AI in Energy Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Technology Type (Machine learning, Natural language processing, Computer vision, Predictive analytics systems), by Application (Smart grid management, Energy demand forecasting, Renewable energy integration, Predictive maintenance systems), by Deployment Model (Cloud based, On premises, Hybrid systems), by End User (Utilities, Oil and gas companies, Renewable energy providers, Industrial energy consumers)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9212 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 152 |

AI in Energy Market Overview

The global AI in energy market, which was valued at approximately USD 9.28 billion in 2025 and is estimated to reach around USD 12.82 billion in 2026, is projected to reach approximately USD 235.8 billion by 2035, expanding at a CAGR of about 38.2% during the forecast period from 2026 to 2035.

Market expansion is driven by more deployment of AI driven grid optimization systems and the growing integration of renewable forecasting alongside demand response technologies. International Energy Agency reviews and various national energy department reports point to higher global electricity demand and more variability in renewables, which is pushing adoption of intelligent energy-balancing solutions. Ongoing progress in machine learning-based predictive maintenance and smart grid automation also adds fuel to this market growth.

Government initiatives around energy transition, decarbonization and smart grid modernization are making adoption easier across key regions. National programs managed by energy ministries and public utilities are increasingly weaving in AI enabled monitoring systems to enhance transmission efficiency and trim operational losses. Regulatory frameworks that back carbon reduction targets and digital energy infrastructure upgrades, are also pushing utilities and enterprises toward AI based optimization tools.

AI in Energy Market Dynamics

Market Trends

The market is shifting toward AI driven grid automation and real time energy optimization systems. There is higher adoption of predictive energy management solutions for higher efficiency, sustainability, and cost optimization. Assessments aligned with the International Energy Agency point to increasing renewable volatility, which is basically pushing utilities to look for smarter balancing systems across power networks. The integration of smart grid analytics and AI enabled digital twins is driven by regulatory alignment to decarbonization targets and the quick growth of digital penetration inside utility infrastructure.

Growth Drivers

The market is growing due to smart grid modernization initiatives that keep expanding and more renewable energy investments across global power systems. Government backed energy transition programs are also accelerating use of AI based forecasting and grid optimization tools. Utilities and industrial players are adopting these tools for real operations. The demand for energy efficiency and cost reduction is encouraging deployment of predictive maintenance and load balancing solutions. Utilities and enterprises that prioritize reliability, compliance and operational efficiency are expected to keep driving demand across the forecast period.

Market Restraints / Challenge

The market has high implementation costs for AI enabled energy infrastructure and that can restrict adoption for smaller utilities and developing regions. Regulatory complexity across energy markets makes it harder to roll things out at scale, and it slows deployment timelines down. There is also dependence on legacy grid systems and shortage of skilled AI energy professionals reduces scalability and deployment speed.

Market Opportunities

There are strong opportunities in the market in AI driven renewable integration and smart grid optimization solutions, especially as solar and wind penetration keeps rising. Demand for scalable energy management platforms is increasing across utility networks. Another opportunity comes from AI based energy storage optimization and decentralized grid systems. This is supported by government led digital energy transformation programs, along with growing investments in intelligent power infrastructure.

Global AI in Energy Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 9.28 Billion |

|

Revenue Forecast in 2035 |

USD 235.8 Billion |

|

Growth Rate |

38.2% |

|

Segments Covered in the Report |

Technology Type, Application, Deployment Model, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

ABB, Accenture, Alphabet (Google), Amazon Web Services, General Electric, IBM, Microsoft, NVIDIA, Schneider Electric, Siemens |

|

Customization |

Available upon request |

AI in Energy Market Segmentation

By Technology Type

Machine learning took the biggest market share in 2025, about 41% of total revenue mainly due to heavy rollouts in grid forecasting demand response optimization and energy load balancing use cases. Higher usage across utility analytics platforms and government supported smart grid modernization programs keep pushing its lead in both developed and newer energy markets.

Predictive analytics systems are expected to be the quickest mover, with an estimated CAGR of 24.8% from 2026 to 2035. This is mainly because utilities and operators keep asking for real time forecasting, outage detection and maintenance optimization. More money is flowing into digital energy infrastructure and public sector efforts aimed at grid resilience and renewable integration are speeding up uptake across utility teams and industrial energy networks.

By Application

Smart grid management held the largest slice in 2025, roughly 38%, due to ongoing modernization of transmission and distribution networks and broad adoption of digital utility platforms. Government led energy transition programs along with regulatory rules aimed at grid efficiency promote big scale deployment.

Renewable energy integration apps are projected to expand the fastest, with an estimated CAGR of 25.6% between 2026 and 2035 due to rising solar and wind penetration across global energy systems. Also, international climate targets and national decarbonization policies are pushing demand for AI powered forecasting and grid balancing approaches among utility operators.

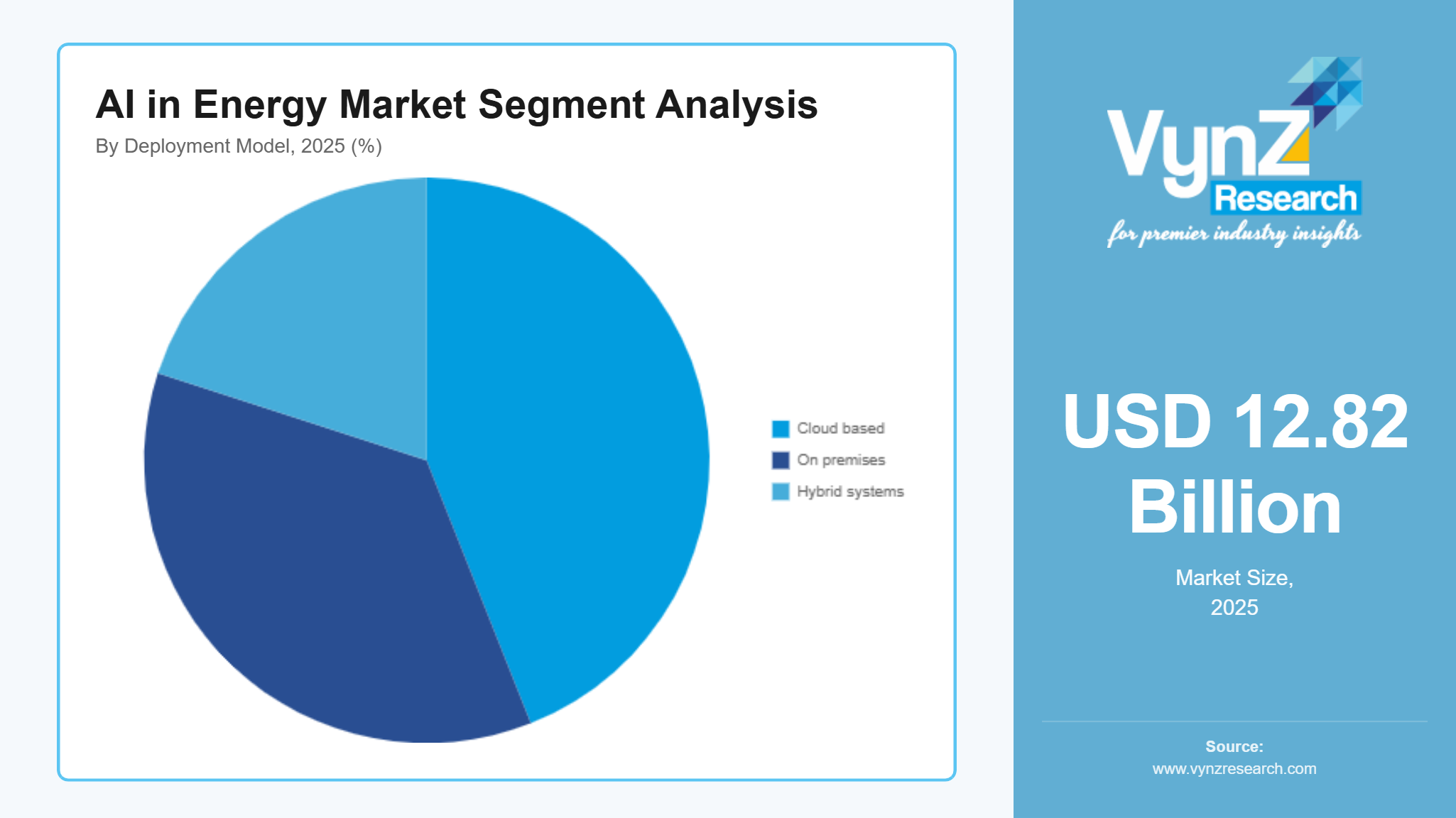

By Deployment Model

On premises solutions held the largest market share in 2025, near 44%, mostly due to data security expectations, operational control requirements and the reality of legacy infrastructure that many utilities already run. Plus, regulatory compliance needs in critical energy infrastructure keep reinforcing that direction.

Cloud based deployment is expected to grow the fastest, with an estimated CAGR of 27.2% from 2026 to 2035 due to higher acceptance of scalable analytics platforms, remote monitoring and real time energy optimization.

By End User

Utilities accounted for the biggest share in 2025, around 36%, supported by large scale grid modernization projects and growing use of AI driven energy management systems. Public sector funding for smart grid infrastructure, along with regulatory mandates for efficiency improvements, also pushes this segment forward.

Renewable energy providers are expected to see the fastest growth, with an estimated CAGR of 26.1% from 2026 to 2035, driven by rapid wind and solar installations and the increasing need for predictive generation forecasting. Government backed renewable energy targets and climate policy playbooks are also accelerating adoption across many global energy markets.

Regional Insights

North America

North America accounted for approximately 38% of the market in 2025, driven by advanced smart grid infrastructure, strong renewable energy integration and rapid adoption of AI based utility management systems across the United States and Canada. Major energy hubs including Texas, California and Ontario continue to attract significant investments in grid modernization and digital energy platforms. Government backed initiatives supported by the U.S. Department of Energy focusing on grid resilience, decarbonization and energy efficiency are accelerating deployment of AI enabled forecasting and optimization systems.

Europe

Europe accounted for approximately 27% of the market in 2025, supported by strict climate regulations, aggressive renewable energy adoption and strong digital transformation across energy utilities in Germany, the United Kingdom, France and the Nordic countries. Policy frameworks aligned with European Union decarbonization targets and energy efficiency directives are driving large scale deployment of AI driven grid optimization and demand management systems. Increasing investments in offshore wind, solar integration and smart grid modernization are further strengthening regional adoption of intelligent energy solutions across utility and industrial sectors.

Asia Pacific

Asia Pacific accounted for approximately 28% of the market in 2025, driven by rapid industrialization, rising electricity demand and large-scale renewable energy expansion across China, India, Japan and South Korea. Government led programs focused on smart grid development, renewable integration and digital energy transformation supported by national energy ministries are accelerating AI adoption in utility operations. Expansion of solar and wind capacity along with modernization of aging transmission infrastructure is further supporting strong regional demand for AI powered energy forecasting and optimization systems.

Rest of the World

Rest of the world including the Middle East, Africa and Latin America accounted for approximately 7% of the AI in energy market in 2025, driven by increasing investments in smart city development, energy diversification strategies and utility modernization programs in countries such as the United Arab Emirates, Saudi Arabia, Brazil and South Africa. Government supported national transformation agendas and renewable energy expansion initiatives are encouraging gradual adoption of AI based energy management systems. Rising focus on grid efficiency and infrastructure upgrades continues to support steady but emerging growth across these regions.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with the presence of global and regional players focusing on AI driven grid optimization, predictive analytics and smart energy management solutions. Companies are increasingly investing in research and development, digital capabilities and advanced analytics platforms to strengthen their market position. Government backed energy transition programs and regulatory frameworks supported by international energy agencies and national energy ministries are encouraging innovation in grid modernization and decarbonization technologies. Strategic partnerships, cloud integration and AI enabled automation are further intensifying competition across utility and industrial energy ecosystems.

Mini Profiles

Accenture focuses on AI driven energy consulting and digital transformation services, supported by strong enterprise brand recognition and global delivery capabilities, enabling utilities to improve grid efficiency and operational intelligence worldwide.

ABB operates in premium industrial automation and electrification solutions, emphasizing performance and energy efficiency through advanced grid technologies and smart infrastructure systems supporting large scale utility modernization projects globally.

Alphabet (Google) leverages digital reach and advanced AI capabilities to expand market presence, offering cloud-based AI analytics and energy optimization platforms that enhance forecasting, efficiency, and sustainability across energy systems.

Amazon Web Services focuses on scalable cloud computing infrastructure for energy analytics and AI workloads, supported by strong global distribution and hyperscale data center capabilities enabling real time energy optimization solutions.

Siemens operates in industrial energy and automation solutions, emphasizing integrated smart grid technologies and digital energy systems supported by strong engineering expertise and widespread industrial presence across global markets.

Key Players

- ABB

- Accenture

- Alphabet (Google)

- Amazon Web Services

- General Electric

- IBM

- Microsoft

- NVIDIA

- Schneider Electric

- Siemens

Recent Developments

In October 2025, Microsoft expanded its AI energy infrastructure investments by strengthening partnerships with global utilities to support large scale deployment of AI optimized data center operations. The initiative focuses on improving energy efficiency and grid integration for hyperscale cloud workloads.

In April 2026, Siemens announced enhanced deployment of AI driven grid automation systems aimed at improving renewable energy integration and predictive maintenance across utility networks. The development supports modernization of smart grids and strengthens digital energy management capabilities.

In March 2026, ABB secured major contracts to supply advanced power stabilization systems for AI driven data centers, reinforcing its role in supporting hyperscale infrastructure expansion. The project focuses on improving grid reliability and enabling high density AI computing environments.

In April 2026, NVIDIA continued expanding its AI energy optimization ecosystem through collaborations focused on accelerating GPU powered grid analytics and data center efficiency solutions. The initiative strengthens its position in AI compute infrastructure supporting energy intensive workloads.

In April 2026, Schneider Electric advanced its digital energy management portfolio by expanding AI enabled automation solutions for smart grids and industrial energy systems. The development enhances real time energy optimization and supports global decarbonization efforts in utility infrastructure.

Global AI in Energy Market Coverage

Technology Type Insight and Forecast 2026 - 2035

- Machine learning

- Natural language processing

- Computer vision

- Predictive analytics systems

Application Insight and Forecast 2026 - 2035

- Smart grid management

- Energy demand forecasting

- Renewable energy integration

- Predictive maintenance systems

Deployment Model Insight and Forecast 2026 - 2035

- Cloud based

- On premises

- Hybrid systems

End User Insight and Forecast 2026 - 2035

- Utilities

- Oil and gas companies

- Renewable energy providers

- Industrial energy consumers

Global AI in Energy Market by Region

- North America

- By Technology Type

- By Application

- By Deployment Model

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Technology Type

- By Application

- By Deployment Model

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Technology Type

- By Application

- By Deployment Model

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Technology Type

- By Application

- By Deployment Model

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for AI in Energy Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Technology Type

1.2.2. By

Application

1.2.3. By

Deployment Model

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Technology Type

5.1.1. Machine learning

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Natural language processing

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Computer vision

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Predictive analytics systems

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Application

5.2.1. Smart grid management

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Energy demand forecasting

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Renewable energy integration

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Predictive maintenance systems

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Deployment Model

5.3.1. Cloud based

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. On premises

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Hybrid systems

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Utilities

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Oil and gas companies

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Renewable energy providers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Industrial energy consumers

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Technology Type

6.2. By

Application

6.3. By

Deployment Model

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Technology Type

7.2. By

Application

7.3. By

Deployment Model

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Technology Type

8.2. By

Application

8.3. By

Deployment Model

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Technology Type

9.2. By

Application

9.3. By

Deployment Model

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

ABB

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Accenture

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Alphabet (Google)

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Amazon Web Services

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

General Electric

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

IBM

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

NVIDIA

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Schneider Electric

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Siemens

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

AI in Energy Market