Autonomous Medical Coding Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Software Solutions, Services, Integrated Platforms), by Deployment (Cloud Based, On Premise, Hybrid), by Pricing Model (Subscription Based, License Based, Pay Per Use), by End User (Hospitals, Insurance Payers, Ambulatory Care Centers, Diagnostic Laboratories)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9213 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 142 |

Autonomous Medical Coding Market Overview

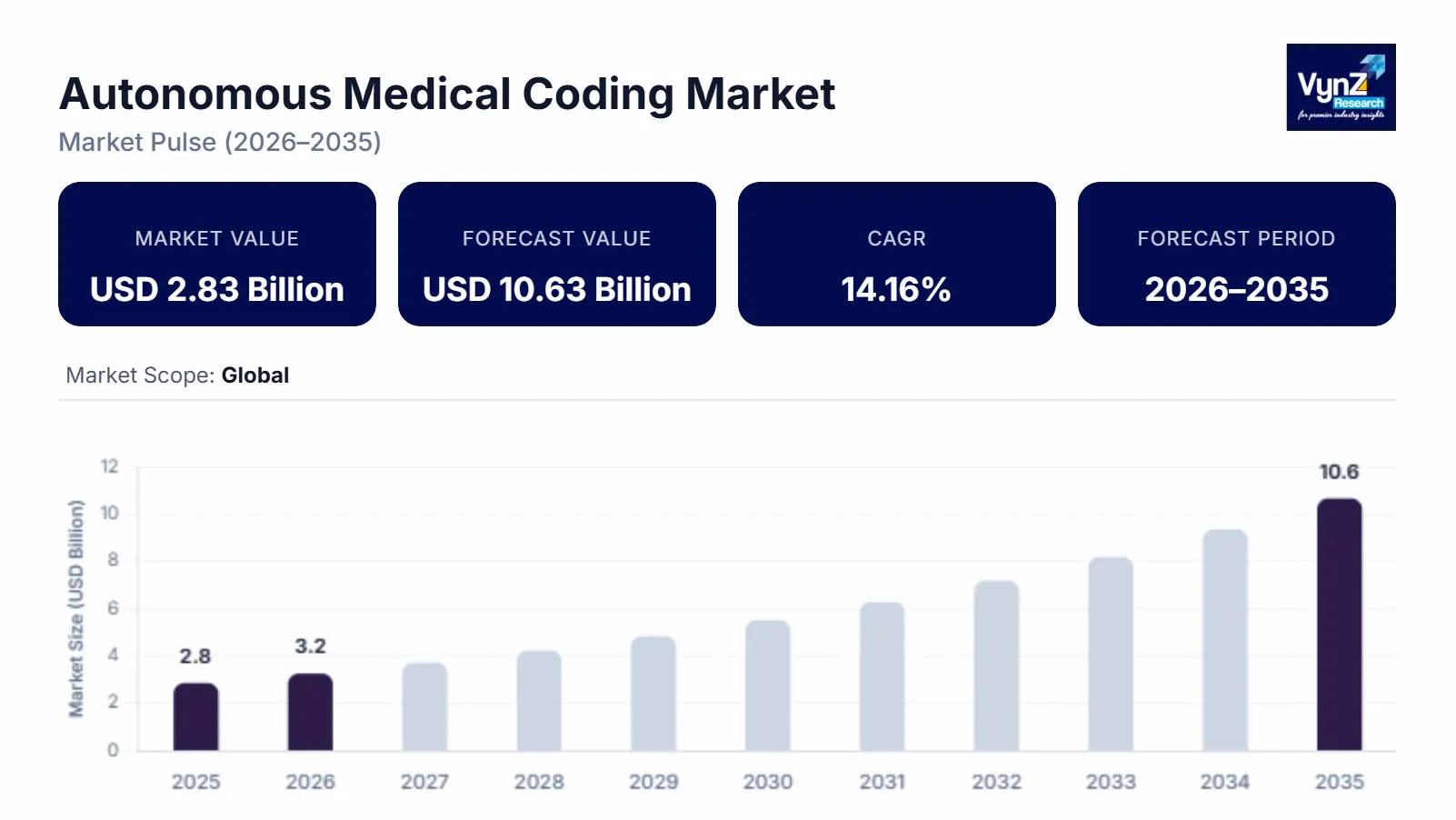

The Autonomous Medical Coding market which was valued at approximately USD 2.83 billion in 2025 and is estimated to rise further up to almost USD 3.23 billion by 2026, is projected to reach around USD 10.63 billion by 2035, expanding at a CAGR of about 14.16% during the forecast period from 2026 to 2035.

The market is growing because healthcare data volumes and the administrative workload in healthcare systems increases and there is a strong demand for automated coding. The adoption of AI and natural language processing within clinical documentation is also speeding things along the whole healthcare ecosystems to ensure billing accuracy, operational efficiency and well-maintained electronic health record systems. As noted by the World Health Organization and the Centers for Medicare & Medicaid Services, healthcare systems are increasingly making digital workflow automation and reimbursement efficiency a top priority. Government backed healthcare IT modernization initiatives are additionally helping adoption in key areas like United States, Germany and Japan.

Autonomous Medical Coding Market Dynamics

Market Trends

The market is witnessing noticeable changes in how healthcare documentation gets automated and how AI is used for clinical workflow improvements. A big trend is the wider adoption of natural language processing centered coding systems to ensure better and faster throughput with less admin load during billing. There is more integration of AI enabled revenue cycle management platforms driven by digital transformation efforts and the regulatory push to standardize electronic health records. The World Health Organization and Centers for Medicare & Medicaid Services highlight that healthcare systems are putting more emphasis on interoperable digital workflows using automated coding tools that support compliance and speed up reimbursement.

Growth Drivers

The market growth is driven by rising healthcare data volumes and the ongoing need for consistent accurate medical billing and reimbursement automation across hospitals and insurance providers. More investment into healthcare digital infrastructure is helping the market keep expanding across both public and private systems. AI enabled clinical documentation tools are getting adopted faster than before to maintain cost efficiency, regulation alignment and operational speed and accuracy, and government backed digital health initiatives in major economies are adding extra momentum.

Market Restraints / Challenges

The market faces regulatory complexity and stricter medical coding standards that vary across different regions which affect system accuracy and deployment consistency. This is a crucial problem for smaller healthcare facilities, especially where digital infrastructure is limited. The reliance on high quality clinical data and advanced AI training models affect solution providers and if there aren’t enough skilled healthcare IT professionals or integration gets stuck with legacy hospital systems, then costs rise and implementations take longer.

Market Opportunities

The market has real room to grow in hospital automation and revenue cycle optimization due to ongoing digital transformation across healthcare organizations. Firms that offer AI powered, scalable, and cost-efficient coding solutions will be better off getting more business from big hospital networks and insurance providers. Another opportunity comes from cloud-based healthcare analytics and intelligent documentation platforms. With increasing investments in digital health ecosystems, this space is seeing strong potential upside.

Global Autonomous Medical Coding Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 2.83 Billion |

|

Revenue Forecast in 2035 |

USD 10.63 Billion |

|

Growth Rate |

14.16% |

|

Segments Covered in the Report |

Component, Deployment, Pricing Model, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Asia Pacific, Europe, Rest of the World |

|

Key Companies |

3M Health Information Systems, Amazon Web Services, Apixio, CereCore, Clintegrity, Dolbey Systems, Epic Systems Corporation, nThrive, Optum Inc., Solventum |

|

Customization |

Available upon request |

Autonomous Medical Coding Market Segmentation

By Component

The software solutions held the biggest share, about 52%, of the market in 2025 due to large number of hospitals and insurance providers rolling it out for scalability, automation for clinical documentation and billing correctness. The AI driven coding engines plus natural language processing tools, are slowly but surely making things even stronger for this segment.

Services and integrated platforms are expected to move quicker, at around 19.2% CAGR, during 2026 to 2035 due to growing need for implementation support, system integration and workflow tuning.

By Deployment

Cloud based deployment had the majority share, close to 58% in 2025, since many healthcare providers prefer scalability, easier remote access and better cost handling when dealing with huge amounts of clinical data. The broader digital transformation within healthcare infrastructure keeps pushing cloud adoption, especially for bigger hospital networks.

Hybrid deployment is showing the fastest growth, around 20.1% CAGR due to the demand for data security, regulatory compliance and flexibility to connect with older and legacy systems. A lot of healthcare organizations adopt hybrid models to balance control and scalability for clinical coding tasks.

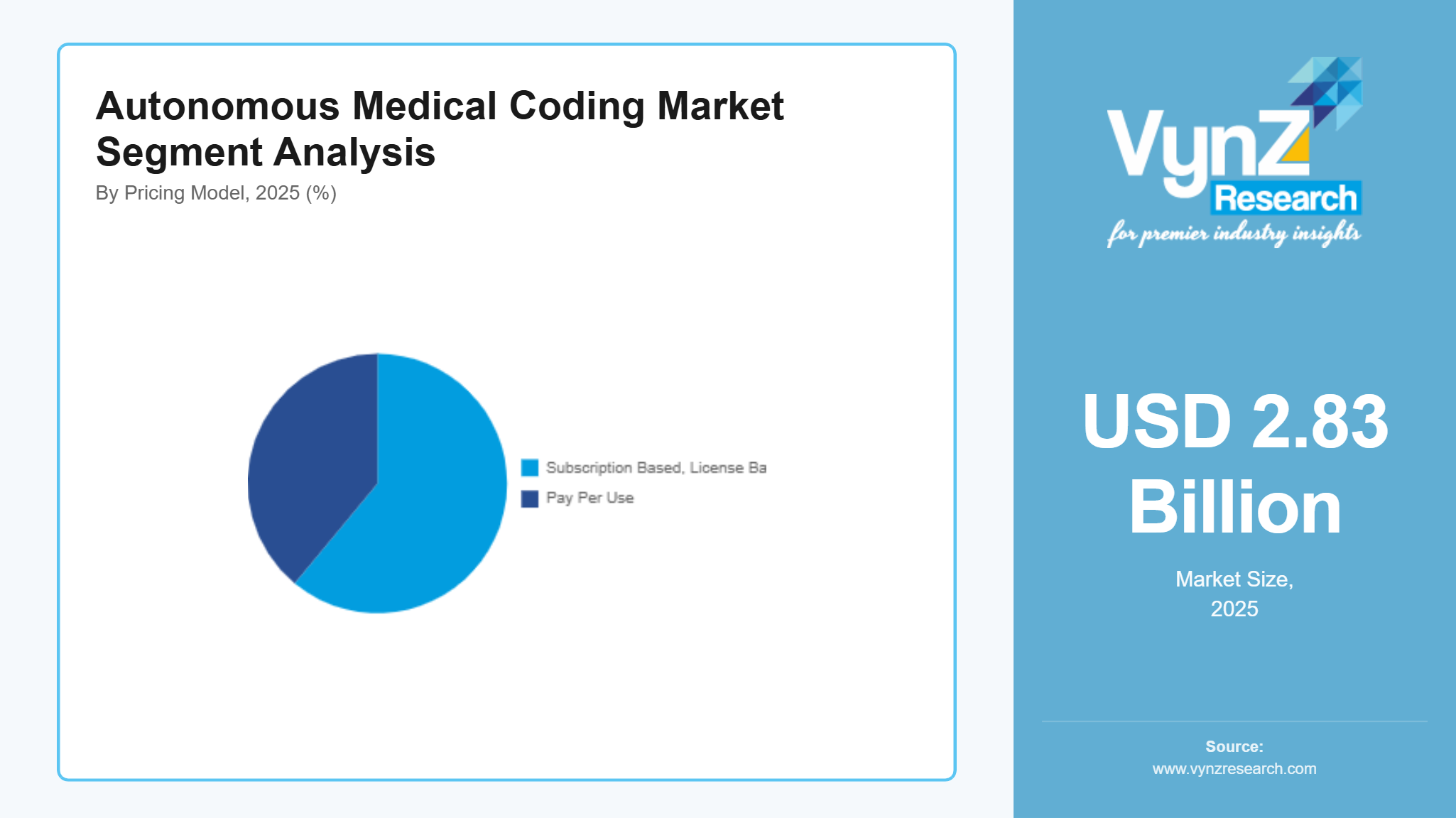

By Pricing Model

In 2025, subscription-based models led, taking about 61% of the market share because the cost patterns are more stable, software updates keep coming and healthcare providers broadly accept this approach to achieve operational agility and spend less money upfront.

Pay per use models are expected to climb the fastest, roughly 20.5% CAGR during the forecast period driven by adoption among small and mid-sized healthcare facilities wanting cost optimized access to advanced coding solutions for their long-term commitments.

By End User

Hospitals had the largest share, approximately 49% in 2025, largely due to high patient loads, more complicated coding needs and strong uptake of electronic health record systems. Government supported healthcare digitization programs and regulatory compliance rules also help strengthen hospital adoption across different regions.

Insurance payers are projected to grow fastest at about 19.8% CAGR during the forecast period from 2026 to 2035 due to the increasing need for automated claims handling, fraud detection and reduction, and better reimbursement accuracy.

Regional Insights

North America

North America accounted for approximately 42% of the market in 2025, driven by advanced healthcare digitization, strong EHR penetration and large-scale adoption of AI based revenue cycle management systems across hospital networks in the United States. Government initiatives supported by the Centers for Medicare & Medicaid Services and World Health Organization are accelerating digital health transformation, while increasing demand for billing accuracy and operational efficiency is strengthening adoption of automated coding platforms.

Asia Pacific

Asia Pacific accounted for approximately 27% of the market in 2025, supported by rapid hospital digitization, expanding insurance coverage and healthcare IT investments across China, India and Japan. Government led digital health missions and national healthcare modernization programs are accelerating automation adoption in clinical documentation, while rising patient volumes and infrastructure expansion are supporting sustained growth.

Europe

Europe accounted for approximately 19% of the market in 2025, driven by healthcare system modernization, regulatory focus on standardized coding practices and rising adoption of digital health platforms. Government backed healthcare digitization initiatives in Germany, France and the United Kingdom are improving interoperability and reducing administrative burden, supporting steady market expansion.

Rest of the World

Rest of the world accounted for approximately 12% of the market in 2025, supported by gradual healthcare digitization, improving hospital infrastructure and rising adoption of AI enabled coding solutions across emerging economies in the Middle East, Latin America and Africa. Government healthcare modernization programs and global health collaborations are supporting adoption, while cloud-based platforms are improving accessibility and workflow efficiency.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with global healthcare IT vendors and AI driven startups focusing on product innovation, workflow automation and geographic expansion across hospital and payer ecosystems. Companies are increasingly investing in AI research and development, digital capabilities and interoperability features to strengthen market position and improve clinical coding accuracy. Government backed healthcare digitization initiatives supported by the Centers for Medicare & Medicaid Services and guidance from the World Health Organization are further encouraging adoption of standardized digital coding systems, intensifying competition across solution providers globally.

Mini Profiles

3M Health Information Systems focuses on healthcare coding, clinical documentation improvement, and revenue cycle management solutions, supported by strong global healthcare brand recognition and extensive hospital system integration capabilities across digital health ecosystems.

Amazon Web Services operates in cloud healthcare infrastructure and AI enabled analytics segments, emphasizing scalable computing performance, interoperability, and secure data processing for autonomous medical coding and clinical workflow automation.

Apixio leverages AI driven healthcare data analytics and strategic payer provider partnerships to expand market presence, enabling advanced clinical coding accuracy and value based care optimization across healthcare organizations.

CereCore focuses on healthcare IT services and enterprise clinical system support, supported by strong hospital network integration capabilities and expertise in EHR optimization and revenue cycle management solutions.

Clintegrity operates in niche healthcare coding and compliance solutions, emphasizing coding accuracy, regulatory alignment, and workflow efficiency for hospitals and healthcare providers adopting automated coding systems.

Key Players

- 3M Health Information Systems

- Amazon Web Services

- Apixio

- CereCore

- Clintegrity

- Dolbey

- Systems

- Epic Systems Corporation

- nThrive

- Optum Inc.

- Solventum

Recent Developments

In February 2025, Dolbey Systems enhanced its AI driven medical coding platform with improved natural language processing capabilities for clinical documentation workflows. The update focused on increasing coding accuracy and reducing manual intervention in hospital revenue cycle processes.

In March 2025, Epic Systems Corporation strengthened its integrated EHR ecosystem with enhanced autonomous coding and clinical documentation features. The development improved billing accuracy and streamlined hospital revenue cycle operations across large healthcare networks.In May 2025, nThrive expanded its revenue cycle management solutions with advanced automation tools for autonomous coding validation and claims processing. The upgrade improved reimbursement accuracy and reduced administrative workload for healthcare providers.

In July 2025, Optum Inc. advanced its healthcare analytics and coding automation suite with AI driven enhancements for clinical documentation and claims optimization. The development strengthened payer provider workflow efficiency and reduced coding errors.

In September 2025, Solventum upgraded its clinical documentation and coding solutions with enhanced AI based automation capabilities. The improvement focused on increasing coding efficiency and supporting hospitals in reducing administrative burden.

Global Autonomous Medical Coding Market Coverage

Component Insight and Forecast 2026 - 2035

- Software Solutions

- Services

- Integrated Platforms

Deployment Insight and Forecast 2026 - 2035

- Cloud Based

- On Premise

- Hybrid

Pricing Model Insight and Forecast 2026 - 2035

- Subscription Based

- License Based

- Pay Per Use

End User Insight and Forecast 2026 - 2035

- Hospitals

- Insurance Payers

- Ambulatory Care Centers

- Diagnostic Laboratories

Global Autonomous Medical Coding Market by Region

- North America

- By Component

- By Deployment

- By Pricing Model

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Deployment

- By Pricing Model

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Deployment

- By Pricing Model

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Deployment

- By Pricing Model

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Autonomous Medical Coding Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Deployment

1.2.3. By

Pricing Model

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Software Solutions

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Integrated Platforms

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Deployment

5.2.1. Cloud Based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. On Premise

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Hybrid

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Pricing Model

5.3.1. Subscription Based

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. License Based

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Pay Per Use

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Insurance Payers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Ambulatory Care Centers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Diagnostic Laboratories

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Deployment

6.3. By

Pricing Model

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Deployment

7.3. By

Pricing Model

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Deployment

8.3. By

Pricing Model

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Deployment

9.3. By

Pricing Model

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

3M Health Information Systems

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amazon Web Services

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Apixio

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

CereCore

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Clintegrity

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Dolbey Systems

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Epic Systems Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

nThrive

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Optum Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Solventum

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Autonomous Medical Coding Market