Asia Pacific Electric Bus Market Overview

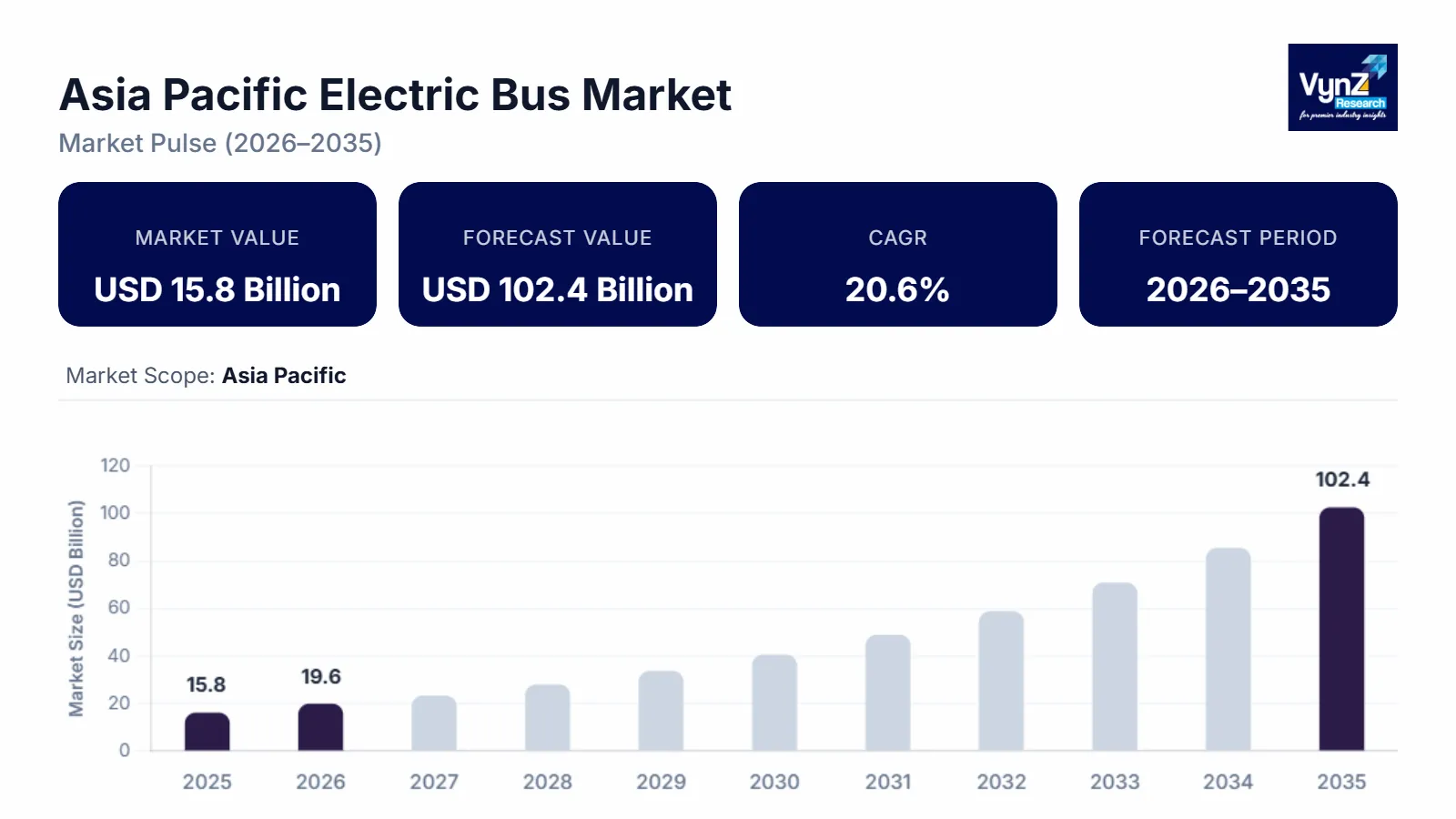

The Asia Pacific electric bus market which had a value of about USD 15.8 billion in 2025 and is expected to grow to around USD 19.6 billion by 2026, will achieve a market value of approximately USD 102.4 billion by 2035 which will expand at a compound annual growth rate of 20.6% from 2026 to 2035.

The market experiences growth because government agencies provide strong support for zero emission public transport systems, urban areas continue to develop which creates more demands for mass transit services, and rising fuel prices drive transit systems toward electrification while battery electric bus systems gain more users. Market expansion in major regions such as China, India and Japan benefits from rising demand for sustainable urban mobility solutions and ongoing public transport electrification program investments.

The region uses government-backed initiatives along with policy frameworks to speed up technology adoption throughout its territories. The International Energy Agency reports that China remains the top global electric bus operator through its extensive public procurement programs which provide subsidies for fleet electrification. National schemes in India along with central authorities backed public transport electrification programs help drive adoption through demand incentives and infrastructure development while Japan uses hydrogen fuel cell technology and battery electric integration to decrease transport emissions. The World Health Organization established environmental guidelines and air quality improvement targets which require urban areas to cut vehicular emissions, so these guidelines lead to stronger policy support for electric mobility adoption.

Asia Pacific Electric Bus Market Dynamics

Market Trends

The industry is experiencing major technological changes together with new purchasing practices and electric vehicle deployment methods because of regulatory requirements and sustainability initiatives. The market is currently experiencing a major shift toward battery electric buses and zero emission bus technologies which results from the need for more efficient energy systems, reduced operational costs and decreased urban pollution. Public transport authorities are increasingly supporting large scale electrification initiatives which receive backing from national clean mobility roadmaps and emission reduction goals.

Advanced battery technologies together with smart fleet management systems are being integrated into new systems which maintain continuous development through energy storage technology and digital monitoring technology. The product development process is being determined by real time vehicle diagnostics and telematics integration together with route optimization. The International Energy Agency reports that electric buses are becoming more common in urban transit networks because of decreased battery prices and better charging infrastructure which is transforming market competition.

Growth Drivers

The market is experiencing growth because government policies that support low emission transportation create permanent demand for electric buses in urban transit systems and public fleet operations. Public transport infrastructure projects create a charging network and depot electrification system, which drives market growth across urban areas with high population density. The national electrification programs and their subsidy structures enable transport agencies to transition their diesel operations into full electric vehicle usage through their large-scale implementation programs.

The combination of environmental issues and new emission regulations has resulted in increased electric bus adoption rates. Public authorities and transit operators need electric buses to achieve their climate goals while cutting operational costs and boosting energy efficiency, which will maintain strong demand for these vehicles throughout the entire forecast period. The World Health Organization established policy frameworks and urban air quality improvement initiatives which provide essential methods for reducing transport emissions, enabling major regional economies to adopt electric vehicles permanently.

Market Restraints / Challenges

The market has positive growth projections, yet several obstacles will hinder its market development. The high initial expenses linked to electric buses and their charging equipment together with battery replacement costs, create obstacles for transit agencies in developing countries which have limited budgets to invest in electric buses. The process of purchasing new equipment for large-scale deployment of electric vehicle fleets faces delays due to two main issues, which include budget limits and restricted financing options.

Manufacturers and suppliers encounter operational difficulties because they depend on battery supply networks and essential raw material vendors for their business operations. The market experiences economic difficulties because businesses that depend on imported lithium-ion batteries and electronic components face three major challenges, which include increased expenses and interruptions in supply chain operations as well as obstacles to market expansion. The International Energy Agency reports that battery material supply chains exhibit concentration risks which can impact production output and long-term pricing trends in the industry.

Market Opportunities

The market offers substantial growth possibilities through the development of electric mobility infrastructure, which will expand in response to urban population growth and rising demand for environmentally friendly public transport systems. Government transit agencies and private fleet operators who need cost-effective electric buses will purchase from companies that provide modular electric buses with their high-performance capabilities.

The development of smart and connected transport ecosystems creates major business potential through digital fleet management systems, autonomous technologies and energy optimization systems which help companies develop operations that deliver better performance with long-term contracts. The development of charging technology solutions, which include fast charging and battery swapping systems, will provide businesses with better operational flexibility and increased usage of their entire fleet. The World Health Organization and regional energy agencies support clean transport programs and climate action frameworks, which drive the adoption of electric vehicles and create long-term market growth for electric buses in the Asia Pacific region.

Asia Pacific Electric Bus Market Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 15.8 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 102.4 Billion

|

|

Growth Rate

|

20.6%

|

|

Segments Covered in the Report

|

Propulsion Type, Bus Length, Battery Type, End Use

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

China, India, Japan, South Korea, Rest of Asia Pacific

|

Asia Pacific Electric Bus Market Segmentation

By Propulsion Type

The market for battery electric buses reached its highest point in 2025 when they generated approximately 68% of total market revenue. The technology achieves market leadership through its extensive implementation in public transportation systems which receive funding from government-backed acquisition programs and mandatory reduction of emissions. Urban areas with high population density have seen increased adoption because strong policy support delivers both subsidies and electrification targets. The International Energy Agency reports demonstrate that transit authorities prefer battery electric buses because these vehicles deliver better operational performance while producing fewer emissions throughout their entire lifespan.

The fuel cell electric bus market will experience its most rapid growth during the forecast period from 2026 to 2035 with a projected compound annual growth rate of 22.1%. Hydrogen infrastructure development drives market expansion because it creates more funding opportunities for alternative clean fuel technologies and enables government backing of multiple zero emission transportation solutions. The countries of Japan and South Korea are working to develop hydrogen mobility systems because these systems will promote development within the hydrogen mobility sector.

The transition to fully electrified bus systems will lead to moderate growth for plug in hybrid electric buses, which will achieve an estimated 14.8% CAGR boost through their first years of transitional adoption in areas without complete electrification infrastructure. The new bus models enable operational flexibility for transportation systems while decreasing their need for charging infrastructure, which leads to continued demand in developing transit systems.

By Bus Length

The market segment between 9 to 14 meters reached its highest market share in 2025 when it produced around 57% of total revenue. The system achieves its greatest usage because urban public transit networks depend on it to maximize passenger capacity while providing flexible route options. Standard-sized bus demand in metropolitan areas keeps growing because of ongoing urbanization and the establishment of intra-city transit networks. The segment experiences growth from government spending on city transport modernization projects.

The market will experience the highest growth through buses that exceed 14 meters, which will achieve a 21.4% CAGR increase throughout the forecast period. The demand for high-capacity bus rapid transit systems and intercity routes, which requires highly populated urban centers to provide public transportation system capacity, drives market expansion. The growing number of passengers and need for congestion control led to increased use of articulated buses and long capacity buses.

The below 9-meter segment is projected to grow at a CAGR of 15.2% because feeder routes and last mile connectivity and smaller urban clusters require more deployment. The demand for flexible and affordable transport options drives the need for transport solutions in semi-urban areas and developing regions.

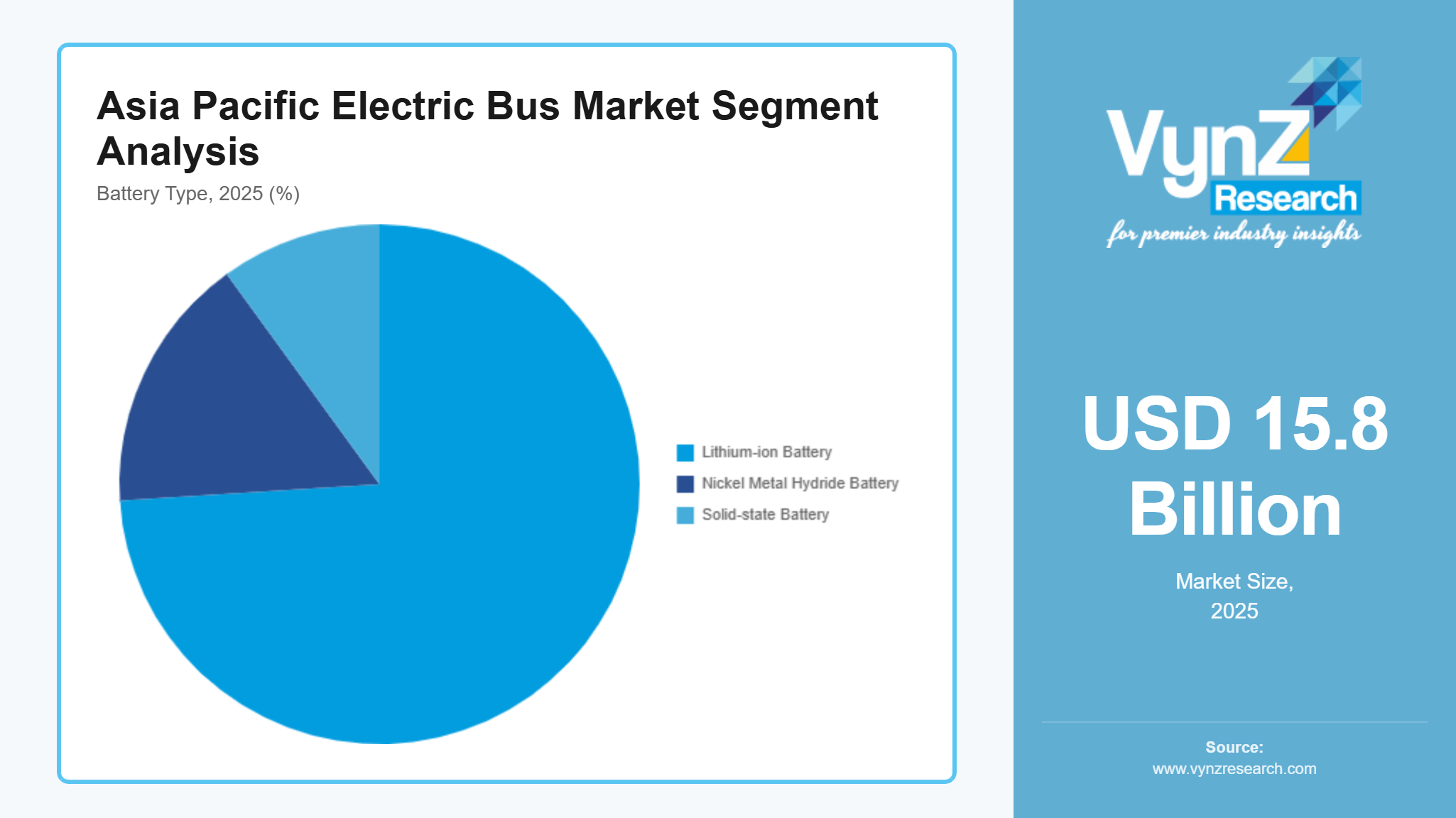

By Battery Type

Lithium-ion batteries accounted for the largest share of the market in 2025 because they represented approximately 74% of total segment revenue. The market position of the product exists because it offers high energy density together with extended product lifespan and decreasing costs which result from large scale production and technological progress. The International Energy Agency reports that lithium-ion battery prices have decreased significantly during the last decade, which allows electric buses to be deployed cost effectively in public transportation networks.

The market will experience solid-state batteries as the fastest growing segment, which will achieve a 23.6% CAGR increase between the years 2026 and 2035. The market expansion exists because research and development strives to enhance energy efficiency while improving safety and charging speed. The battery market will grow through the establishment of new technologies, which will reach commercial status after their development has received adequate funding.

Nickel metal hydride batteries continue to exhibit stable growth with a CAGR of 12.9%, which results from their dependable performance in specific legacy systems. The market share of these products decreases because their energy efficiency does not match the performance of newer battery technologies.

By End Use

Public transport accounted for the largest segment in 2025 which generated 72% of total market revenue. The urban area emissions reduction strategy, which includes government programs to electrify transportation and extensive fleet purchasing together with policy requirements, enables public transportation systems to achieve their highest operational efficiency. The adoption of sustainable mobility infrastructure and the expansion of city bus networks drive transportation networks in both China and India, which represent major economic powers. The World Health Organizations air quality improvement targets compel cities to adopt electric public transport systems as an essential requirement.

Private fleet operators are expected to register the fastest growth with an estimated CAGR of 20.3% during the forecast period from 2026 to 2035. The adoption rate of electric buses for corporate transport and logistics support and institutional programs drives market expansion. The need for sustainability commitments together with operational cost optimization from private companies leads to their active participation in electric mobility.

The market for other applications which include school transportation and shuttle services will experience a 16.7% CAGR increase because people are becoming more aware of clean mobility options and institutions are gradually adopting electric transport systems. The segment growth process receives support from both infrastructure development and policy frameworks which create a favorable environment.

Regional Insights

China

China achieved 58% market share in 2025 because its electric public transport system expansion combined with its domestic production capacity. The major urban centers of Beijing, Shanghai and Shenzhen show extensive system use because the government supports their public transportation programs through procurement and subsidy initiatives. The International Energy Agency reports that China currently holds the top position worldwide for electric bus deployment because the country continues to finance its clean mobility system and battery manufacturing infrastructure development.

India

In 2025 India holds an 11% market share which continues to grow because of its fast urban development and rising need for environmentally friendly public transportation systems. The public fleet electrification initiatives together with demand from Delhi, Mumbai, and Bengaluru metropolitan areas create continuous need for electric buses. The state transport departments are advancing electric bus implementation through their vehicle procurement programs and government-backed electric mobility promotion initiatives.

Japan

The Japanese market will reach 6% share in 2025 because the country drives its market growth through technological advancements and development of clean energy alternatives. Tokyo and Osaka are modernizing their public transport systems through their investments in electric and hydrogen powered buses which will lower emissions. The increasing use of battery electric systems with fuel cell technology creates possibilities for companies to pursue multiple electric power distribution methods.

South Korea

The market in South Korea is growing because the country develops its clean transportation policies while constructing new infrastructure which supports 4% of market demand. The national decarbonization strategies drive Seoul and other major cities to expand their electric bus fleets. The market penetration in the region expands when companies invest in smart transport systems and battery technologies. The remaining market is shared by the other regions.

Competitive Landscape / Company Insights

In this highly competitive market, global manufacturers and regional manufacturers compete in the market through their established presence and product development and cost reduction and international market expansion efforts. Companies are increasing their research and development spending and their battery technology development and their digital fleet management system development to improve their market power. The International Energy Agency reports that manufacturers are focusing on energy efficiency and lifecycle cost reduction while government-backed electrification programs are increasing competition across major regional markets.

Mini Profiles

Ashok Leyland focuses on electric bus manufacturing and integrated mobility solutions, supported by strong domestic distribution networks, cost efficient production capabilities, and established brand presence across public transport segments in Asia Pacific.

BYD Company Ltd. operates in mass electric mobility segments, emphasizing battery innovation, performance efficiency, and vertically integrated manufacturing, enabling competitive pricing and large-scale deployment across urban transit systems globally.

CRRC Corporation Limited leverages extensive local manufacturing capabilities and government backed contracts to expand market presence, supported by strong engineering expertise and large scale production capacity in rail and electric bus systems.

Daimler Truck AG focuses on premium electric bus and commercial vehicle solutions, supported by advanced engineering, strong global brand recognition, and continuous investment in sustainable transport technologies and digital fleet solutions.

Foton Motor Group operates in cost competitive segments, emphasizing scalable production, performance optimization, and strategic partnerships, enabling expansion across emerging markets and strengthening its position in electric commercial vehicle manufacturing.

Key Players

- Ashok Leyland

- BYD Company Ltd.

- CRRC Corporation Limited

- Daimler Truck AG

- Foton Motor Group

- Higer Bus Company Limited

- Hyundai Motor Company

- Tata Motors Limited

- Volvo Group

- Yutong Bus Co., Ltd.

Recent Developments

In November 2025, BYD secured a contract in Singapore to pilot Level 4 autonomous electric buses, marking a significant step toward integrating automation with electric mobility solutions. This development reflects increasing government support for smart transport systems and next generation urban mobility deployment.

In May 2025, Yutong introduced its U12DD 12-meter battery electric double deck bus in Zhengzhou, strengthening its product portfolio in high-capacity urban transit solutions. The launch highlights growing demand for advanced electric buses designed for dense metropolitan transport networks.

In July 2025, Tata Motors emerged as the lowest bidder for a major articulated electric bus project in Nagpur, supported by government backed urban mobility initiatives. The project includes deployment of high-capacity buses and charging infrastructure to improve city transport efficiency.

In November 2025, Hyundai secured a contract to supply electric buses to Indonesia under an international green mobility program, expanding its presence in Southeast Asia. This development reflects increasing cross border collaborations and government backed electrification programs in emerging markets.

In January 2026, Foton continues expanding its electric bus operations through international deployments and partnerships, strengthening its footprint in emerging and export markets. The company’s strategy aligns with increasing global demand for cost efficient electric mobility solutions and large-scale fleet electrification.