Europe Light Electric Vehicle Market Overview

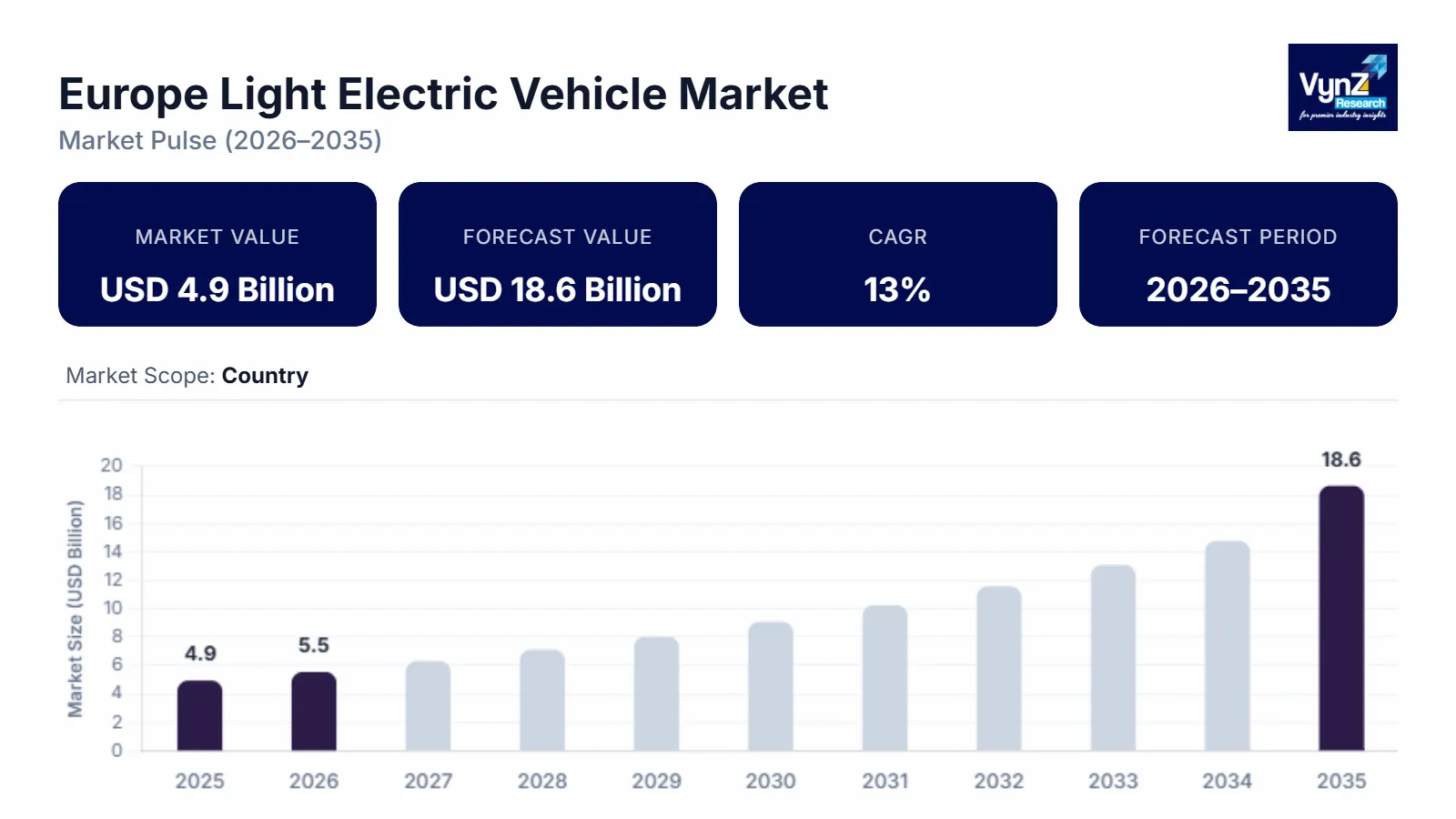

The Europe light electric vehicle market which was valued at approximately USD 4.9 billion in 2025 and is estimated to rise further up to almost USD 5.5 billion in 2026, is projected to reach around USD 18.6 billion by 2035, expanding at a CAGR of about 13% during the forecast period from 2026 to 2035.

The market experiences growth because three factors are driving short distance electrification, environmental regulations becoming more stringent and government financial support for electric mobility grows. The industry experiences growth because urban residents need small electric transport options which serve both their daily commutes and their last mile delivery needs in multiple European cities that prioritize congestion control and pollution reduction.

The adoption of sustainable transportation policies and low emission transportation policies from regional authorities strengthens their commitment to sustainable mobility. The government support of subsidy programs together with electric mobility tax break programs and charging station development activities in Germany, France and the Netherlands enhances light electric vehicle accessibility. International energy and climate agencies report that urban areas are using electric vehicle adoption as a primary method to decrease greenhouse gas emissions produced by road transportation. The development of dedicated cycling paths, shared mobility services and smart city transportation systems across major European cities creates additional demand for light electric mobility solutions throughout the entire region.

Europe Light Electric Vehicle Market Dynamics

Market Trends

The industry is moving toward sustainable micro mobility solutions and digitally integrated urban transport systems because of changing consumer mobility patterns and environmental policy priorities that exist in European nations. The European Commission climate neutrality roadmap supports public transport and mobility frameworks that require decreased usage of fossil fuel transport and increased development of low emission personal mobility solutions. Urban areas that prioritize congestion relief together with energy efficient design are now choosing electric bicycles and compact electric scooters and lightweight urban vehicles. Municipal authorities in cities like Amsterdam, Paris and Berlin are using smart mobility programs to develop mobility networks that connect cycling infrastructure with shared electric mobility fleets and digital route management platforms. Manufacturers are being motivated to create lightweight vehicles which include advanced battery technology and connected mobility features that will improve user experience and operational performance.

Growth Drivers

The European transport sectors have experienced market growth because environmental regulations and carbon reduction commitments have become mandatory. The European Union Green Deal climate policies require governments to decrease greenhouse gas emissions from road transport which leads to swift electric mobility technology adoption. International energy agencies report that short distance mobility electrification is essential for achieving urban transport emission reductions and energy efficiency targets. The electric bicycle subsidy programs implemented by Germany, France and the Netherlands are making electric bicycles and personal electric mobility devices more accessible to urban commuters and delivery service operators.

The increasing need for economical last mile delivery and urban delivery services stands as the main driver for this trend. Logistics providers are now deploying lightweight electric mobility solutions in European cities because e commerce distribution networks have expanded rapidly throughout the region. The government has established urban mobility strategies to promote zero emission delivery vehicles which businesses must use in city centers because they want to decrease air pollution and traffic congestion.

Market Restraints / Challenges

The operational constraints of the sector will impact its adoption rates despite the existence of strong policy support and technological development. The primary obstacle arises from electric mobility devices which have their power range and operational capabilities restricted compared to traditional transportation methods. European transport policy agencies report that battery capacity and charging time and lifecycle costs play a critical role in consumer purchasing behavior especially among users who prioritize price.

Manufacturers and mobility service providers must deal with compliance challenges because European countries have different regulatory frameworks which establish speed limits and vehicle classifications and licensing requirements. International energy organizations report that lithium and cobalt and rare earth material supply exist in concentrated locations throughout the world which leads to price changes and procurement difficulties. Manufacturers who depend on imported battery components and semiconductor technologies face cost volatility and production delays which occur during supply disruptions that impact their entire regional product availability.

Market Opportunities

European urban centers present substantial market prospects through the development of smart city mobility infrastructure and digitally integrated transportation systems. The European environmental programs back municipal mobility strategies which focus on developing low emission mobility corridors. expanding cycling infrastructure and creating digital transport platforms that connect public transit with micro mobility services. The market provides favorable business conditions to manufacturers and mobility operators who deliver high performance electric bicycles and scooters and lightweight delivery vehicles.

The development of battery technology and energy efficient drivetrain systems for compact electric vehicles creates a valuable business opportunity. European energy and mobility agencies fund research and innovation programs to develop battery technology which improves battery density and charging speed and creates lightweight vehicle materials that enhance operational efficiency. The European market offers shared mobility operators, logistics providers and urban commuters who seek sustainable transportation solutions an increasing demand for companies which develop modular battery systems and connected mobility features and fleet management platforms.

Europe Light Electric Vehicle Market Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 4.9 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 18.6 Billion

|

|

Growth Rate

|

13%

|

|

Segments Covered in the Report

|

By Product, By Voltage, By Application and By Battery

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

Western Europe, Northern Europe and Southern Europe

|

Europe Light Electric Vehicle Market Segmentation

By Product

The battery electric vehicle segment achieved the highest market share in 2025 when it generated approximately 44% of total segment revenue. European countries throughout the continent enact strict emission regulations which sustain their dominance while governments provide strong backing to zero emission transportation methods. The policy frameworks designed to decrease carbon emissions from road transport results in consumers and fleet operators switching to battery powered mobility options. European economies dedicate increasing funds to battery manufacturing facilities and charging network construction which strengthens this market segment's position within the regional mobility network.

The plug-in hybrid electric vehicle market will experience the fastest growth during the forecast period at an expected annual growth rate of about 14%. The product range enables buyers to drive their vehicle at maximum distance because it combines electric system power with traditional gasoline engine power. The hybrid electric vehicle segment maintains stable market presence because it offers reasonable pricing and operates with existing fuel infrastructure. The transportation sector will see increasing hybrid and plug-in hybrid system implementation because of better powertrain efficiency and energy management system development.

By Voltage

The 48V category reached its peak market share in 2025 when it accounted for approximately 38% of total segment revenue. Its prominent market position exists because the product delivers balanced performance and better energy efficiency while supporting all light electric mobility vehicles from compact cars to urban transport systems. Automotive manufacturers implement 48V electrical systems because they successfully boost power delivery while keeping battery usage at efficient levels. European automotive manufacturers use advanced electric drivetrain systems together with vehicle electrification technologies which enhance their 48V electrical system.

The higher voltage standards 60V and 72V will demonstrate faster growth during the upcoming period with an expected annual growth rate of approximately 15%. The systems deliver better power output which results in extended operational range therefore they prove beneficial for high-performance light electric vehicles and commercial mobility vehicle systems. The entry-level transportation market and small electric transport systems still use 24V and 36V systems as their main voltage standard.

By Battery

The market in 2025 saw lithium cobalt battery systems achieve the highest market share which generated around 41% of total revenue from that market segment. Their leadership position arises from their ability to deliver high energy density, better power output and their steady performance across all compact electric mobility systems. Ongoing European energy transition research programs drive progress in lithium-based battery technology which enhances energy storage performance and increases vehicle driving distance.

The forecast period will see lithium-ion polymer batteries achieve the highest growth rate with an expected CAGR of approximately 14%. The battery design provides better safety features which enable weight reduction, form flexibility and design. The market continues to use nickel metal hydride batteries because they provide dependable performance with established production infrastructure. The battery segment will experience structural changes because manufacturers will focus on advanced lithium-based battery technologies which deliver better energy efficiency and vehicle performance improvements.

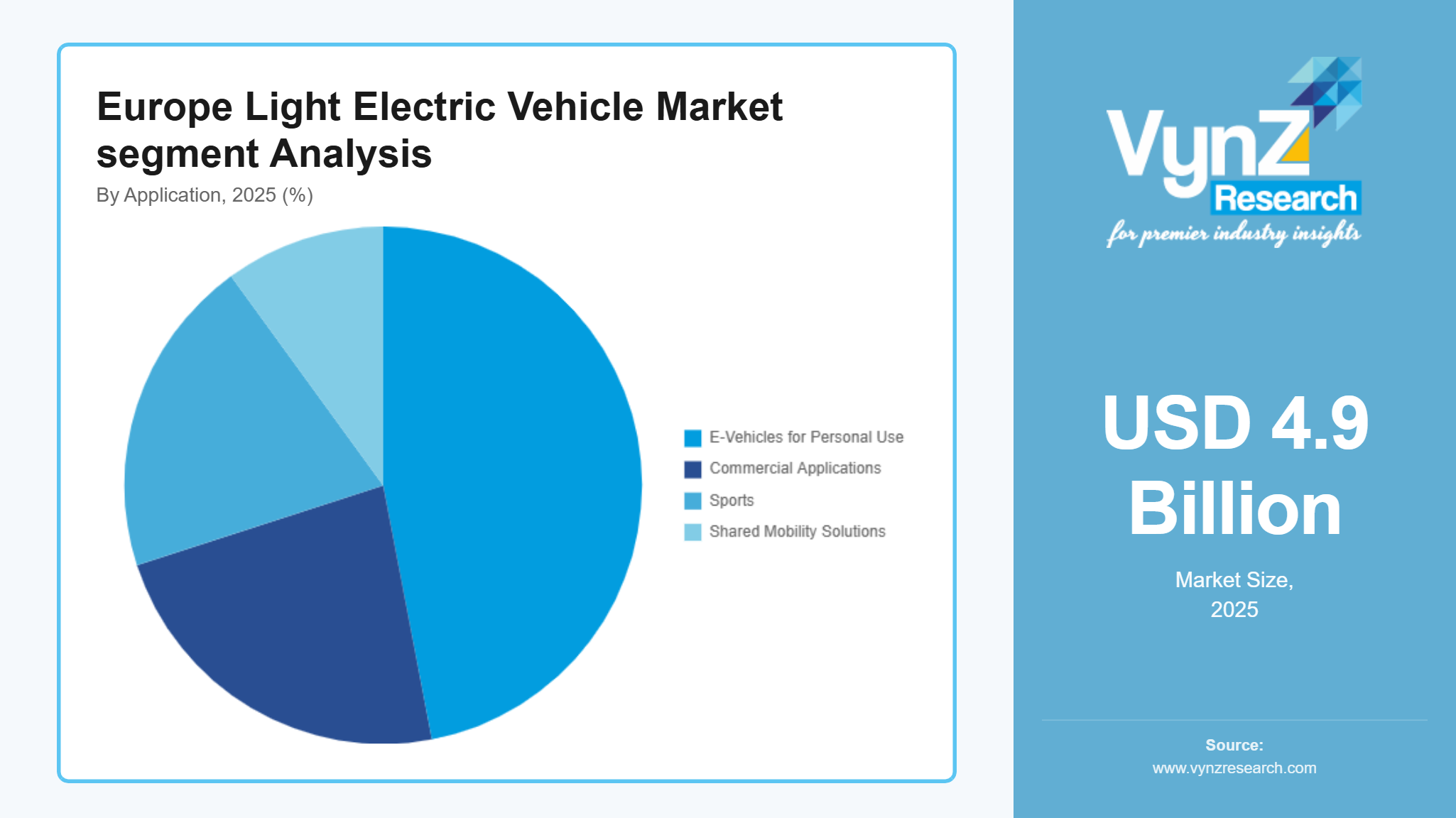

By Application

The personal mobility segment reached its highest market share in 2025 when it accounted for about 47% of the total segment revenue. European cities see urban commuters using light electric mobility solutions for both short distance travel and daily commuting and recreational activities. Public funding for cycling infrastructure combined with sustainable urban transportation programs leads to increased usage of personal electric mobility products in metropolitan areas.

The shared mobility solutions market will achieve the highest growth rate during the forecast period with an estimated CAGR of about 16%. The quick development of urban micro mobility systems and digital fleet management systems enables cities across Europe to implement shared electric vehicle networks. Businesses in commercial sectors adopt efficient environmentally friendly transportation solutions which they need to support logistics operations, courier services and urban delivery work. Government initiatives which promote low-emission urban transport systems will increase the demand for light electric mobility solutions which serve personal and commercial transportation needs.

Regional Insights

Western Europe

The market in 2025 saw Western Europe take the largest regional share which amounted to 34% because the region had strong automotive manufacturing capabilities and showed early acceptance of sustainable transportation methods. Germany, France and the Netherlands built electric mobility systems which included extensive charging networks and supportive regulatory frameworks to create electric mobility systems. Berlin, Paris and Amsterdam currently experience rising usage of compact electric vehicles which people use for short distance travel and shared transportation services.

The European Commission Green Deal established government climate strategies together with emission reduction goals which promote large scale electrification efforts in transportation systems. The national incentive programs which help people buy electric vehicles together with public charging network investments and battery technology research funding lead to more people using light electric vehicles in urban and suburban areas.

Northern Europe

The regional market in 2025 will see Northern Europe capture 25% of the market share through its strong environmental awareness and established clean mobility policies. Norway, Sweden and Denmark have become leading electric mobility solution adopters because their consumers widely accept sustainable transportation while their governments back zero emission mobility systems. The cities of Oslo, Stockholm and Copenhagen promote micro mobility solutions through their support of electric scooters and bicycles and compact electric vehicles.

The region sees increased light electric vehicle adoption because government programs which focus on carbon neutrality and sustainable urban transport systems. National transport authorities and energy agencies continue to expand charging infrastructure and implement fiscal incentives for electric mobility adoption. The transition to electric transportation systems receives support from these initiatives which include substantial investments in renewable energy integration.

Southern Europe

The market in 2025 saw Southern Europe capture 19% of the market share which resulted from increased urban development and improved financing for sustainable transportation development. The municipalities of Rome, Madrid and Barcelona in Spain and Portugal see rising demand for electric mobility solutions which operate in their crowded urban areas. The region keeps growing its market because people are becoming more interested in urban transport options which produce lower emissions.

Government programs aligned with European Union sustainability targets are encouraging adoption of electric mobility through subsidies tax incentives and infrastructure investments. The national ministries which handle transport and environmental sustainability continue to support electrified urban mobility systems and electric vehicle sharing platforms. The remaining share of the European market is distributed across other countries not specifically covered in the above analysis which collectively contribute to the overall demand for light electric mobility solutions in the region.

Competitive Landscape / Company Insights

The market operates at a competitive level which ranges from moderate to high because global and regional manufacturers have established their presence through product innovations and pricing methods and their expansion into various urban mobility markets. Companies are increasingly investing in advanced battery technologies lightweight vehicle platforms and digital fleet management solutions to strengthen their market position. European cities see enhanced adoption because of European Commission and national transport authorities which provide regulatory frameworks and sustainability programs that support electric mobility infrastructure and aim to decrease transport emissions.

Mini Profiles

BMW focuses on premium electric mobility solutions and advanced battery electric vehicle platforms, supported by strong brand recognition, extensive European distribution networks, and continuous investment in sustainable automotive technologies.

Ford Motor Company operates in mass and performance electric vehicle segments, emphasizing engineering reliability, scalable manufacturing platforms, and expanding electrification strategies supported by established global production and supply networks.

Groupe Renault leverages local manufacturing capabilities and strategic alliances within Europe to expand market presence, offering compact and urban electric mobility solutions supported by efficient supply chains and regional distribution infrastructure.

Mercedes Benz focuses on luxury electric vehicle innovation, supported by strong premium brand positioning, advanced battery technology development, and integrated digital mobility platforms enhancing vehicle performance and consumer experience.

Tesla operates in high-performance electric vehicle segments, emphasizing battery innovation, software-driven vehicle architecture, and direct-to-consumer distribution models that strengthen technological leadership and global market visibility.

Key Players

- BMW

- Ford Motor Company

- Groupe Renault

- Mercedes Benz

- Peugeot S.A.

- Stellantis

- Tesla

- Toyota Motor Corporation

- Volkswagen AG

Recent Developments

In March 2026, Using Geely's electrical architecture, Mercedes-Benz has started developing a new electric car platform in China. The business has given a research facility outside of Germany independent development authority for a new vehicle platform. While the German development center will concentrate on mid-size and big vehicles, the German luxury automaker's Chinese R&D center will now function as the worldwide headquarters for small vehicle development.

In July 2026, With Software Update 2026, Tesla is introducing a new feature called "Comfort Braking."8. The new Model Y is the only vehicle in the Tesla series with this capability. Toyota Motor Corporation and Konica Minolta, Inc. have worked together on dust reduction technologies. Konica Minolta will look into the possibility of developing a dust removal system for a manned pressurized rover in space in collaboration with Toyota.

In January 2025, The new line of electric vehicles that Flexis has unveiled is anticipated to be on sale in 2026. Renault, Volvo, and CMA CGM jointly own the business. It was established in order to provide a new class of urban logistics solutions. The Step-in van, the Cargo van, and the Panel van make up the first lineup. Renault's Ampere division created the electronic architecture for their EV-native skateboard platform.