TIC Market for Aerospace and Aviation Industry Overview

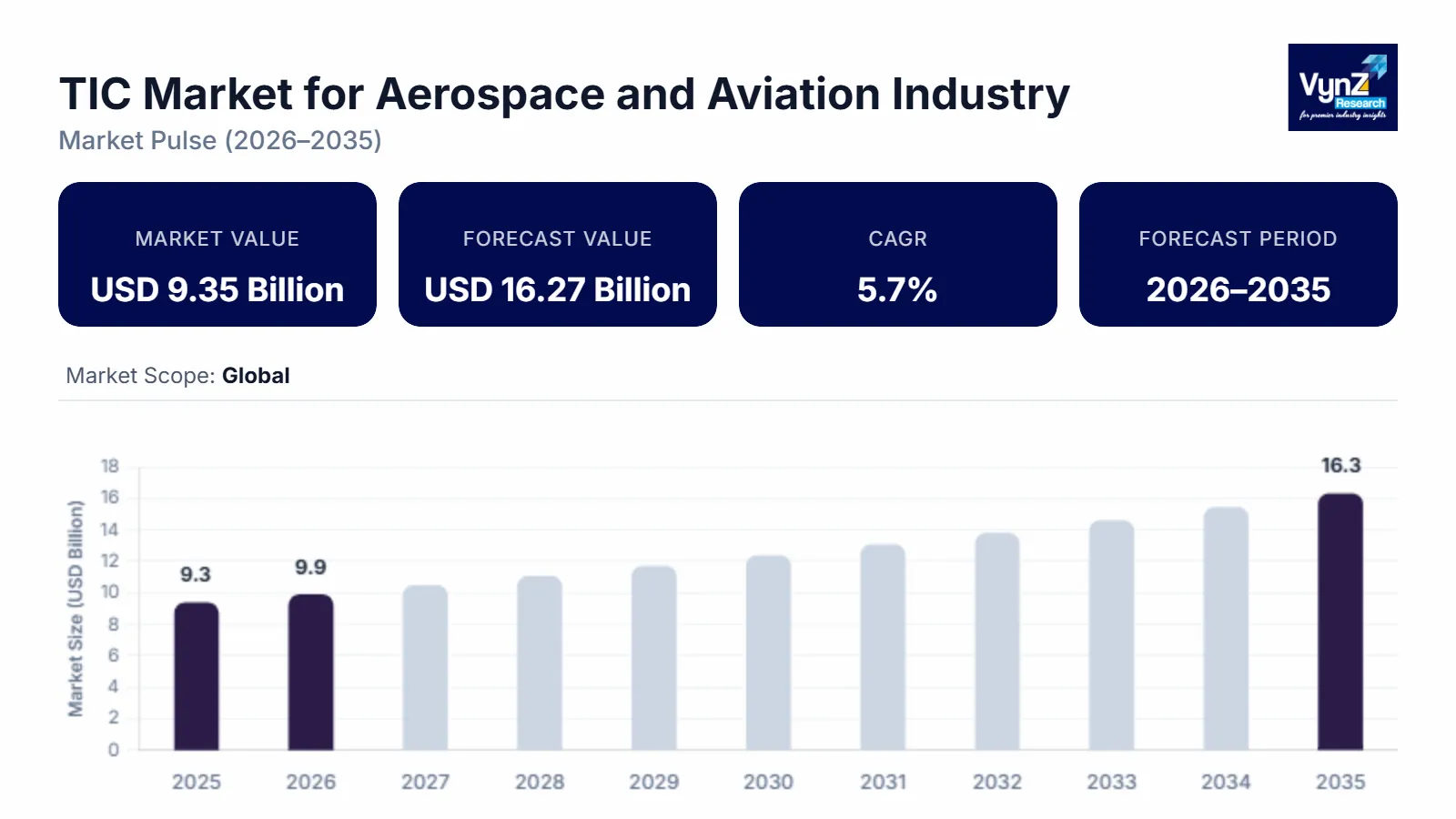

In the Aerospace and Aviation Industry, the Market for Testing, Inspection, and Certification reached USD 9.35 billion in 2025 and is estimated to rise further up to almost USD 9.88 billion by 2026 and is expected to reach USD 16.27 billion in 2035, exhibiting a promising CAGR of 5.7% from 2026 to 2035.

Independent services that guarantee aircraft, parts, materials, and systems adhere to strict safety, quality, and regulatory standards are included in the Testing, Inspection, and Certification (TIC) market for the aerospace and aviation sector. From design, development, and manufacture to maintenance, repair, and overhaul (MRO), these services are critical to the aerospace product lifecycle.

Visual and non-destructive testing (NDT) are used by inspection services to verify integrity and identify defects during production and in-service operations. Adherence to international aviation regulations and standards set by regulatory bodies such as the FAA, EASA, and others is ensured via certification. Structural, mechanical, environmental, and performance assessments of aircraft components and systems are all included in testing services.

TIC Market for Aerospace and Aviation Industry Dynamics

Market Trends

The fast digital revolution and industrial consolidation have a big impact on the aerospace and aviation TIC sector. While data-driven certification procedures and real-time monitoring are made possible by cloud-based platforms and connected devices, increasing investments in AR and VR improve training effectiveness and inspection precision. Globalization, service capabilities, and TIC providers' capacity to support intricate, global aerospace operations are all being bolstered by a rise in mergers and acquisitions and supplier consolidation.

Growth Drivers

The aerospace and aviation industries are among the most tightly controlled ones worldwide. Every single step involved in the design, manufacturing, and operation of an aircraft as well as its maintenance requires certification. Conformity to airworthiness directives, type certification, and continuing operational safety requirements call for TIC engagement regularly rather than on a one-off basis. It is estimated that compliance-driven activities make up about 42-44% of the total aerospace TIC demand, with the intensity of the service increasing gradually as the fleets grow and the regulatory pressure becomes tighter.

Besides, fleet modernization and production ramp-ups are major structural demand drivers. In 2024, the total number of commercial aircraft on backorder reached more than 14,000 units worldwide which resulted that the manufacturers have been forced to not only increase their production but at the same time maintain strict quality control. Any production increase will result in a multiplication of inspection points not only for the materials but also for the components, assemblies, and systems. The demand for TIC linked to aircraft manufacturing and final assembly is on the rise, at approximately 7% CAGR, which is being fueled by the narrow-body completions and the defense procurement programs.

Moreover, operational safety and lifecycle assurance are the main factors that are influencing TIC demand besides manufacturing. As a result of the older aircraft fleets, longer service intervals, and higher utilization rates, the frequent inspections, non-destructive testing, and compliance audits have become the norm. At the same time, sustainability oversight in areas such as emissions, noise, and fuel efficiency is gaining ground in regulatory frameworks. The TIC activities that are closely related to operational safety and environmental compliance are being carried out at almost 8% and thus leaving baseline inspection growth behind.

Market Restraints / Challenges

It is essential to always invest in cutting-edge digital tools and testing apparatus, due to the rapid advancement of technology. Long certification periods, supply chain interruptions, and the requirement to save costs without sacrificing safety regulations limit market expansion. The market for aerospace and aviation is beset by issues such as expensive certification and compliance costs, complicated and dynamic international rules, and a lack of qualified inspectors and NDT specialists.

Market Opportunities

The aerospace and aviation TIC industry offers strong development prospects that gains traction by rising demand for MRO services, growing global fleets, and increased aircraft manufacturing. Demand is further increased by growth in emerging markets in the Middle East and Asia-Pacific. New testing and certification needs are being created by the rise of innovative air mobility platforms, UAVs, and electric and hybrid aircraft. Specialized validation services are also needed for the expanding usage of additive manufacturing and lightweight composites. Furthermore, new opportunities for environmental testing and compliance are being created by sustainability rules and carbon reduction targets.

Global TIC Market for Aerospace and Aviation Industry Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 9.35 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 16.27 Billion

|

|

Growth Rate

|

5.7%

|

|

Segments Covered in the Report

|

Aircraft Category, Lifecycle Stage, System Focus, Regulatory Authority Alignment

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

North America, Europe, Asia Pacific

|

TIC Market for Aerospace & Aviation Industry Segmentation

By Aircraft Category

Commercial aviation represents the major part of the total TIC demand with about 46-48%, the main reasons being the high volumes of the fleets, regulatory complexity, and continuous airworthiness requirements. The share of defense aviation is estimated to be around 32-34%, it is mainly supported by the needs for defense certification, testing, and secure inspection mandates. General aviation together with business jets making the rest of the share but the per-unit TIC value is higher for them because of the personalized certification processes.

By Lifecycle Stage

Manufacturing and assembly-stage TIC service providers are responsible for approximately 38-40% of the overall demand, it is their work that is supported by material testing, component validation, and conformity assessment. Inspection and maintenance activities which are a part of the in-service program follow closely with a contribution of around 36-38%, they are a reflection of the recurring checks across the operational fleets. Design and certification activities make up the rest of the share but they are showing the highest increase as a result of new platforms and variants entering development.

By System Focus

The largest TIC focal point is the airframe and structural systems which make up about 41% of the service demand due to various heaviness tests, structural integrity checks, and damage tolerance analysis. Next come engine and propulsion systems which contribute approximately 29% of the service demand and are supported with performance testing and safety validation. Avionics and electronic systems are the smallest share but are expanding at the fastest pace and are getting close to 8.5% CAGR as digital complexity is on the rise.

By Regulatory Authority Alignment

Most of the TIC activities are related to certification in line with FAA and EASA standards and therefore this kind of certification accounts for almost 57% of the total TIC activities due to worldwide acceptance and aircraft operations across different countries. The rest of the share is with defense-specific authorities, and national aviation regulators. There are more and more multi-authority compliance projects especially for export aircraft and worldwide fleet operators which results in higher TIC engagement per program.

Regional Insights

North America

The aerospace TIC market of North America is still the largest one, and it is responsible for close to 34-36% of the total worldwide demand. The US is the main source of the region's activity and thus the area is bustling with aircraft manufacturing, defense aviation programs, and commercial fleet operations.

TIC demand is the result of a continuous production activity, recurring airworthiness checks, and safety oversight that is stringent. The services that are related to manufacturing conformity and in-service inspection are upgrading at around 6.5-6.8% each year.

The compliance with environmental goals and the certification of the next-generation aircraft are gradually gaining the status of main demand drivers.

Europe

With a contribution of almost 27-29% to the global aerospace TIC demand, Europe can be considered as a region with a solid manufacturing base and a set of harmonized regulatory frameworks. Among the certified services EASA-aligned ones as well as safety audits are the pillars of the most consistent service demands.

Growth is mostly the result of aircraft development programs, sustainability mandates, and fleet renewal activities. The TIC services related to environmental performance and system validation are moving forward at a pace very close to 7.2% CAGR. Defense aviation and cross-border compliance requirements are still adding complexity and deepening inspections.

Asia Pacific

Asia Pacific is the regional market with the quickest pace of growth, and its CAGR is estimated to be between 8 and 9%. The expansion of the fleets in China, India, and Southeast Asia is the main source of the continuous demand for certification, inspection, and operational audits.

Airlines in the region are becoming more and more dependent on third-party TIC providers in order to meet the standards of safety that are set internationally. Aircraft maintenance, repair, and overhaul activities are also the reasons for the demand in recurring inspection services that is growing.

When domestic manufacturing programs become mature, the demand for design and certification-related TIC is going up at a high rate.

Competitive Landscape / Company Insights

The aerospace and aviation testing, inspection, and certification (TIC) industry is dominated by multinational firms such as SGS SA, Intertek, TÜV SÜD, Bureau Veritas, and Element who compete on the basis of their technological prowess, worldwide presence, and regulatory expertise. These companies offer multi-jurisdictional services and extensive approved labs. These businesses. Specialists in the mid-tier focus on niche areas such as composites and avionics. In addition, regional labs and digital TIC platforms are rivals because of the stringent safety requirements and the demand for faster, more compliant certification globally.

Mini Profiles

Intertek provides a diverse range of both military and civil Aerospace and Defence Services of all aspects of production and performance.

MISTRAS can perform inspections on single components, or centralize testing and machining aerospace production milestones in a purpose-built facility.

With its headquarters located in Neuilly-sur-Seine, Paris, Bureau Veritas S.A. is a French company that leads the world in testing, inspection, and certification (TIC) services that works in over 140 countries. Through inspections, audits, laboratory testing, and certification services, the company assists clients in a variety of industries, like agri-food, aerospace, construction, maritime, and industrial.

Key Players

- Intertek Group Plc

- Bureau Veritas

- MISTRAS Group

- SGS SA

- Eurofins Scientific

- TUV Rheinland

- TUV SUD

- DEKRA SE

- Applus+

- DNV GL

- Renesas Electronics Corporation

Recent Developments

In February 2026, In order to improve product safety, compliance, and quality assurance throughout its marketplace, DEKRA announced a partnership with Temu, an e-commerce platform, broadening DEKRA's TIC reach beyond conventional industries.

In December 2025, Solar manufacturer JA Solar and TÜV Rheinland have collaborated on Joint validation of next-generation multi-cut cell technology. Under this agreement, JA Solar will provide product data, cell and module structures, manufacturing process details, and test samples to support TÜV Rheinland’s work on developing testing standards, conducting verification tests, advancing certification procedures, and performing quality assessments related to multi-segmentation technology.

February 2025 - Renesas Electronics Corporation which is a premier supplier of advanced semiconductor solutions, has successfully obtained PSA Certified Level 1 certification with the European Cyber Resilience Act (CRA) compliance extension for three of its latest microcontroller Groups (MCUs). This certification, evaluated by Applus+ Laboratories, marks a significant step in Renesas' commitment to cybersecurity and cmpliance with upcoming European regulations.