- Home >

- Automotive & Transportation >

- Europe Electric Bus Market

Europe Electric Bus Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Propulsion Type (Battery Electric Bus (BEB), Plug-in Hybrid Electric Bus (PHEV), Fuel Cell Electric Bus (FCEV), Hybrid Electric Bus (HEV)), by Battery Type (Lithium Iron Phosphate (LFP), Lithium Nickel Manganese Cobalt (NMC), Other Lithium-ion Variants), by Bus Length (Less than 9 meters, to 14 meters, Above 14 meters), by Application (Intercity, Intracity / Urban Transit), by Charging Infrastructure (Depot Charging, Opportunity Charging, Pantograph Charging, Plug-in Charging), by Power Output (Up to 250 kW, kW to 400 kW, Above 400 kW), by Seating Capacity (Up to 40 seats, to 70 seats, Above 70 seats)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9661 | Industry : Automotive & Transportation | Available Format :

|

Page : 145 |

Europe Electric Bus Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Propulsion Type (Battery Electric Bus (BEB), Plug-in Hybrid Electric Bus (PHEV), Fuel Cell Electric Bus (FCEV), Hybrid Electric Bus (HEV)), by Battery Type (Lithium Iron Phosphate (LFP), Lithium Nickel Manganese Cobalt (NMC), Other Lithium-ion Variants), by Bus Length (Less than 9 meters, to 14 meters, Above 14 meters), by Application (Intercity, Intracity / Urban Transit), by Charging Infrastructure (Depot Charging, Opportunity Charging, Pantograph Charging, Plug-in Charging), by Power Output (Up to 250 kW, kW to 400 kW, Above 400 kW), by Seating Capacity (Up to 40 seats, to 70 seats, Above 70 seats)

Europe Electric Bus Market Overview

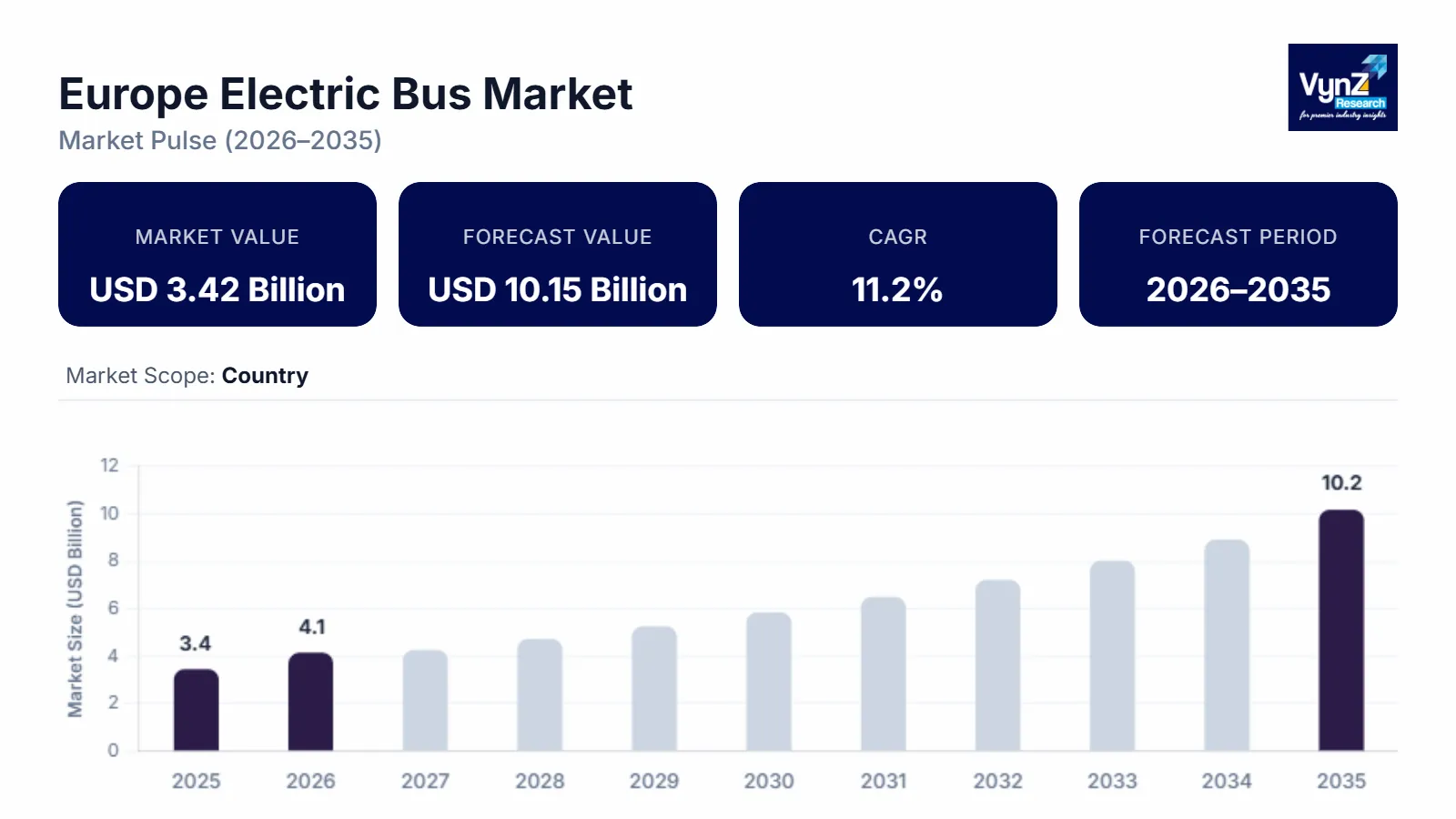

The Europe electric bus market which was valued at approximately USD 3.42 billion in 2025 and is estimated to reach around USD 4.12 billion by 2026, is projected to expand to approximately USD 10.15 billion by 2035, growing at a CAGR of about 11.2% during the forecast period from 2026 to 2035.

The Europe electric bus market shows permanent growth expansion because three factors operate together which include mandatory regional decarbonization requirements, ongoing battery price reductions, and broader zero emission public procurement standards. The European Commission Clean Vehicles Directive together with national climate neutrality laws, requires member states to establish their electrification timelines for fleet vehicles. International Energy Agency strategic assessments show that electric buses function as a vital component to help advanced economies achieve their transportation sector emission reduction goals.

Furthermore, the market expands because three elements drive its growth which includes urban air quality compliance programs, funding mechanisms for public transport electrification, and increasing municipal fleet replacement cycles at a time when battery electric propulsion technologies achieve wider adoption through charging network expansion. Demand from metropolitan transit authorities who want operational efficiency during their extended operational period continues to boost procurement volume. The European Environment Agency uses sustainability monitoring to direct investments towards zero emission mobility infrastructure, which enables Germany and the United Kingdom and France to create their infrastructure while maintaining market equilibrium until 2035.

Europe Electric Bus Market Dynamics

Market Trends

The market is going through fundamental changes because procurement methods, technology selection, and fleet upgrade methods now match the regional decarbonization objectives. The market also undergoes transformation because the industry now adopts battery electric buses which deliver superior energy efficiency and longer driving distances as operators seek to achieve lower operational costs while reducing emissions. The current trend shows that digital fleet management systems now connect with telematics platforms because the systems need both regulatory adherence and technological progress to function correctly. The International Energy Agency reports that organizations are now using connected charging infrastructure together with predictive maintenance solutions to enhance fleet reliability while decreasing their operational downtime.

The European Commission enforces public procurement rules which require greater percentages of zero-emission buses according to the Clean Vehicles Directive and Fit for 55 frameworks to establish designated timelines for implementing their adoption. The European Environment Agency has released data which shows that cities need to develop electric transport systems because these systems are essential for meeting carbon neutrality targets. So, cities invest in both depot charging systems and smart grid technology.

Growth Drivers

The market experiences its expansion because strict emission rules and urban air quality requirements create ongoing demand within city transportation systems. The market growth accelerates because funding for charging stations and renewable energy systems and sustainable transportation routes increases. The European Investment Bank together with national recovery programs provides financial support for zero emission fleet purchases and infrastructure development which creates sustainable deployment pathways.

The member states' climate neutrality commitments which they have embraced serve as a fundamental element for increasing adoption rates. Public transport authorities will maintain strong demand for battery electric buses throughout the forecasting period because they focus on cost reduction and environmental performance and compliance. The International Energy Agency strategic roadmaps show electrified public transport as the essential method to decrease urban pollution and reduce oil dependence which drives continuous investment in Germany and France and the United Kingdom.

Market Restraints / Challenges

The market has positive development prospects but the industry encounters specific obstacles which will restrict its market growth. The market faces budget allocation challenges because high upfront procurement costs and battery price fluctuations hinder market access for smaller municipalities and regions which are sensitive to pricing. The European Commission regulatory documents show total ownership costs have improved but capital costs still prevent transit authorities from obtaining funding unless they have established funding frameworks.

The operational difficulties which manufacturers and suppliers must manage stem from their reliance on battery cell imports together with essential raw material needs. The European Environment Agency assessment reports show that organizations must manage global supply chain disruptions together with resource concentration risks which create operational difficulties and increase project costs and extend delivery times. The rapid growth of fleet electrification will become unsustainable because infrastructure systems lack sufficient charging capacity and grid enhancement capabilities.

Market Opportunities

The market offers excellent opportunities because intercity and regional electric bus operations will grow through the development of advanced battery systems which can handle high capacity and fast charging capabilities. The public transport operators who intend to shift from hybrid systems to complete electric solutions should choose companies that supply modular platforms which deliver outstanding performance. The European Investment Bank-backed investment programs enable widespread use of depot charging and smart energy management systems which will reach larger areas.

The rising demand for digital-enabled mobility systems creates better chances to develop renewable energy charging networks which allow vehicle-to-grid connections to enhance grid stability while reducing operational costs. The International Energy Agency strategic outlooks predict that electrified public transport solutions which use renewable energy systems increase energy security while decreasing emissions. The regional electric mobility system will benefit from advancements in battery recycling and circular supply chains and intelligent fleet analytics which will enhance customer relationships and boost overall efficiency.

Europe Electric Bus Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

U.S.D. 3.42 Billion |

|

Revenue Forecast in 2035 |

U.S.D. 10.15 Billion |

|

Growth Rate |

11.2% |

|

Segments Covered in the Report |

Propulsion Type, Battery Type, Bus Length, Application, Charging Infrastructure |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, France, UK, Italy, Rest of Europe |

Europe Electric Bus Market Segmentation

By Propulsion Type

The market reached its peak in 2025 through battery electric buses which generated roughly 69% of total market revenue. The existing technology enables the European Union member states to meet their zero-emission procurement requirements while German and French and Nordic countries maintain their governmental funding support. The declining battery costs and total cost of ownership improvements led to a market expansion of 15% in 2025 which supported the electrification of urban public transportation systems.

The fastest market growth among bus types will occur through fuel cell electric buses which will achieve a compound annual growth rate of 18.4% between 2026 and 2035. The development of hydrogen mobility frameworks and international hydrogen corridor construction projects provide essential support for expansion efforts. The emerging market for plug-in hybrid electric buses will expand at a rate of 9.2% because municipalities between infrastructure readiness and their planned electrification schedule adopt this technology.

By Battery Type

The market distribution in 2025 showed lithium iron phosphate batteries as the leading technology which achieved a market share of almost 58%. The public fleets experience cost-efficient benefits from their thermal stability and extended product lifespan which provides reliable service across high-demand periods. The municipal adoption of this technology increased by 13% in 2025 because they chose battery systems which fulfilled safety standards and environmental requirements of European sustainability frameworks.

The market demand for lithium nickel manganese cobalt batteries will increase through the forecast period which will see a market expansion of 17.5% between 2026 and 2035. The product evolution creates demand for higher energy systems which extend range performance on long-distance routes. The market for other lithium-ion battery types will increase by 10.4% through battery chemistry improvements and battery recycling projects.

By Bus Length

The 9 to 14 meters bus category accounted for the largest share in 2025, contributing approximately 62% of overall market revenue. The current segment offers maximum passenger space which enables bus operations to run on different routes while using standardized depot charging systems. The annual production of this category increased by 14 percent because Western European cities implemented organized programs to refresh their urban vehicle fleets.

The forecast period will show the fastest growth for buses which exceed 14 meters with a projected compound annual growth rate of 16.8%. The current period sees bus rapid transit corridors in metropolitan areas that have high population density extending their use of articulated buses to make more public transit available. The electrification of suburban and feeder services will drive a market expansion of 11.3% for the smaller-length bus segment.

By Charging Infrastructure

The depot charging sector achieved market leadership in 2025 through its 64% share of total charging systems installed. The solution enables public transit authorities to achieve operational efficiency through centralized energy management which helps them reduce their capital expenses. The municipal electrification targets led to a 14% increase in annual depot charger installations for 2025.

The most rapid market growth will occur through opportunity charging systems which will reach a compound annual growth rate of 17.2% between 2026 and 2035. The demand for high-frequency routes requires operators to use smaller batteries which results in increased operational time for the system. Pantograph systems are becoming popular in key urban corridors because they help sustain ongoing infrastructure upgrades.

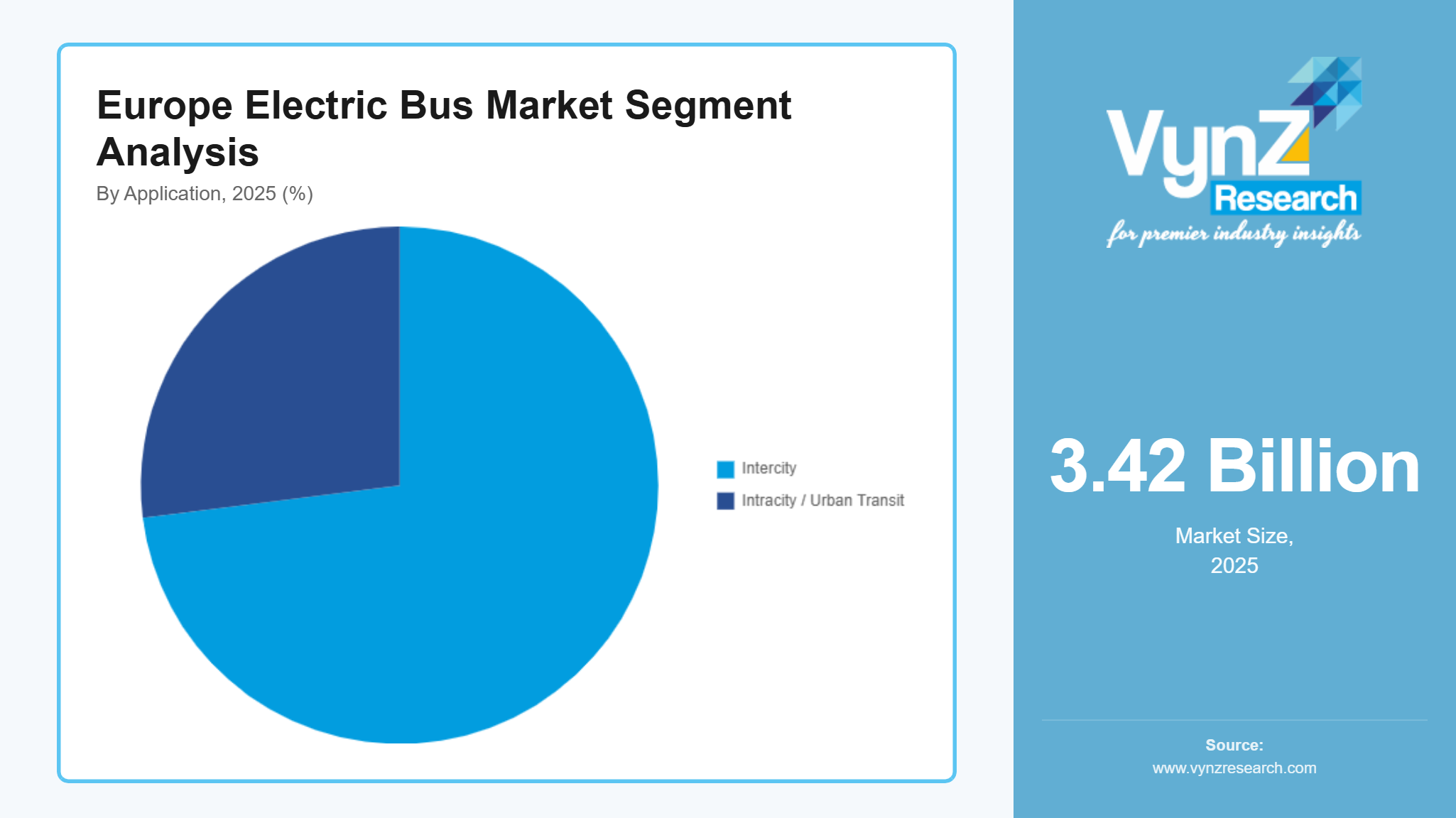

By Application

The largest revenue share for the market in 2025 came from intracity and urban transit applications which generated 73% of total earnings. The current technology enables urban centers to impose strict emission regulations while their congestion control measures allocate public funds for sustainable transportation solutions. Urban electric bus deployment expanded by nearly 16% in 2025, reflecting accelerated replacement of diesel fleets in capital cities.

Intercity applications will experience the highest growth rate in the forecast period with a market development estimate of 17.1% annual growth between 2026 and 2035. The current market growth stems from improved battery capabilities which enable longer distance travel and national projects that develop zero-emission corridors which connect the country. The regional charging network expansion complete supports increased use of charging stations across both city routes and rural travel paths.

Regional Insights

Germany

In 2025, Germany held approximately 24% of the market because the central government backed funding programs and cities like Berlin, Hamburg, and Munich implemented extensive fleet electrification projects. The Federal Ministry for Digital and Transport has allocated substantial subsidies under national climate action targets which align with the European Green Deal. The structured procurement mandates together with low-emission transport regulations led to an 18% rise in electric bus registrations throughout Germany during 2025. The adoption of electric buses is being accelerated through governmental grants which fund both vehicle purchases and depot infrastructure development. The dual incorporation of hydrogen pilot projects under Germany's National Hydrogen Strategy together with public-private battery manufacturing partnerships establishes enduring stability for the market.

United Kingdom

The United Kingdom represented approximately 17% of the market in 2025. This was due to the Zero Emission Bus Regional Areas (ZEBRA) program and national net-zero transport commitments. Major cities including London, Manchester, and Birmingham continue expanding zero-emission fleets. The Department for Transport provided funding support which enabled electric bus adoption to grow by about 15% during 2025. The combination of government-backed financing mechanisms and local authority partnerships is improving the deployment of charging infrastructure. The domestic manufacturing support together with regulatory decarbonization mandates is driving the transition from diesel fleets to battery-electric platforms at an accelerated pace.

France

France accounted for nearly 19% of the regional market in 2025. The market growth occurred because of energy transition policies and sustainable mobility investment frameworks. The cities of Paris, Lyon, and Marseille are implementing public transport electrification projects to achieve national emission reduction goals. The Ministry for the Ecological Transition supervised grants and infrastructure programs which led to an approximate 16% increase in electric bus fleet expansion throughout the year. The combination of public funding for depot electrification and hydrogen mobility pilot programs enables organizations to create procurement pathways and develop sustained electrification plans for the future.

Rest of Europe

The Rest of Europe occupied approximately 18% of the market in 2025. The market included countries which were Italy, Spain, the Netherlands, Sweden and Poland. The European Union decarbonization mandates together with European Commission financing programs enable these markets to achieve their growth targets. The countries experienced a 14% increase in electric bus registrations during 2025. This growth resulted from expanding urban sustainability initiatives and structured fleet replacement cycles. The national recovery and resilience plans along with European Investment Bank funding are helping to expand charging infrastructure and acquire new vehicles.

The combined market share of Germany, the United Kingdom, France, and Rest of Europe in 2025 reached approximately 78%. The remaining market share is distributed among smaller emerging European markets to maintain total proportional alignment within the regional framework.

Competitive Landscape / Company Insights

The electric bus market in Europe experiences a competitive environment which ranges from moderate competition to intense market battles as both international and domestic manufacturers concentrate on developing new technologies and implementing their pricing methods and expanding their bus fleets. The main industry players are making investments in battery research and development together with charging station infrastructure and digital fleet control technologies to achieve better operational performance. Government initiatives such as the national electrification incentives in Germany and the Zero Emission Bus Regional Areas (ZEBRA) program in the UK and the sustainable urban mobility grants in France serve as strong drivers for technology adoption. These initiatives drive businesses to enhance their market reach while expanding their production capabilities and developing better customer support systems throughout Europe.

Mini Profiles

AB Volvo focuses on electric bus manufacturing and sustainable transport solutions, supported by global distribution networks, strong brand recognition, and cost‑efficient production strategies that strengthen presence in Europe and international markets.

BYD Company Limited operates in mass and premium electric bus segments, emphasizing battery technology, performance, and customization, supported by strategic partnerships, localized assembly, and extensive after‑sales service networks.

Daimler AG focuses on innovative commercial vehicle design and advanced propulsion technologies, supported by high‑performance engineering, global service infrastructure, and integration of digital fleet management solutions.

Ebusco N.V. operates in premium electric bus solutions, emphasizing lightweight design, energy efficiency, and digital fleet integration, supported by international R&D collaborations and sustainable urban mobility initiatives.

Iveco S.p.A. leverages local manufacturing and strategic partnerships to expand market presence, delivering electric bus solutions with modular design, energyoptimized performance, and regional service networks across Europe.

Key Players

- AB Volvo

- Alexander Dennis Limited

- BYD Company Limited

- Daimler AG

- Ebusco N.V.

- Iveco S.p.A.

- Karsan Otomotiv Sanayi ve Ticaret A.S.

- MAN Truck & Bus SE

- Yutong Group Co., Ltd.

Recent Developments

In January2026, A comprehensive agreement has been reached between MAN Truck & Bus and employee representatives about the implementation of "MAN2030+," a program designed to improve competitiveness and secure the future of its locations. Over one billion euros will have been invested in MAN Truck & Bus SE's German locations by the end of 2030. In the future, Eastern Europe will also make the substantial additional investments required for the next generation of automobiles based on the TRATON Modular System (TMS).

In August 2026, Daimler India Commercial Vehicles has introduced New BharatBenz heavy-duty truck models that better meet the specific needs of customers in India's growing mining and construction industries. The BharatBenz HX series includes the 2828C HX and 3532C HX models, which are intended for use in the construction industry and are available in two powerful and efficient versions. All of the BharatBenz HX series trucks have an innovative driver state monitoring system, a wind deflector for better aerodynamics, unitized front axle bearings for less maintenance, and Hill Hold Assist.

In July 2025, by purchasing NOVO R&D, Volvo Group has made an investment in the green transformation process. Due to the acquisition, Gothenburg and Sweden will continue to have this superior expertise, enhancing the area's ability to compete in clean technology. The organization has a fantastic chance to improve its proficiency in the fields of material research and battery cell chemistry. The company's plan to become 100% fossil fuel-free by 2040 will be a great advantage. Through the acquisition, Volvo Group gains control of the battery cell chemistry and material development team and facilities, assisting Volvo Group in its transition to more environmentally friendly transportation options.

Table of Contents for Europe Electric Bus Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Propulsion Type

1.2.2. By

Battery Type

1.2.3. By

Bus Length

1.2.4. By

Application

1.2.5. By

Charging Infrastructure

1.2.6. By

Power Output

1.2.7. By

Seating Capacity

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Propulsion Type

5.1.1. Battery Electric Bus (BEB)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Plug-in Hybrid Electric Bus (PHEV)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Fuel Cell Electric Bus (FCEV)

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Hybrid Electric Bus (HEV)

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Battery Type

5.2.1. Lithium Iron Phosphate (LFP)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Lithium Nickel Manganese Cobalt (NMC)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Other Lithium-ion Variants

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Bus Length

5.3.1. Less than 9 meters

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. to 14 meters

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Above 14 meters

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Intercity

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Intracity / Urban Transit

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By Charging Infrastructure

5.5.1. Depot Charging

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Opportunity Charging

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Pantograph Charging

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Plug-in Charging

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.6. By Power Output

5.6.1. Up to 250 kW

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. kW to 400 kW

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Above 400 kW

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.7. By Seating Capacity

5.7.1. Up to 40 seats

5.7.1.1. Market Definition

5.7.1.2. Market Estimation and Forecast to 2035

5.7.2. to 70 seats

5.7.2.1. Market Definition

5.7.2.2. Market Estimation and Forecast to 2035

5.7.3. Above 70 seats

5.7.3.1. Market Definition

5.7.3.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Propulsion Type

6.2. By

Battery Type

6.3. By

Bus Length

6.4. By

Application

6.5. By

Charging Infrastructure

6.6. By

Power Output

6.7. By

Seating Capacity

7. France Market Estimate and Forecast

7.1. By

Propulsion Type

7.2. By

Battery Type

7.3. By

Bus Length

7.4. By

Application

7.5. By

Charging Infrastructure

7.6. By

Power Output

7.7. By

Seating Capacity

8. UK Market Estimate and Forecast

8.1. By

Propulsion Type

8.2. By

Battery Type

8.3. By

Bus Length

8.4. By

Application

8.5. By

Charging Infrastructure

8.6. By

Power Output

8.7. By

Seating Capacity

9. Italy Market Estimate and Forecast

9.1. By

Propulsion Type

9.2. By

Battery Type

9.3. By

Bus Length

9.4. By

Application

9.5. By

Charging Infrastructure

9.6. By

Power Output

9.7. By

Seating Capacity

10. Rest of Europe Market Estimate and Forecast

10.1. By

Propulsion Type

10.2. By

Battery Type

10.3. By

Bus Length

10.4. By

Application

10.5. By

Charging Infrastructure

10.6. By

Power Output

10.7. By

Seating Capacity

11. Company Profiles

11.1.

AB Volvo

11.1.1.

Snapshot

11.1.2.

Overview

11.1.3.

Offerings

11.1.4.

Financial

Insight

11.1.5.

Recent

Developments

11.2.

Alexander Dennis Limited

11.2.1.

Snapshot

11.2.2.

Overview

11.2.3.

Offerings

11.2.4.

Financial

Insight

11.2.5.

Recent

Developments

11.3.

BYD Company Limited

11.3.1.

Snapshot

11.3.2.

Overview

11.3.3.

Offerings

11.3.4.

Financial

Insight

11.3.5.

Recent

Developments

11.4.

Daimler AG

11.4.1.

Snapshot

11.4.2.

Overview

11.4.3.

Offerings

11.4.4.

Financial

Insight

11.4.5.

Recent

Developments

11.5.

Ebusco N.V.

11.5.1.

Snapshot

11.5.2.

Overview

11.5.3.

Offerings

11.5.4.

Financial

Insight

11.5.5.

Recent

Developments

11.6.

Iveco S.p.A.

11.6.1.

Snapshot

11.6.2.

Overview

11.6.3.

Offerings

11.6.4.

Financial

Insight

11.6.5.

Recent

Developments

11.7.

Karsan Otomotiv Sanayi ve Ticaret A.S.

11.7.1.

Snapshot

11.7.2.

Overview

11.7.3.

Offerings

11.7.4.

Financial

Insight

11.7.5.

Recent

Developments

11.8.

MAN Truck & Bus SE

11.8.1.

Snapshot

11.8.2.

Overview

11.8.3.

Offerings

11.8.4.

Financial

Insight

11.8.5.

Recent

Developments

11.9.

Yutong Group Co., Ltd.

11.9.1.

Snapshot

11.9.2.

Overview

11.9.3.

Offerings

11.9.4.

Financial

Insight

11.9.5.

Recent

Developments

12. Appendix

12.1. Exchange Rates

12.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Europe Electric Bus Market Coverage

Propulsion Type Insight and Forecast 2026 - 2035

- Battery Electric Bus (BEB)

- Plug-in Hybrid Electric Bus (PHEV)

- Fuel Cell Electric Bus (FCEV)

- Hybrid Electric Bus (HEV)

Battery Type Insight and Forecast 2026 - 2035

- Lithium Iron Phosphate (LFP)

- Lithium Nickel Manganese Cobalt (NMC)

- Other Lithium-ion Variants

Bus Length Insight and Forecast 2026 - 2035

- Less than 9 meters

- to 14 meters

- Above 14 meters

Application Insight and Forecast 2026 - 2035

- Intercity

- Intracity / Urban Transit

Charging Infrastructure Insight and Forecast 2026 - 2035

- Depot Charging

- Opportunity Charging

- Pantograph Charging

- Plug-in Charging

Power Output Insight and Forecast 2026 - 2035

- Up to 250 kW

- kW to 400 kW

- Above 400 kW

Seating Capacity Insight and Forecast 2026 - 2035

- Up to 40 seats

- to 70 seats

- Above 70 seats

Europe Electric Bus Market by Region

- Germany

- By Propulsion Type

- By Battery Type

- By Bus Length

- By Application

- By Charging Infrastructure

- By Power Output

- By Seating Capacity

- U.K.

- By Propulsion Type

- By Battery Type

- By Bus Length

- By Application

- By Charging Infrastructure

- By Power Output

- By Seating Capacity

- France

- By Propulsion Type

- By Battery Type

- By Bus Length

- By Application

- By Charging Infrastructure

- By Power Output

- By Seating Capacity

- Italy

- By Propulsion Type

- By Battery Type

- By Bus Length

- By Application

- By Charging Infrastructure

- By Power Output

- By Seating Capacity

- Spain

- By Propulsion Type

- By Battery Type

- By Bus Length

- By Application

- By Charging Infrastructure

- By Power Output

- By Seating Capacity

- Russia

- By Propulsion Type

- By Battery Type

- By Bus Length

- By Application

- By Charging Infrastructure

- By Power Output

- By Seating Capacity

- Rest of Europe

- By Propulsion Type

- By Battery Type

- By Bus Length

- By Application

- By Charging Infrastructure

- By Power Output

- By Seating Capacity

Vynz Research know in your business needs, you required specific answers pertaining to the market, Hence, our experts and analyst can provide you the customized research support on your specific needs.

After the purchase of current report, you can claim certain degree of free customization within the scope of the research.

Please let us know, how we can serve you better with your specific requirements to your research needs. Vynz research promises for quick reversal for your current business requirements.

- AB Volvo

- Alexander Dennis Limited

- BYD Company Limited

- Daimler AG

- Ebusco N.V.

- Iveco S.p.A.

- Karsan Otomotiv Sanayi ve Ticaret A.S.

- MAN Truck & Bus SE

- Yutong Group Co., Ltd.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: 1 888 253 3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com