TIC Market for Building & Construction Industry Overview

The global building & construction industry testing, inspection, and certification (TIC) market was valued at USD 12.40 billion in 2025 and is expected to reach USD 13.12 billion in 2026. The market is projected to grow steadily, reaching USD 21.79 billion by 2035, with a compound annual growth rate (CAGR) of 5.8% from 2026 to 2035.

The Testing, Inspection, and Certification (TIC) market for the building and construction industry plays a critical role in ensuring structural safety, material quality, regulatory compliance, and sustainability across residential, commercial, and infrastructure projects. TIC services verify that construction materials, components, and systems meet national and international standards throughout the project lifecycle from design and material sourcing to construction, commissioning, and maintenance.

Technological advancements, including digital inspections, Building Information Modeling (BIM), drones, IoT-enabled monitoring, and data analytics, are transforming traditional TIC processes, improving accuracy and reducing project delays. As construction projects become more complex and risk-sensitive, outsourcing TIC services to specialized providers has become a preferred strategy, supporting steady growth of the TIC market within the building and construction industry worldwide.

TIC Market for Building & Construction Industry Dynamics

Market Trends

The Testing, Inspection & Certification (TIC) market for the building and construction industry is undergoing significant transformation driven by regulatory, technological, and sustainability forces. As urbanization accelerates and large infrastructure programs expand globally, construction projects are subject to increasingly stringent safety, quality, and compliance standards, prompting developers and regulators to rely more on independent TIC services to validate materials, workmanship, and structural integrity.

Growth Drivers

Building and construction projects are heavily regulated and overseen at multiple levels. Different layers of supervisory agents are involved in the control of these projects, ranging from their type and location to the stage of the asset’s life cycle the projects are at. Apart from the general regulations imposed by the structural safety codes, fire resistance norms, seismic standards, and material compliance requirements, there is a growing need for independent testing and inspection services. It is estimated that regulatory-driven TIC activities account for about 36-38% of sector demand, with service volumes growing by approximately 6.6% every year as authorities step up enforcement at the time of construction and after completion.

The global construction spending's scale and complexity remain another continuous factor to drive the industry. Public infrastructure programs, commercial real estate development, and big residential projects are examples of activities that need repeated inspection of materials, foundations, structural components, and installed systems. In fact, global construction output exceeded USD 13 trillion in 2023, and TIC services directly linked to construction execution and quality assurance are getting almost 7.2% CAGR higher, thus they are being supported by multi-stage inspection requirements.

Sustainability and lifecycle performance have also become compulsory evaluation points instead of simply being optional considerations. Currently, energy efficiency standards, green building certifications, and environmental impact verification significantly influence getting project approvals and access to financing. The TIC services that are linked to sustainability audits, material traceability, and environmental compliance are advancing more quickly than the traditional testing ones, reaching close to 8% growth in the markets where the green construction mandates are mature.

Market Restraints / Challenges

The testing, inspection, and certification market face certain challenges like trade wars and growth fluctuations, a huge investment for automation and installation of industrial safety systems, and the high cost of TIC owing to diverse standards and regulations globally. Moreover, there are certainly more challenges faced by the building & construction industry such as projects should be completed on schedule, products being safe and having quality standards, costs should not overrun, compliance to CSR, and effective risk management. Moreover, a lack of testing facilities and skilled personnel may hamper the growth of the TIC market.

Market Opportunities

The TIC market for building and construction is poised for long-term growth as the industry demands shift from simple compliance to performance assurance, strategic risk management and sustainability validation. Another high-growth area is sustainability and green building compliance. As legislators, investors, and end users prioritize low-carbon building, energy efficiency, and environmental stewardship, there is an increasing demand for energy performance testing, carbon footprint verification, indoor air quality tests, and green certification. By expanding into environmental assurance and ESG reporting, TIC businesses can create new revenue sources in addition to traditional safety and compliance testing.

Global TIC Market for Building & Construction Industry Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 12.40 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 21.79 Billion

|

|

Growth Rate

|

5.8%

|

|

Segments Covered in the Report

|

Service Type, Project Type, Sourcing Type, and Compliance Focus

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

North America, Europe, Asia Pacific

|

TIC Market for Building & Construction Industry Segmentation

By Service Type

Testing services are the major portion of the building and construction industry's TIC revenue with a contribution of approximately 44-46%. The need for the same is created by such works as concrete testing, soil analysis, material strength validation, and fire resistance assessment. Next in line, the Inspection services comprise the 33-35% share and are the fastest-growing service line by nearly 8% CAGR attributed to the on-site structural checks and compliance monitoring. The last pieces of the puzzle are Certification services representing the remaining share.

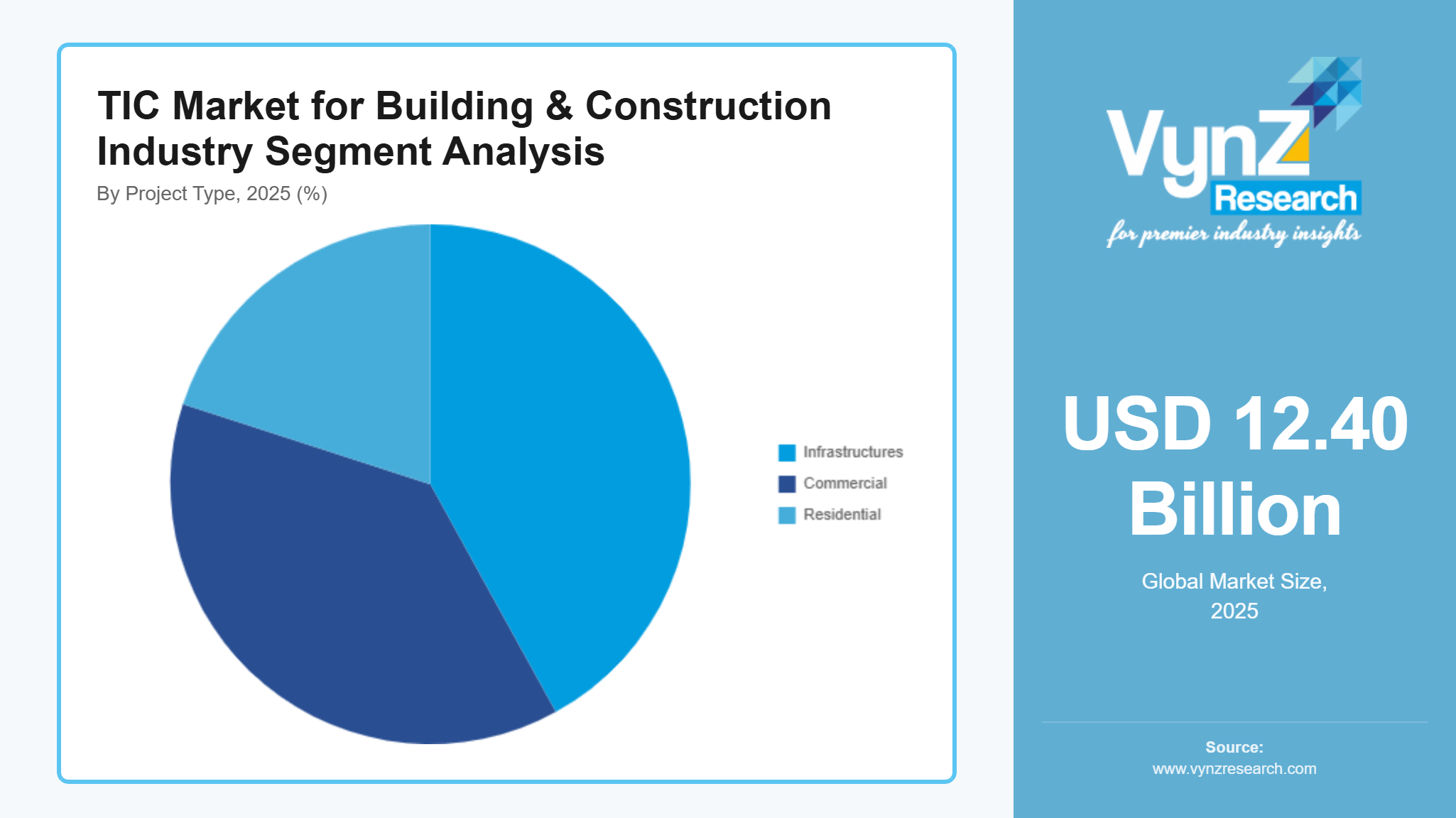

By Project Type

Infrastructures like roads, bridges, railways, and public utilities are the prime sources of demand for TIC services, approximately accounting for 42% of the consumption, due to their magnitude and the regulatory rigor. Commercial construction is responsible for about 34% of the activity volume and is mainly driven by office, retail, and mixed-use developments. The residential sector forms the rest of the demand, however, through safety and occupancy certification, it continues to provide recurring demand.

By Sourcing Type

Most of the TIC operations, almost 67-69%, are carried out through outsourcing which is why construction stakeholders are eager to engage independent third parties as a means for regulatory acceptance and risk mitigation. Outsourced services are on the rise at a rate of about 7.5% CAGR. The rest 31-33% of demand is attributed to the in-house testing and inspection, which are mainly done by large contractors and developers, and their progress, is close to 4.5% but slower than that of outsourced services.

By Compliance Focus

One of the largest focus areas is structural and safety compliance that makes up almost 41% of the TIC demand. Following that, there is environmental and sustainability compliance that makes up around 32%, which is mainly driven by green building norms and emissions oversight. The remaining share is accounted for by fire safety and occupancy certification. Sustainability-related compliance services are growing at the fastest rate, which is more than 8% a year in developed markets.

Regional Insights

North America

North America is responsible for about 30-32% of the world demand for TIC in the building and construction industry. The US is the main driver of the regional activity that results from strict building codes, liability risk, and the enforcement of safety and environmental standards.

The demand for TIC is fueled by the continued infrastructure upgrades, commercial redevelopment, and recurring inspection mandates for existing assets. The services that are related to structural inspection and energy efficiency verification are increasing their turnover by 6.7-7% annually.

The use of green building certifications is further enhanced by the demand for specialized testing and audit services.

Europe

Europe accounts for about 26-28% of the global TIC demand for the construction industry. It is influenced by the harmonized standards and strict enforcement. The main reason for the structural safety norms and sustainability directives compliance is a stable demand for the services.

Environmental and energy performance assessments are becoming more and more present as part of the project approval processes which result in increased demand for sustainability-focused TIC services at nearly 7.4% CAGR.

The modernization of Europe’s old infrastructure as well as the retrofitting of energy-efficient buildings will continue to give rise to long-term TIC needs.

Asia Pacific

Asia Pacific is a rapidly expanding regional market. It is estimated that the market is growing at a CAGR of 8.3-8.8%. China, India, and Southeast Asia are the main drivers of the demand due to their large-scale urban development, transport infrastructure expansion, and industrial construction.

As the components of the regulatory framework get more standardized, the trust to certified third-party TIC providers increases as well. At the same time, it is beneficial for the local industries to have export-driven construction materials and cross-border investment projects which, in turn, increase the need for certification.

The region is undergoing a transition from very basic compliance testing to more thorough, lifecycle-based inspection ones.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional players focusing on product innovation, pricing strategies, and geographic expansion. Companies such as Microsoft, IBM, Google, Amazon Web Services, and Oracle are investing heavily in R&D, cloud infrastructure, and AI model optimization. Government-backed initiatives, including NIST AI guidelines, the EU AI Act, and national AI strategies in APAC, support technology adoption and reinforce vendor positioning across enterprise and public sector clients.

Mini Profiles

MISTRAS can perform inspections on single components, or centralize testing and machining aerospace production milestones in a purpose-built facility.

Bureau Veritas provides electrical safety testing and certification services that help gain access to global markets. This certification program test products against recognized safety standards relating to criteria such as electric shock, excessive temperature, radiation, implosion, and mechanical hazards and fire.

Intertek provides a diverse range of both military and civil Aerospace and Defence Services of all aspects of production and performance.

Key Players

- Intertek Group Plc

- Bureau Veritas

- MISTRAS Group

- SGS SA

- Eurofins Scientific

- TUV Rheinland

- TUV SUD

- DEKRA SE

- Applus+

- DNV GL

- Element Materials Technology

- UL Solutions

- Lloyd’s Register Group

- BSI Group

- Cotecna Inspection SA

Recent Developments

In June 2025, UL Solutions launched its new testing and certification service for immersion cooling fluids used in data centers. This offering is designed to help ensure the safety, performance, energy efficiency and reliability of immersion cooling fluids that protect critical IT equipment—especially in high‑demand environments such as AI and high‑performance computing centers.

In May 2025, Sustainable technology firm GoBlu International collaborated with testing specialist Eurofins Sustainability Services to help drive sustainable chemical management and testing in the textile and footwear industries.

In March 2025, Lloyd’s Register has completed a joint development project (JDP) designing ammonia dual-fuel systems on Trafigura's newbuild medium gas carriers (MGCs).