TIC Market for Fire Safety Equipment Industry Overview

The Fire Safety Equipment’s Testing, Inspection, and Certification Market was valued at approximately USD 1.1 billion in 2025 and is estimated to rise further rise to almost USD 1.15 billion by 2026, is projected to reach around USD 1.75 billion in 2035, expanding at a CAGR of about 4.8% during the forecast period 2026 to 2035.

Globalization has led to product standardization norms and has penetrated developed technologies across various industries such as fire safety equipment, food and beverage, electronics and automotive industries, etc., resulting in the growth of the TIC market during the forecast period 2025-2030. Moreover, the growing middle-class population, rapid urbanization, mandatory safety regulations, upsurge in the illicit trade of counterfeit and pirated products, advancement in networking and communication technology, the inclination of outsourcing testing, inspection, and certification services has propelled the growth of the TIC market in the fire safety equipment. Ensuring that fire protection systems and products meet national and international safety standards is the primary goal of the Testing, Inspection, and Certification (TIC) industry for fire safety equipment.

Stricter fire safety laws, fast urbanization, industrial growth, and rising awareness of home and workplace safety are the main factors propelling the market. As governments and insurance firms increasingly require third-party verification there is the need for independent TIC services. Technological advancements like digital inspection tools, IoT-enabled fire detection systems etc are altering the way services are delivered. Furthermore, new compliance requirements are being created by energy facilities, data centers, smart buildings, and transportation infrastructure.

TIC Market for Fire Safety Equipment Dynamics

Market Trends

Stricter fire safety laws, more infrastructure development and more urbanization drive the Testing, Inspection, and Certification (TIC) market for fire safety equipment. Governments and insurance companies, enforce stronger compliance requirements that increases demand for certified suppression systems, sprinklers, extinguishers, and alarms. The use of AI-driven predictive inspections, remote audits, digital compliance management, and IoT-enabled fire detection systems are some of the major themes. Demand is also driven by rising awareness of industrial safety and the adoption of smart buildings. International standard harmonization and third-party certification are also becoming essential for manufacturers operating worldwide.

Growth Drivers

Fire safety compliance has become a continuous obligation rather than a one-time approval process. Across commercial buildings, factories, logistics hubs, and public infrastructure, regulations increasingly require periodic inspection, functional testing, and third-party validation of installed fire safety systems. These requirements are enforced not only by building authorities but also by insurers and municipal safety departments. As a result, compliance-driven TIC activity now contributes an estimated 35–38% of total market demand, with inspection volumes rising steadily even in years when new construction slows.

A second layer of demand comes from the growing installed base of fire safety equipment rather than fresh equipment sales alone. Warehouses, data centers, power plants, and high-density residential complexes rely on detection and suppression systems that must be inspected and tested at fixed intervals. Global spending on fire protection equipment crossed USD 90 billion in 2023, and every expansion of this installed base increases recurring TIC requirements. Services linked to existing system inspection and performance testing are expanding at close to 7% annually, largely independent of economic cycles.

Technology adoption is also reshaping certification and testing needs. Addressable fire alarms, smart detectors, integrated building safety platforms, and gas-based suppression systems introduce software, communication, and interoperability risks that were previously irrelevant. Certification today extends beyond hardware compliance to system behavior under simulated fire conditions. TIC demand related to advanced and digitally integrated fire safety equipment is growing faster than the overall market, with growth trending toward the 8–9% range.

Market Restraints / Challenges

The testing, inspection, and certification market face certain challenges like trade wars and growth fluctuations, huge investment for automation and installation of industrial safety systems, high cost of TIC owing to diverse standards and regulations of fire testing services globally. Moreover, lack of awareness about fire safety in emerging economies, testing facilities, and skilled personnel may hamper the growth of the TIC market.

Market Opportunities

Increasing accuracy and efficiency through the use of cutting-edge technologies like IoT, AI-driven inspections, and predictive maintenance are examples of growth potential. There are numerous potential in the TIC market for fire safety equipment as global regulatory compliance tightens and fire safety awareness increases. Digital platforms and remote audits can expedite reporting and lower expenses. The need for TIC services is being driven by emerging economies' expansion of infrastructure and fire safety regulations, particularly in Asia-Pacific and other developing regions. New revenue sources are provided via joint ventures with construction companies and forays into non-traditional industries (such as data centers and EV charging stations).

Global TIC Market for Fire Safety Equipment Industry Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 1.1 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 1.75 Billion

|

|

Growth Rate

|

4.8%

|

|

Segments Covered in the Report

|

Service Type, Sourcing Type, Equipment category and End-use Environment

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

North America, Europe, Asia Pacific

|

TIC Market for Fire Safety Equipment Segmentation

By Service Type

Inspection services represent the largest portion of TIC activity in fire safety equipment, contributing approximately 43–45% of total revenue due to mandatory periodic checks across commercial and industrial buildings. Testing services account for around 33–35%, driven by functional testing of alarms, sprinklers, suppression agents, and control panels. Certification services remain smaller at roughly 20–22%, but retain stable demand due to regulatory approvals and insurance acceptance requirements.

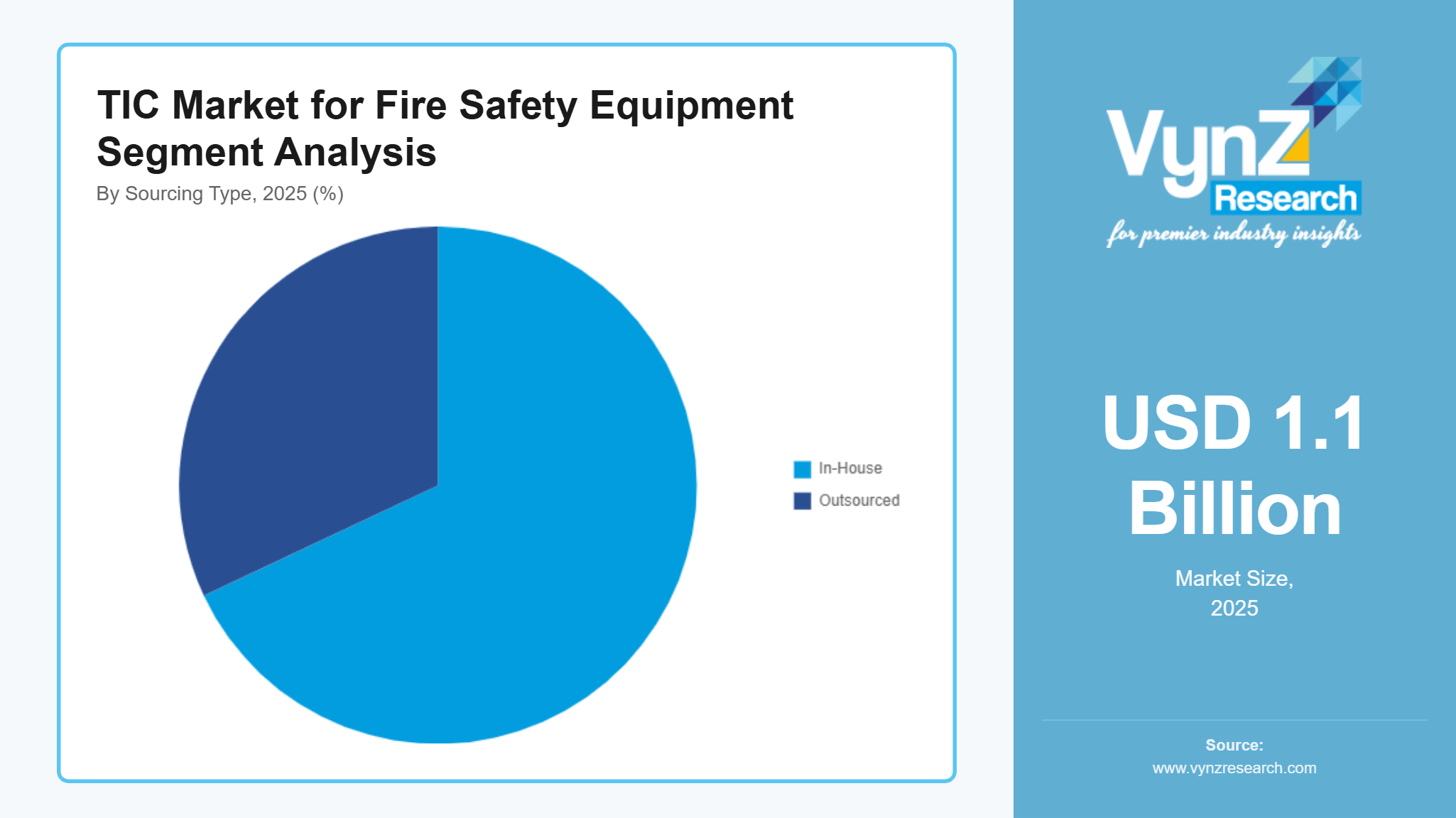

By Sourcing Type

Outsourced TIC services dominate the market, accounting for nearly 68% of total demand, as most building owners and facility operators do not maintain accredited internal inspection capabilities. Independent service providers are preferred for regulatory neutrality and insurer recognition. Outsourced services are expanding at about 7.5–7.8% CAGR. In-house TIC activity, largely confined to large industrial facilities and government assets, grows more slowly at around 4%.

By Equipment Category

Fire detection systems generate the highest TIC demand, contributing close to 38% of service volumes, reflecting frequent inspection cycles and sensitivity of electronic components. Fire suppression systems, including sprinklers and gas-based solutions, follow with roughly 32% share, supported by strict performance validation requirements. Portable extinguishers and evacuation systems account for the remaining demand, though suppression-related TIC services are growing faster at nearly 8% annually.

By End-Use Environment

Commercial buildings account for just over 40% of TIC demand, driven by offices, malls, hospitals, hotels, and institutional buildings with fixed inspection schedules. Industrial facilities represent approximately 33–35% of demand due to higher fire risk and insurance-linked audits. High-rise residential buildings form a smaller share today but are expanding at close to 8% CAGR as urban safety regulations tighten.

Regional Insights

North America

North America represents one of the most regulation-intensive markets for fire safety TIC services, contributing roughly 30–32% of global revenue. The United States leads demand due to strict building codes, strong enforcement, and high insurance penetration across commercial and industrial properties.

Recurring inspection requirements across offices, healthcare facilities, logistics centers, and data centers create stable service volumes. TIC services linked to installed fire safety systems in North America are expanding at around 6.5–6.8% annually, supported more by compliance cycles than new construction activity.

The region also shows growing demand for certification of smart fire detection systems, particularly in large commercial and mixed-use developments adopting integrated building management platforms.

Europe

Europe accounts for approximately 25–27% of global TIC demand for fire safety equipment and is characterized by harmonized regulatory standards and high compliance consistency. Growth in the region is steady rather than rapid, supported by mandatory inspection regimes across commercial and residential buildings.

Fire safety TIC activity in Europe is increasingly influenced by renovation and retrofitting of older buildings to meet updated safety standards. Inspection and testing services related to system upgrades are growing at around 6.8–7% annually.

In addition, stricter safety requirements for public buildings and transport infrastructure continue to support long-term demand for independent testing, inspection, and certification services.

Asia Pacific

Asia Pacific is the fastest-growing regional market, with expansion estimated between 8% and 9% CAGR. Rapid urbanization, vertical construction, and industrial expansion across China, India, and Southeast Asia are increasing the need for structured fire safety inspection and certification.

Historically uneven enforcement is becoming more consistent, particularly in major cities and export-oriented industrial zones. This shift is driving increased reliance on third-party TIC providers rather than internal checks. Public infrastructure and high-rise residential projects are major contributors to regional growth.

As regulatory oversight strengthens, TIC demand is transitioning from reactive inspection to scheduled, recurring compliance programs across the region.

Competitive Landscape / Company Insights

Market competitiveness is centered on technological innovation, such as IoT-enabled testing and digital compliance solutions. Bureau Veritas, SGS S.A., Intertek Group plc, TUD SUD and UL LLC led the market. Global laboratory networks, digital inspection technologies, regulatory experience, and brand credibility are these companies' main areas of competition. Regional providers give cost-effectiveness and specialized fire safety certification services. Primary growth tactics include strategic mergers, acquisitions, and international expansions, especially in the Asia-Pacific and Middle East regions.

Mini Profiles

Bureau Veritas is a France-based global TIC giant with a long history in testing, inspection and certification across industries. It offers fire safety compliance services worldwide, helping ensure regulatory conformity and performance standards.

SGS S.A. is a Swiss multinational providing a broad suite of testing, verification, inspection and certification services. Its large global network supports fire safety system testing and compliance across sectors.

Intertek Group is an UK-based TIC group offering safety testing, inspection and certification, serving fire protection and broader product compliance markets.

UL LLC is an U.S. safety science and certification organization known for fire safety standards and lab testing.

Key Players

- Intertek Group Plc

- Bureau Veritas

- MISTRAS Group

- SGS SA

- Eurofins Scientific

- TUV Rheinland

- TUV SUD

- DEKRA SE

- Applus+

- DNV GL

Recent Developments

In January 2026, UL Solutions has introduced a dedicated testing and certification framework for plug-in “balcony” solar systems, defining safety and performance requirements that support broader residential solar adoption in the United States. This initiative aims to create clearer safety standards for these small-scale solar products and help align legislation with certification criteria.

In November 2025 - Intertek Group Plc, a leading Total Quality Assurance provider to industries worldwide, has acquired Suplilab, a market-leading provider of food safety and medical devices testing services, based in San José, Costa Rica. Acquisition of Suplilab has given Intertek immediate access to attractive ATIC growth opportunities in Central America.

In December 2025 - Bureau Veritas Marine & Offshore (BV) has classed its first methanol-fueled containership, CMA CGM ANTIGONE. The 15,000 TEU methanol dual-fuel vessel was built by CSSC Jiangnan Shipyard for the CMA CGM Group.