Saudi Arabia Quantum Computing Market Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Deployment Model (On-Premise, Cloud-Based), by Application (Optimization, Cryptography and Cybersecurity, Simulation and Modeling, Other Applications), by End User (Government and Public Sector, Enterprise, Academic and Research Institutions)

| Status : Published | Published On : Jan, 2026 | Report Code : VRICT5208 | Industry : ICT & Media | Available Format :

|

Page : 150 |

Saudi Arabia Quantum Computing Market Overview

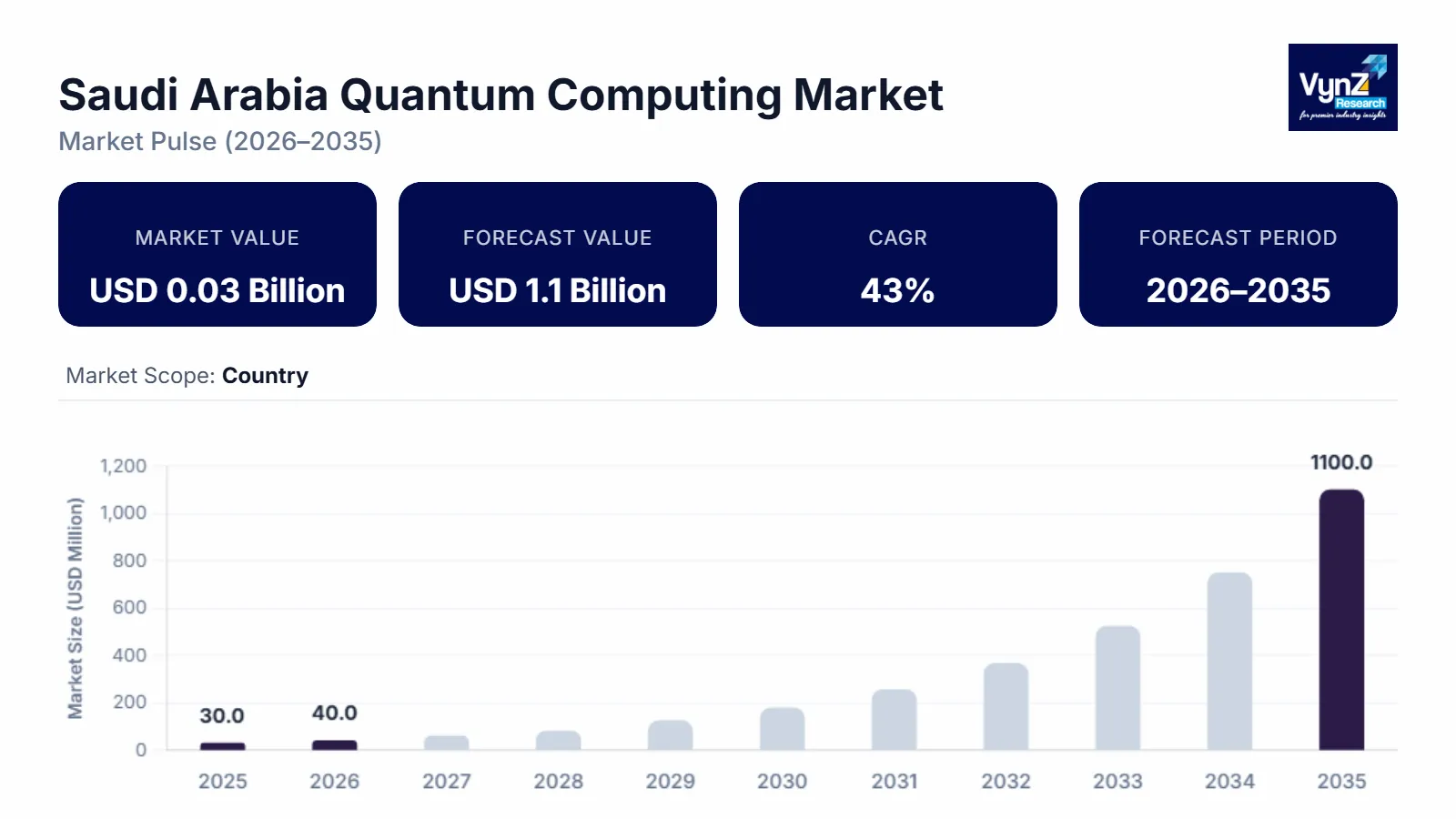

The Saudi Arabia quantum computing market which was valued at approximately USD 0.03 billion in 2025 and is estimated to rise further up to almost USD 0.04 billion in 2026 is projected to reach around USD 1.1 billion by 2035 expanding at a CAGR of about 43% during the forecast period from 2026 to 2035. Market expansion is primarily supported by national digital transformation priorities under Vision 2030 increased public funding for advanced computing research and rising enterprise demand for high performance computing across energy finance and cybersecurity applications.

Adoption is supported by government backed initiatives led by the Ministry of Communications and Information Technology the Digital Government Authority and national innovation programs promoting quantum research talent development and strategic partnerships. Public sector investments combined with deployments by entities such as Saudi Aramco and national research institutes are accelerating early adoption. Quantum computing enables complex optimization secure communication and advanced simulation capabilities aligning with national priorities for economic diversification technological sovereignty and long-term competitiveness.

Saudi Arabia Quantum Computing Market Dynamics

Market Trends

The Saudi Arabia quantum computing industry is witnessing a structural shift toward research driven and government anchored technology adoption aligned with national digital transformation objectives. One of the key trends shaping the market is the growing focus on sovereign computing capabilities and advanced research infrastructure which reflects preferences toward long term technological independence high security computing and national innovation capacity. Government bodies such as the Ministry of Communications and Information Technology and the National Transformation Program emphasize advanced computing including quantum technologies as part of Vision 2030 to support strategic sectors such as energy finance defense and cybersecurity.

Another emerging trend is the gradual integration of quantum computing with high performance computing and artificial intelligence platforms driven by public sector research initiatives and academic collaborations. National entities including King Abdulaziz City for Science and Technology and government backed research universities are promoting quantum algorithms simulation and workforce development. These initiatives encourage solution providers to focus on hybrid architectures cloud-based access models and research partnerships thereby reshaping competitive dynamics and accelerating ecosystem development within the domestic market.

Growth Drivers

The growth of the market is strongly supported by national digital transformation priorities under Vision 2030. Government-led initiatives led by the Ministry of Communications and Information Technology and the National Transformation Program emphasize advanced computing, high-performance data infrastructure, and next-generation research capabilities. Public investment in emerging technologies, including quantum algorithms and hardware research, is expanding demand across defense, cybersecurity, financial services, and energy optimization applications, positioning quantum computing as a strategic enabler of national innovation objectives.

Another critical growth driver is rising government-backed investment in artificial intelligence and advanced analytics ecosystems. The Saudi Data and AI Authority continue to promote integration of quantum computing with large-scale data platforms to enhance modeling, simulation, and optimization capabilities. National programs supporting smart cities, including NEOM and other giga-projects, are accelerating demand for quantum-enabled solutions capable of solving complex logistical, energy, and urban planning challenges, thereby reinforcing sustained market adoption.

Expansion of domestic research and development infrastructure further supports market growth. King Abdulaziz City for Science and Technology and leading academic institutions are increasing funding for quantum research laboratories, talent development, and public-private collaboration frameworks. These initiatives aim to reduce dependence on external technologies while strengthening local capabilities in quantum hardware development, quantum-safe cryptography, and algorithm research. This ecosystem development is expected to generate long-term demand from government agencies, research institutions, and enterprise users within the Kingdom.

Market Restraints / Challenges

The marketplace faces challenges related to high capital intensity and technological complexity. Development and deployment of quantum hardware require advanced cryogenic systems, specialized fabrication facilities, and high-cost research infrastructure. Government reports and strategic documents issued by the Ministry of Communications and Information Technology and the Saudi Data and AI Authority highlight that early-stage quantum technologies demand sustained public funding, long development cycles, and specialized expertise, which can slow commercialization and limit near-term adoption beyond government and research institutions.

Another key restraint is dependence on external technologies and skilled talent. Saudi Arabia currently relies on imported quantum hardware components, software frameworks, and foreign technical expertise, creating exposure to supply chain risks and cost pressures. Public assessments by King Abdulaziz City for Science and Technology emphasize the shortage of locally trained quantum scientists and engineers, which can affect scalability and technology transfer. These constraints increase operational complexity for domestic stakeholders and may delay large-scale enterprise adoption during periods of global technology supply uncertainty.

Market Opportunities

The market presents significant opportunities through government-backed research, innovation, and digital transformation programs aligned with Vision 2030. National initiatives led by the Ministry of Communications and Information Technology and the Saudi Research Development and Innovation Authority prioritize advanced computing, quantum research, and deep technology commercialization. Growing demand for high-performance computing in energy optimization, cryptography, logistics modeling, and defense analytics positions quantum computing as a strategic solution for complex national use cases.

Another major opportunity lies in the integration of quantum computing with artificial intelligence and data analytics platforms. The Saudi Data and AI Authority continue to promote advanced data ecosystems that support hybrid quantum-classical computing models. Investments linked to giga-projects such as NEOM and smart infrastructure programs are creating long-term demand for specialized quantum-enabled simulations and optimization tools. These developments support higher-value applications, encourage public-private partnerships, and enhance the Kingdom’s ability to build a competitive and resilient quantum technology ecosystem.

Saudi Arabia Quantum Computing Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 0.03 Billion |

|

Revenue Forecast in 2035 |

USD 1.1 Billion |

|

Growth Rate |

43% |

|

Segments Covered in the Report |

By Component, By Deployment Model, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Riyadh Region, Eastern Province, Western Region, Other Regions |

|

Key Companies |

Saudi Aramco, Pasqal, Wa’ed Ventures, Quantum Technologies Company (Quantum.sa), Advanced Electronics Company (AEC), Humain, Alfanar, Elm Company, STC (Saudi Telecom Company), Sahara Net |

|

Customization |

Available upon request |

Saudi Arabia Quantum Computing Market Segmentation

By Component

Hardware is estimated to account for approximately 46% of the Saudi Arabia quantum computing market in 2025. This reflects the early-stage nature of the market, where investment remains concentrated on quantum processors, cryogenic systems, control electronics, and specialized infrastructure required for stable qubit operation. Government-backed research centers and national laboratories continue to prioritize hardware capability building to establish sovereign quantum capacity, which supports this segment’s position as the largest contributor to market revenue. Hardware spending is further reinforced by pilot programs and testbeds linked to national research initiatives and university-led quantum labs.

Software contributes an estimated 34% of market revenue in 2025, supported by growing demand for quantum algorithms, development frameworks, simulators, and hybrid quantum-classical platforms. Increased focus on application development in optimization, cryptography, and materials science is driving steady growth in this segment. Services account for approximately 20%, reflecting consulting, system integration, training, and maintenance activities. Services adoption is expanding as enterprises and public institutions require technical expertise to integrate quantum solutions into existing high-performance computing environments.

By Deployment Model

On-premise deployment is projected to represent approximately 58% of the Saudi Arabia quantum computing market in 2025. This dominance is driven by data sovereignty requirements, national security considerations, and government preference for localized infrastructure. Critical sectors such as defense, energy, and public research institutions continue to favor direct control over quantum systems and associated data, reinforcing on-premise adoption. Significant capital allocation toward national computing centers and research campuses further supports this segment’s leadership.

Cloud-based deployment accounts for an estimated 42% of market revenue in 2025 and is the fastest-growing deployment model. Growth is supported by improved access to global quantum platforms, lower upfront investment requirements, and increasing adoption among startups and academic users. Cloud-based access enables experimentation, algorithm development, and workforce training without the need for full hardware ownership. Ongoing investments in digital infrastructure and national cloud strategies are expected to sustain strong growth for this segment during the forecast period.

By Application

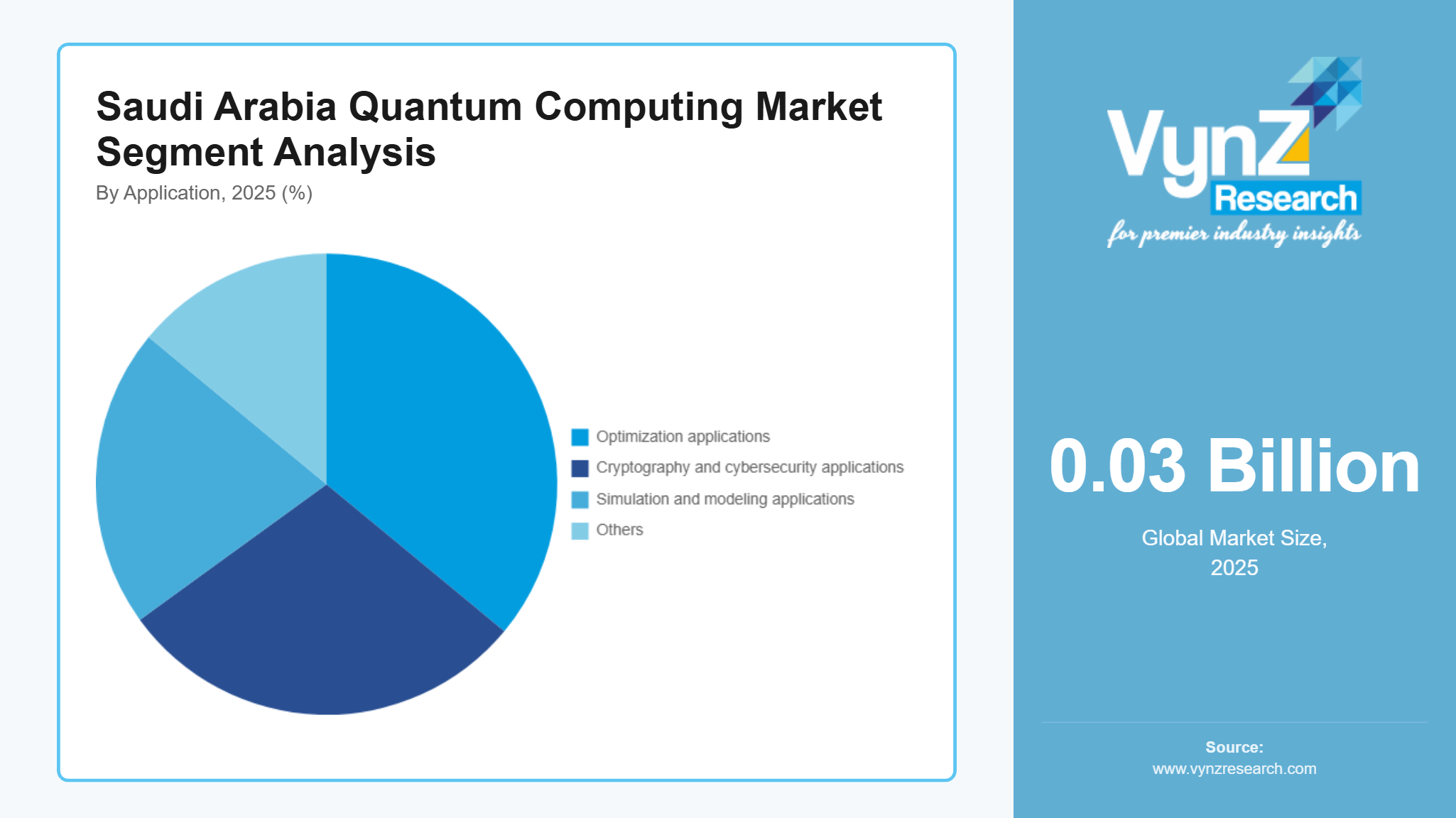

Optimization applications are estimated to account for approximately 36% of the market in 2025, making this the largest application segment. Demand is driven by use cases in logistics optimization, energy system modeling, supply chain management, and smart infrastructure planning aligned with national development programs. Financial modeling and portfolio optimization are also gaining traction as institutions explore quantum-enabled advantages for complex computations.

Cryptography and cybersecurity applications contribute around 29% of total market revenue, supported by rising awareness of post-quantum security and data protection requirements. Simulation and modeling applications represent approximately 21%, driven by interest in materials science, chemical simulations, and advanced research. Other applications account for roughly 14%, including artificial intelligence acceleration and advanced analytics, reflecting early-stage experimentation and proof-of-concept deployments across academic and enterprise environments.

By End User

Government and public sector institutions account for approximately 44% of total market revenue in 2025, supported by national research funding, defense applications, and digital transformation initiatives. Strong policy alignment with advanced computing, cybersecurity, and scientific research positions this segment as the largest end user category. Public universities and national laboratories continue to act as primary adopters and innovation hubs within the ecosystem.

Enterprise users represent an estimated 33% of the market, driven by interest from energy, financial services, and logistics organizations exploring quantum advantages for optimization and risk modeling. Academic and research institutions contribute approximately 23%, supported by government grants, international collaborations, and workforce development clearly focused on building long-term quantum capabilities within Saudi Arabia.

Regional Insights

Riyadh Region

The Riyadh region is estimated to account for approximately 32% of the Saudi Arabia quantum computing market in 2025. Growth is driven by concentration of government ministries, national research bodies, and leading universities actively involved in advanced computing initiatives. Programs aligned with Vision 2030, supported by entities such as the Ministry of Communications and Information Technology and the National Center for Artificial Intelligence, are encouraging investments in quantum research platforms, high performance computing infrastructure, and workforce development. Strong demand from public sector research, defense related applications, and national innovation hubs continues to support regional market expansion.

Eastern Province

The Eastern Province is projected to represent roughly 24% of the market in 2025, supported by strong industrial activity and energy sector adoption. National oil and energy enterprises are exploring quantum computing for optimization, reservoir modeling, and materials simulation to improve operational efficiency. Government backed digital transformation initiatives and R&D funding programs promote collaboration between industry, academic institutions, and technology partners. Expansion of applied research centers and integration of advanced analytics platforms are strengthening demand for quantum computing capabilities across this region.

Western Region

The Western region is estimated to contribute around 20% of the Saudi Arabia quantum computing market in 2025. Growth is supported by increasing investment in academic research institutions, smart city development, and emerging technology ecosystems. Government supported education and innovation programs are expanding access to advanced computing resources and specialized training. Rising collaboration between universities, research centers, and public sector entities is creating long term opportunities for quantum computing adoption. The remaining 24% of market demand is distributed across other regions of Saudi Arabia, reflecting early-stage adoption and gradual ecosystem development outside the major hubs.

Competitive Landscape / Company Insights

The Saudi Arabia quantum computing market is moderately competitive, with global technology firms and emerging regional players focusing on research partnerships, capability development, and geographic presence. Key participants collaborate with government entities and academic institutions to deploy quantum platforms, simulators, and hybrid computing solutions. Market adoption is supported by Vision 2030 initiatives led by the Ministry of Communications and Information Technology, SDAIA, and the National Center for Artificial Intelligence, encouraging R&D investment, talent development, and long-term ecosystem growth.

Mini Profiles

Saudi Aramco powers the Kingdom's energy sector while diving into quantum tech ahead of many others. This firm taps quantum computing to fine-tune heavy industry tasks instead of relying on traditional methods. Team-ups helped roll out the country’s initial quantum machine - boosting both studies and day-to-day performance.

Pasqal works worldwide, including in Saudi Arabia. There, it rolled out the area’s debut neutral-atom quantum setup. Instead of just selling tech, it helps nearby sectors through algorithm tools, practice labs, or hands-on courses.

Wa’ed Ventures puts money into cutting-edge tech, like quantum computing. This branch backs bold new companies, boosting their growth fast. Instead of just funding, it guides startup progress through hands-on support. Innovation drives its mission - backing projects that push limits. With each step, it builds up Saudi Arabia’s high-tech future from the ground up.

Quantum Technologies Company, known as Quantum.sa, runs data centers across Saudi Arabia while offering cloud services alongside modern digital setups. These tools create powerful computing spaces, so businesses can run future-focused apps or shift smoothly into digital operations.

AEC, a key tech player in Saudi Arabia, focuses on gadgets, online safety, and smart digital tools. Thanks to its solid engineering know-how and flexible digital setups, the nation's better prepared for future computing - like quantum - moving forward.

Key Players

- Saudi Aramco

- Pasqal

- Wa’ed Ventures

- Quantum Technologies Company (Quantum.sa)

- Advanced Electronics Company (AEC)

- Humain

- Alfanar

- Elm Company

- STC (Saudi Telecom Company)

- Sahara Net

Recent Developments

January 2026 - SATORP, which has been in operation since 2014, is among the biggest and most sophisticated petrochemical and refining platforms globally. Being a full-conversion platform, SATORP can produce high-value refined products without producing heavy fuel oil from heavy, high-sulfur crude oil that is particularly challenging to process. Apart from the SATORP platform, TotalEnergies and Saudi Aramco have reinforced their collaboration by funding a new complementary project to construct a massive global petrochemical complex that is completely integrated with the refinery. This project, which is called Amiral, shall cost USD 11 billion. Commercial operation is anticipated to start in 2027.

January 2026 - AIQu VEIL, a data handling layer for AI systems, was introduced by Integrated Quantum Technologies. According to the business, it keeps raw data out of the AI pipeline. Businesses have increased their use of AI, but many large organizations still have issues with security, privacy, and cross-border compliance. In many regions, multinational corporations operate distinct AI and machine learning stacks. Inconsistent model versions and redundant infrastructure may result from this. According to Integrated Quantum Technologies, AIQu VEIL uses a unique method known as Informationally Compressive Anonymization to solve these problems. Before data is transmitted to any AI or machine learning system, this procedure transforms it into compressed vector representations.

November 2025 - With the successful deployment of Saudi Arabia's first quantum computer—and the region's first quantum computer devoted to industrial applications - Aramco, one of the top integrated energy and chemicals companies in the world, and Pasqal, a world leader in neutral-atom quantum computing, have made a significant technological advancement for the Middle East. The installation of Pasqal's neutral-atom-powered quantum computer at Aramco's data center in Dhahran is a significant step toward developing regional expertise and quickening the development of quantum applications in the Kingdom of Saudi Arabia and the wider Middle East in the fields of energy, materials, and industry.

Saudi Arabia Quantum Computing Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Deployment Model Insight and Forecast 2026 - 2035

- On-Premise

- Cloud-Based

Application Insight and Forecast 2026 - 2035

- Optimization

- Cryptography and Cybersecurity

- Simulation and Modeling

- Other Applications

End User Insight and Forecast 2026 - 2035

- Government and Public Sector

- Enterprise

- Academic and Research Institutions

Saudi Arabia Quantum Computing Market by Region

- Riyadh Region

- By Component

- By Deployment Model

- By Application

- By End User

- Eastern Province

- By Component

- By Deployment Model

- By Application

- By End User

- Western Region

- By Component

- By Deployment Model

- By Application

- By End User

- Other Regions

- By Component

- By Deployment Model

- By Application

- By End User

Table of Contents for Saudi Arabia Quantum Computing Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Deployment Model

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Saudi Market Estimate and Forecast

4.1. Saudi Market Overview

4.2. Saudi Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Deployment Model

5.2.1. On-Premise

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Cloud-Based

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Optimization

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cryptography and Cybersecurity

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Simulation and Modeling

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Other Applications

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Government and Public Sector

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Enterprise

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Academic and Research Institutions

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. Riyadh Region Market Estimate and Forecast

6.1. By

Component

6.2. By

Deployment Model

6.3. By

Application

6.4. By

End User

7. Eastern Province Market Estimate and Forecast

7.1. By

Component

7.2. By

Deployment Model

7.3. By

Application

7.4. By

End User

8. Western Region Market Estimate and Forecast

8.1. By

Component

8.2. By

Deployment Model

8.3. By

Application

8.4. By

End User

9. Other Regions Market Estimate and Forecast

9.1. By

Component

9.2. By

Deployment Model

9.3. By

Application

9.4. By

End User

10. Company Profiles

10.1.

Saudi Aramco

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Pasqal

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Wa’ed Ventures

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Quantum Technologies Company (Quantum.sa)

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Advanced Electronics Company (AEC)

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Humain

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Alfanar

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Elm Company

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

STC (Saudi Telecom Company)

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Sahara Net

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Saudi Arabia Quantum Computing Market