Geospatial Intelligence Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Offering (Hardware, Software, Services), by Technology (Remote Sensing, Geographic Information Systems, Global Positioning Systems), by Application (Defense and Security, Urban Planning, Environmental Monitoring, Disaster Management), by Vertical (Government and Defense, Energy and Utilities, Transportation and Logistics, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRICT5230 | Industry : ICT & Media | Available Format :

|

Page : 195 |

Geospatial Intelligence Market Overview

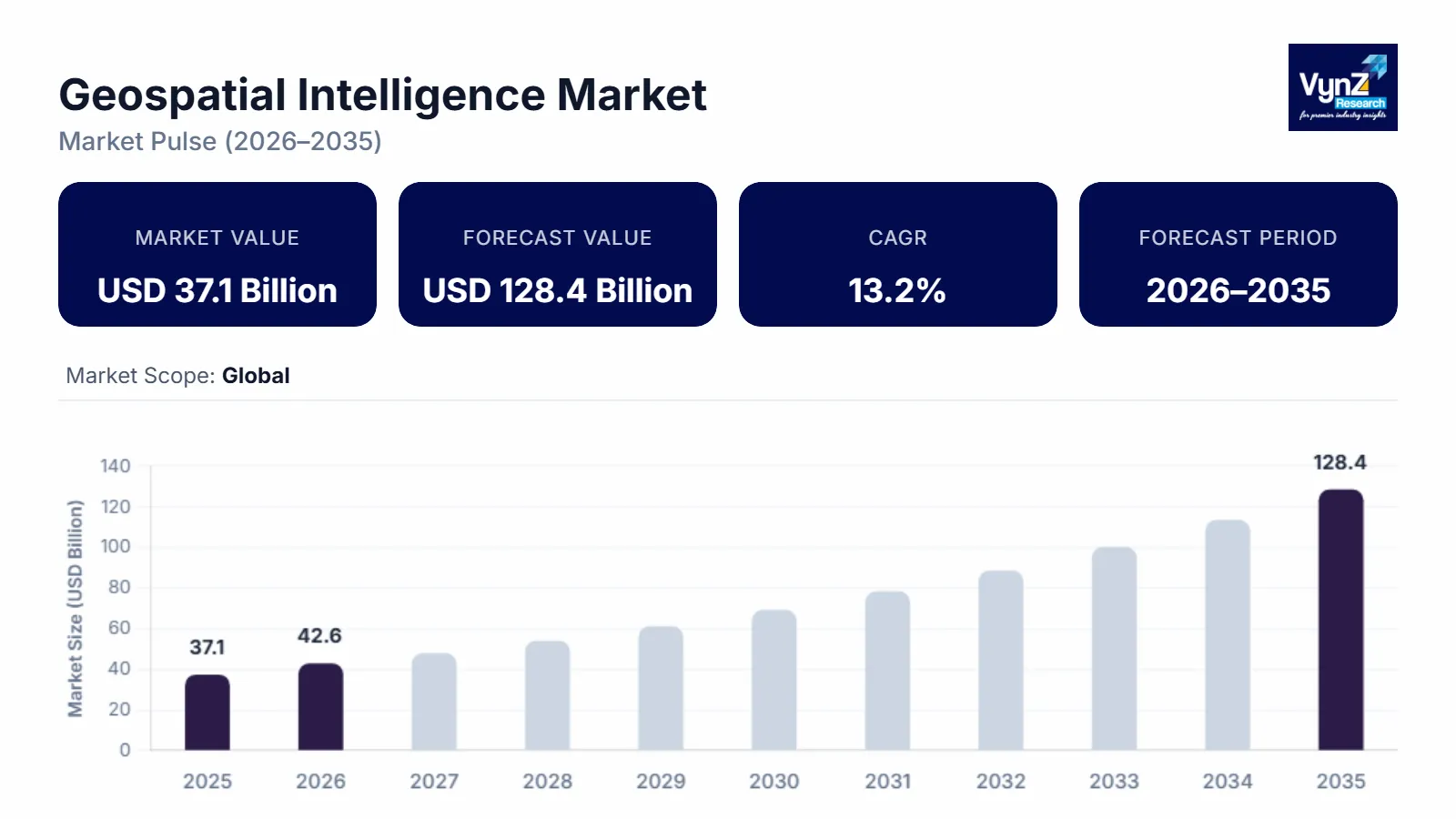

The global geospatial intelligence market which was valued at approximately USD 37.1 billion in 2025 and is estimated to rise further up to almost USD 42.6 billion by 2026, is projected to reach around USD 128.4 billion in 2035, expanding at a CAGR of about 13.2% during the forecast period from 2026 to 2035.

The market experiences growth because the demand for real-time geospatial data analysis shows an upward trend along with the increasing use of artificial intelligence in spatial intelligence systems and the growing adoption of cloud-based geospatial platforms. The ongoing development of national geospatial policies and digital mapping programs together with the rising requirement for location-based decision support systems in urban planning, disaster management and infrastructure monitoring activities, results in market expansion across major regions including the United States, China, and India.

The geospatial intelligence landscape receives global strengthening through government-backed initiatives which establish operational frameworks in developing countries. The World Health Organization and other United Nations organizations have shown that geospatial data provides essential support for the public health surveillance system and epidemic tracking system and environmental monitoring system which increases its strategic importance. The national geospatial data policies, satellite imaging programs and smart city missions which government agencies support, together with the enhancement of data accessibility and interoperability standards, have improved data accessibility and interoperability standards. The market growth receives a boost through increased funding which supports earth observation systems, defense intelligence modernization and digital infrastructure development in regions that implement geospatial capabilities for governance, climate resilience planning and national security frameworks.

Geospatial Intelligence Market Dynamics

Market Trends

The industry experiences significant transformation because organizations now adopt new technology and use data-based decision systems, which resulted from the rapid digital changes and increased use of spatial analytics in essential industries. The market now integrates artificial intelligence and machine learning technologies with geospatial platforms because organizations increasingly prefer predictive analytics and automation tools for real-time situational awareness. Public systems need to implement geospatial intelligence for climate monitoring and epidemiological tracking and disaster response planning, which United Nations and World Health Organization frameworks support as essential elements of their research requirements.

The rising digital penetration of society and the need for better data processing capacity drive the development of geographical cloud systems for processing visual information. The current trends are changing product offerings because companies now develop platforms which integrate satellite data with real-time analysis and data systems that can work together, which creates new market competition. The combination of digital mapping projects with national spatial data infrastructure systems and satellite observation programs will drive technology adoption in areas that need smart governance and environmental monitoring and infrastructure digitization.

Growth Drivers

The market grows because defense systems and urban planning activities and environmental monitoring tasks now require location-based analytics systems, security intelligence systems and advanced surveillance systems. The market growth rate accelerates because organizations invest in digital network systems, satellite technology and smart city development projects. National geospatial policies and open data programs enable government agencies to develop spatial data ecosystems which connect public institutions and private enterprises through shared spatial data across major economies.

Disaster risk management has become essential for organizations, which drives them to develop climate resilience plans to protect their assets. The demand for advanced geospatial intelligence solutions will remain strong during the entire forecast period because enterprises and governments need these technologies to achieve operational efficiency, predictive capacities and regulatory compliance. The World Meteorological Organization and other institutional bodies show how institutions now use geospatial technologies to create weather forecasts and plan disaster responses and build sustainable environmental systems, which contributes to market growth in the long term.

Market Restraints / Challenges

The market shows strong growth potential at present, but the industry faces certain obstacles which will restrict its future growth. The market faces challenges which emerge from two main factors, which include data privacy issues, regulatory requirements that especially affect sensitive geospatial and surveillance data in different regions. Service providers need to face compliance difficulties because satellite image regulations, cross border data transfer restrictions and national security rules create requirements for use in markets with strict regulatory requirements.

The organization must meet operational challenges because its employees depend on both advanced technological systems and specialized knowledge. Organizations which depend on overseas software and satellite systems with high-resolution graphics, and geospatial professionals with special training, will encounter financial problems and difficulty in scaling their business. Reports and policy frameworks created by European Commission organizations show how developing regions suffer from technological infrastructure and workforce differences, which delay the adoption of digital transformation during its initial stages.

Market Opportunities

The market offers major chances, which will increase geospatial intelligence usage in smart cities and infrastructure management systems, because urban areas keep growing and the government supports digital transformation initiatives. Government agencies and infrastructure developers will need to adopt geospatial solutions, which provide cloud-based systems and scalable high-performance capabilities. Organizations which handle land management, smart mobility and environmental sustainability, will create powerful demand for spatial analytics, which advanced platforms deliver.

The defense sector presents opportunities for growth, because defense modernization programs and space-based intelligence systems now use satellite technology for real-time surveillance. Advanced artificial intelligence analytics systems combined with automated mapping systems and real-time data visualization tools will create operational efficiency improvements, which will lead to better decision-making results. The Indian Space Research Organization and government-backed space program investments will develop geospatial infrastructure growth in emerging markets and developed economies, which will boost market potential in both regions.

Global Geospatial Intelligence Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 37.1 Billion |

|

Revenue Forecast in 2035 |

USD 128.4 Billion |

|

Growth Rate |

13.2% |

|

Segments Covered in the Report |

Offering, Technology, Application, Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Alteryx, Inc., Caliper Corporation, Esri, Fugro N.V., General Electric Company, Hexagon AB, IBM, Precisely, TomTom, Trimble Inc |

|

Customization |

Available upon request |

Geospatial Intelligence Market Segmentation

By Offering

The hardware segment achieved the most substantial market share in 2025 with 47% of total revenue which resulted from widespread satellite system and GPS device and sensing platform deployment in defense and environmental monitoring uses. Government spending on satellite systems and earth observation initiatives which agencies like NASA support creates ongoing demand for advanced hardware systems in all major global markets.

Software will experience the fastest growth rate which will achieve a compound annual growth rate of 14.2% during the period that runs from 2026 until 2035 because more businesses adopt geospatial analytics platforms together with artificial intelligence powered spatial data processing solutions. The operational efficiency of urban planning and logistics operations improves through the growing adoption of cloud mapping systems and predictive analytics tools.

The services sector shows consistent growth because more businesses require consulting and integration and maintenance services which help drive 12.8% growth particularly in public sector digital transformation projects.

By Technology

Remote sensing technology captured the largest segment of the market in 2025 by delivering approximately 45% of total segment revenue through its widespread implementation of satellite imagery and aerial surveillance systems for military operations and environmental monitoring and disaster management purposes. Government agencies use both developed and emerging regions to adopt satellite missions and imaging programs which receive backing from governmental institutions.

Geographic information systems will experience the highest growth rate of 14.5% because businesses need spatial analytics which delivers real time results and data visualization capabilities while working together with artificial intelligence technologies. Smart city projects and infrastructure digitization initiatives drive further adoption expansion.

Global positioning systems show continuous market growth because their navigation and tracking and location-based services create an estimated growth rate of 12.6% which benefits the transportation and logistics industries.

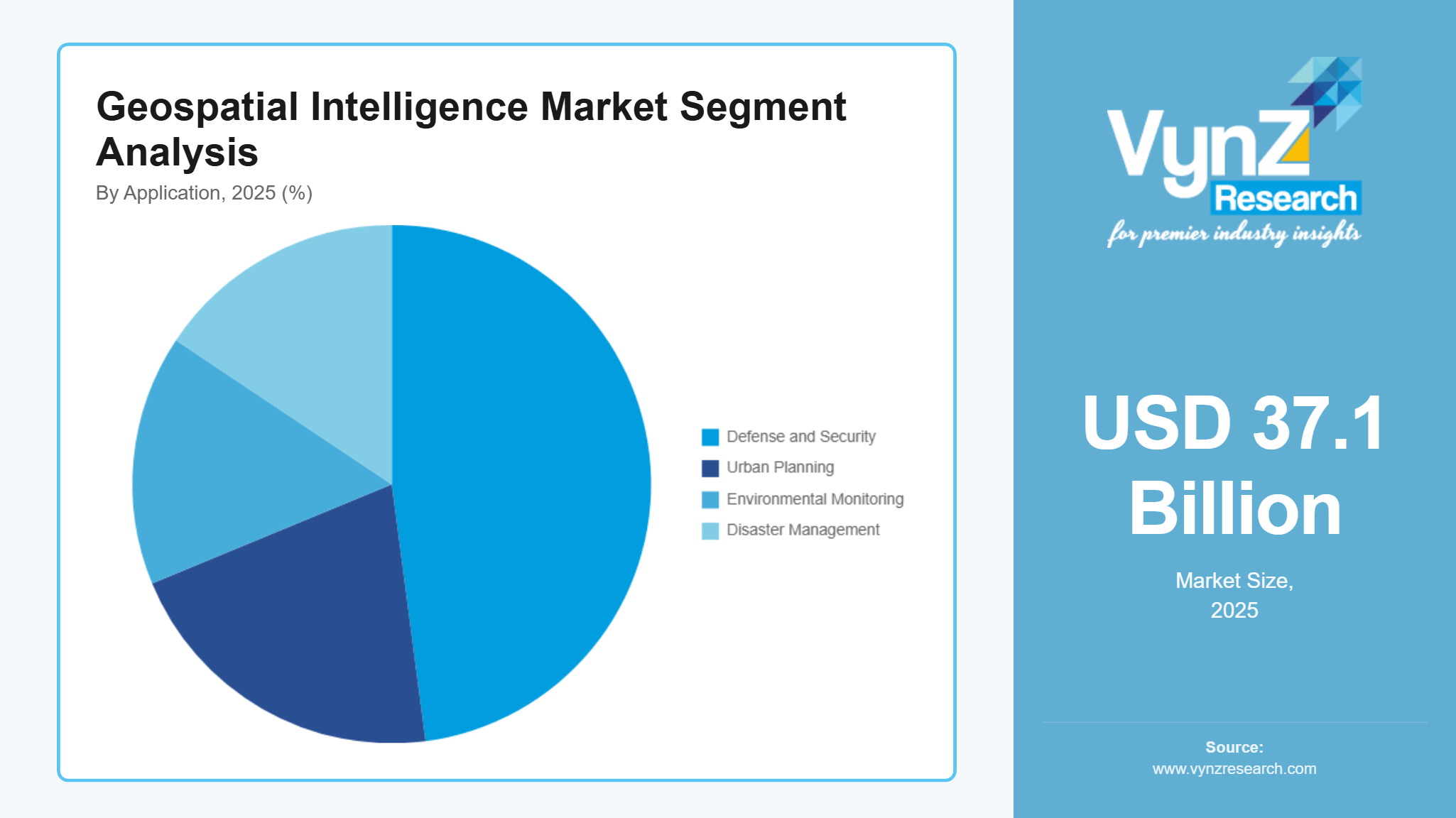

By Application

The defense and security sector captured the biggest market share in 2025 which reached 46% of total revenue because countries expanded their investments in surveillance systems and intelligence operations and border protection technologies. Government agencies establish geospatial intelligence solutions to boost their operational capacity which enables them to achieve better situational awareness.

The urban planning sector will grow at the strongest pace in 2026 to 2035 with a projected compound annual growth rate of 14.7% which results from urban centers experiencing rapid growth and smart city systems becoming more common. The segment expansion proceeds through investments that enhance infrastructure planning and traffic management systems and land use optimization.

The United Nations Environment Programs for climate resilience together with their institutional framework systems lead to continuous growth in environmental monitoring and disaster management applications which achieve a 13.3% growth rate.

By Vertical

The government and defense sector generated the most revenue in 2025 which accounted for 51% of total market revenues because government agencies maintained their national security spending, satellite system investments and spatial data infrastructure development. National geospatial policies and defense modernization programs continue to reinforce adoption across major regions.

The transportation and logistics sector will experience the highest growth rate during the forecast period with an estimated compound annual growth rate of 14.6% because businesses need systems that optimize routes and manage fleets and track shipments in real-time. The combination of geospatial intelligence and digital logistics platforms improves operational performance while supporting better decision-making abilities.

The energy and utilities sector together with other business sectors achieves stable market growth through their infrastructure monitoring and resource management and asset tracking applications which experience an estimated growth rate of 12.9% and drive overall market growth.

Regional Insights

North America

The market in North America reached 30% share by 2025 because defense spending, satellite infrastructure development and spatial analytics usage in public and private sectors continue to grow. Washington D.C., New York and Los Angeles function as major urban centers which drive geospatial intelligence system implementation in defense activities and urban planning work and environmental monitoring operations. The National Aeronautics and Space Administration together with federal agencies through their policy frameworks allocate government funding to develop earth observation systems and spatial data infrastructure.

Europe

The market in 2025 received 23% of its value from Europe which benefits from strong regulatory frameworks, environmental monitoring requirements and advanced digital infrastructure in Germany, the United Kingdom, France and Italy. Geospatial intelligence adoption in urban development, climate monitoring and transportation planning sectors drives the region's continuous growth. The European Space Agency provides institutional support which improves satellite observation systems and spatial data merging capabilities.

Asia Pacific

The market in 2025 reached 22% share for Asia Pacific which results from fast-growing urban areas, better digital infrastructure and greater government dedication to integrating geospatial data in China, India and Japan. The major cities of Beijing, Mumbai and Tokyo serve as important centers for deploying geospatial intelligence which supports urban planning, disaster management and transportation operations.

Rest of the World

The Rest of the World includes Latin America, Middle East and Africa which together represent 18% of the market in 2025. The regions experience development progress because they receive more funding for infrastructure projects, natural resource management activities and disaster risk reduction programs. Geospatial intelligence solutions are being adopted by countries throughout these regions to enhance their capabilities in governance, environmental monitoring and urban planning.

Geospatial data usage for resilience planning and emergency response receives promotion through government-supported programs which organizations such as the United Nations Office for Disaster Risk Reduction have established through their international collaborations. The remaining market shares will transition to newly developing markets and markets with lower penetration.

Competitive Landscape / Company Insights

The market shows a competition level that ranges from moderate to severe because both global and regional companies enter the market with their product development efforts and their pricing methods and their plans to enter new markets. Companies are increasingly investing in research and development, cloud-based analytics and artificial intelligence integration to strengthen their market position. Government-supported space and geospatial programs that operate under the National Aeronautics and Space Administration and United Nations international frameworks drive the development of industry innovation and data standardization and strategic partnerships.

Mini Profiles

Alteryx, Inc. focuses on advanced data analytics and geospatial processing solutions, supported by strong enterprise adoption, intuitive platforms, and efficient data integration capabilities across industries requiring scalable and automated spatial insights.

Caliper Corporation operates in niche geospatial and transportation analytics segments, emphasizing precision mapping, modeling accuracy, and specialized software solutions tailored for urban planning, logistics, and infrastructure analysis applications.

Esri leverages extensive digital platforms and global partnerships to expand market presence, offering comprehensive geographic information system solutions widely adopted across government, environmental, and commercial applications for spatial intelligence.

Fugro N.V. focuses on geodata acquisition and analysis services, supported by strong offshore expertise, advanced surveying technologies, and established presence in energy, infrastructure, and environmental monitoring sectors globally.

IBM leverages cloud infrastructure and artificial intelligence capabilities to expand market presence, delivering integrated geospatial analytics and data solutions that enhance enterprise decision making and large-scale operational efficiency.

Key Players

- Alteryx, Inc.

- Caliper Corporation

- Esri

- Fugro N.V.

- General Electric Company

- Hexagon AB

- IBM

- Precisely

- TomTom

- Trimble Inc.

Recent Developments

In April, 2025, Precisely enhanced its location intelligence capabilities through updates to its data integrity platform. The upgrade improves spatial data accuracy and supports enterprise level geospatial analytics adoption.

In June, 2025, Hexagon AB launched new geospatial solutions integrating digital twin and AI technologies. The development strengthens applications across infrastructure monitoring and industrial intelligence systems.

In August, 2025, TomTom expanded its real time mapping platform with improved traffic and navigation data capabilities. The update supports mobility, automotive, and logistics optimization use cases.

In January, 2026, Trimble Inc. introduced enhanced positioning and geospatial solutions with cloud-based integration. The innovation improves operational accuracy across construction and agriculture sectors.

In March, 2026, Fugro N.V. secured new geospatial survey projects supporting offshore energy and environmental monitoring. The expansion reinforces its role in global geodata acquisition and analysis services.

Global Geospatial Intelligence Market Coverage

Offering Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Technology Insight and Forecast 2026 - 2035

- Remote Sensing

- Geographic Information Systems

- Global Positioning Systems

Application Insight and Forecast 2026 - 2035

- Defense and Security

- Urban Planning

- Environmental Monitoring

- Disaster Management

Vertical Insight and Forecast 2026 - 2035

- Government and Defense

- Energy and Utilities

- Transportation and Logistics

- Others

Global Geospatial Intelligence Market by Region

- North America

- By Offering

- By Technology

- By Application

- By Vertical

- By Country - U.S., Canada, Mexico

- Europe

- By Offering

- By Technology

- By Application

- By Vertical

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Offering

- By Technology

- By Application

- By Vertical

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Offering

- By Technology

- By Application

- By Vertical

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Geospatial Intelligence Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Offering

1.2.2. By

Technology

1.2.3. By

Application

1.2.4. By

Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Offering

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Remote Sensing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Geographic Information Systems

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Global Positioning Systems

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Defense and Security

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Urban Planning

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Environmental Monitoring

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Disaster Management

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Vertical

5.4.1. Government and Defense

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Energy and Utilities

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Transportation and Logistics

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Others

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Offering

6.2. By

Technology

6.3. By

Application

6.4. By

Vertical

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Offering

7.2. By

Technology

7.3. By

Application

7.4. By

Vertical

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Offering

8.2. By

Technology

8.3. By

Application

8.4. By

Vertical

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Offering

9.2. By

Technology

9.3. By

Application

9.4. By

Vertical

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Alteryx, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Caliper Corporation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Esri

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Fugro N.V.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

General Electric Company

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Hexagon AB

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

IBM

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Precisely

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

TomTom

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Trimble Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Geospatial Intelligence Market