Edge AI for Smart Manufacturing Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Application (Predictive Maintenance, Quality Inspection, Production Optimization, Supply Chain Management, Others), by Deployment Type (On Premise, Cloud Integrated Edge), by End Use (Automotive, Electronics and Semiconductors, Healthcare and Medical Devices, Aerospace and Defense, Industrial Machinery, Others), by Region (North America, Europe, Asia Pacific, Rest of the World)

| Status : Published | Published On : May, 2026 | Report Code : VRICT5231 | Industry : ICT & Media | Available Format :

|

Page : 154 |

Edge AI for Smart Manufacturing Market Overview

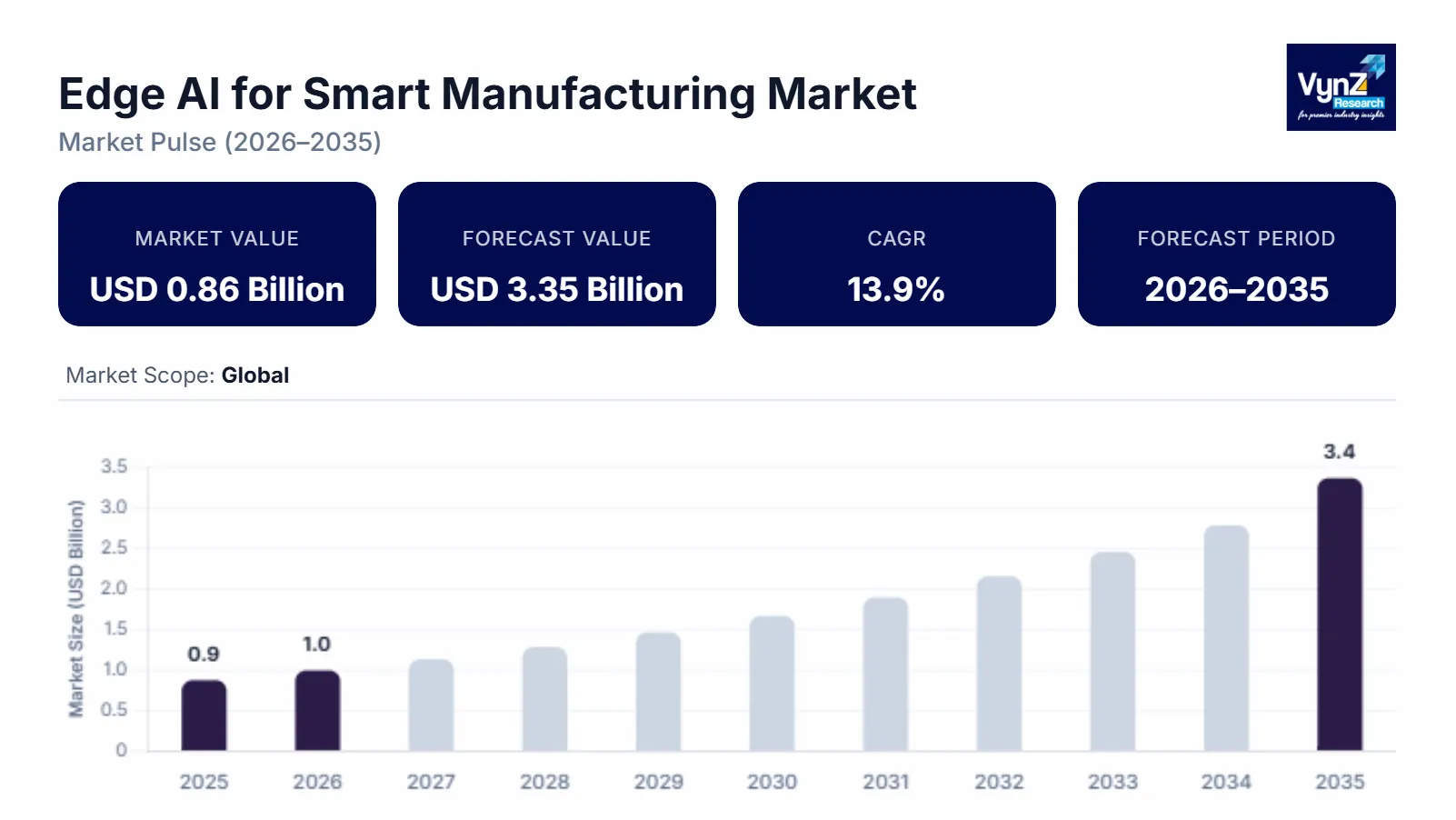

The edge AI for smart manufacturing market which was valued at approximately USD 0.86 billion in 2025 and is estimated to rise further up to almost USD 0.98 billion by 2026, is projected to reach around USD 3.35 billion in 2035, expanding at a CAGR of about 13.9% during the forecast period from 2026 to 2035.

The need for real-time data processing at device level, the growth of industrial automation with IIoT systems, the need for predictive maintenance to decrease operational downtime and the increasing use of edge AI technology in manufacturing operations all drive market expansion. Industrial facilities that handle large operations need efficient production processes with fast decision times and secure data protection which leads to their increasing adoption of new technologies. The industry expansion receives additional support from ongoing digital industrial transformation funding and smart factory project implementation across major global economies.

Government supported programs which promote advanced manufacturing technologies and AI integration methods are accelerating technology adoption through industry 4.0 implementation and national digitalization initiatives. Global institutions like the World Health Organization demonstrate how resilient technology enabled manufacturing systems have become essential for healthcare and medical device production supply chains. The industrial AI infrastructure market is expanding in Asia Pacific, North America and Europe because companies are investing more into industrial AI and adopting decentralized computing systems.

Edge AI for Smart Manufacturing Market Dynamics

Market Trends

The sector is experiencing substantial technological transformations along with new data processing methods which utilize edge artificial intelligence technology. Real-time edge analytics have emerged as a primary market trend because customers now prefer systems which deliver instant results while improving efficiency and security in production activities. The automated production lines now require immediate insights because they need real-time information to maintain product quality and enhance production processes.

The creation of AI systems which work with industrial Internet of Things networks became a major industry trend which emerged because of digital transformation and government support for Industry 4.0 development. The new developments create demand for product development because they lead companies to develop integrated products which combine hardware, software, and analytics solutions. The World Health Organization and other international bodies developed policy frameworks which emphasize that production systems must achieve both digital resilience and operational resilience particularly for healthcare manufacturing because it drives adoption of edge computing technology.

Growth Drivers

The market develops through edge AI technology which receives support from industrial automation these days because the technology creates permanent market demand in automotive, electronics, and healthcare manufacturing. Smart factory implementation and digital infrastructure development create market growth because businesses use real-time data to optimize their operations while controlling their productivity.

The predictive maintenance trend creates a demand that drives industry adoption of AI-based monitoring and fault detection systems. AI-powered monitoring and fault detection solutions will maintain strong market demand throughout the forecast period because enterprises now seek cost-effective solutions which maintain their operational activities. The advanced manufacturing and digital transformation programs which the government supports, together with the institutional backing for technology-driven industrial ecosystems, create a strong demand foundation for major economies.

Market Restraints / Challenges

The market shows excellent growth potential but several obstacles stand in its way of reaching its full market potential. The market continues to face two main challenges which make market entry difficult for small and medium-scale manufacturers who have restricted budget resources. The implementation process becomes more difficult because businesses need specialized infrastructure which must work with their current legacy systems.

The AI and advanced analytics shortage of skilled workers create operational difficulties for both manufacturers and solution providers. Technology companies which depend on outside technology experts and advanced semiconductor parts experience cost difficulties because their growth needs workability must be maintained during supply chain interruptions. The complete data privacy aspect and the industrial cybersecurity element which multiple government and institutional guidelines described create sector-specific adoption barriers.

Market Opportunities

Smart factory ecosystem expansion presents major market opportunities because industrial digitalization increases and demand for autonomous production systems becomes stronger. Scalable edge AI companies which deliver high performance solutions enable large enterprises and mid-sized manufacturers to enter the market.

Healthcare and precision manufacturing fields provide another main opportunity because their rising demand for specialized digital production systems enables businesses to create valuable new products. The combined development of edge computing, AI chipsets, and industrial analytics platforms will create better system performance which allows for real-time operational decision making. Public investment in advanced manufacturing technologies together with government-sponsored innovation programs will drive long-term growth for all industrial sectors throughout the world.

Global Edge AI for Smart Manufacturing Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 0.86 Billion |

|

Revenue Forecast in 2035 |

USD 3.35 Billion |

|

Growth Rate |

13.9% |

|

Segments Covered in the Report |

Component, Application, Deployment Type, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Cisco Systems, Inc., General Electric Company, Hewlett Packard Enterprise Development LP, IBM Corporation, Intel Corporation, Microsoft Corporation, NVIDIA Corporation, Rockwell Automation, Inc., Siemens AG, Zebra Technologies Corporation |

|

Customization |

Available upon request |

Edge AI for Smart Manufacturing Market Segmentation

By Component

The market in 2025 received its largest market share through hardware which generated around 48% of total revenue. The technology maintains its market position through the extensive installation of edge devices, industrial sensors and AI processors which handle real time data processing and local decision-making in production facilities. The adoption of hardware technology is increasing across major economies because industrial companies are investing in automation infrastructure and governments are implementing digital manufacturing programs. Smart factories require on-site computing resources to meet their need for quick processing and safe data management because both of these factors are becoming more essential.

The software sector will achieve the highest growth rate according to projections which estimate its compound annual growth rate will reach 14.6% between 2026 and 2035. The increasing use of AI algorithms in predictive maintenance and quality control combined with the need for better scalable analytics solutions drives market expansion. Industrial manufacturing software deployment is growing because AI frameworks have been established across industries and industrial AI frameworks have been linked to cloud systems. The service sector is experiencing growth because companies need system integration services and lifecycle management services, which helps the segment expand at a compound annual growth rate of 13.2%.

By Application

Predictive maintenance accounted for the largest market share in 2025, representing approximately 34% of total revenue. The technology received its major market demand because it helps organizations reduce maintenance expenses and equipment downtime through its real time assessment capabilities and its early fault detection technology. The resource optimization standard which manufacturing industries must follow receives implementation support from the industrial efficiency programs which the government supports. The local machine data processing capability of edge AI systems enhances operational reliability which makes predictive maintenance crucial for all industrial sectors.

Quality inspection is expected to witness the fastest growth, registering a CAGR of 14.9% during the forecast period. Production accuracy improves through the use of computer vision and AI defect detection systems which leads to a decline in production waste. Resource allocation efficiency and streamlined logistics requirements drive steady growth for production optimization and supply chain management applications. The two applications will experience growth through CAGRs of 13.5% and 13.1% which indicates that AI-driven decision-making is becoming more common in manufacturing processes.

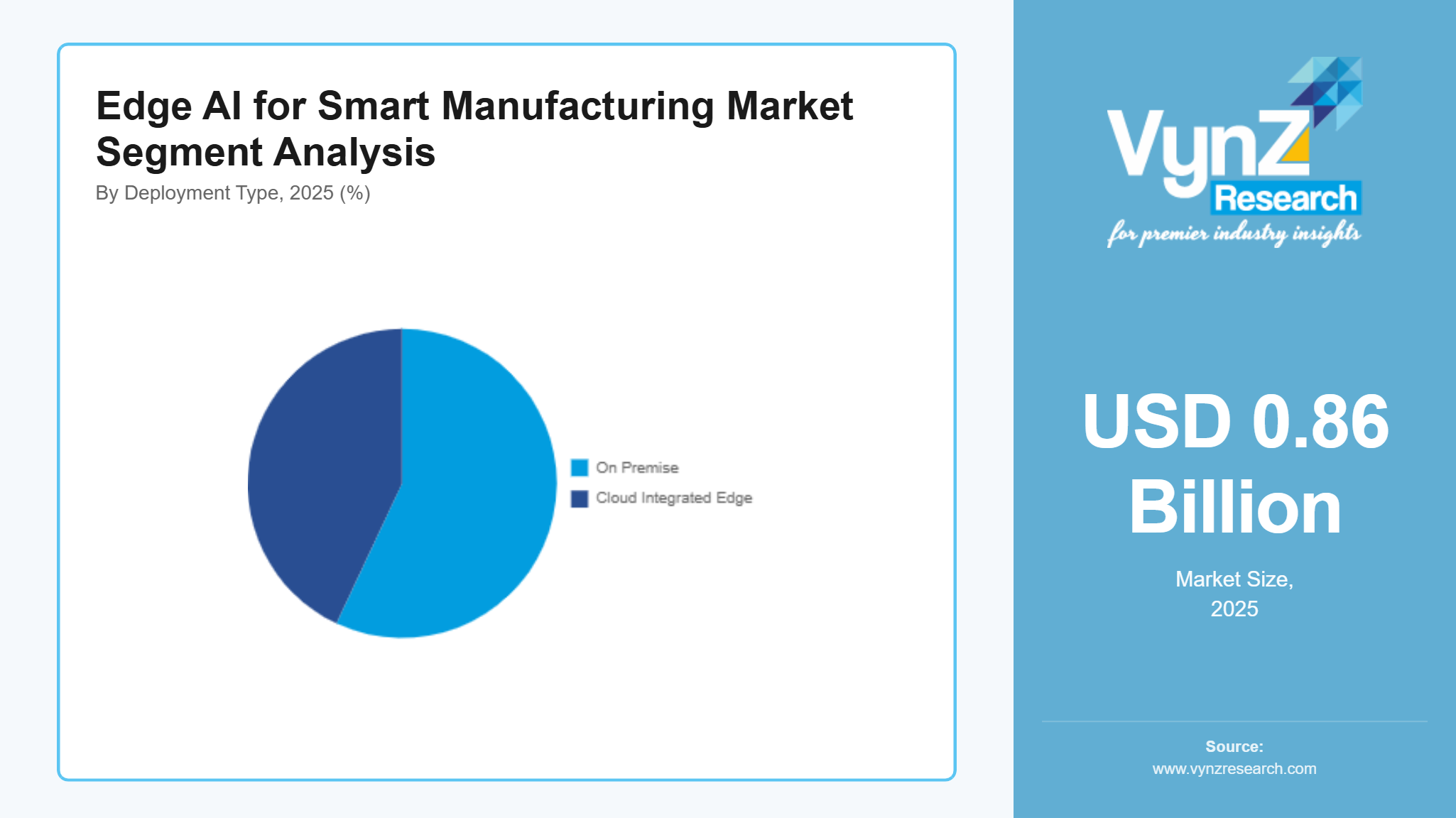

By Deployment Type

The on-premise deployment method had the biggest market share in 2025 with its revenue share reaching approximately 57% of total market revenue. The industrial sector needs secure data processing solutions which provide low latency times and complete operational control to protect its existing market position. The manufacturing industry requires local computing systems to meet data governance requirements and maintain their business operations without interruptions. The preference for on-premises deployment in critical manufacturing sectors gets reinforced through government regulations which protect industrial data security and safeguard infrastructure resilience.

The cloud integrated edge deployment method will achieve the highest growth rate with its estimated compound annual growth rate of 14.4% for the forecast period. Organizations need hybrid computing systems which deliver immediate edge processing capabilities together with centralized cloud data analysis, which drives system growth. Manufacturing operations can achieve better results through cloud platform integration which provides scalability options, remote monitoring features and data-driven insights. The industrial market is experiencing a surge in hybrid deployment model adoption because digital infrastructure and industrial connectivity investments are increasing for both large corporations and medium-sized manufacturing businesses.

By End Use

Automotive manufacturing held the biggest market share in 2025 through its contribution of approximately 29% of total market revenue. The technology maintains its market position through the extensive installation of edge devices, industrial sensors and AI processors which handle real time data processing and local decision-making in production facilities. Government initiatives which promote smart mobility and advanced manufacturing applications create a favorable environment for automotive production facilities to implement edge AI technologies. The segment continues to experience demand because companies need precise engineering methods and systems that continuously enhance their operational processes.

The electronics and semiconductor manufacturing sector will experience the highest growth rate with a projected compound annual growth rate of 15.1% between 2026 and 2035. The rising need for advanced precision quality control systems drives market growth because production processes have become more complicated. The healthcare and medical device manufacturing, aerospace, defense and industrial machinery sectors are experiencing steady market growth because they need to meet regulatory standards and improve their operational efficiency. The various industries will experience market growth with compound annual growth rates between 12.8% and 13.6%, which will lead to overall market expansion.

Regional Insights

North America

North America is predicted to capture about 30% of the market in 2025 because of its advanced industrial automation system, high AI technology adoption rate and presence of major technology companies. United States and Canada industrial centers show continuous growth in edge computing technology adoption for their automotive, electronics and aerospace manufacturing operations. The combination of government programs that back advanced manufacturing and digital transformation and National Institute of Standards and Technology smart manufacturing standardization initiatives leads to increased funding for AI powered industrial systems. The regional market performance receives support from businesses that concentrate on improving their operational efficiency and cybersecurity and developing strong supply chain networks.

Europe

Europe supplied around 25% of the market in 2025 because its industrial ecosystems operate with established systems, data security and industrial operation regulations function as strong regulatory frameworks. The countries of Germany, France and Italy are experiencing gradual adoption of edge AI technology through their precision manufacturing and industrial automation industries. The region experiences growth because its digital innovation programs and sustainability focused manufacturing initiatives receive policy backing. The automotive and industrial machinery industries encourage companies to build smart factories through their regulatory requirements and financial backing which drives ongoing demand for advanced edge computing technologies.

Asia Pacific

Asia Pacific is expected to have about 22% of the market in 2025 because countries like China, India, Japan and South Korea develop their digital infrastructure and their manufacturing sector and their industrial base expands. The industrial zones implement AI driven automation systems to boost their productivity while they work to stay competitive with international markets. The government backed initiatives that support industry 4.0 adoption together with AI integration programs for manufacturing processes boost regional deployment speed. The smart factory trend creates long term business opportunities because companies need cost efficient production systems.

Rest of the World

The global market for 2025 reached approximately 23% from all regions which includes Latin America, the Middle East and Africa. The regions experience growth as emerging economies raise their industrial infrastructure spending and begin to adopt automation technologies. The regions show progress as countries start to use AI solutions for better production processes and lower their manufacturing expenses. Government programs for industrial diversification and digital transformation drive slow but steady market growth.

Competitive Landscape / Company Insights

The market maintains a moderate level of competition because both international and local companies compete through their product development efforts, strategies for setting prices and expanding into new regions. The market position of companies improves through their increased spending on research and development combined with their digital capability enhancements. The National Institute of Standards and Technology and international standards organizations create government-backed frameworks which institutions use to promote secure and scalable AI deployment. The manufacturing ecosystems of strategic partnerships and industrial collaborations provide key advantages which companies use to improve their competitive position.

Mini Profiles

Cisco Systems, Inc. focuses on industrial networking and edge computing solutions, supported by strong global distribution capabilities and enterprise level brand recognition across manufacturing and digital infrastructure ecosystems.

General Electric Company operates in industrial and niche manufacturing segments, emphasizing performance driven automation, predictive analytics, and advanced digital solutions for large scale industrial operations.

Hewlett Packard Enterprise Development LP leverages hybrid cloud platforms, edge computing infrastructure, and strategic partnerships to expand market presence across smart manufacturing and industrial digitalization environments globally.

IBM Corporation focuses on AI driven analytics and industrial software solutions, supported by strong research capabilities, enterprise client base, and advanced digital integration across manufacturing value chains.

NVIDIA Corporation operates in high performance computing segments, emphasizing GPU accelerated AI platforms, real time processing capabilities, and scalable solutions for edge based industrial applications.

Key Players

- Cisco Systems, Inc.

- General Electric Company

- Hewlett Packard Enterprise Development LP

- IBM Corporation

- Intel Corporation

- Microsoft Corporation

- NVIDIA Corporation

- Rockwell Automation, Inc.

- Siemens AG

- Zebra Technologies Corporation

Recent Developments

In January 2026, Siemens AG expanded its industrial AI capabilities through enhanced integration of edge computing within smart factory environments. The development focuses on improving digital twin accuracy and enabling real time production optimization across manufacturing operations.

In September 2025, Intel Corporation introduced new edge optimized processors designed for industrial automation and AI driven manufacturing systems. These solutions improve low latency processing and support scalable deployment across smart factory infrastructures.

In October 2025, Rockwell Automation, Inc. strengthened its smart manufacturing portfolio by integrating advanced analytics and AI based monitoring solutions. The initiative enhances predictive maintenance capabilities and supports efficient industrial process management.

In August 2025, Hewlett Packard Enterprise Development LP expanded its edge to cloud platform offerings to support industrial AI workloads. The development enables improved data processing efficiency and seamless integration across manufacturing ecosystems.

In December, 2025, Zebra Technologies Corporation advanced its real time asset tracking solutions using AI enabled edge devices. The upgrade supports enhanced visibility, operational efficiency, and automation across manufacturing and supply chain environments.

Global Edge AI for Smart Manufacturing Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Application Insight and Forecast 2026 - 2035

- Predictive Maintenance

- Quality Inspection

- Production Optimization

- Supply Chain Management

- Others

Deployment Type Insight and Forecast 2026 - 2035

- On Premise

- Cloud Integrated Edge

End Use Insight and Forecast 2026 - 2035

- Automotive

- Electronics and Semiconductors

- Healthcare and Medical Devices

- Aerospace and Defense

- Industrial Machinery

- Others

Region Insight and Forecast 2026 - 2035

- North America

- Europe

- Asia Pacific

- Rest of the World

Global Edge AI for Smart Manufacturing Market by Region

- North America

- By Component

- By Application

- By Deployment Type

- By End Use

- By Region

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Application

- By Deployment Type

- By End Use

- By Region

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Application

- By Deployment Type

- By End Use

- By Region

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Application

- By Deployment Type

- By End Use

- By Region

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Edge AI for Smart Manufacturing Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Application

1.2.3. By

Deployment Type

1.2.4. By

End Use

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Application

5.2.1. Predictive Maintenance

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Quality Inspection

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Production Optimization

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Supply Chain Management

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Others

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Deployment Type

5.3.1. On Premise

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cloud Integrated Edge

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Automotive

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Electronics and Semiconductors

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Healthcare and Medical Devices

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Aerospace and Defense

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Industrial Machinery

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Others

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. North America

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Europe

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Asia Pacific

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Rest of the World

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Application

6.3. By

Deployment Type

6.4. By

End Use

6.5. By

Region

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Application

7.3. By

Deployment Type

7.4. By

End Use

7.5. By

Region

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Application

8.3. By

Deployment Type

8.4. By

End Use

8.5. By

Region

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Application

9.3. By

Deployment Type

9.4. By

End Use

9.5. By

Region

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Cisco Systems, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

General Electric Company

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Hewlett Packard Enterprise Development LP

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

IBM Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Intel Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Microsoft Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

NVIDIA Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Rockwell Automation, Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Siemens AG

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Zebra Technologies Corporation

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Edge AI for Smart Manufacturing Market