Data Center Rack Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Rack Type (Open Frame Racks, Enclosed Racks, Wall-Mounted Racks), by Height (Below 42U, U – 47U, Above 48U), by Width (inch Rack, inch Rack, Others), by Data Center Type (Enterprise Data Centers, Colocation Data Centers, Hyperscale Data Centers, Edge Data Centers), by Component (Rack Enclosure, Power Distribution Units (PDUs), Cable Management, Cooling & Airflow Accessories, Monitoring & Management Systems), by End User (BFSI, IT & Telecommunications, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Media & Entertainment, Others)

| Status : Published | Published On : Feb, 2026 | Report Code : VRICT5221 | Industry : ICT & Media | Available Format :

|

Page : 183 |

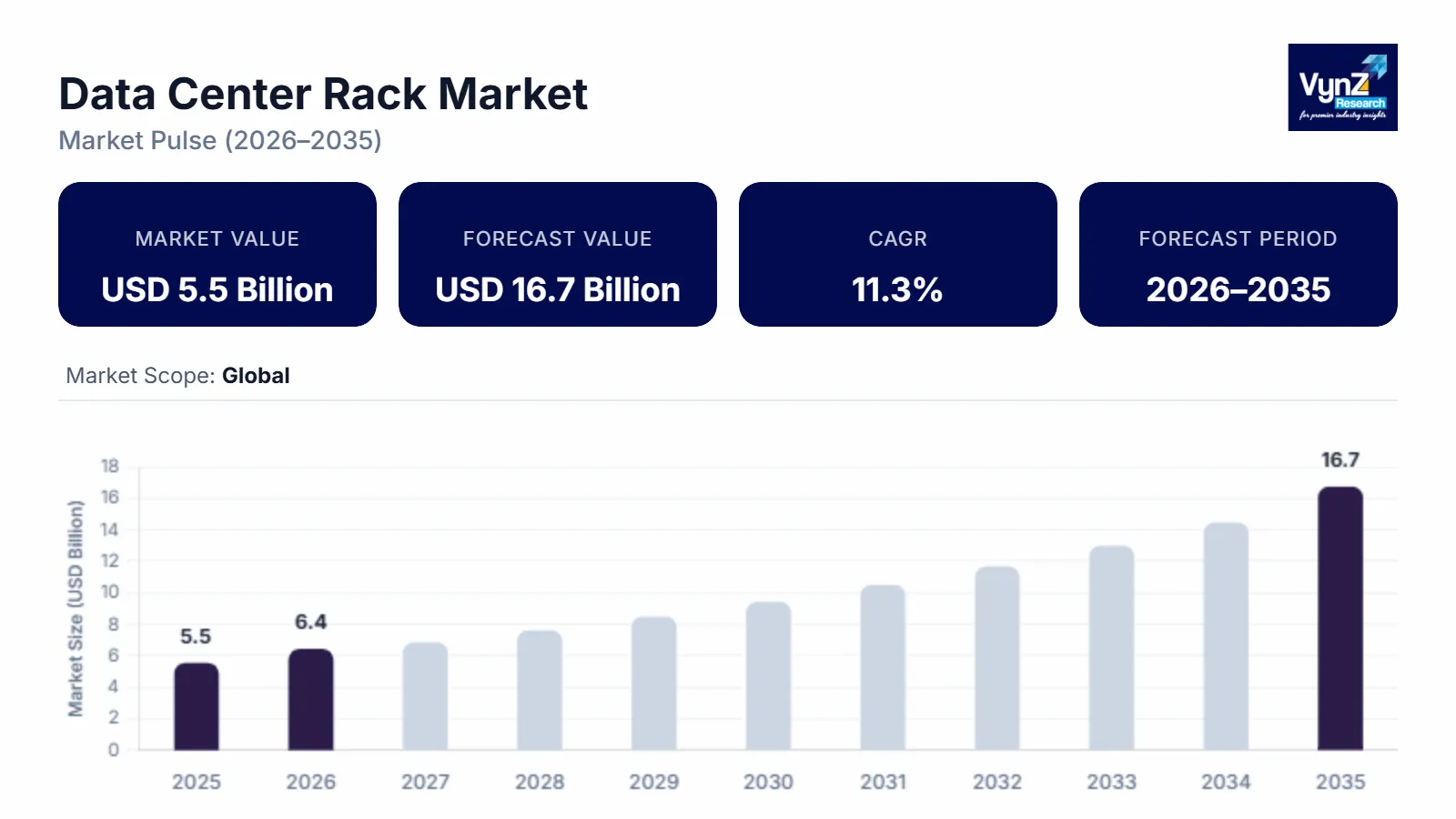

Data Center Rack Market Overview

The data center rack market, which was valued at approximately USD 5.5 billion in 2025 and is estimated to reach around USD 6.4 billion in 2026, is projected to reach close to USD 16.7 billion by 2035, expanding at a CAGR of about 11.3% during the forecast period from 2026 to 2035.

This market is primarily driven by the rapid expansion of digital infrastructure across industries, fueled by rising cloud adoption, big data analytics, artificial intelligence workloads, and IoT-enabled ecosystems. The expansion of hyperscale data centers run by companies like Amazon Web Services, Microsoft Corporation and Google LLC has placed a greater demand on high-density and modular and scalable rack solutions. Businesses are modernizing old IT infrastructure, which allows virtualization and edge computing, and this speeds up rack deployment even more. Advanced rack deployments are also being enhanced by the increased requirement of efficient thermal management, structured cabling, and space optimization of data centers.

Further, the deployment of 5G networks worldwide and growing traffic of data is forcing telecom operators to increase server capacity that will directly benefit rack demand. Increased colocation infrastructure and the hybrid cloud systems are producing long-term infrastructure investments in the global arena. In addition, the implementation of smarter racks with embedded power monitoring and cooling technologies is being promoted by the heavier energy-efficiency standards and sustainability across the board, which add to the long-term market development.

Data Center Rack Market Dynamics

Market Trends

Hyperscale data centers are a significant growth factor in the data center rack market as the global cloud service providers keep building more data centers to satisfy the growing digital demand. Amazon Web Services, Microsoft Corporation, Google LLC, and Meta Platforms, Inc. companies are constantly working on large-scale facilities, which can accommodate tens of thousands of servers. Such hyper scale constructs demand standardized, high-density, and modular rack systems that are space- and power-dense and highly efficient in their cooling capacity. Uttar Pradesh signed multiple MoUs for a ₹2,500 crore hyperscale data center park in Greater Noida (40 MW IT load capacity) as part of broader infrastructure investment deals totaling ~₹19,877 crore. With the explosion of data traffic related to cloud computing, streaming services, AI workloads, and enterprise digital transformation, the operators are not only expanding existing campuses but also constructing new ones in various regions. Also required with hyperscale facilities are sophisticated cable management and containment solutions, and engineered rack designs become more valuable. They also favour pre-configured and scalable rack architectures which facilitates large scale procurement and long-term supplier relationships.

Growth Drivers

The data center rack market is driven by the rapid development of cloud computing infrastructure as more organizations switch workloads off their on-premises systems to scalable cloud computing platforms. Businesses are embracing the infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS) models to enhance flexibility, minimize capital spending, and facilitate remote operations. According to a United Nations Conference on Trade and Development (UNCTAD) report, data centres fundamental to cloud computing infrastructure captured more than one-fifth of global greenfield investment in 2025 with announced investments exceeding USD 270 billion, reflecting strong international public-private interest in cloud-linked digital infrastructure. The major players, including Amazon Web Services, Microsoft Corporation, and Google LLC are ever increasing data center footprints all over the world to satisfy the increasing demand. This growth necessitates high density, modular, and standardized rack systems that have the capacity to accommodate the large-scale deployment of servers. The cloud environments require effective cable management, efficiency in airflow, and incorporated power distribution units in the rack architecture as well. AI, streaming, e-commerce, and enterprise SaaS-based applications are rising in number, straining servers even more, which also speeds up rack deployments. With ongoing penetration of the cloud in the developed and emerging markets, long-term infrastructure investments have been driving the need to adopt the high-end data center rack solutions.

Market Restraints / Challenges

Increasing power usage and power capacities are also a major issue to the Data Center Rack Market since growing rack densities would require considerably larger electricity draws. The current-day AI-enabled servers and cloud-computing and big data analytics are more than fivefold as power-hungry as the IT equipment they aim to replace, pushing current electrical infrastructure. Most data centers have grid capacity limits, transformer upgrades, and power distribution scales, so they cannot scale their operations. Also, increased energy consumption also results in greater cooling needs, which increases power consumption of the entire facility. Increasing power bills in various areas are the direct influence on operational cost and profitability of data center operators. Companies are also being compelled by the sustainability goals and carbon minimization pledges to reconsider rack power effectiveness and to embrace progressed power sharing units (PDUs). Consequently, it has become a major challenge to strike a balance between high performance computing requirements and energy efficiency and consistent power supply to racks as it relates to rack deployment and expansion.

Market Opportunities

The market of data center racks is experiencing tremendous growth opportunities because the expansion of edge data center is driving organizations to bring computing resources closer to the end users to minimize latency, and maximize real-time processing. The implementation of 5G networks and the sharp increase in the number of IoT devices are enhancing the demand of the localized data processing infrastructure. Organizations like AT&T Inc. and Verizon Communications Inc. are making investments to distributed network architecture which entails small compact and efficient rack systems. In contrast to the traditional hyperscale locations, edge sites can be in a space-constrained facility like a telecom shelter, a retail store, or an industrial facility. Telecommunications provider Telefónica has begun rolling out edge data center nodes in five major Spanish cities, financed partly with nearly €100 million (~USD 107 million) in EU strategic funds, supporting distributed compute close to users and regulatory goals under the EU’s Digital Strategy. This is leading to the growing demand of wall-mounted, micro, and ruggedized rack designs that have a high level of security and thermal management capability. Also, edge deployments need to be scalable and modular so that they can be expanded in capacity. With the increasing demands on single rack solutions, the use of edge data centres will persist in driving the development of autonomous systems, smart cities, and video analytics as real-time applications continue to gain popularity.

Global Data Center Rack Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 5.5 Billion |

|

Revenue Forecast in 2035 |

USD 16.7 Billion |

|

Growth Rate |

11.3% |

|

Segments Covered in the Report |

Rack Type, Height, Width, Data Center Type, Component |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Schneider Electric SE, Vertiv Holdings Co, Eaton Corporation plc, Legrand SA, Rittal GmbH & Co. KG, Hewlett Packard Enterprise Company, Dell Technologies Inc., IBM Corporation, Chatsworth Products, Inc., Black Box Corporation, Tripp Lite, Fujitsu Limited |

|

Customization |

Available upon request |

Data Center Rack Market Segmentation

By Rack Type

Enclosed racks are the largest category with a market share of about 55% in 2025, and it is the fastest-growing category during the forecast period, due to rising deployment of AI workloads, GPU-intensive servers, and high-performance computing infrastructure, which require controlled environments and advanced airflow design. They provide enhanced security, optimized airflow management, structured cable organization, and better thermal containment compared to open-frame alternatives. Most enterprise, hyperscale, and colocation data centers prefer enclosed systems to support high-density IT environments and protect mission-critical equipment. Additionally, increasing emphasis on energy efficiency and cooling optimization further strengthens their adoption across modern facilities.

By Height

42U–47U is the largest category with a market share of about 45% in 2025, as it represents the long-established industry standard. This size offers an optimal balance between space efficiency and service accessibility, making it widely adopted across enterprise and colocation data centers. Most IT infrastructure is designed around this height, ensuring strong and consistent demand.

Above 48U is the fastest-growing category with a CAGR of 11.4% during the forecast period, due to increasing high-density deployments. Hyperscale operators aim to maximize compute capacity per square foot, and taller racks allow greater vertical expansion without increasing floor space. This makes them attractive for large-scale cloud environments.

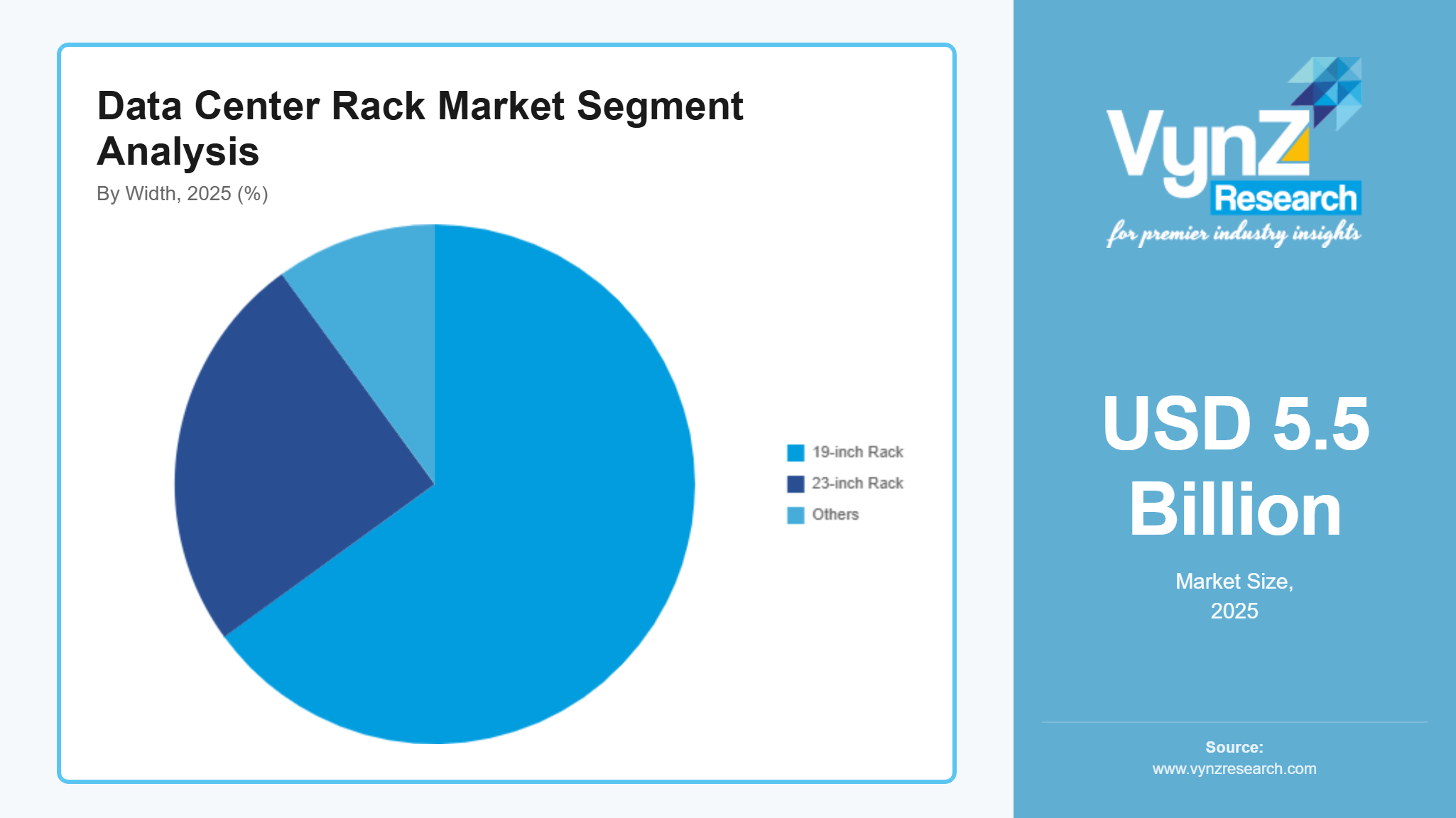

By Width

19-inch rack is the largest category with a market share of about 65% in 2025, as they are the global industry standard for server, networking, and telecom equipment. Most IT hardware manufacturers design their equipment to fit 19-inch rack configurations, ensuring universal compatibility across enterprise, colocation, and hyperscale facilities. Their standardized dimensions simplify procurement, installation, and scalability. Data center layouts, containment systems, and accessories are primarily optimized for 19-inch formats, reinforcing widespread adoption.

23-inch rack is the fastest-growing category with a CAGR of 11.6% during the forecast period, driven by increasing demand in telecom infrastructure and specialized high-capacity deployments. Telecom operators often prefer 23-inch racks to accommodate larger networking equipment and enhanced cable management requirements. Expansion of 5G networks and fiber infrastructure is accelerating demand for wider rack configurations. These racks provide additional internal space for power distribution and airflow optimization in high-load environments.

By Data Center Type

Hyperscale data centers is the largest category with a market share of about 30% in 2025, due to large-scale investments by cloud providers expanding global infrastructure. These facilities require bulk procurement of standardized, high-density rack systems. Rapid growth in cloud computing, AI workloads, and streaming services sustains their dominance. Hyperscale operators emphasize efficiency, scalability, and modular deployment strategies. Continuous campus expansions across North America, Europe, and Asia-Pacific reinforce steady rack demand.

Edge data centers is the fastest-growing category with a CAGR of 11.7% during the forecast period, supported by increasing demand for low-latency processing and real-time data analytics. Expansion of 5G networks and IoT ecosystems is accelerating distributed infrastructure development. Compact and modular rack solutions are witnessing strong uptake in this segment. Enterprises are investing in localized computing to support autonomous systems and smart city applications. Edge facilities often require ruggedized and space-efficient rack configurations.

By Component

Rack enclosure is the largest category with a market share of about 45% in 2025, as they form the foundational structural framework of all server deployments. Every data center installation requires standardized rack cabinets, ensuring consistent baseline demand. Enclosures provide physical protection, airflow control, and organized equipment housing. Their integration with PDUs and cooling accessories strengthens their central role. Replacement cycles and data center upgrades further sustain steady revenue generation.

Monitoring & management systems is the fastest-growing category with a CAGR of 11.5% during the forecast period, driven by the need for real-time performance tracking, predictive maintenance, and energy optimization. Increasing adoption of smart racks and DCIM integration is accelerating growth. Operators are prioritizing remote monitoring to enhance uptime and reduce operational risks. Advanced analytics platforms enable better capacity planning and energy efficiency management. Cybersecurity-enhanced monitoring systems are also gaining importance in enterprise environments.

By End User

IT & Telecommunications is the largest category with a market share of about 35% in 2025, due to massive data generation from cloud services, streaming platforms, enterprise SaaS applications, and telecom network expansion. Continuous infrastructure upgrades by telecom operators and cloud providers sustain strong rack demand. The proliferation of data-intensive services such as video streaming and online gaming further accelerates server deployments. Rapid 5G rollout and fiber network expansion strengthens infrastructure needs.

Healthcare is the fastest-growing category during the forecast period, supported by digital health records, telemedicine platforms, AI-driven diagnostics, and medical imaging storage requirements. Increasing regulatory focus on secure patient data storage is driving data center expansion in healthcare institutions. Hospitals and research centers are investing in localized data infrastructure for improved data security. Growth in genomics research and precision medicine further increases compute requirements.

Regional Insights

North America

North America is the largest regional market for the data center rack market, which is backed with highly established digital infrastructure and high investments made in hyperscale and colocation centers. The United States has the highest concentration of large-scale data centers and unrelenting expansion initiatives to address cloud computing and AI workloads in the region. A four-facility, 902 MW hyperscale data center campus led by Vantage Data Centers with approximately USD 15 billion in investment. Continued demand is being led by ongoing modernization of its legacy facilities and the introduction of upgrades to high-density rack designs. Federal and state-level programs to facilitate broadband expansion and the implementation of the 5G also enhance infrastructure development. Industrial industries like BFSI, healthcare, retail, and technology have become major contributors of large volume of data, which is adding more servers. There is also a high regulatory emphasis on energy efficiency and sustainability, which encourages the use of superior rack systems that have better airflow and monitoring.

Asia Pacific

Asia-Pacific is the fastest-growing region in the data center rack market, due to the speed of digitalization, the growth of internet penetration, and the favorable attitude towards data localization by the government. The countries that have been experiencing a considerable increase in hyperscale and edge data center development are China, India, Japan, Singapore, and Indonesia. India’s data center capacity is projected to grow significantly — industry analysis shows installed power capacity exceeding 2 GW by 2026 and potentially growing fivefold by 2030, implying over USD 30 billion in capital expenditures across the ecosystem. The high-paced urbanization and the thriving e-commerce infrastructures are driving the adoption of the cloud and server installations. Governments are putting a lot of money in development of digital infrastructure and smart cities. The increase in 5G release and IoT are also augmenting capacity requirements of distributed data centres. Rack deployments in the region are still increasing owing to an excellent economic growth and good policy frameworks.

Europe

Europe has a high presence in the data center rack market because of the stringent data protection policies and emphasis on sustainability. The area focuses on energy-efficient and carbon-neutral operation of data centers and promotes the use of more sophisticated rack solutions with better thermal management. The European Data Centre Association highlights that about €100 billion of investment is reshaping the region’s data centre landscape, expanding AI and cloud infrastructure, and supporting growth in digital capacity through 2030. Germany, the Netherlands, Ireland, and the Nordic countries are some of the key colocations and hyperscale centers. New investments in facilities are motivated by continuing modernization of infrastructure and the demand to have data sovereignty. The modern rack deployment in the area is also supported by the initiatives of the circular economy and integration of renewable energy.

Rest of the World

The rest of the world such as Latin America, Middle East and Africa is witnessing a consistent rise in the development of data centre infrastructure. Brazil and Mexico are developing digital connectivity and cloud adoption in Latin America, which results in new rack installations. Middle East, especially the UAE and Saudi Arabia are making massive investments in smart city developments and hyperscale plants, to diversify their economy. In Africa, other countries like South Africa are slowly enhancing digital framework with the assistance of foreign direct investment and public and private associations. Even though the level of infrastructure development differs by region, the increasing rate of digital adoption and governmental funding of technology forces is likely to drive rack market expansion.

Competitive Landscape / Company Insights

The data center rack market is fragmented in nature. The rack segment has relatively lower technological complexity and entry barriers compared to other data center components such as servers or advanced cooling systems. This allows many regional and local manufacturers to operate alongside established global suppliers. Many vendors compete in standard rack enclosures, open-frame racks, and customized configurations, creating strong price competition across regions. Additionally, the rise of edge data centers and regional colocation facilities has increased opportunities for smaller manufacturers to supply localized projects. While large infrastructure providers secure major hyperscale contracts, their dominance does not significantly limit overall competition.

Mini Profiles

Schneider Electric SE is a leading provider of data center infrastructure solutions, offering integrated rack systems, intelligent power distribution units, cooling technologies, and DCIM software to optimize energy efficiency and operational reliability across hyperscale, colocation, and enterprise facilities.

Vertiv Holdings Co delivers comprehensive data center rack enclosures and integrated infrastructure solutions, including thermal management, power systems, and monitoring platforms, supporting high-density computing environments and edge deployments worldwide.

Rittal GmbH & Co. KG specializes in modular IT rack systems and enclosure solutions designed for scalable data center environments, with strong capabilities in climate control integration, security features, and industrial-grade customization.

Legrand SA provides advanced rack cabinets, structured cabling systems, and intelligent PDUs through its data center solutions portfolio, enabling efficient space utilization and reliable power management in enterprise and colocation facilities.

Eaton Corporation plc offers rack enclosures integrated with power management technologies, including UPS systems and advanced distribution units, helping data center operators improve resilience, monitoring, and energy optimization.

Key Players

- Schneider Electric SE

- Vertiv Holdings Co

- Eaton Corporation plc

- Legrand SA

- Rittal GmbH & Co. KG

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- IBM Corporation

- Chatsworth Products, Inc.

- Black Box Corporation

- Tripp Lite

- Fujitsu Limited

Recent Developments

January 2026 – Schneider Electric SE announced the launch of a next-generation smart rack platform integrated with AI-based power monitoring and predictive thermal management to support high-density AI and hyperscale data center deployments.

December 2025 – Vertiv Holdings Co introduced a modular rack solution designed for liquid-cooling environments, enabling efficient deployment of GPU-intensive workloads in hyperscale and colocation facilities.

October 2025 – Rittal GmbH & Co. KG expanded its global production capacity for IT rack enclosures to address rising demand from European and Asia-Pacific data center expansion projects. The move strengthens supply capabilities amid growing regional demand.

August 2025 – Eaton Corporation plc unveiled an advanced intelligent rack PDU portfolio featuring enhanced cybersecurity protocols and real-time energy analytics for enterprise and edge data centers. It improves power security and monitoring efficiency.

June 2025 – Legrand SA launched a new high-density rack cabinet series optimized for hyperscale operators, focusing on improved airflow containment and scalable cable management systems. The series enhances space utilization and airflow performance.

Global Data Center Rack Market Coverage

Rack Type Insight and Forecast 2026 - 2035

- Open Frame Racks

- Enclosed Racks

- Wall-Mounted Racks

Height Insight and Forecast 2026 - 2035

- Below 42U

- U – 47U

- Above 48U

Width Insight and Forecast 2026 - 2035

- inch Rack

- inch Rack

- Others

Data Center Type Insight and Forecast 2026 - 2035

- Enterprise Data Centers

- Colocation Data Centers

- Hyperscale Data Centers

- Edge Data Centers

Component Insight and Forecast 2026 - 2035

- Rack Enclosure

- Power Distribution Units (PDUs)

- Cable Management

- Cooling & Airflow Accessories

- Monitoring & Management Systems

End User Insight and Forecast 2026 - 2035

- BFSI

- IT & Telecommunications

- Government & Defense

- Healthcare

- Retail & E-commerce

- Manufacturing

- Media & Entertainment

- Others

Global Data Center Rack Market by Region

- North America

- By Rack Type

- By Height

- By Width

- By Data Center Type

- By Component

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Rack Type

- By Height

- By Width

- By Data Center Type

- By Component

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Rack Type

- By Height

- By Width

- By Data Center Type

- By Component

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Rack Type

- By Height

- By Width

- By Data Center Type

- By Component

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Data Center Rack Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Rack Type

1.2.2. By

Height

1.2.3. By

Width

1.2.4. By

Data Center Type

1.2.5. By

Component

1.2.6. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Rack Type

5.1.1. Open Frame Racks

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Enclosed Racks

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Wall-Mounted Racks

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Height

5.2.1. Below 42U

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. U – 47U

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Above 48U

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Width

5.3.1. inch Rack

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. inch Rack

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Others

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Data Center Type

5.4.1. Enterprise Data Centers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Colocation Data Centers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Hyperscale Data Centers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Edge Data Centers

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Component

5.5.1. Rack Enclosure

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Power Distribution Units (PDUs)

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Cable Management

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Cooling & Airflow Accessories

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Monitoring & Management Systems

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.6. By End User

5.6.1. BFSI

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. IT & Telecommunications

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Government & Defense

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. Healthcare

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

5.6.5. Retail & E-commerce

5.6.5.1. Market Definition

5.6.5.2. Market Estimation and Forecast to 2035

5.6.6. Manufacturing

5.6.6.1. Market Definition

5.6.6.2. Market Estimation and Forecast to 2035

5.6.7. Media & Entertainment

5.6.7.1. Market Definition

5.6.7.2. Market Estimation and Forecast to 2035

5.6.8. Others

5.6.8.1. Market Definition

5.6.8.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Rack Type

6.2. By

Height

6.3. By

Width

6.4. By

Data Center Type

6.5. By

Component

6.6. By

End User

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Rack Type

7.2. By

Height

7.3. By

Width

7.4. By

Data Center Type

7.5. By

Component

7.6. By

End User

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Rack Type

8.2. By

Height

8.3. By

Width

8.4. By

Data Center Type

8.5. By

Component

8.6. By

End User

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Rack Type

9.2. By

Height

9.3. By

Width

9.4. By

Data Center Type

9.5. By

Component

9.6. By

End User

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Schneider Electric SE

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Vertiv Holdings Co

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Eaton Corporation plc

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Legrand SA

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Rittal GmbH & Co. KG

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Hewlett Packard Enterprise Company

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Dell Technologies Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

IBM Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Chatsworth Products, Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Black Box Corporation

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Tripp Lite

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Fujitsu Limited

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Data Center Rack Market