Green Data Centers Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge / Modular Data Centers), by Component (Solutions, Services), by Technology (Renewable Energy Integration, Energy-Efficient Cooling, Waste Heat Recovery Systems, AI & Smart Energy Management Systems, Modular & Prefabricated Green Infrastructure), by Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs)), by Industry Vertical (IT & Telecommunication, BFSI, Healthcare, Government & Public Sector, Retail & E-commerce, Manufacturing, Media & Entertainment, Others)

| Status : Published | Published On : Feb, 2026 | Report Code : VRICT5219 | Industry : ICT & Media | Available Format :

|

Page : 183 |

Green Data Centers Market Overview

The green data centres market, valued at approximately USD 43.1 billion in 2025 and estimated to reach around USD 58.0 billion in 2026, is projected to reach close to USD 438.0 billion by 2035, expanding at a CAGR of about 25.2% from 2026 to 2035.

The Green Data Centres Market is primarily driven by the growing need to reduce carbon emissions and energy consumption associated with rapidly expanding digital infrastructure. Global data traffic surges due to cloud computing, AI, streaming services, and IoT adoption, and data centres are under increasing pressure to improve energy efficiency and lower their environmental footprint. Governments worldwide are introducing stricter regulations and sustainability mandates that encourage the adoption of renewable energy, efficient cooling systems, and low-PUE designs. Rising electricity costs are also pushing operators to invest in energy-efficient architectures that reduce long-term operational expenses. Major cloud service providers are committing to carbon neutrality and net-zero targets, accelerating investments in green building standards and renewable-powered facilities. Innovations such as liquid cooling, waste heat recovery, and AI-driven energy optimisation further support sustainable operations. Additionally, growing environmental awareness among enterprises and consumers is reinforcing demand for environmentally responsible data infrastructure, driving continued market expansion.

Green Data Centers Market Dynamics

Market Trends

The deployment of energy-efficient cooling technologies is a major trend driving the green data centers market, as cooling systems account for a significant share of total facility energy consumption. Operators are increasingly adopting advanced solutions such as liquid cooling, free cooling, and adiabatic cooling to reduce power usage and improve overall thermal performance. These technologies enable better heat dissipation while consuming less electricity compared to conventional air-based systems. AI-driven cooling optimization tools are also being integrated to dynamically adjust airflow and temperature based on real-time workload demands. The Australian government-owned green bank has committed over $33 billion to clean energy and decarbonisation investments, with a record $4.7 billion in new commitments in the most recent financial year, which supports sustainable infrastructure including renewable power and energy-efficient technologies that data centers can leverage for efficient cooling integration. This helps lower Power Usage Effectiveness (PUE) and reduce operational costs over the long term. Additionally, many facilities are incorporating waste heat recovery systems to reuse excess thermal energy for nearby industrial or residential applications.

Growth Drivers

The rapid growth of cloud computing and AI workloads is a major driver of the green data centers market, as digital transformation continues to accelerate across industries. Enterprises are increasingly migrating applications, storage, and computing resources to cloud platforms to enhance scalability and operational efficiency. Similarly, AI, machine learning, and big data analytics require high-performance processors and GPU-intensive servers that significantly increase energy consumption. This surge in power demand is pushing operators to design more energy-efficient and environmentally sustainable facilities. Reliance and Adani commit a combined $210 billion to AI and data centre infrastructure in India, supported by national policies that offer tax breaks and incentives to stimulate investments in large-scale computing facilities that underpin cloud and AI workloads. Green data centers help manage these high-density workloads through optimized power distribution, advanced cooling technologies, and renewable energy integration. Hyperscale providers are investing heavily in low-carbon infrastructure to support AI-driven services while meeting sustainability commitments.

Market Restraints / Challenges

High initial capital investment is a major challenge in the green data centers market, as building environmentally sustainable facilities requires substantial upfront expenditure. Operators must invest in renewable energy infrastructure such as solar panels, wind power agreements, and energy storage systems to reduce carbon dependency. Advanced cooling technologies, including liquid cooling and free cooling systems, also involve higher procurement and installation costs compared to conventional setups. Additionally, energy-efficient servers, smart power management systems, and green-certified building materials further increase initial project budgets. Achieving certifications such as LEED or other sustainability standards adds design, compliance, and consulting expenses. For smaller operators and developing regions, these high capital requirements can limit adoption.

Market Opportunities

The adoption of advanced energy-efficient cooling technologies represents a significant opportunity in the green data centers market as operators seek to minimize power consumption and environmental impact. Cooling systems traditionally account for a large share of total energy use, making efficiency improvements critical for sustainable operations. Technologies such as liquid cooling, free cooling, and adiabatic systems enable more effective heat dissipation while reducing electricity demand. AI-driven thermal management tools further optimize airflow and temperature in real time, lowering Power Usage Effectiveness (PUE). According to the United Nations Conference on Trade and Development (UNCTAD), data centers captured more than one-fifth of global greenfield investment in 2025, with announced foreign direct investment (FDI) exceeding $270 billion worldwide. This data is published on UNCTAD’s official platform, making it a credible intergovernmental source. These solutions not only cut operational costs but also help meet strict carbon reduction targets. Additionally, energy-efficient cooling reduces dependence on water-intensive systems, supporting broader sustainability goals.

Global Green Data Centers Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 43.1 Billion |

|

Revenue Forecast in 2035 |

USD 438.0 Billion |

|

Growth Rate |

25.2% |

|

Segments Covered in the Report |

Data Center Type, Component, Technology, Organization Size, Industry Vertical, By Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Schneider Electric SE (France), Vertiv Group Corp. (U.S.), Johnson Controls International plc (Ireland), Siemens AG (Germany), ABB Ltd (Switzerland), Eaton Corporation plc (Ireland), Cisco Systems, Inc. (U.S.), Huawei Technologies Co., Ltd. (China), NTT Ltd. (Japan), Google LLC (U.S.), Microsoft Corporation (U.S.), Amazon Web Services, Inc. (U.S.) |

|

Customization |

Available upon request |

Green Data Centers Market Segmentation

By Data Centers Type

Hyperscale Data Centers is the largest category with a market share of about 50% in 2025, due to large-scale investments by cloud providers in renewable-powered campuses and ultra-efficient cooling systems. Hyperscale facilities consume massive amounts of electricity, making sustainability strategies essential for long-term cost control and carbon reduction. Major operators are designing purpose-built green campuses incorporating solar farms, wind PPAs, and optimized PUE designs. The scale of these projects drives substantial infrastructure spending.

Edge / Modular Data Centers is the fastest-growing category with a CAGR of 25.6% during the forecast period, due to rising demand for decentralized, low-latency computing powered by compact and energy-efficient infrastructure. Edge facilities are increasingly designed with modular, prefabricated green components that reduce construction waste and energy use. These systems often integrate renewable microgrids and advanced cooling technologies. Rapid deployment requirements and sustainability mandates are accelerating adoption. The distributed nature of edge infrastructure supports strong growth momentum.

By Component

Solutions is the largest category with a market share of about 70% in 2025, due to the high capital expenditure associated with deploying energy-efficient cooling systems, renewable power integration, advanced UPS systems, and smart monitoring platforms. Green data centers require substantial upfront investment in infrastructure hardware to reduce carbon emissions and optimize energy performance. These solutions form the core operational backbone of sustainable facilities and account for the majority of project budgets. Hyperscale and colocation operators prioritize direct investments in efficient cooling and renewable energy systems to meet net-zero commitments.

There Solutions further classified into followings

- Cooling Systems

- Power Systems (UPS, PDUs, Renewable Integration)

- Monitoring & Management Systems

- Networking Equipment

Services is the fastest-growing category with a CAGR of 25.8% during the forecast period, due to increasing demand for sustainability consulting, energy audits, system integration, and lifecycle optimization. As regulatory requirements become stricter, operators rely on expert advisory services to design energy-efficient architectures and achieve green certifications. Continuous monitoring and predictive maintenance services also support long-term operational efficiency. The complexity of integrating renewable energy and AI-driven management systems further boosts service demand.

There Services further classified into followings

- Consulting

- Design & Integration

- Maintenance & Support

By Technology

Energy-Efficient Cooling Technologies is the largest category with a market share of about 30% in 2025, due to cooling systems accounting for a major share of total data center energy consumption. Operators prioritize liquid cooling, free cooling, and adiabatic systems to significantly lower electricity usage and improve Power Usage Effectiveness (PUE). Cooling optimization directly impacts operational costs and carbon footprint reduction. Because thermal management is critical to performance and sustainability, this technology segment commands the largest investment share.

AI & Smart Energy Management Systems is the fastest-growing category during the forecast period, due to increasing adoption of intelligent monitoring and automation platforms. AI-driven systems optimize power distribution, predict energy demand, and dynamically adjust cooling loads in real time. These technologies enhance efficiency while reducing human intervention and operational costs. Sustainability reporting and carbon tracking become mandatory, smart management systems gain strategic importance.

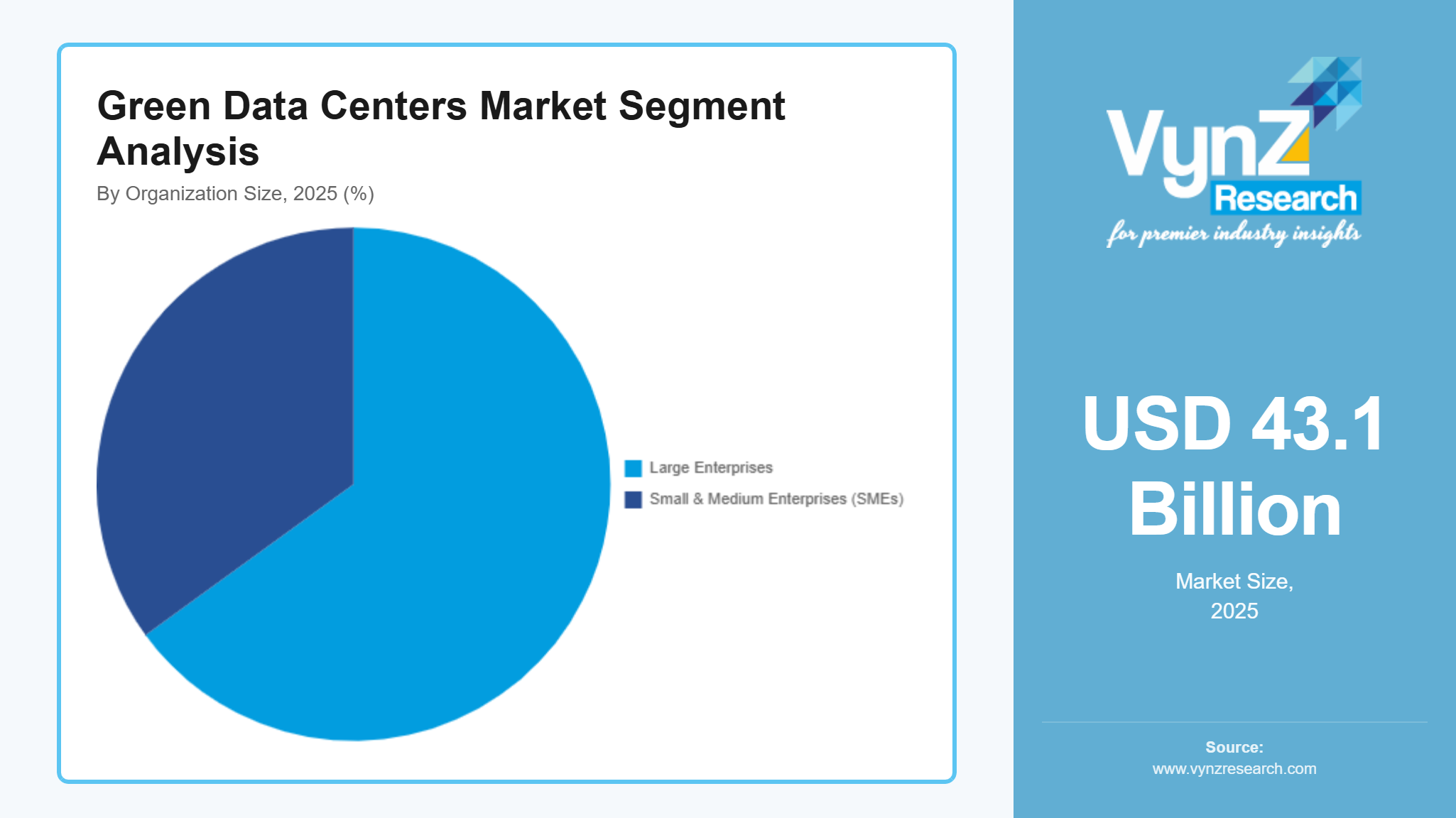

By Organization Size

Large Enterprises is the largest category with a market share of about 65% in 2025, due to their substantial capital resources and strong ESG commitments. Large cloud providers and multinational corporations operate high-capacity facilities that require advanced sustainable infrastructure. They are more capable of investing in renewable energy contracts and high-efficiency technologies. Regulatory pressure and public sustainability pledges further encourage adoption.

Small & Medium Enterprises (SMEs) is the fastest-growing category during the forecast period, due to increasing cloud migration and managed green colocation services. SMEs are seeking sustainable hosting solutions without heavy infrastructure investment. Green colocation options become more accessible, adoption rises among smaller firms.

By Industry Vertical

IT & Telecommunications is the largest category with a market share of about 35% in 2025, due to its heavy reliance on cloud computing, data storage, and digital service delivery. Telecom operators and cloud providers operate extensive data infrastructure requiring energy-efficient and low-carbon facilities. Rapid data traffic growth increases power demand, reinforcing the need for green solutions.

Healthcare is the fastest-growing category with a CAGR of 25.8% during the forecast period, due to increasing digitization of medical records, AI diagnostics, and telemedicine platforms. Healthcare institutions are investing in secure and sustainable data infrastructure to meet regulatory compliance and environmental goals. Rising adoption of high-performance computing for research further increases energy demand. Sustainability commitments within the healthcare sector are accelerating green data center adoption.

Regional Insights

North America

North America is the largest regional market for green data centers, supported by strong hyperscale presence and aggressive corporate sustainability commitments. The United States leads the region with large-scale investments in renewable-powered campuses and carbon-neutral operations. Major cloud providers are signing long-term power purchase agreements (PPAs) for wind and solar energy to reduce grid dependency and meet net-zero targets. The U.S. DOE announced $40 million in funding for 15 projects focused on developing high-performance, energy-efficient cooling solutions for data centers to reduce energy use and carbon emissions directly supporting advanced cooling technologies needed by green data centers. Canada is also emerging as a preferred location due to abundant renewable hydropower and naturally cooler climates that enable free cooling.

Asia Pacific

Asia Pacific is the fastest-growing region in the green data centers market, driven by rapid digital transformation, rising cloud adoption, and expanding renewable energy capacity. China, India, Japan, Singapore, and Australia are witnessing strong investment in sustainable data infrastructure. Governments across the region are promoting energy efficiency policies and encouraging renewable integration to reduce carbon intensity. India’s expanding data center capacity and China’s large-scale renewable projects are accelerating demand for energy-efficient cooling and smart power systems. Singapore is focusing on green building standards and water-efficient cooling due to land and resource constraints. Growing AI workloads and 5G deployment are further increasing energy demand, prompting operators to invest in sustainable designs. Gujarat Government approves ₹25,000 crore investment for a 250 MW green AI-ready data centre campus, aimed at bolstering cloud computing and AI infrastructure, positioning the region as a tech hub with sustainable digital infrastructure that supports energy-efficient operations.

Europe

Europe’s green data centers market is strongly influenced by strict climate regulations and ambitious carbon neutrality targets set by the European Union. Countries such as Germany, the Netherlands, Ireland, France, and the Nordic nations are leading in renewable-powered data center deployment. The region emphasizes energy efficiency, waste heat recovery, and circular economy practices in infrastructure development. Nordic countries benefit from cold climates and renewable hydropower, enabling highly efficient cooling operations. UK modular data center firm Sonic Edge partnered with Deep Green to deploy 50 modular HPC/EdgePod units across the UK powered by carbon-free energy and using immersion cooling technology, enabling highly efficient thermal management and reduced environmental impact for high-performance computing operations. The EU’s sustainability mandates and green financing programs are encouraging investments in low-carbon facilities. Strong public awareness and regulatory enforcement make Europe a benchmark region for environmentally responsible data center operations. The European Union’s €20 billion InvestAI initiative, which includes the development of four large-scale AI gigafactories equipped with around 100,000 next-generation AI chips each, is indirectly relevant to the Green Data Centers Market. These AI facilities will require massive computing power, leading to high energy consumption and significant heat generation.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is gradually expanding its presence in the green data centers market as digital infrastructure develops. In Latin America, countries such as Brazil and Mexico are investing in renewable-powered facilities to support growing cloud and enterprise demand. The Middle East, particularly the UAE and Saudi Arabia, is aligning green data center projects with national sustainability visions and smart city initiatives. In Africa, countries such as South Africa and Kenya are emerging as regional hubs supported by renewable energy expansion and improving connectivity. While infrastructure maturity varies, increasing government focus on sustainability and rising data consumption are expected to accelerate green data center adoption across these regions in the coming years.

Competitive Landscape / Company Insights

The green data centers market is moderately consolidated in nature. A significant portion of the market is controlled by large global infrastructure, engineering, and technology companies that possess strong financial capacity, advanced technological expertise, and established global networks. These players dominate large-scale hyperscale and enterprise green data center projects due to their ability to deliver integrated solutions that combine renewable energy integration, energy-efficient cooling systems, and smart power management technologies. High capital investment requirements act as a major entry barrier in this market. Developing green data centers involves substantial spending on sustainable building materials, advanced cooling technologies, renewable energy procurement, and digital energy optimization systems.

Mini Profiles

Schneider Electric SE (France) develops integrated energy management and data center infrastructure solutions, including energy-efficient cooling, power distribution, and smart monitoring platforms designed to minimize carbon footprint and improve sustainability across digital facilities.

Vertiv Group Corp. (U.S.) offers critical digital infrastructure products and services, such as precision cooling, renewable-ready power systems, and integrated management solutions that support energy-efficient and low-PUE green data center deployments.

Johnson Controls International plc (Ireland) supplies HVAC, power systems, and building automation technologies that enable data centers to achieve energy efficiency and sustainability goals through optimized cooling and advanced energy management.

Siemens AG (Germany) provides a broad portfolio of digital and energy technologies including smart grid integration, energy automation, and green building solutions that support sustainable data center operations and enhanced energy performance.

ABB Ltd (Switzerland) delivers electrification, automation, and energy optimization products that help data center operators reduce energy loss, integrate renewable power sources, and improve overall resource efficiency.

Eaton Corporation plc (Ireland) offers power management solutions including energy-efficient uninterruptible power supplies (UPS), power distribution units, and integrated energy monitoring systems critical for green data center infrastructure.

Key Players

- Schneider Electric SE (France)

- Vertiv Group Corp. (U.S.)

- Johnson Controls International plc (Ireland)

- Siemens AG (Germany)

- ABB Ltd (Switzerland)

- Eaton Corporation plc (Ireland)

- Cisco Systems, Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- NTT Ltd. (Japan)

- Google LLC (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

Recent Developments

February 2026 – Schneider Electric SE launched an enhanced EcoStruxure Green Cooling Suite with AI-driven optimization features, improving energy efficiency and enabling predictive temperature management across hyperscale and colocation data centers.

January 2026 – Microsoft Corporation announced that its global data center operations reached 80% renewable energy usage, backed by long-term power purchase agreements and new wind and solar projects, accelerating its commitment to carbon-neutral operations.

December 2025 – Google LLC signed multiple renewable energy supply deals in Europe and Asia Pacific to power its data center campuses entirely with wind and solar, supporting the expansion of sustainable infrastructure and reducing grid-based emissions.

October 2025 – Amazon Web Services, Inc. announced plans to invest in utility-scale solar and battery storage systems in North America to support long-term renewable integration for its expanding data center footprint.

Global Green Data Centers Market Coverage

Data Center Type Insight and Forecast 2026 - 2035

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Edge / Modular Data Centers

Component Insight and Forecast 2026 - 2035

- Solutions

- Services

Technology Insight and Forecast 2026 - 2035

- Renewable Energy Integration

- Energy-Efficient Cooling

- Waste Heat Recovery Systems

- AI & Smart Energy Management Systems

- Modular & Prefabricated Green Infrastructure

Organization Size Insight and Forecast 2026 - 2035

- Large Enterprises

- Small & Medium Enterprises (SMEs)

Industry Vertical Insight and Forecast 2026 - 2035

- IT & Telecommunication

- BFSI

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Media & Entertainment

- Others

Global Green Data Centers Market by Region

- North America

- By Data Center Type

- By Component

- By Technology

- By Organization Size

- By Industry Vertical

- By Country - U.S., Canada, Mexico

- Europe

- By Data Center Type

- By Component

- By Technology

- By Organization Size

- By Industry Vertical

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Data Center Type

- By Component

- By Technology

- By Organization Size

- By Industry Vertical

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Data Center Type

- By Component

- By Technology

- By Organization Size

- By Industry Vertical

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Green Data Centers Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Data Center Type

1.2.2. By

Component

1.2.3. By

Technology

1.2.4. By

Organization Size

1.2.5. By

Industry Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Data Center Type

5.1.1. Hyperscale Data Centers

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Colocation Data Centers

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Enterprise Data Centers

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Edge / Modular Data Centers

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Component

5.2.1. Solutions

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Services

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Renewable Energy Integration

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Energy-Efficient Cooling

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Waste Heat Recovery Systems

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. AI & Smart Energy Management Systems

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Modular & Prefabricated Green Infrastructure

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Organization Size

5.4.1. Large Enterprises

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Small & Medium Enterprises (SMEs)

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By Industry Vertical

5.5.1. IT & Telecommunication

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. BFSI

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Healthcare

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Government & Public Sector

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Retail & E-commerce

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Manufacturing

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.5.7. Media & Entertainment

5.5.7.1. Market Definition

5.5.7.2. Market Estimation and Forecast to 2035

5.5.8. Others

5.5.8.1. Market Definition

5.5.8.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Data Center Type

6.2. By

Component

6.3. By

Technology

6.4. By

Organization Size

6.5. By

Industry Vertical

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Data Center Type

7.2. By

Component

7.3. By

Technology

7.4. By

Organization Size

7.5. By

Industry Vertical

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Data Center Type

8.2. By

Component

8.3. By

Technology

8.4. By

Organization Size

8.5. By

Industry Vertical

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Data Center Type

9.2. By

Component

9.3. By

Technology

9.4. By

Organization Size

9.5. By

Industry Vertical

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Schneider Electric SE (France)

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Vertiv Group Corp. (U.S.)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Johnson Controls International plc (Ireland)

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Siemens AG (Germany)

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

ABB Ltd (Switzerland)

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Eaton Corporation plc (Ireland)

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Cisco Systems, Inc. (U.S.)

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Huawei Technologies Co., Ltd. (China)

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

NTT Ltd. (Japan)

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Google LLC (U.S.)

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Microsoft Corporation (U.S.)

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Amazon Web Services, Inc. (U.S.)

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Green Data Centers Market