Data Center Cooling Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Cooling Type (Air-Based Cooling, Liquid-Based Cooling), by Component (Solutions, Services), by Technology (Free Cooling, Evaporative Cooling, Adiabatic Cooling, Mechanical Refrigeration Cooling, Hybrid Cooling Systems, AI-Enabled Smart Cooling), by Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers), by Industry Vertical (IT & Telecommunications, BFSI, Healthcare, Government & Defense, Retail & E-commerce, Manufacturing, Others)

| Status : Published | Published On : Feb, 2026 | Report Code : VRICT5218 | Industry : ICT & Media | Available Format :

|

Page : 186 |

Data Center Cooling Market Overview

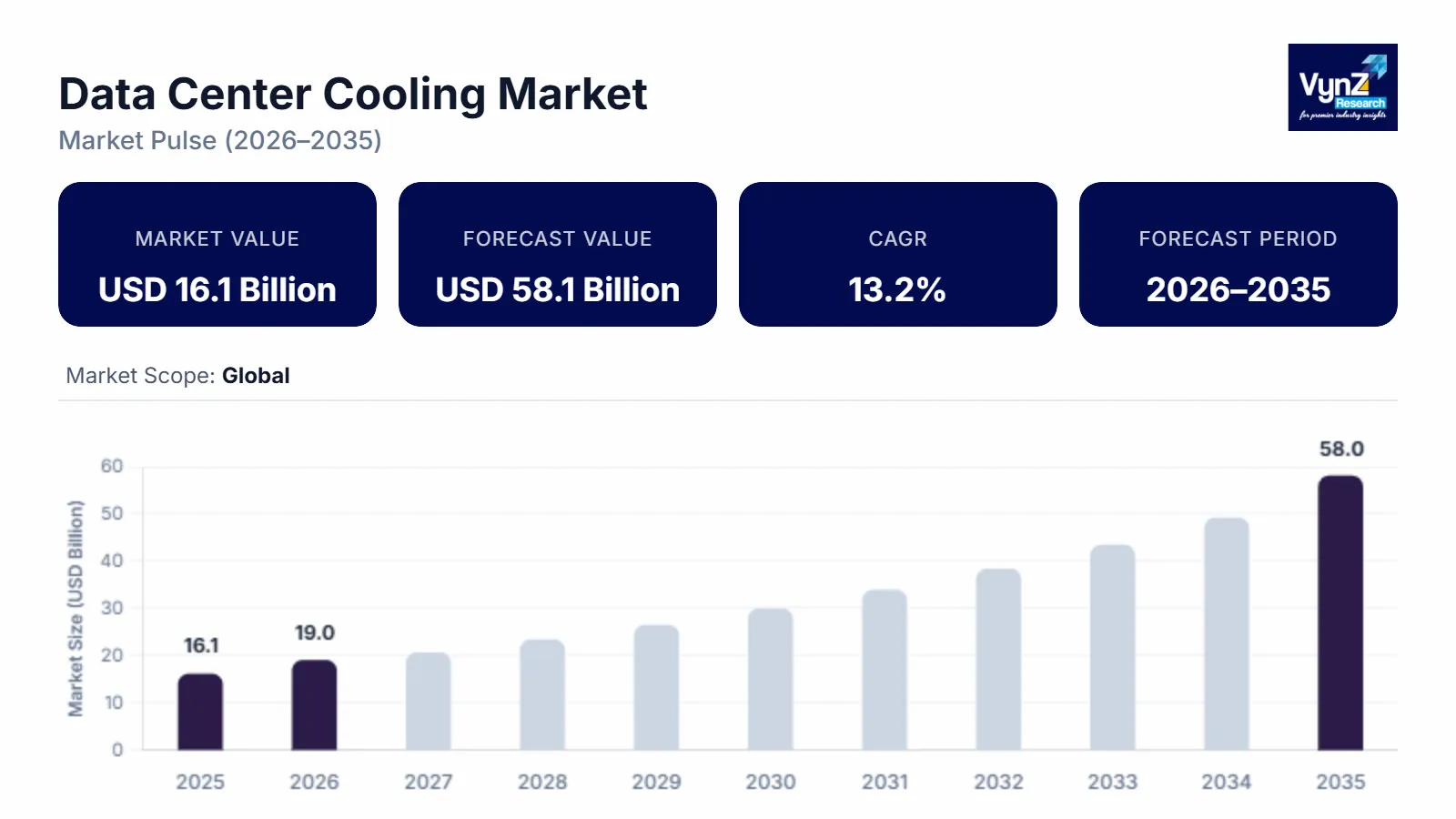

The data center cooling market which was valued at approximately USD 16.1 billion in 2025 and is estimated to reach around USD 19.0 billion in 2026, is projected to reach close to USD 58.1 billion by 2035, expanding at a CAGR of about 13.2% during the forecast period from 2026 to 2035.

This market is primarily driven by the exponential growth in global data generation and cloud computing adoption, which has significantly increased the number and scale of hyperscale and colocation facilities worldwide. Rapid expansion of artificial intelligence (AI), machine learning workloads, and high-performance computing has intensified rack densities, generating greater heat loads that require advanced and energy-efficient cooling solutions.

Moreover, stringent government regulations on energy efficiency and carbon emissions are pushing operators to adopt sustainable cooling systems that reduce Power Usage Effectiveness (PUE). Growing investments in edge computing infrastructure further contribute to the need for compact and efficient thermal management solutions. Increasing electricity costs globally are also encouraging operators to shift toward energy-optimized cooling architectures. Moreover, advancements in smart monitoring, IoT-enabled cooling controls, and AI-driven thermal optimization are enhancing operational efficiency, further propelling market growth.

Market Dynamics

Market Trends

The adoption of liquid cooling technologies is accelerating as modern data centers handle increasingly power-dense workloads driven by AI, machine learning, and high-performance computing. Traditional air-cooling systems are becoming less efficient in managing the extreme heat generated by advanced processors and GPUs, prompting operators to shift toward liquid-based solutions. Direct-to-chip cooling, which delivers coolant directly to heat-generating components, significantly improves thermal transfer efficiency and reduces energy consumption. Immersion cooling, where servers are submerged in dielectric fluid, further enhances cooling performance while lowering space and infrastructure requirements. The U.S. Department of Energy announced a $40 million funding initiative under which 15 projects will develop high-performance, energy-efficient cooling systems for data centers, aiming to reduce cooling energy use and associated carbon emissions a move that accelerates innovation in next-generation cooling technologies including liquid-based solutions. These systems help improve Power Usage Effectiveness (PUE) and support sustainability goals by reducing electricity usage. Liquid cooling also enables higher rack densities, allowing data centers to maximize computational capacity within limited footprints.

Growth Drivers

The rapid expansion of hyperscale data centers is a major growth driver for the data center cooling market, as large-scale facilities require highly efficient and scalable thermal management systems. Cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud are continuously investing in massive data center campuses to meet growing demand for cloud computing, AI processing, and digital services. These hyperscale facilities operate with extremely high rack densities and power loads, generating substantial heat that must be effectively managed to ensure performance and uptime. Advanced cooling solutions, including liquid cooling, containment systems, and modular cooling units, are increasingly deployed to maintain optimal operating temperatures. The Department of Science and Technology, Government of Gujarat formally signed the Memorandum of Understanding (MoU) with L&T Vyoma to explore the development of a 250 MW green AI-ready hyperscale data centre campus at the Dholera Special Investment Region (SIR). This agreement was finalised during the India AI Impact Summit 2026 and outlines a proposed ₹25,000 crore investment for the project, which is expected to support sustainable digital infrastructure growth in Gujarat. Hyperscale operators prioritize energy efficiency, there is strong demand for cooling technologies that improve Power Usage Effectiveness (PUE). The scale of these projects also requires flexible and expandable cooling architectures to support phased capacity growth.

Market Restraints / Challenges

High energy consumption and operating costs represent a significant challenge for the data center cooling market, as cooling systems account for a substantial share of total facility power usage. In many conventional data centers, cooling can consume 30–40% of overall electricity, directly impacting operational expenditure. As rack densities increase due to AI and high-performance computing workloads, thermal loads rise sharply, requiring more powerful and energy-intensive cooling equipment. Fluctuating global electricity prices further increase financial pressure on operators, particularly in regions with limited energy subsidies. Additionally, continuous 24/7 operations mean that cooling systems must run uninterrupted, leading to higher maintenance and lifecycle costs. The need to maintain optimal temperatures to prevent server overheating also limits opportunities for reducing cooling intensity.

Market Opportunities

The rapid expansion of edge data centers is creating significant growth opportunities in the data center cooling market, as organizations deploy smaller, decentralized facilities closer to end users. The rise of 5G networks, IoT devices, autonomous systems, and real-time analytics applications requires low-latency data processing, which edge infrastructure is designed to support. Unlike hyperscale facilities, edge data centers are often located in space-constrained or remote environments, increasing the need for compact, modular, and energy-efficient cooling systems. These facilities typically operate with limited on-site maintenance, driving demand for reliable and low-maintenance thermal management solutions. Advanced cooling technologies such as in-row cooling, liquid cooling, and self-contained precision air systems are increasingly adopted in edge deployments. Additionally, scalability is critical, as edge infrastructure must expand quickly to meet rising local data demand.

Global Data Center Cooling Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 16.1 Billion |

|

Revenue Forecast in 2035 |

USD 58.1 Billion |

|

Growth Rate |

13.2% |

|

Segments Covered in the Report |

Cooling Type, Component, Technology, Data Center Type, Industry Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Vertiv Group Corp. (U.S.), Schneider Electric SE (France), Daikin Industries, Ltd. (Japan), Johnson Controls International plc (Ireland), STULZ GmbH (Germany), Munters Group AB (Sweden), Rittal GmbH & Co. KG (Germany), Alfa Laval AB (Sweden), Asetek A/S (Denmark), CoolIT Systems Inc. (Canada), Airedale International Air Conditioning Ltd (United Kingdom), Submer Technologies SL (Spain) |

|

Customization |

Available upon request |

Market Segmentation

By Cooling Type

Air-Based Cooling is the largest category with a market share of about 65% in 2025, due to its widespread adoption across enterprise, colocation, and legacy data centers, being cost-effective, and having an established global installation base. Traditional air-based systems such as CRAC and CRAH units are deeply integrated into existing infrastructure, making them the preferred choice for retrofits and medium-density facilities. These systems are easier to deploy, maintain, and scale in conventional environments. Additionally, operators are familiar with airflow management practices like hot and cold aisle containment, which enhances efficiency. The strong installed base and lower upfront costs continue to support the dominance of this category.

There Air-Based Cooling further classified into followings

- Air-Based Cooling

- Computer Room Air Conditioners (CRAC)

- Computer Room Air Handlers (CRAH)

- In-Row Cooling

- Hot/Cold Aisle Containment

Liquid-Based Cooling is the fastest-growing category with a CAGR of 13.6% during the forecast period, due to increasing rack densities driven by AI, high-performance computing, and GPU-intensive workloads. Liquid cooling technologies such as direct-to-chip and immersion cooling provide superior heat dissipation compared to air systems. As hyperscale facilities push beyond traditional thermal thresholds, liquid cooling becomes essential for maintaining operational stability. These solutions improve energy efficiency and reduce power usage effectiveness (PUE). Growing investments in AI data centers and sustainability goals are accelerating the transition toward liquid-based systems.

There Liquid-Based Cooling further classified into followings

- Direct-to-Chip Cooling

- Immersion Cooling

- Rear Door Heat Exchangers

By Application

Solutions is the largest category with a market share of about 70% in 2025, due to high capital expenditure on chillers, cooling towers, air handling units, and economizers that form the core infrastructure of data center cooling. These hardware components represent significant upfront investment and are essential for maintaining optimal thermal conditions. Every new data center build requires large-scale cooling equipment, which drives revenue concentration in this segment. Additionally, hyperscale expansion projects further amplify demand for large-capacity mechanical systems. The scale and cost intensity of cooling infrastructure ensure this segment’s leadership.

There are solutions further classified into followings

- Chillers

- Cooling Towers

- Economizers

- Air Conditioning Units

Services is the fastest-growing category during the forecast period, due to increasing demand for maintenance, consulting, and optimization services. As data centers operate 24/7, ensuring reliability and uptime requires ongoing monitoring and predictive maintenance. Operators are increasingly outsourcing thermal optimization and energy-efficiency upgrades to specialized providers. The rise of AI-enabled monitoring tools also supports service-based recurring revenue models. Growing complexity of cooling environments is accelerating demand for lifecycle management services.

There Services further classified into followings

- Installation & Deployment

- Maintenance & Support

- Consulting Services

By Technology

Mechanical Refrigeration Cooling is the largest category with a market share of about 40% in 2025, due to its reliability, consistent performance across climates, and long-standing deployment in large-scale facilities. Mechanical chillers and compressor-based systems provide precise temperature control regardless of external environmental conditions. They are widely installed in hyperscale and colocation data centers where uptime is critical. Despite energy concerns, these systems remain essential in regions where free cooling is not feasible year-round. Their proven performance and global adoption support their dominant position.

AI-Enabled Smart Cooling is the fastest-growing category with a CAGR of 13.8% during the forecast period, due to increasing integration of artificial intelligence and IoT in thermal management systems. AI-driven optimization helps reduce energy consumption, predict cooling demand, and dynamically adjust airflow. These technologies enable real-time monitoring and automated efficiency improvements, lowering operational costs. As sustainability targets become stricter, smart cooling solutions are gaining rapid traction. Continuous innovation in digital infrastructure further strengthens growth prospects.

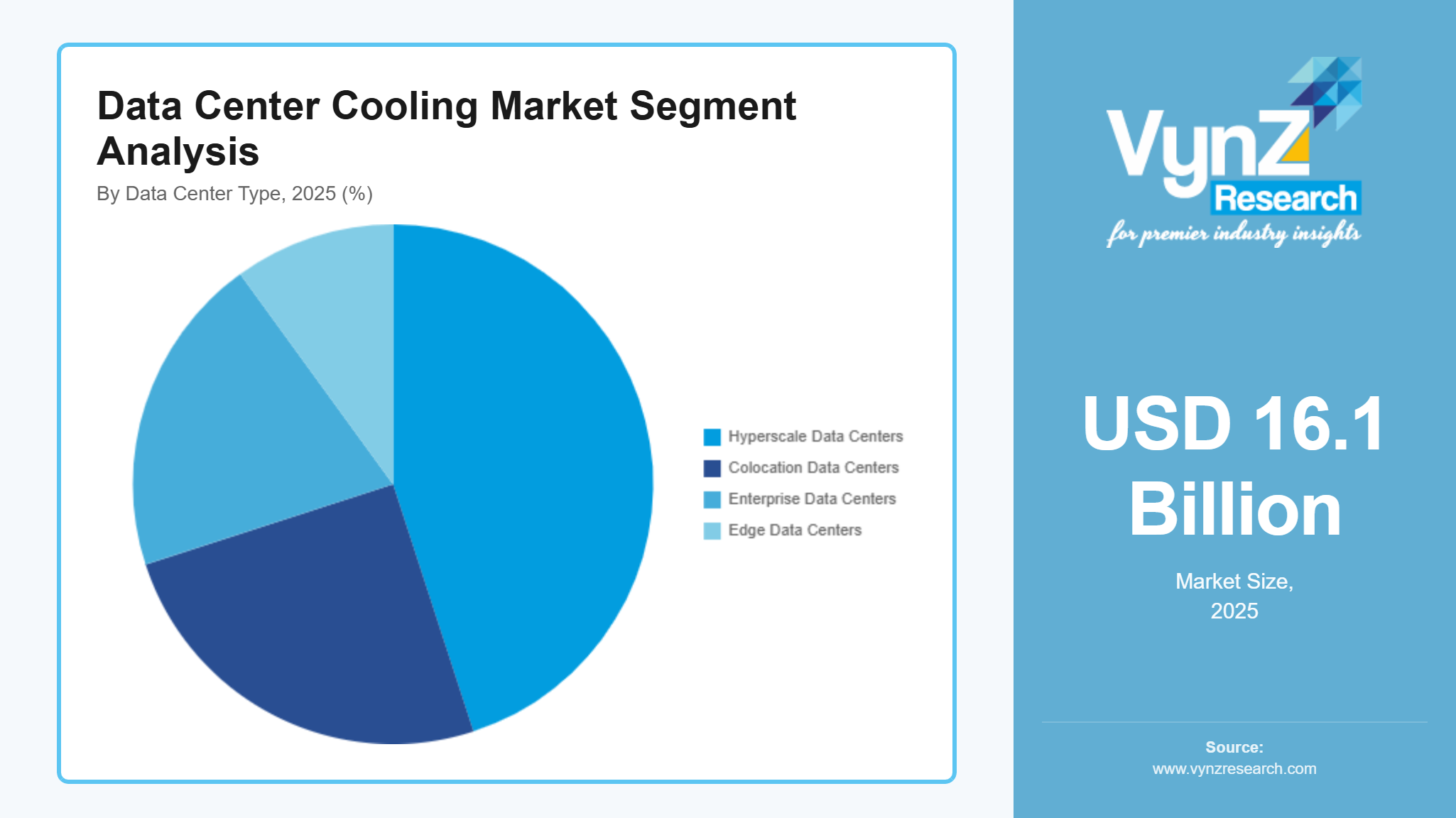

By Data Center Type

Hyperscale Data Centers is the largest category with a market share of about 45% in 2025, due to massive investments by global cloud providers and the growing demand for large-scale digital infrastructure. Hyperscale facilities operate with extremely high server density and power capacity, requiring advanced cooling systems. These projects involve substantial infrastructure spending, driving high revenue concentration. The expansion of cloud services, AI computing, and enterprise digital transformation supports their leadership. Their scale and continuous expansion maintain their dominance in the market.

Edge Data Centers is the fastest-growing category with a CAGR of 13.3% during the forecast period, due to the rapid rollout of 5G networks, IoT ecosystems, and low-latency applications. Edge facilities require compact, modular, and energy-efficient cooling systems suited for distributed deployment. Increasing demand for real-time data processing in remote locations is accelerating their development. These centers are often installed in urban or constrained environments, driving innovation in localized cooling technologies. The decentralization of computing infrastructure continues to boost this segment’s growth.

By Industry Vertical

IT & Telecommunications is the largest category with a market share of about 40% in 2025, due to continuous expansion of cloud computing, data traffic, streaming platforms, and enterprise digital services. Telecom operators and cloud service providers operate extensive data center networks that require robust cooling systems. The growth of internet penetration and mobile connectivity further supports infrastructure expansion. Large-scale investments in hyperscale and colocation facilities keep this segment dominant. The sector’s dependence on uninterrupted digital services drives consistent cooling demand.

Healthcare is the fastest-growing category with a CAGR of 13.5% during the forecast period, due to increasing adoption of electronic health records, telemedicine, AI diagnostics, and medical data storage. Healthcare institutions are investing in secure and reliable data center infrastructure to manage sensitive patient information. Rising digitization in hospitals and research institutions is accelerating cooling system deployment. Regulatory compliance and uptime requirements further necessitate advanced thermal management solutions. These factors collectively drive rapid growth in this vertical.

Regional Insights

Asia Pacific

Asia Pacific is the fastest-growing region in the data center cooling market, driven by rapid digital transformation, expanding cloud infrastructure, and strong government support for digital economies. India’s data center sector is attracting significant investment growth projected ~US $4.6 billion annually by 2025 under national frameworks supporting digital infrastructure, which indirectly supports the adoption of advanced cooling solutions including liquid cooling as part of overall data center build-outs. Countries such as China, India, Japan, Singapore, and South Korea are witnessing aggressive hyperscale and colocation data center expansion. China continues to invest heavily in western-region mega data center clusters to optimize energy efficiency, while India’s data center capacity is projected to more than double by the end of the decade due to rising internet penetration and 5G rollout. Governments across the region are introducing sustainability mandates and energy-efficiency standards, encouraging the adoption of advanced cooling technologies including liquid and free cooling systems. Singapore, despite land constraints, remains a key hub for high-efficiency cooling innovation. Growing AI workloads, smart city initiatives, and cloud adoption are accelerating demand for scalable and energy-efficient cooling infrastructure across the Asia Pacific.

Europe

Europe’s data center cooling market is strongly influenced by strict environmental regulations and ambitious climate neutrality targets. The European Union’s sustainability frameworks and energy-efficiency directives are pushing operators to adopt green cooling technologies such as free cooling and adiabatic systems. Countries including Germany, the Netherlands, Ireland, France, and the Nordic nations serve as major data center hubs due to strong connectivity and renewable energy integration. The Nordic region, in particular, benefits from naturally cold climates that enable efficient air-side cooling solutions. Increasing investments in hyperscale and colocation facilities, combined with sustainability-driven innovation, are strengthening Europe’s role as a key region in the global cooling landscape. Continuous modernization of legacy facilities is also creating demand for retrofit cooling upgrades.

North America

North America is the largest regional market for data center cooling, consisting of approx. 35% of the market share in 2025, supported by the presence of leading hyperscale cloud providers and advanced digital infrastructure. The United States dominates regional demand due to large-scale investments in hyperscale campuses supporting AI, cloud computing, and enterprise digital services. The U.S. Department of Energy (DOE) announced a $40 million funding program to support 15 innovative projects focused on developing advanced, energy-efficient data center cooling technologies. Data centers account for about 2% of total U.S. electricity consumption, with nearly 40% of that energy used for cooling, making thermal management a critical efficiency target. The region hosts some of the world’s highest data center concentrations, particularly in states such as Virginia, Texas, and California. Rising rack densities and GPU-intensive workloads are accelerating the transition toward liquid cooling technologies. Additionally, strong regulatory focus on energy efficiency and carbon neutrality is encouraging operators to optimize Power Usage Effectiveness (PUE). Canada is also emerging as a preferred location due to its cooler climate and renewable energy availability, further supporting advanced cooling deployments.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is experiencing gradual but steady growth in the data center cooling market as digital infrastructure expands. In Latin America, countries such as Brazil and Mexico are attracting colocation and cloud investments to support rising internet and enterprise adoption. The Middle East, particularly the UAE and Saudi Arabia, is investing heavily in smart city programs and hyperscale data center projects aligned with national digital transformation strategies. In Africa, countries such as South Africa and Kenya are emerging as regional data hubs, supported by improving connectivity and foreign investment. While infrastructure maturity varies across these regions, growing cloud penetration, government initiatives, and rising data consumption are expected to accelerate cooling system adoption in the coming years.

Competitive Landscape / Company Insights

The global data center cooling market is moderately consolidated in nature. A limited number of large, established companies account for a significant share of total market revenue due to their strong technological capabilities, global service networks, and ability to execute large-scale hyperscale and colocation projects. The market requires high capital investment, advanced engineering expertise, and strict reliability standards, which create substantial entry barriers for new participants. Additionally, rapid innovation in areas such as liquid cooling, immersion cooling, and AI-enabled thermal optimization has allowed niche technology providers to enter the market and gain traction, especially in high-density AI-focused facilities. However, scaling globally, securing large enterprise contracts, and meeting strict compliance standards remain challenging for new entrants.

Mini Profiles

Vertiv Group Corp. is a global provider of critical digital infrastructure solutions, offering precision air conditioning, chilled water systems, and advanced liquid cooling technologies for hyperscale, colocation, and enterprise data centers worldwide.

Schneider Electric SE delivers integrated data center cooling and energy management solutions through its Eco Structure platform, focusing on modular, energy-efficient, and AI-enabled thermal management systems.

Daikin Industries, Ltd. manufactures advanced HVAC and refrigeration technologies, supplying high-efficiency cooling systems tailored for large-scale data center applications globally.

Johnson Controls International plc provides YORK® chillers and precision cooling solutions, supporting mission-critical data centers with energy-optimized and sustainable HVAC infrastructure.

STULZ GmbH specializes in precision air conditioning, in-row cooling, and modular data center cooling systems designed for high-density and scalable environments.

Munters Group AB offers energy-efficient air treatment and evaporative cooling systems, enabling low-PUE operations for hyperscale and colocation data centers.

Rittal GmbH & Co. KG supplies enclosure-based cooling, liquid cooling packages, and modular data center infrastructure solutions for industrial and IT environments.

Key Players

- Vertiv Group Corp.

- Schneider Electric SE

- Daikin Industries, Ltd.

- Johnson Controls International plc

- STULZ GmbH

- Munters Group AB

- Rittal GmbH & Co. KG

- Alfa Laval AB

- Asetek A/S

- CoolIT Systems Inc.

- Airedale International Air Conditioning Ltd

- Submer Technologies SL

Recent Developments

February 2026 – Johnson Controls International plc announced the acquisition of a liquid cooling technology firm to strengthen its data center thermal management portfolio, enhancing its capabilities in direct-to-chip and high-density cooling solutions to address rising AI-driven workloads.

February 2026 – Trane Technologies plc entered into a definitive agreement to acquire a leading immersion cooling company, expanding its end-to-end thermal management solutions and reinforcing its position in next-generation liquid cooling infrastructure.

October 2025 – Schneider Electric SE introduced advanced AI-enabled cooling optimization upgrades within its Eco-Structure platform, enabling real-time monitoring, predictive maintenance, and improved energy efficiency for hyperscale data centers.

September 2025 – Vertiv Group Corp. launched a next-generation high-capacity liquid cooling system designed specifically for GPU-intensive AI data centers, supporting higher rack densities and improved power usage effectiveness (PUE).

July 2025 – Daikin Industries, Ltd. expanded its data center cooling product portfolio through strategic integration of modular and liquid cooling technologies, strengthening its global footprint in hyperscale and colocation facilities.

Global Data Center Cooling Market Coverage

Cooling Type Insight and Forecast 2026 - 2035

- Air-Based Cooling

- Liquid-Based Cooling

Component Insight and Forecast 2026 - 2035

- Solutions

- Services

Technology Insight and Forecast 2026 - 2035

- Free Cooling

- Evaporative Cooling

- Adiabatic Cooling

- Mechanical Refrigeration Cooling

- Hybrid Cooling Systems

- AI-Enabled Smart Cooling

Data Center Type Insight and Forecast 2026 - 2035

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Edge Data Centers

Industry Vertical Insight and Forecast 2026 - 2035

- IT & Telecommunications

- BFSI

- Healthcare

- Government & Defense

- Retail & E-commerce

- Manufacturing

- Others

Global Data Center Cooling Market by Region

- North America

- By Cooling Type

- By Component

- By Technology

- By Data Center Type

- By Industry Vertical

- By Country - U.S., Canada, Mexico

- Europe

- By Cooling Type

- By Component

- By Technology

- By Data Center Type

- By Industry Vertical

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Cooling Type

- By Component

- By Technology

- By Data Center Type

- By Industry Vertical

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Cooling Type

- By Component

- By Technology

- By Data Center Type

- By Industry Vertical

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Data Center Cooling Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Cooling Type

1.2.2. By

Component

1.2.3. By

Technology

1.2.4. By

Data Center Type

1.2.5. By

Industry Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Cooling Type

5.1.1. Air-Based Cooling

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Liquid-Based Cooling

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Component

5.2.1. Solutions

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Services

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Free Cooling

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Evaporative Cooling

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Adiabatic Cooling

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Mechanical Refrigeration Cooling

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Hybrid Cooling Systems

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. AI-Enabled Smart Cooling

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.4. By Data Center Type

5.4.1. Hyperscale Data Centers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Colocation Data Centers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Enterprise Data Centers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Edge Data Centers

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Industry Vertical

5.5.1. IT & Telecommunications

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. BFSI

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Healthcare

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Government & Defense

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Retail & E-commerce

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Manufacturing

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.5.7. Others

5.5.7.1. Market Definition

5.5.7.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Cooling Type

6.2. By

Component

6.3. By

Technology

6.4. By

Data Center Type

6.5. By

Industry Vertical

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Cooling Type

7.2. By

Component

7.3. By

Technology

7.4. By

Data Center Type

7.5. By

Industry Vertical

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Cooling Type

8.2. By

Component

8.3. By

Technology

8.4. By

Data Center Type

8.5. By

Industry Vertical

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Cooling Type

9.2. By

Component

9.3. By

Technology

9.4. By

Data Center Type

9.5. By

Industry Vertical

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Vertiv Group Corp.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Schneider Electric SE

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Daikin Industries, Ltd.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Johnson Controls International plc

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

STULZ GmbH

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Munters Group AB

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Rittal GmbH & Co. KG

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Alfa Laval AB

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Asetek A/S

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

CoolIT Systems Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Airedale International Air Conditioning Ltd

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Submer Technologies SL

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Data Center Cooling Market