalinity enhancement and seaweed-based carbon sequestration systems development shows a preference for scalable and durable carbon removal approaches which help achieve net zero emissions targets. The Intergovernmental Panel on Climate Change published assessments which show that marine carbon sequestration functions as an essential method to achieve emissions reduction targets while providing systematic funding support to coastal economies.

The current trend involves organizations using electrochemical removal methods which digital monitoring systems support because these methods match regulatory requirements and environmental verification needs. The United Nations Environment Program requires carbon removal markets to use transparent measurement systems for carbon reporting which enables organizations to trace marine carbon emissions through specialized accounting tools. The developments are driving project design changes which lead operators to build their work on lifecycle validation plus environmental protection and long-lasting storage security to create stronger institutional trust in the industry.

Growth Drivers

The market grows because both national decarbonization commitments and climate neutrality targets become legally binding for countries to follow. The International Energy Agency demonstrates that carbon removal solutions function as essential tools for reducing emissions from industries that face major challenges. The rising public funding for climate innovation funds together with marine research infrastructure development is accelerating the progress of demonstration projects and early-stage commercialization efforts in coastal areas of developed countries.

The expansion of voluntary carbon markets acts as a fundamental factor which increases market participation. The demand for verified negative emission credits from marine pathways remains stable because multinational corporations now aim to meet science-based climate targets. The United Nations climate framework provides guidance which establishes high-integrity carbon accounting standards to help enterprises create sustainable platforms that combine permanent removal credits with their compliance-based transition plans.

Market Restraints / Challenges

The market encounters challenges because its regulatory structure depends on the marine ecosystem protection laws and environmental permitting requirements despite its positive market prospects. The Intergovernmental Oceanographic Commission under UNESCO requires environmental assessments before marine projects begin their work which results in more time needed for project approval and higher expenses to meet regulatory requirements. The regulatory framework establishes various rules which hinder growth potential for new maritime governance frameworks used by early-stage developers.

The operational environment becomes more difficult due to scientific uncertainty about how long-term ecological changes will affect the ecosystem. The deployment process requires implementation of advanced monitoring systems together with marine engineering expertise and ongoing environmental monitoring activities which lead to higher capital expenses. National ocean authorities demand continuous ecosystem impact evaluations which create ongoing compliance responsibilities that might affect profitability during periods of funding shortages or regulatory changes.

Market Opportunities

The large-scale coastal deployment programs which benefit from climate legislation and public climate finance support create major growth possibilities. The North American and Northern European governments now include marine carbon removal as part of their national climate innovation programs which establish designated funding streams to support pilot and pre-commercial project development. The industrial emitters who need lasting offset options are likely to choose providers who deliver both modular electrochemical systems and proven alkalinity enhancement technologies.

The integration of blue economy and coastal resilience strategies presents additional growth potential. The increase in sustainable maritime development investments is generating both blended financing options and enduring partnerships between financial institutions. The upcoming improvements in satellite-based ocean monitoring along with automated carbon flux measurement and digital verification systems will boost transparency while enhancing investor confidence which will benefit commercialization efforts in multilateral climate finance systems.

Global Ocean-based Carbon Dioxide Removal Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 0.85 Billion |

|

Revenue Forecast in 2035 |

USD 3.2 Billion |

|

Growth Rate |

13% |

|

Segments Covered in the Report |

Type, Technology, Application, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Arca Climate, Blue Planet System, Carbon Clean Solutions, Carbon Cure Technologies Inc, Carbon Engineering Ltd, Cella Mineral Storage, Climeworks AG, Equinor Carbofex Ltd, Mitsubishi Heavy Industries, Thermostat |

|

Customization |

Available upon request |

Ocean-based Carbon Dioxide Removal Market Segmentation

By Type

The biological approaches market segment achieved the highest market share in 2025, generating approximately 38% of overall revenue. The main reason for their market share exists because coastal regions are increasing their efforts to use macroalgae cultivation and blue carbon ecosystems for restoration purposes. The funding availability for nature-based carbon sinks has improved because government policies now recognize these carbon sinks under the Intergovernmental Panel on Climate Change framework and the United Nations Environment Program framework. The public research grants and coastal resilience programs currently support biological solutions, which are expected to grow at a 12.8% CAGR until 2035 because of their ability to scale and create ecosystem advantages.

The chemical pathways generated nearly 27% of market revenue in 2025, which investors now show growing interest in ocean alkalinity enhancement and mineralization technologies. Scientists about the long-term effectiveness of mineral based sequestration which led them to develop demonstration projects across North America and Europe. The deployment standards for projects are currently being determined through environmental protection regulations which define the criteria for regulatory assessment processes. The market segment will experience sustained growth of 13.2% because multiple carbon credit methodologies will achieve maturity and industrial partnerships will enhance their capacity to verify carbon credits.

The electrochemical and engineering solutions generated about 23% of total revenue for 2025, but they will experience the fastest growth at 14.1% for the upcoming forecast period. The system growth occurs through the combination of renewable energy sources with electrochemical capture systems and digital storage monitoring solutions which provide certified storage capabilities. The commercialization process received a boost from increased venture capital investments together with additional climate innovation funding. Research stage sequestration pilots and collaborative marine engineering programs supported by a 11.4% expansion rate accounted for 12% of the total storage and hybrid configuration space.

By Technology

Seaweed cultivation and sinking technologies held the largest share in 2025, contributing nearly 30% of total segment revenue. The combination of coastal farming pilot projects and established marine biomass accounting systems has driven the adoption of these practices. The international climate mitigation roadmaps now focus on biological sequestration methods which can be scaled up to enhance both scientific research partnership development and environmental research monitoring systems. The segment is projected to grow at 12.6% as lifecycle assessment methodologies improve and carbon market certification mechanisms evolve.

Ocean alkalinity enhancement accounted for around 24% of revenue, supported by mineral dissolution research and controlled field trials. Research institutes and industrial emitters have established partnerships which improve scientific validation for pilot projects to scale up operations. The technology is projected to grow at an annual rate of 13.4% because measurement standards and reporting standards are getting stronger.

Ocean storage electrochemical removal and direct air capture methods together created a 28% market share which is expected to grow at 14.3% because modular systems are becoming established through renewable energy system integration. Biochar and enhanced mineralization solutions created an 18% market share which is expected to grow at 11.7% because both the dual commercialization and policy-based research funding are progressing.

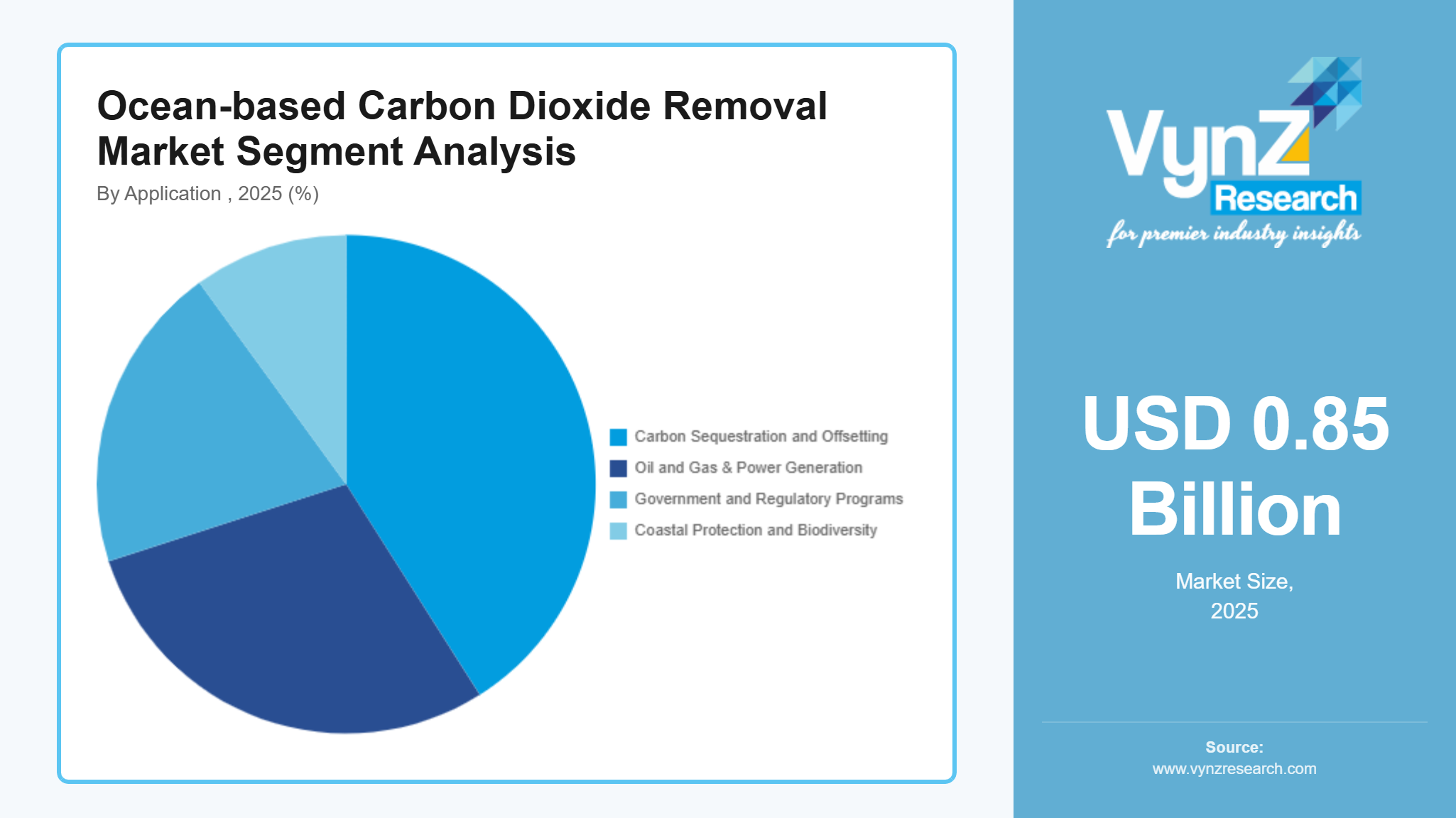

By Application

The carbon sequestration and offsetting applications led the market in 2025 as they generated close to 41% of total market revenue. The development of voluntary carbon markets generates demand which organizations want because their removal credits will meet international climate reporting standards. Corporate sustainability disclosures together with science-based targets create demand for structured procurement. The segment will grow at 13.1% because verification standards are becoming more developed while the number of long-term offtake agreements is increasing.

Oil and gas as well as power generation applications represented approximately 26% combined share, supported by decarbonization commitments and residual emission balancing requirements. Marine removal strategies have become part of industrial emissions reduction plans, leading to a growth rate of 12.4% in this sector. Public climate funding has led to a 12.9% growth rate for government and regulatory backed programs which currently account for 18% of the total programs available. Coastal protection and biodiversity linked applications, along with other niche uses, made up 15% of the total while ecosystem restoration activities advanced at a growth rate of 11.2%.

By End Use

Industrial users accounted for the largest share in 2025, representing roughly 36% of total revenue, supported by compliance driven decarbonization commitments and structured carbon accounting obligations. The demand for long term removal contracts from heavy industry will create better stability for demand. The segment will grow at 12.7% because the emission reduction pathways will include permanent sequestration technologies.

Utilities and power generation services generated almost 21% of total revenue which rose at 12.3% because utilities needed to meet their national net zero goals and renewable transition requirements. Climate finance distribution together with pilot funding systems has driven government and regulatory bodies to increase their share of this market from 12.9% to 17%. Environmental organizations and research institutes together accounted for 15% and are advancing at 11.8% supported by grant based marine research programs. Corporate stakeholders in the private sector and agricultural stakeholders made up 11% of the total, which is expected to rise at 13.5% because more businesses will participate in voluntary markets while carbon in-setting methods will grow in popularity.

Regional Insights

North America

The ocean-based carbon dioxide removal market in North America got 30% of its revenue in 2025. The region is seeing development because the government is making climate laws and the region has marine research systems. People are also participating in carbon markets through programs. The private sector is getting support for carbon capture projects through government tax benefits and climate innovation funding programs. Digital measurement and reporting systems are making verification standards better. This is increasing investor trust in carbon measurement systems. North America is really important for the ocean-based carbon dioxide removal market.

Europe

The market in Europe held 26% of its revenue in 2025. Europe is expanding because of the European Climate Law. This law is making climate targets. Innovation funding mechanisms are also optimizing negative emissions technology development. The marine protection standards need to be enforced. Public research institutions and environmental monitoring agencies will safeguard resources. The demand for ocean-based removal credits is increasing in Europe. This is because carbon trading systems and sustainability disclosure rules are expanding. Europe is taking steps to reduce carbon emissions.

Asia Pacific

The market in Asia Pacific contributed 24% of its revenue in 2025. Japan, Australia and South Korea are driving research activities in areas. Government agencies are investing in marine science infrastructure and carbon neutrality roadmaps. These roadmaps incorporate negative emission technologies. Japan’s green transformation policy framework and Australia’s marine research programs are supporting pilot deployment and technology validation. Asia Pacific is seeing a lot of development. The industrial sector needs to reduce carbon emissions. This is driving companies to invest in sequestration solutions. These solutions handle sustainability requirements. Academic partnerships and regional oceanographic institutes are empowering scientists.

Rest of the World

The Rest of the World including Latin America, the Middle East and parts of Africa represented 20% of market revenue in 2025. This region is experiencing development through resilience programs and blue economy strategies. Partnerships with climate finance institutions are also helping. Marine carbon initiatives that countries like Chile and the United Arab Emirates are exploring support their climate commitments and energy transition plans. The ocean-based carbon dioxide removal market is really important for these countries. Development banks and international environmental programs are providing funding and technical support for economic development.

Competitive Landscape / Company Insights

The market for carbon removal is pretty competitive with companies and new technology providers working on small tests forming partnerships and expanding to new places near the ocean. These companies are spending money on systems to catch bad stuff from the air platforms that use special chemicals to clean the air and digital tools to watch and check that everything is working. There are also funds from the government like the U.S. Department of Energy and groups, that help with new ideas to fight climate change and guidelines from the Intergovernmental Panel on Climate Change.

Mini Profiles

Arca Climate focuses on industrial mineralization of mine tailings, supported by strategic partnerships with global mining giants to transform waste into permanent, low-cost carbon storage solutions at scale.

Blue Planet System operates in premium construction material segments, emphasizing high-performance synthetic limestone aggregate that sequesters CO2 permanently, allowing developers to create carbon-negative concrete for infrastructure projects.

Carbon Clean Solutions leverages modular point-source technology and proprietary solvents to expand market presence, providing cost-effective decarbonization tools that slot easily into existing heavy industrial manufacturing footprints.

Equinor Carbofex Ltd operates in niche biochar and renewable energy segments, emphasizing high-purity carbon sequestration and heat recovery through co-developed projects that bridge traditional energy expertise with emerging climate technology.

Mitsubishi Heavy Industries leverages global manufacturing scale and deep engineering history to expand market presence, delivering large-scale post-combustion carbon capture plants for the world’s most demanding energy and industrial sectors.

Key Players

- Arca Climate

- Blue Planet System

- Carbon Clean Solutions

- Carbon Cure Technologies Inc

- Carbon Engineering Ltd

- Cella Mineral Storage

- Climeworks

- AG

- Equinor

- Carbofex Ltd

- Mitsubishi Heavy Industries

- Thermostat

Recent Developments

In January 2026, Climeworks AG continued scaling its direct air capture operations as global demand for durable carbon removal surged, positioning itself as a leader in large-scale CO₂ removal projects. The company is playing a central role in advancing verified carbon removal credits and long-term storage solutions.

In January 2026, Carbon Engineering Ltd expanded its large-scale carbon capture project pipeline, targeting multi-million-ton CO₂ removal capacity through partnerships and fuel synthesis initiatives. This development strengthens its role in bridging carbon removal with commercial fuel production and global carbon markets.

In March 2026, Mitsubishi Heavy Industries continued advancing carbon capture technologies as part of broader industrial decarbonization efforts, with increased deployment across energy and heavy industries. The company’s solutions are contributing to scalable carbon removal infrastructure aligned with global net-zero targets.

In February 2026, Carbon Clean Solutions expanded its modular carbon capture systems for industrial applications, focusing on cost-effective and scalable CO₂ removal technologies. This approach supports wider adoption across sectors and strengthens its position in emerging carbon removal markets.

In March 2026, Equinor Carbofex Ltd continued developing carbon storage and removal initiatives linked to offshore and ocean-based CO₂ sequestration projects. These efforts highlight the growing integration of ocean-based carbon removal with energy sector infrastructure to enable large-scale climate solutions.

Global Ocean-based Carbon Dioxide Removal Market Coverage

Type Insight and Forecast 2026 - 2035

- Biological Approaches

- Chemical Pathways

- Electrochemical and Engineering Solutions

- Storage and Hybrid Configurations

Technology Insight and Forecast 2026 - 2035

- Seaweed Cultivation and Sinking

- Ocean Alkalinity Enhancement

- Electrochemical Removal and Direct Ocean Capture

- Biochar and Enhanced Mineralization

Application Insight and Forecast 2026 - 2035

- Carbon Sequestration and Offsetting

- Oil and Gas & Power Generation

- Government and Regulatory Programs

- Coastal Protection and Biodiversity

End Use Insight and Forecast 2026 - 2035

- Industrial Users

- Power Generation and Utilities

- Government and Regulatory Bodies

- Environmental Organizations and Research Institutes

- Private Sector Corporates and Agricultural Stakeholders

Region Insight and Forecast 2026 - 2035

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Global Ocean-based Carbon Dioxide Removal Market by Region

- North America

- By Type

- By Technology

- By Application

- By End Use

- By Region

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Technology

- By Application

- By End Use

- By Region

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Technology

- By Application

- By End Use

- By Region

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Technology

- By Application

- By End Use

- By Region

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Ocean-based Carbon Dioxide Removal Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Technology

1.2.3. By

Application

1.2.4. By

End Use

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Biological Approaches

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Chemical Pathways

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Electrochemical and Engineering Solutions

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Storage and Hybrid Configurations

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Seaweed Cultivation and Sinking

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Ocean Alkalinity Enhancement

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Electrochemical Removal and Direct Ocean Capture

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Biochar and Enhanced Mineralization

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Carbon Sequestration and Offsetting

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Oil and Gas & Power Generation

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Government and Regulatory Programs

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Coastal Protection and Biodiversity

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Industrial Users

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Power Generation and Utilities

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Government and Regulatory Bodies

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Environmental Organizations and Research Institutes

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Private Sector Corporates and Agricultural Stakeholders

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. North America

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Europe

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Asia Pacific

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Latin America

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Middle East & Africa

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Technology

6.3. By

Application

6.4. By

End Use

6.5. By

Region

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Technology

7.3. By

Application

7.4. By

End Use

7.5. By

Region

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Technology

8.3. By

Application

8.4. By

End Use

8.5. By

Region

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Technology

9.3. By

Application

9.4. By

End Use

9.5. By

Region

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Arca Climate

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Blue Planet System

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Carbon Clean Solutions

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Carbon Cure Technologies Inc

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Carbon Engineering Ltd

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Cella Mineral Storage

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Climeworks AG

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Equinor Carbofex Ltd

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Mitsubishi Heavy Industries

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Thermostat

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Ocean-based Carbon Dioxide Removal Market