TIC Market for Chemical Industry Overview

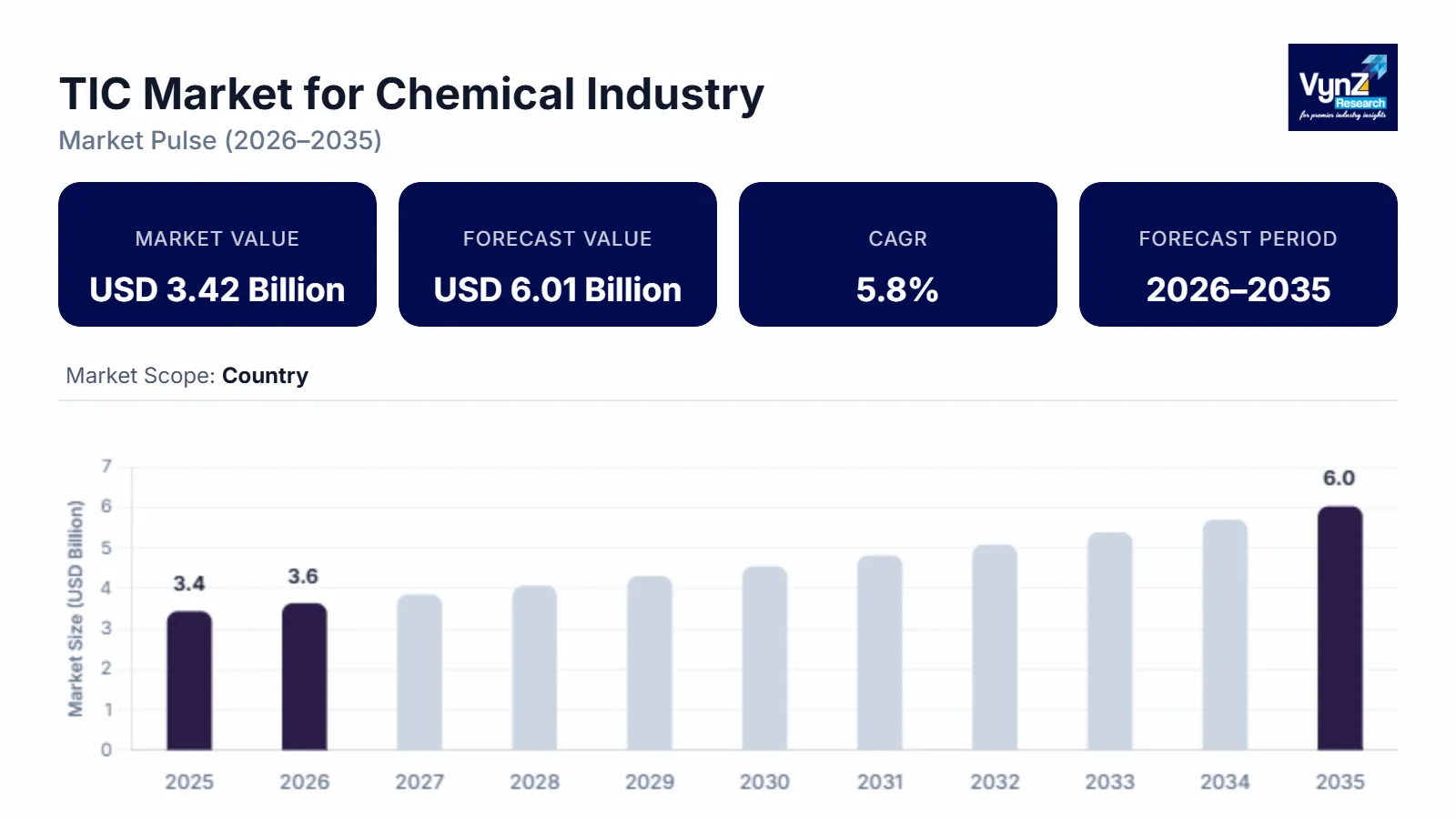

TIC market for chemical industry which was valued at approximately USD 3.42 billion in 2025 and is estimated to reach around USD 3.61 billion in 2026, is projected to reach close to USD 6.01 billion by 2035, expanding at a CAGR of about 5.8% during the forecast period from 2026 to 2035.

Globalization has led to product standardization norms and has penetrated developed technologies across various industries such as the chemical industry, electronics, and automotive industries, etc., resulting in the growth of the TIC market during the forecast period. Moreover, the growing middle-class population, rapid urbanization, mandatory safety regulations, upsurge in the illicit trade of counterfeit and pirated products, advancement in networking and communication technology, the inclination of outsourcing testing, inspection, and certification services has propelled the growth of the TIC market in the chemical industry. Nevertheless, TIC provides various advantages related to its credibility and image, compliance with legal and regulatory requirements, less turnover of employees, high level of cost control improvement, and fast improvement of different processes. It is important to ensure that the quality of products regarding chemical feedstocks like acids, alkalis, and monomers should be reliable, safe, sustainable, and secure in the production and supply chains.

TIC Market for Chemical Industry Dynamics

Market Trends

Globally, service delivery models are changing as a result of risk-based certification frameworks, digital inspection technologies, and laboratory automation. The chemical industry's TIC (Testing, Inspection, and Certification) market is expanding rapidly due to increased cross-border chemical trade, stricter international environmental legislation, and growing safety compliance standards. The need for hazardous material testing, REACH and GHS compliance, and sustainability audits is growing.

Growth Drivers

The chemical manufacturing industry is subject to regulatory pressures that have increased in scope and coverage over different regions instead of stabilizing locally. Regulations pertaining to hazardous substances, emissions, workplace safety, transport classification, and product labeling are enforced at various points along the value chain. Consequently, testing, inspection, and certification activities are needed not only at market entry but also in production and distribution. Compliance-driven TIC operations form around 38–40% of the total chemical industry demand, with the volume of services growing at nearly 6.5–7% yearly as enforcement deepens.

One more fundamental driver is the diversity and risk profile of the chemical products. Industrial chemicals, specialty formulations, agrochemicals, and downstream intermediates all have different testing requirements, and are usually regulated by different authorities. Any change in the formulation, expansion of the capacity, or change of the supplier can become a trigger for new compliance requirements. The demand for TIC linked to formulation testing, safety data validation, and process inspection keeps increasing as a result of growing product complexity and stricter documentation standards.

Environmental accountability is no longer a peripheral demand driver but has become a central one. Monitoring emissions, verifying waste handling, registering substances using REACH, and reporting sustainability now affect the granting of permissions to operate and customer acceptance. Chemical producers are not only evaluated for product safety but also for their environmental performance. TIC associated with environmental compliance and sustainability verification is increasing at a higher rate compared to that of traditional inspection activities, and in several large markets, the growth rate is close to 8%.

Market Restraints / Challenges

The testing, inspection, and certification market face certain challenges like trade wars and growth fluctuations, huge investment for automation and installation of industrial safety systems, high cost of TIC owing to diverse standards and regulations globally. Moreover, high R&D costs, complex processes, use of hazardous reagents, purification issues, the huge volume of waste, and pollution are the challenges faced by the chemical industry. Thus, a lack of testing facilities and skilled personnel may hamper the growth of the TIC market.

Market Opportunities

Tighter international environmental and safety requirements are driving significant development potential in the chemical industry's TIC (Testing, Inspection, and Certification) sector. The need for laboratory testing and certification services is growing as a result of stricter regulations pertaining to emissions control, hazardous material compliance, and product labeling. Lifecycle assessment, carbon footprint verification, and ESG audits are becoming more and more necessary as a result of the move toward sustainable and bio-based chemicals. The need for regulatory conformance assessments like REACH and GHS compliance is further fueled by an increase in cross-border trade. Furthermore, more effective, data-driven service models are being made possible by digital inspection technologies, remote auditing, and laboratory automation, which improve scalability and prospects for long-term market expansion.

Global TIC Market for Chemical Industry Report Coverage

|

Report Metric

|

Details

|

|

Historical Period

|

2020 - 2024

|

|

Base Year Considered

|

2025

|

|

Forecast Period

|

2026 - 2035

|

|

Market Size in 2025

|

U.S.D. 3.42 Billion

|

|

Revenue Forecast in 2035

|

U.S.D. 6.01 Billion

|

|

Growth Rate

|

5.8%

|

|

Segments Covered in the Report

|

Service Type, Sourcing Type, Chemical Type and Compliance Focus

|

|

Report Scope

|

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling

|

|

Regions Covered in the Report

|

North America, Europe, Asia Pacific

|

TIC Market for Chemical Industry Segmentation

By Service Type

Testing services are the major contributor to the total TIC demand in the chemical sector with a share of approximately 47–49% of the total revenue, the main factors being analytical testing, toxicology assessment, and material characterization. The share of inspection services is about 28–30%, mostly associated with plant audits, process safety checks, and transport inspections. Certification services represent the rest of the share, facilitated by regulatory approvals, safety documentation, and export compliance.

By Sourcing Type

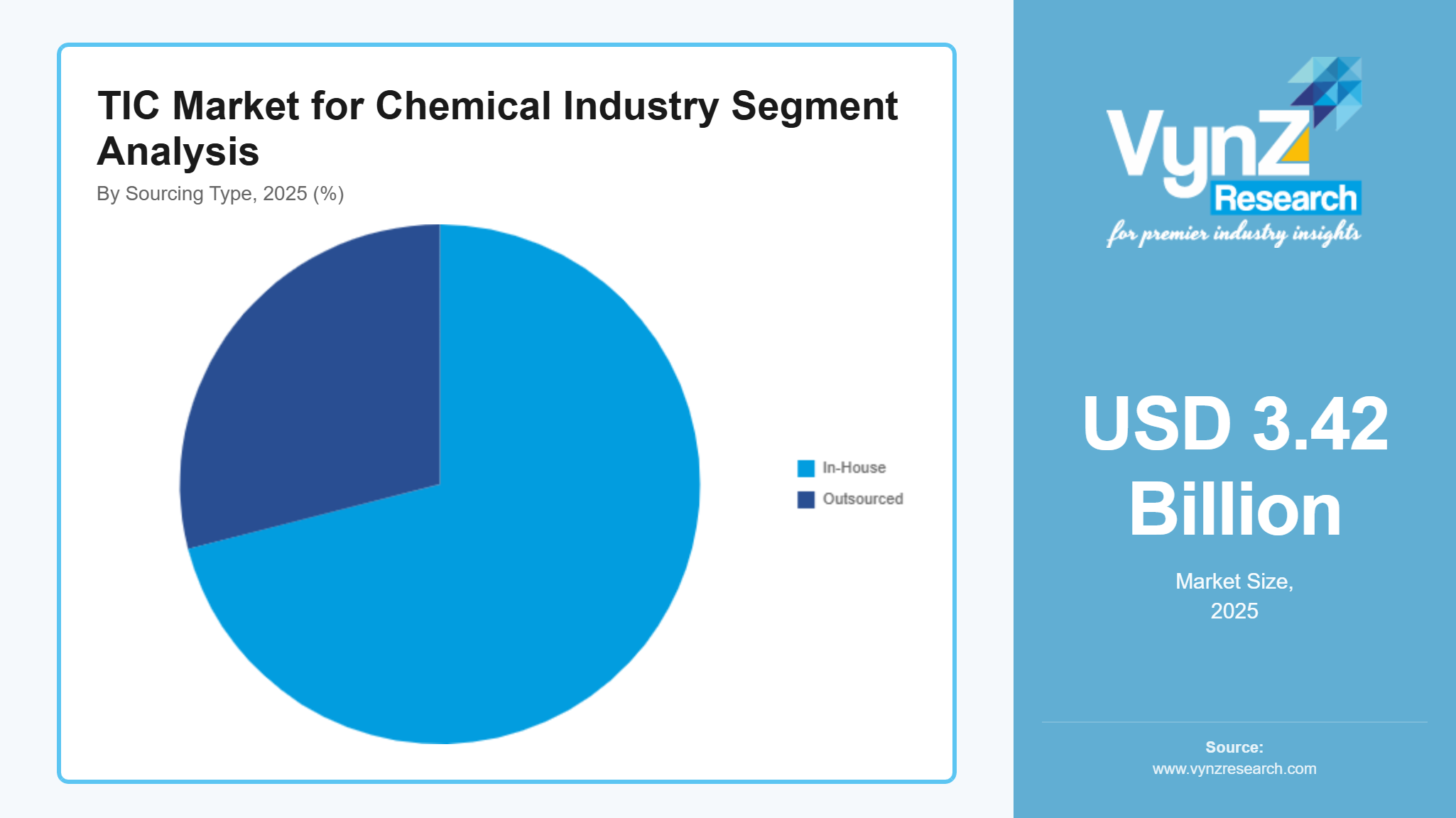

The major part of TIC services is externally sourced, and thus the demand for such services accounts for a 69–71% share. This is because most chemical producers prefer to use the services of accredited third-party laboratories for regulatory acceptance and cross-border recognition. The volume of outsourced services is currently growing at close to 7.4% CAGR. The in-house testing capacity which is mainly the case of large integrated chemical companies, constitutes a share of about 29–31% of the total demand and is developing more slowly at approximately 4.3%, with the primary focus on internal quality control.

By Chemical Type

Industrial and basic chemicals are the major contributors of TIC demand with a share close to 41% of total service volume due to their scale, hazard classification, and transport requirements. Specialty chemicals are the next largest contributors with a share of roughly 35%, the main factors being formulation complexity and customer-specific testing. The share of agrochemicals and other regulated compounds is the rest of the demand; however, they generate higher per-project TIC value due to the need for intensive safety and environmental assessment.

By Compliance Focus

Safety and hazard compliance is the largest area of TIC activities, representing about 43% of the total demand. The main activities are driven by toxicity testing, handling certification, and workplace safety audits. Environmental compliance is the next largest area with a share of around 34%, the most significant activities being emissions monitoring and waste verification. The remainder of the demand is for transport and labeling compliance. The environmental-related TIC services are expanding at a quicker pace, close to 8% per year, due to the increasing strictness of sustainability oversight.

Regional Insights

North America

North America continues to be a lucrative market for chemical TIC services, accounting for nearly 30–32% of the global demand. Most of the activities are going on in the United States, which is supported by the strict enforcement of environmental laws, safety regulations, and heavy requirements for documentation.

The main part of the demand for TIC is made by the recurring inspection and testing which are closely related to emissions control, workplace safety, and chemical transport. Regulatory audits and environmental compliance-related activities in the region are at the take-off phase and develop at the speed of approximately 6.5–6.8% yearly.

The growth is also supported by the increasing attention at the whole chemical supply chain to the issues of hazardous substances and sustainability disclosures.

Europe

Europe is responsible for about 25–27% of the global TIC demand in the chemical industry and is characterized by well-structured regulatory systems. The need to follow REACH, CLP, and environmental directives is the reason for a regular and continuous testing and certification activity.

The environmental and sustainability-related services are a significant and growing part of the TIC demand, especially in the cases of emissions monitoring and substance registration. These activities are progressing at a speed close to 7.5% yearly.

The ongoing reshapings of the regulations and changes in the classification of substances continue to be the main reasons for the long-term demand of independent TIC services across the region.

Asia Pacific

Asia Pacific is the most rapidly expanding regional market, and its growth rate is estimated to be between 8% and 9% CAGR. China, India, and Southeast Asia are not only leading the way in production volumes but also in capacity additions.

The quick industrialization along with the tightening of local regulations have made the demand for third-party testing and inspection providers quite high. Export-oriented chemical producers are the ones who most of all need internationally recognized certification to be able to enter regulated markets.

With the maturing of regulatory frameworks, TIC demand in the region is becoming less about basic inspection and more about structured, recurring compliance programs.

Competitive Landscape / Company Insights

The chemical TIC market is moderately concentrated with strong global competitors and numerous regional specialists competing on service breadth, technical expertise, and regulatory alignment. Leading players dominate through extensive geographic coverage, diversified service portfolios, technological investments, and strategic partnerships or acquisitions to enhance capacity in chemical-specific testing and certification services.

Mini Profiles

SGS S.A. is a global leader with one of the largest lab and inspection networks, offering comprehensive chemical testing, compliance verification, and sustainability services.

TUV SUD and TUV Rheinland are strong in technical inspection, safety validation, and regulatory compliance testing across industrial and chemical applications.

Intertek Group plc is a broad laboratory and inspection services supporting chemical product testing, supply-chain assurance, and sustainability auditing.

Bureau Veritas is an extensive regulatory and certification services across multiple industries including chemicals, with strong digital and risk-management capabilities.

Key Players

- Intertek Group Plc

- Bureau Veritas

- UL LLC

- SGS SA

- Eurofins USA

- TUV Rheinland

- TUV SUD

- MISTRAS Group

- ASTM

- Applus+

- DNV GL

Recent Developments

In January 2026, SPIN360, a Milan-based sustainability advice company that specializes in supply chain traceability, lifecycle analytics, and ESG reporting for high-end fashion and luxury companies, has agreed to be acquired by Bureau Veritas. As regulatory pressure on Scope 3 disclosures and circularity increases throughout Europe, the agreement supports the French testing and certification group's foray into consumer goods sustainability services.

In December 2025 - UL Solutions which is a global leader in applied safety science has signed a memorandum of understanding with Saudi Electricity Company to collaborate on advancing fire protection and life safety standards, reflecting a shared commitment to reduce fire risk and strengthening public safety.

In December 2025, Solar manufacturer JA Solar and TÜV Rheinland have collaborated on Joint validation of next-generation multi-cut cell technology. Under this agreement, JA Solar will provide product data, cell and module structures, manufacturing process details, and test samples to support TÜV Rheinland’s work on developing testing standards, conducting verification tests, advancing certification procedures, and performing quality assessments related to multi-segmentation technology.